Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

Strauss Group (TASE:STRS) presented its Q1 2025 financial results on May 28, 2025, showing strong sales growth across all segments while facing significant margin pressure from commodity inflation. The company’s stock was down 1.83% on the day of the presentation, with shares trading at NIS 8,774, well above the 52-week low of NIS 5,366 but below the 52-week high of NIS 9,092.

The quarter was marked by substantial increases in key commodity prices, with cocoa prices up 269%, Arabica coffee up 212%, and Robusta coffee up 311% from their 2020 levels. These dramatic price increases created significant headwinds for the company’s profitability despite robust top-line growth.

Quarterly Performance Highlights

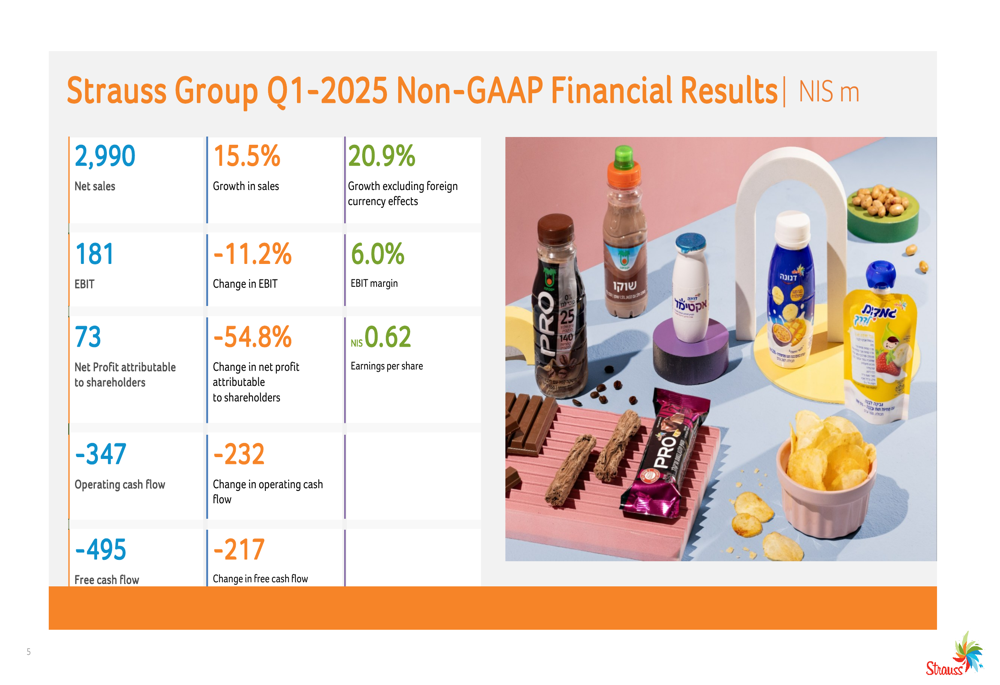

Strauss Group reported Q1 2025 net sales of NIS 2,990 million, representing 15.5% growth year-over-year, or 20.9% growth excluding foreign currency effects. However, EBIT declined 11.2% to NIS 181 million, with EBIT margin contracting to 6.0% from 7.8% in Q1 2024. Net profit attributable to shareholders fell 54.8% to NIS 73 million.

As shown in the following comprehensive financial summary:

The company noted that its results were significantly impacted by a NIS 49 million non-recurring loss on cocoa derivatives. Excluding this loss, EBIT would have reached NIS 230 million, reflecting a 7.7% margin.

