Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

StoneX Group Inc. (NASDAQ:SNEX) reported mixed financial results for its fiscal third quarter of 2025, with strong revenue growth offset by a slight decline in earnings per share. The company also announced the completion of two significant acquisitions that position it for future growth. The financial services firm held its earnings call on August 6, 2025, detailing its performance and strategic initiatives.

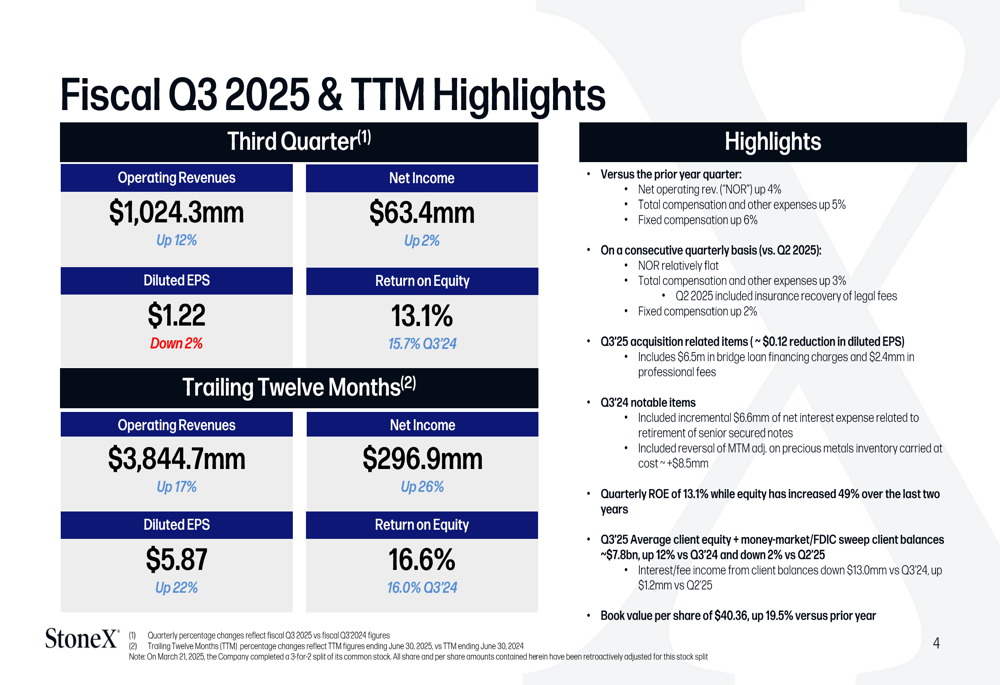

Quarterly Performance Highlights

StoneX reported operating revenues of $1,024.3 million for the third quarter of 2025, representing a 12% increase compared to the same period last year. Net income rose 2% to $63.4 million, while diluted earnings per share (EPS) declined slightly by 2% to $1.22. The company’s return on equity (ROE) for the quarter was 13.1%, down from 15.7% in Q3 2024.

For the trailing twelve months (TTM), StoneX demonstrated stronger performance across all key metrics, with operating revenues of $3,844.7 million (up 17%), net income of $296.9 million (up 26%), and diluted EPS of $5.87 (up 22%). The TTM return on equity improved to 16.6% from 16.0% in the prior year period.

As shown in the following financial highlights slide:

The company’s book value per share reached $40.36, representing a 19.5% increase compared to the prior year. This growth in book value reflects StoneX’s continued focus on building shareholder equity despite the quarterly EPS decline.