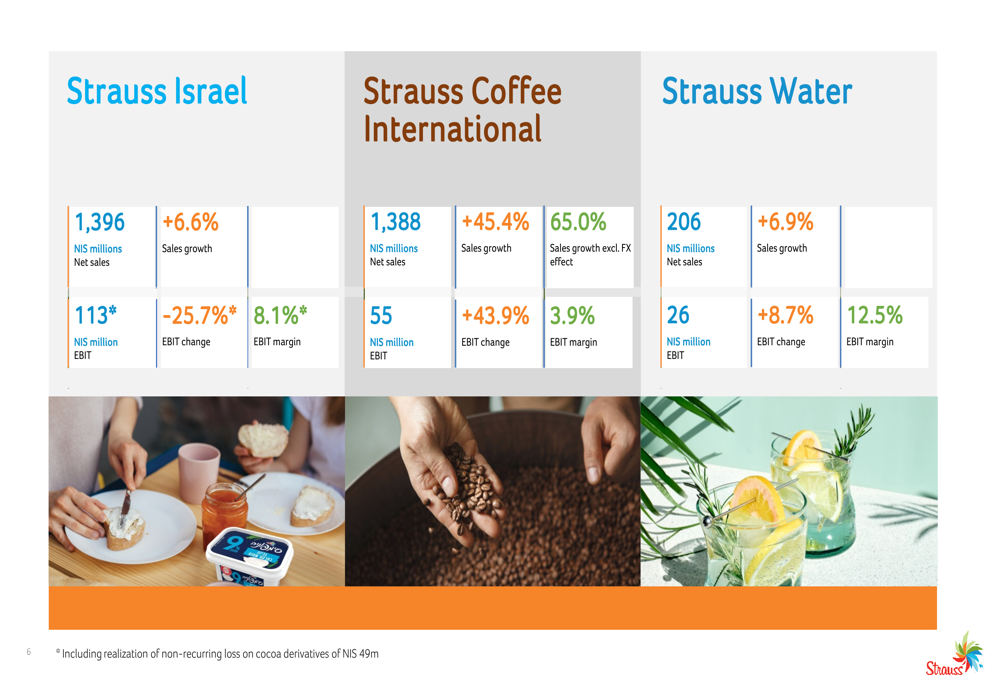

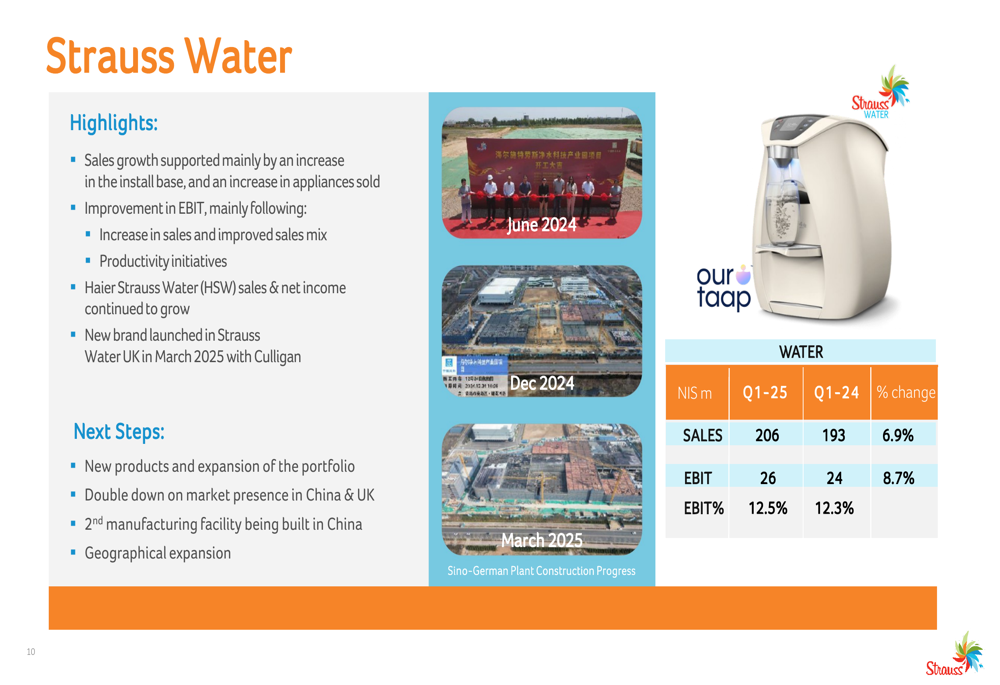

All three main business segments showed sales growth, though with varying profitability impacts. Strauss Israel reported 6.6% sales growth but a 25.7% EBIT decline. Coffee International demonstrated strong performance with 45.4% sales growth (65.0% excluding FX effects) and 43.9% EBIT growth. Strauss Water continued its steady performance with 6.9% sales growth and 8.7% EBIT growth.

The segment breakdown illustrates these varying performances:

Detailed Financial Analysis

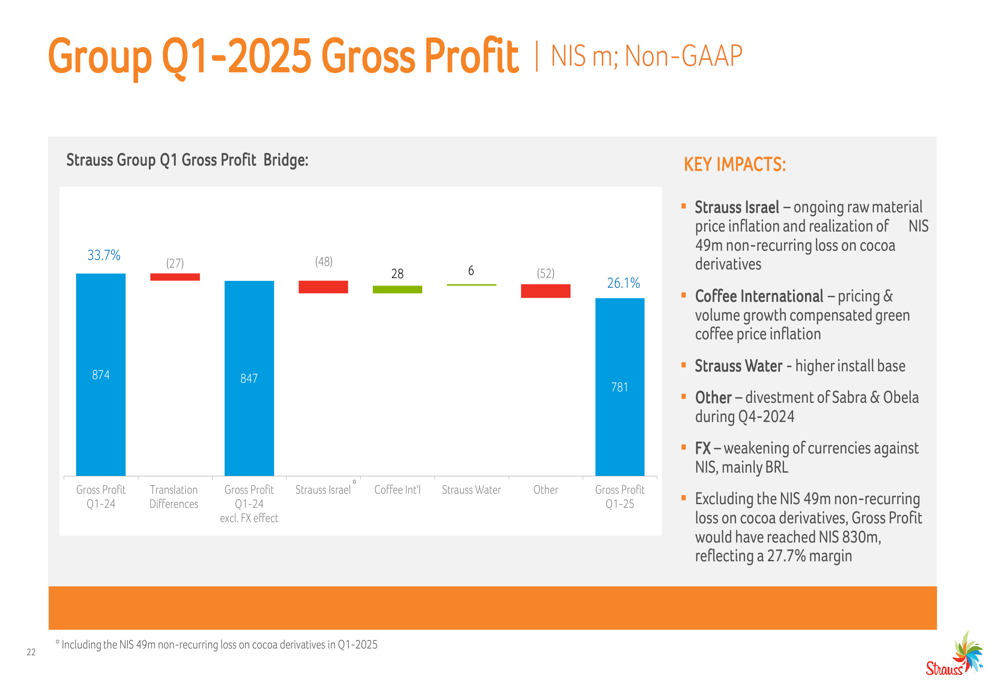

The company’s gross profit declined 10.6% to NIS 781 million, with gross margin contracting to 26.1% from 33.7% in Q1 2024. This decline primarily reflects ongoing raw material price inflation, the sale of Sabra & Obela in Q4 2024, and the realization of the non-recurring loss on cocoa derivatives.

The following bridge analysis illustrates the key factors affecting the company’s gross profit:

Operating cash flow was negative NIS 347 million, compared to negative NIS 115 million in Q1 2024, while free cash flow deteriorated to negative NIS 495 million from negative NIS 278 million. The company attributed this to increased working capital needs driven by raw material price inflation.

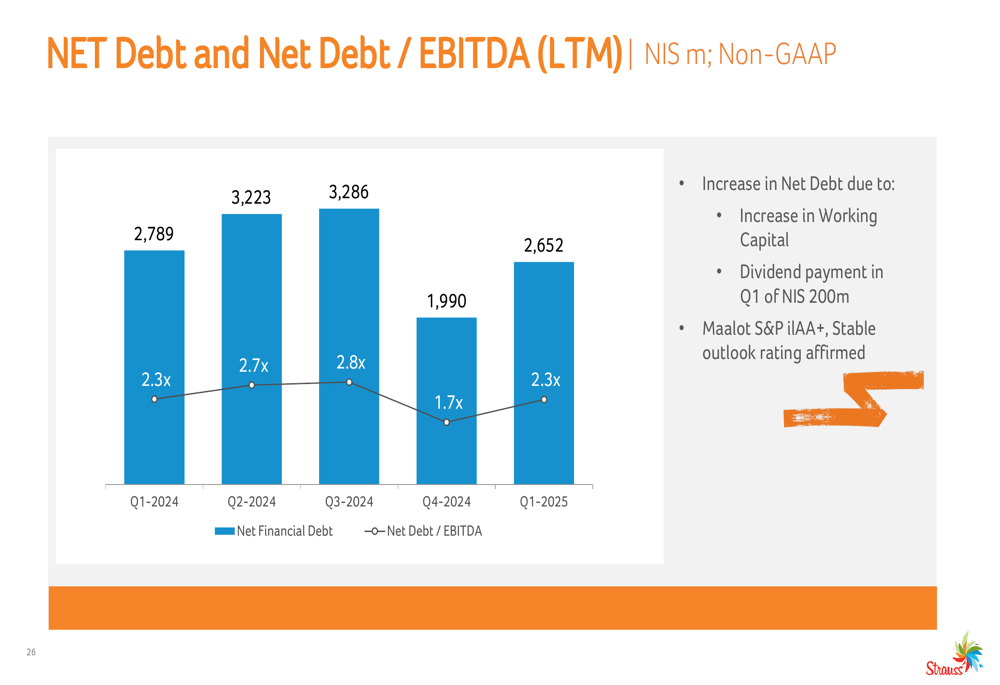

Net debt increased to NIS 2,652 million at the end of Q1 2025, with the net debt to EBITDA ratio at 2.3x, up from 1.7x at the end of Q4 2024 but unchanged from Q1 2024. The increase was primarily due to higher working capital needs and a NIS 200 million dividend payment during the quarter. Despite these increases, Maalot S&P affirmed the company’s ilAA+ rating with a stable outlook.

Segment Performance

Strauss Israel’s performance was significantly impacted by raw material inflation and the cocoa derivatives loss. The segment reported sales of NIS 1,396 million, up 6.6%, but EBIT declined 25.7% to NIS 113 million. Excluding the NIS 49 million non-recurring loss, EBIT would have increased by 6.7% with a margin of 11.6%.

Within Strauss Israel, Health & Wellness performed well with 11.9% EBIT margin, while Fun & Indulgence Snacks & Confectionery was heavily impacted by cocoa price inflation, reporting a negative 4.2% EBIT margin. Coffee Israel maintained a strong 15.7% EBIT margin despite green coffee price inflation.

Coffee International was a standout performer, with sales reaching NIS 1,388 million, up 45.4% (65.0% excluding FX effects). EBIT grew 43.9% to NIS 55 million, maintaining a stable margin of 3.9%. The strong performance was driven by volume growth in Brazil and Central Eastern Europe, price updates in response to green coffee inflation, and continued growth of non-R&G products in Brazil.