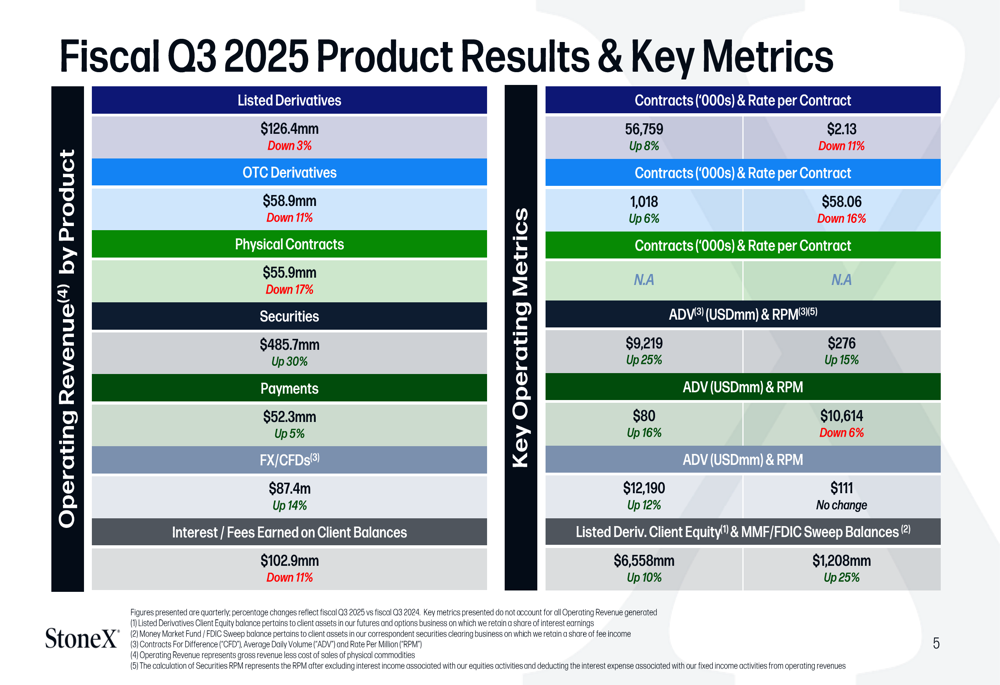

Product and Segment Performance

StoneX’s product performance showed significant variation across its business lines. Securities was the standout performer with a 30% increase in operating revenue to $485.7 million. FX/CFDs also performed well, growing 14% to $87.4 million. However, these gains were partially offset by declines in Physical Contracts (down 17% to $55.9 million), OTC Derivatives (down 11% to $58.9 million), and Listed Derivatives (down 3% to $126.4 million).

The following slide details the company’s product results and key operating metrics:

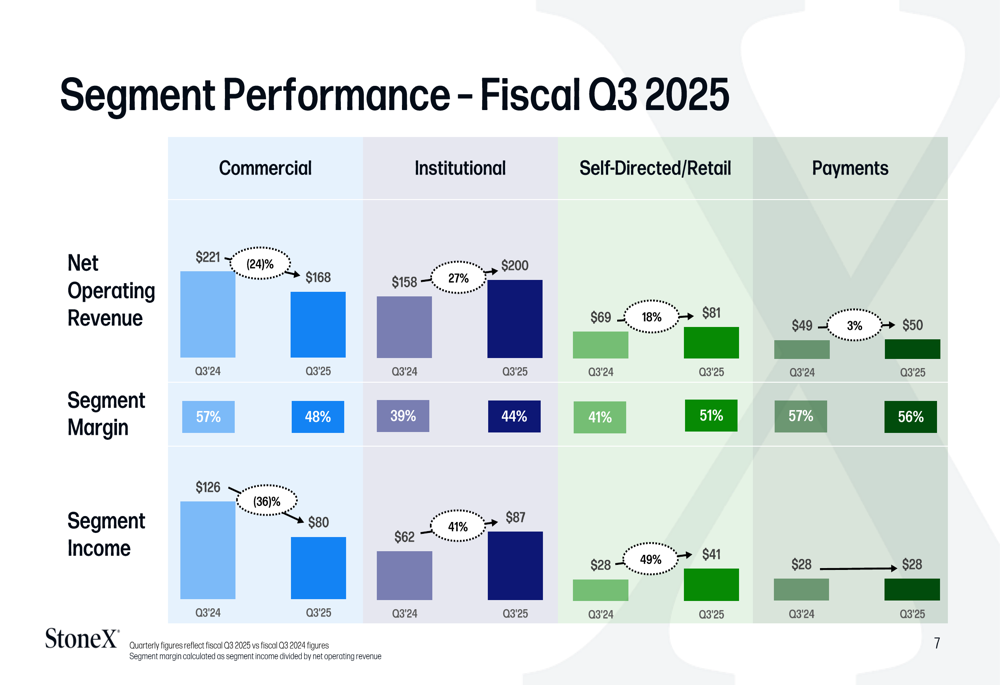

Segment performance revealed divergent trends across StoneX’s business units. The Institutional segment showed strong growth with a 27% increase in net operating revenue to $200 million and a 41% increase in segment income to $87 million. Similarly, the Self-Directed/Retail segment grew by 18% in net operating revenue. However, the Commercial segment experienced a significant decline, with net operating revenue decreasing by 24% to $168 million and segment income falling by 36% to $80 million.

The segment performance breakdown is illustrated in this slide:

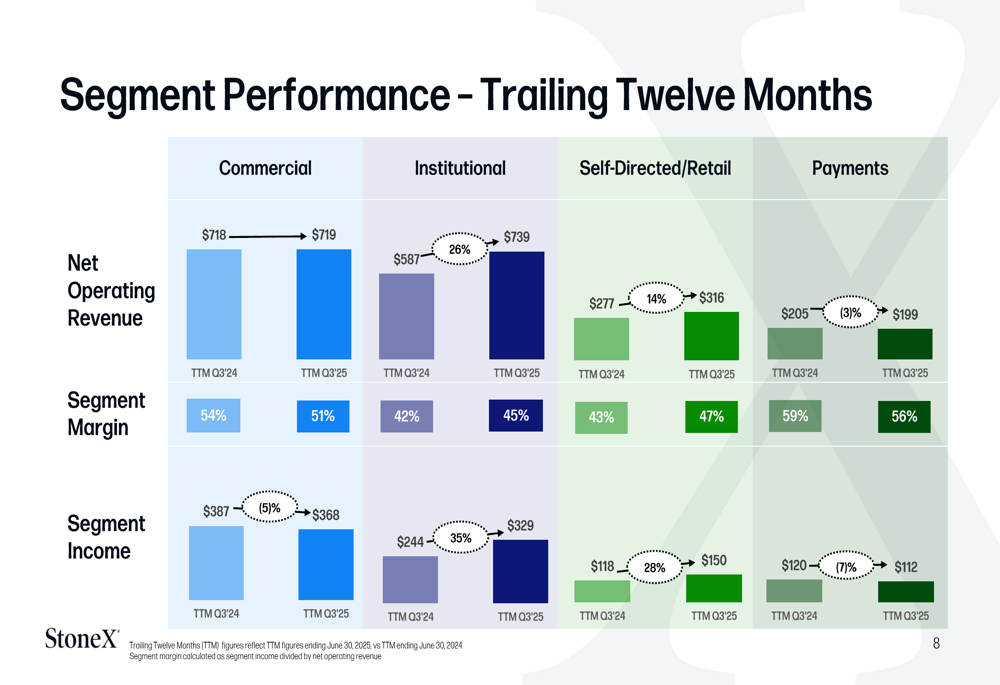

Looking at the trailing twelve months, the company’s segment performance showed more balanced results, with the Institutional segment leading growth at 26% in net operating revenue, while the Commercial segment remained essentially flat year-over-year.

Strategic Acquisitions

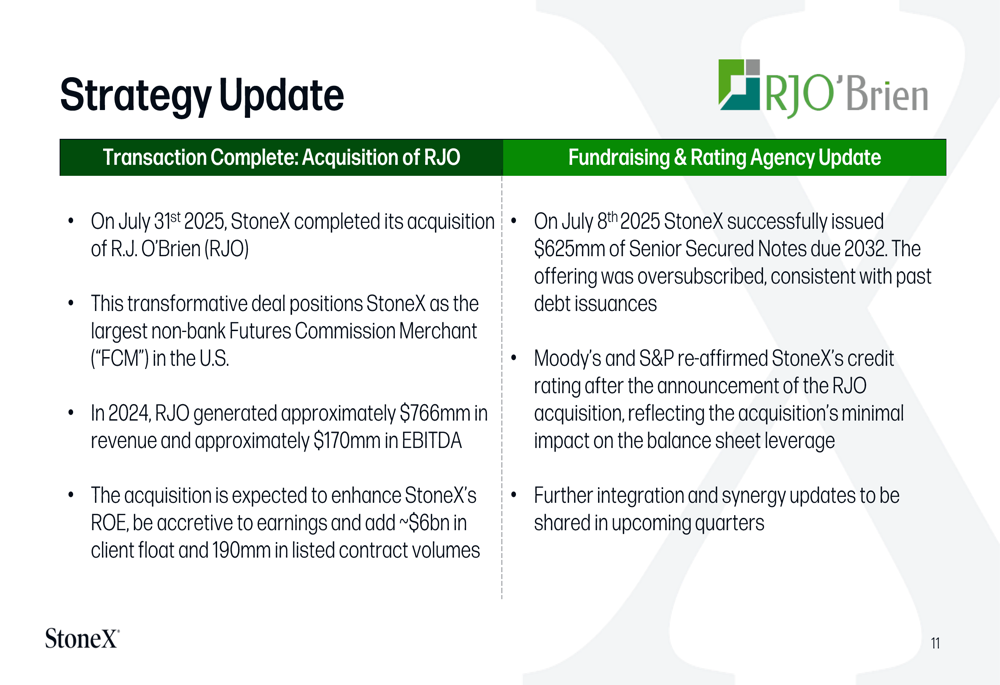

A major highlight of StoneX’s presentation was the announcement of two strategic acquisitions that closed on July 31, 2025. The company completed the acquisition of R.J. O’Brien (RJO), positioning StoneX as the largest non-bank futures commission merchant (FCM) in the United States. In 2024, RJO generated approximately $766 million in revenue and $170 million in EBITDA. The acquisition is expected to enhance StoneX’s return on equity and add approximately $6 billion in client float and 190 million in listed contract volumes.

To support this acquisition, StoneX successfully issued $625 million of Senior Secured Notes due 2032, with credit rating agencies Moody’s and S&P reaffirming the company’s credit rating.

The details of the RJO acquisition are shown in this slide:

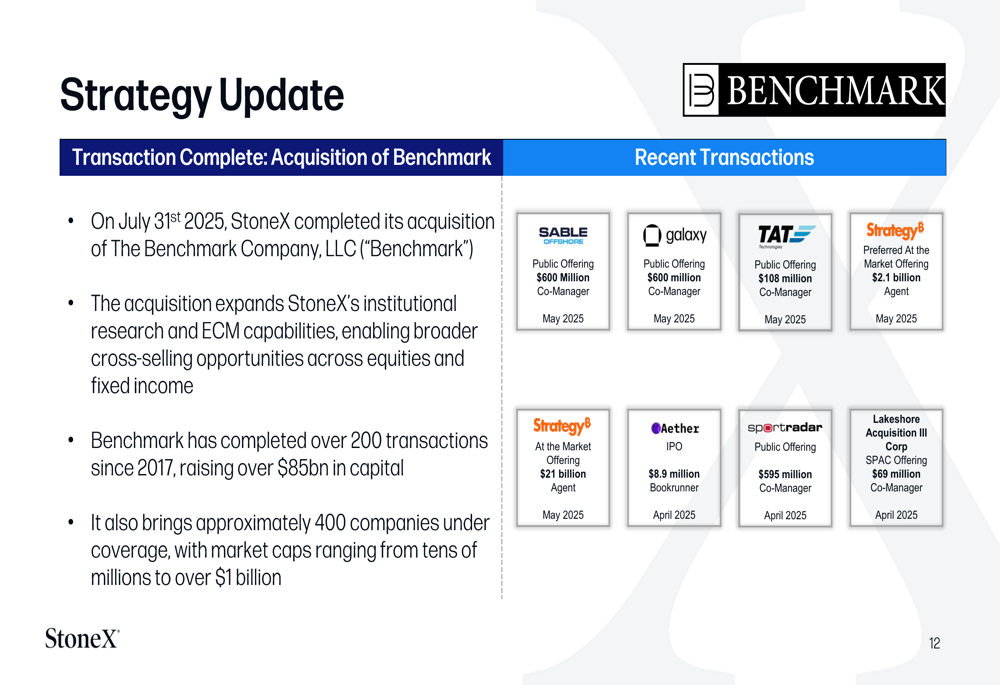

Simultaneously, StoneX completed the acquisition of The Benchmark Company, LLC, expanding its institutional research and equity capital markets (ECM) capabilities. Benchmark has completed over 200 transactions since 2017, raising over $85 billion in capital. The acquisition brings approximately 400 companies under coverage, with market capitalizations ranging from tens of millions to over $1 billion.

The Benchmark acquisition details are presented here:

Custody and Clearing Strategy

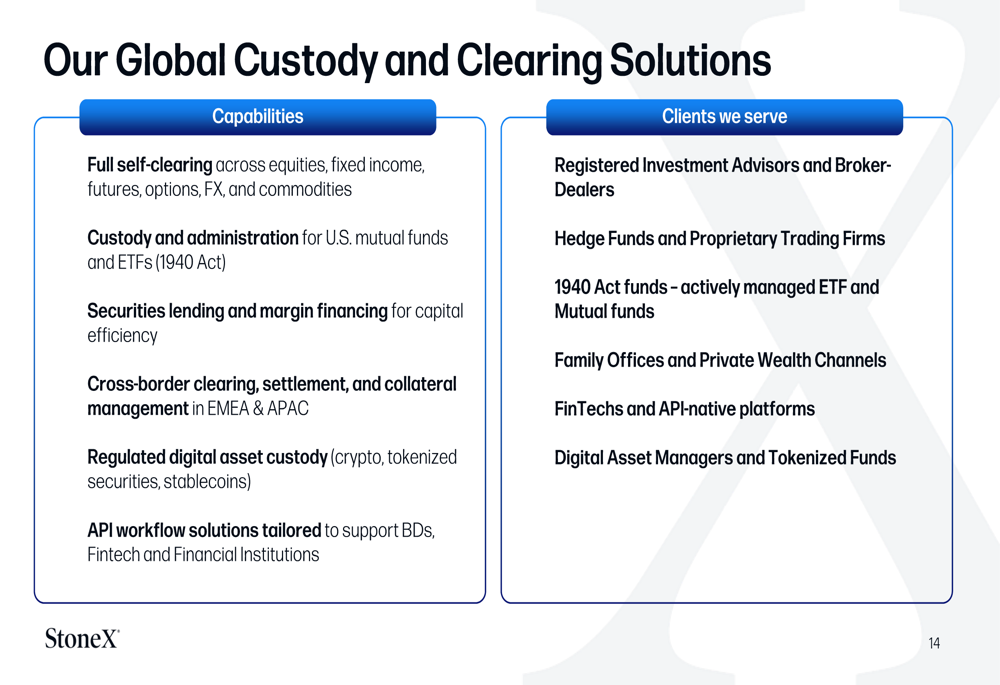

StoneX highlighted its global custody and clearing solutions as a key differentiator in the market. The company offers full self-clearing across multiple asset classes, including equities, fixed income, futures, options, FX, commodities, and regulated digital assets. Its target clients include registered investment advisors, broker-dealers, hedge funds, proprietary trading firms, family offices, and digital asset managers.