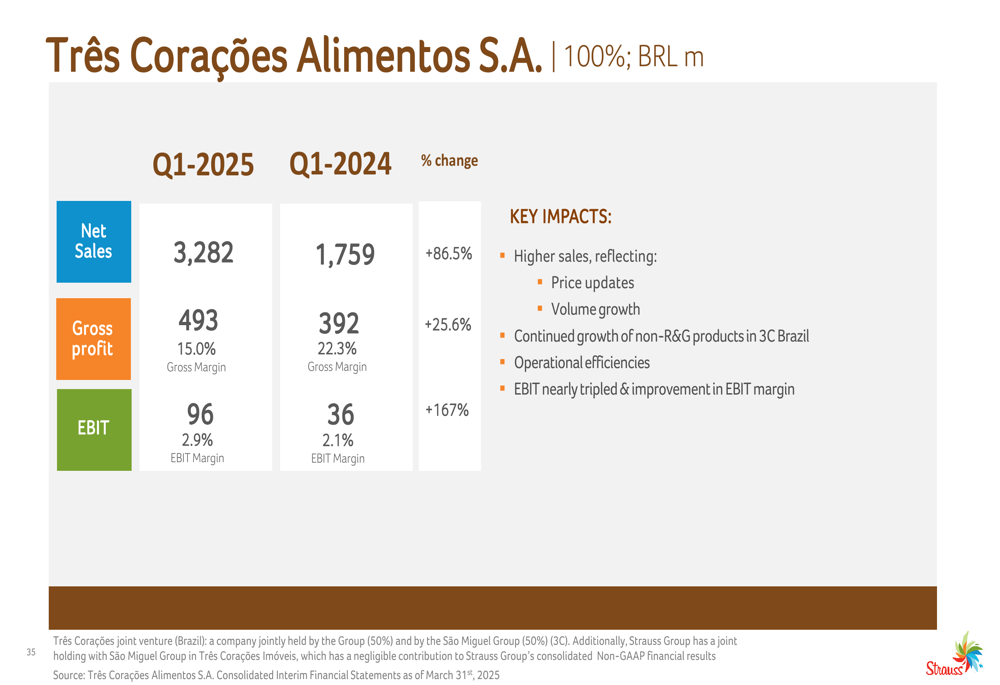

The Três Corações joint venture in Brazil performed exceptionally well, with sales in local currency up 86.5% to BRL 3,282 million and EBIT up 167% to BRL 96 million. This growth was driven by price updates, volume growth, and operational efficiencies.

Strauss Water continued its steady performance with sales up 6.9% to NIS 206 million and EBIT up 8.7% to NIS 26 million, maintaining a healthy 12.5% EBIT margin. Growth was supported by an increased install base and more appliances sold, along with an improved sales mix and productivity initiatives.

Strategic Initiatives

Strauss Group highlighted several strategic initiatives aimed at driving future growth and improving profitability. The company is focusing on consumer-centric food trends, with innovation in areas such as added-value functional nutrition, lifestyle diets, and heritage & nostalgia products.

A key strategic focus is the expansion of plant-based products, with a dedicated facility under construction expected to be completed by the end of 2025. The company is also building a new facility at Yotvata to increase growth, also scheduled for completion by the end of 2025.

In Brazil, the company is focusing on expanding non-Roast & Ground coffee categories to diversify its portfolio and capture growth opportunities. The company is also implementing a comprehensive productivity roadmap targeting NIS 300-400 million in run-rate savings by 2026.

As illustrated in the following productivity roadmap:

Forward-Looking Statements

Despite the current challenges from commodity inflation, Strauss Group maintains a positive long-term outlook. The company reaffirmed its 2026 targets, including 5% CAGR in top-line growth from 2024-2026, expanding EBIT margins to 10-12% by 2026, and enhancing cost structure productivity to achieve NIS 300-400 million in savings by 2026.

The company plans to invest in the future with CAPEX reaching 5-7% of sales during 2024-2026, while focusing on its core business, which is expected to represent 85% of total sales by 2026.

In summary, while Strauss Group faces significant near-term challenges from commodity inflation, particularly in cocoa and coffee, the company’s strong sales growth, strategic investments, and productivity initiatives position it well for long-term success. Management remains focused on executing its strategy to shape the company for future growth while returning capital to shareholders through dividends.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.