The company’s custody and clearing capabilities are outlined in this slide:

StoneX emphasized its unique position as a leading non-bank financial services firm serving mid-tier institutions, with global multi-custody reach and an institutional approach to risk management. The company’s strategic objectives for its custody and clearing business focus on building its ecosystem, growing and diversifying its client base, and digitizing its business.

Interest Rate Sensitivity and Outlook

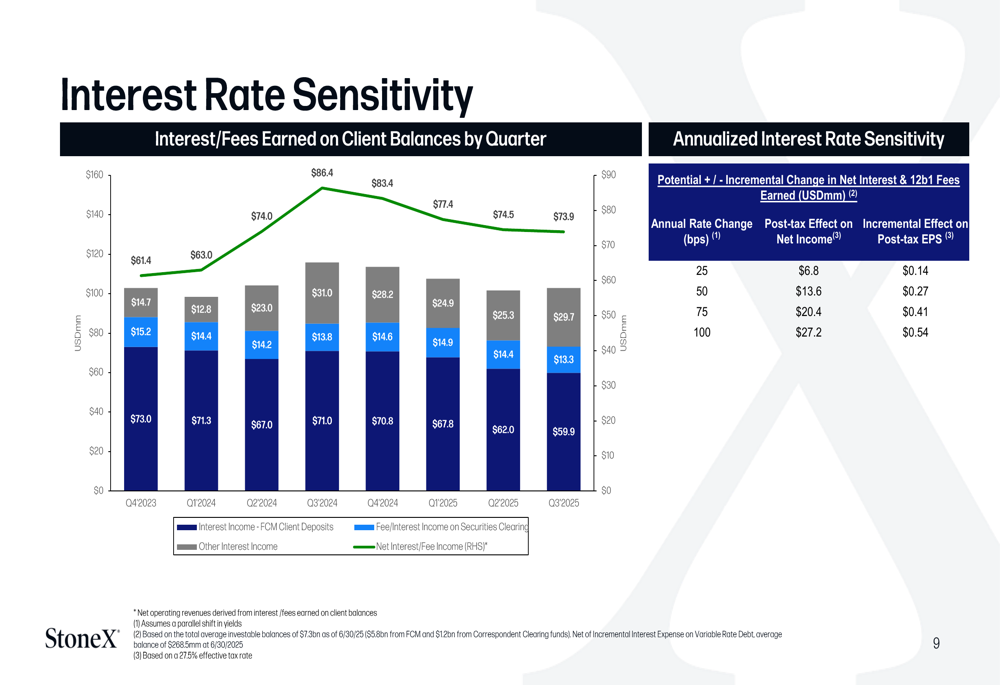

StoneX provided an analysis of its interest rate sensitivity, indicating that a 25 basis point increase in interest rates would result in a $6.8 million post-tax effect on net income, equivalent to $0.14 in EPS. A 100 basis point increase would generate a $27.2 million post-tax effect, or $0.54 in EPS.

In its closing remarks, StoneX reiterated its quarterly performance metrics and highlighted the strategic importance of its recent acquisitions. The company’s book value per share increased by $6.59, or 20% versus the prior year, reflecting continued growth in shareholder equity despite the quarterly EPS decline.

Market Context

StoneX’s stock closed at $96.96 on August 5, 2025, according to available market data, representing a 1.29% decline for the day. The stock has been trading near its 52-week high of $100.40, significantly above its 52-week low of $49.70, indicating strong overall market performance despite the mixed quarterly results.

This performance follows the company’s Q2 2025 results, which showed an EPS beat of $1.41 against a forecast of $1.34, despite revenue falling short of expectations. The completion of the previously announced strategic acquisitions suggests StoneX is executing on the growth strategy outlined in previous earnings calls.

The company’s focus on expanding its institutional capabilities through acquisitions, combined with its emphasis on custody and clearing solutions, positions StoneX to capitalize on market opportunities while navigating the challenges in its Commercial segment. Investors will likely be watching closely to see how the integration of RJO and Benchmark impacts the company’s performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.