Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Super Micro Computer Inc. (NASDAQ:SMCI) presented its fiscal third quarter 2025 results on May 6, revealing a mixed financial performance while emphasizing its strategic focus on AI infrastructure and manufacturing expansion. The company reported year-over-year revenue growth but experienced sequential declines and margin pressure amid a challenging market environment.

The presentation comes as Super Micro continues to position itself as a leading provider of AI infrastructure solutions, with AI GPU platforms accounting for over 70% of its revenues according to the earnings call. Despite beating earnings expectations with a non-GAAP EPS of $0.31 versus the forecast of $0.30, the company’s revenue of $4.6 billion fell short of the expected $5.05 billion, resulting in a 4.77% decline in after-hours trading.

Quarterly Performance Highlights

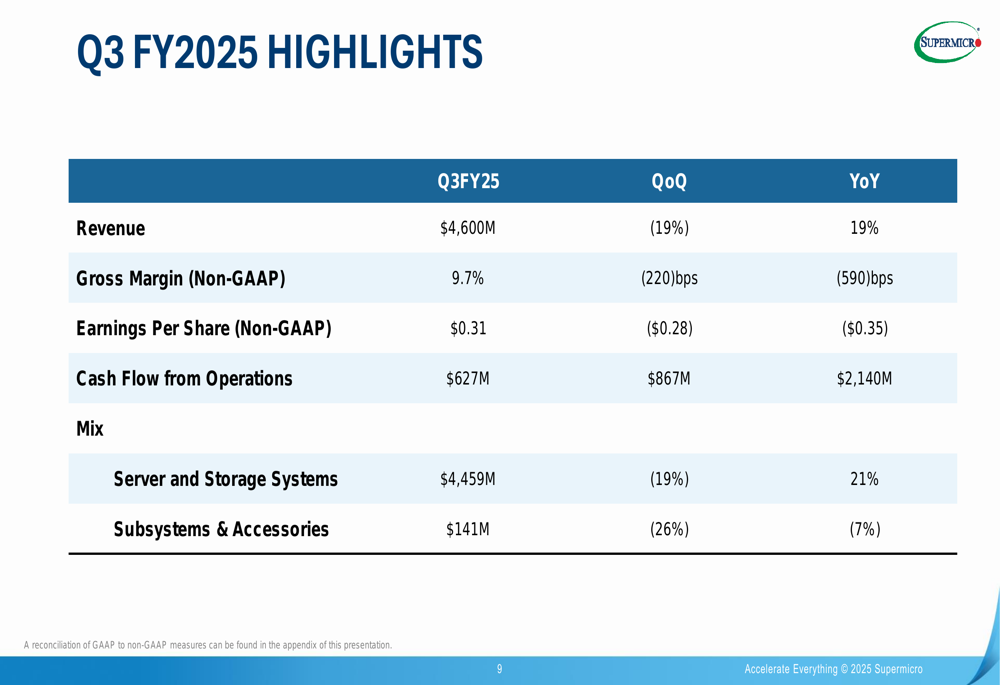

Super Micro reported revenue of $4.6 billion for Q3 FY2025, representing a 19% increase year-over-year but a 19% decrease quarter-over-quarter. The company’s non-GAAP gross margin stood at 9.7%, down 220 basis points sequentially and 590 basis points year-over-year, reflecting significant margin pressure.

As shown in the following financial highlights slide, non-GAAP earnings per share came in at $0.31, down from $0.59 in the same quarter last year and $0.59 in the previous quarter:

The company generated $627 million in cash flow from operations during the quarter, demonstrating its ability to maintain positive cash generation despite the challenging environment. Server and storage systems accounted for $4,459 million of total revenue (down 19% QoQ, up 21% YoY), while subsystems and accessories contributed $141 million (down 26% QoQ, down 7% YoY).

Strategic Initiatives

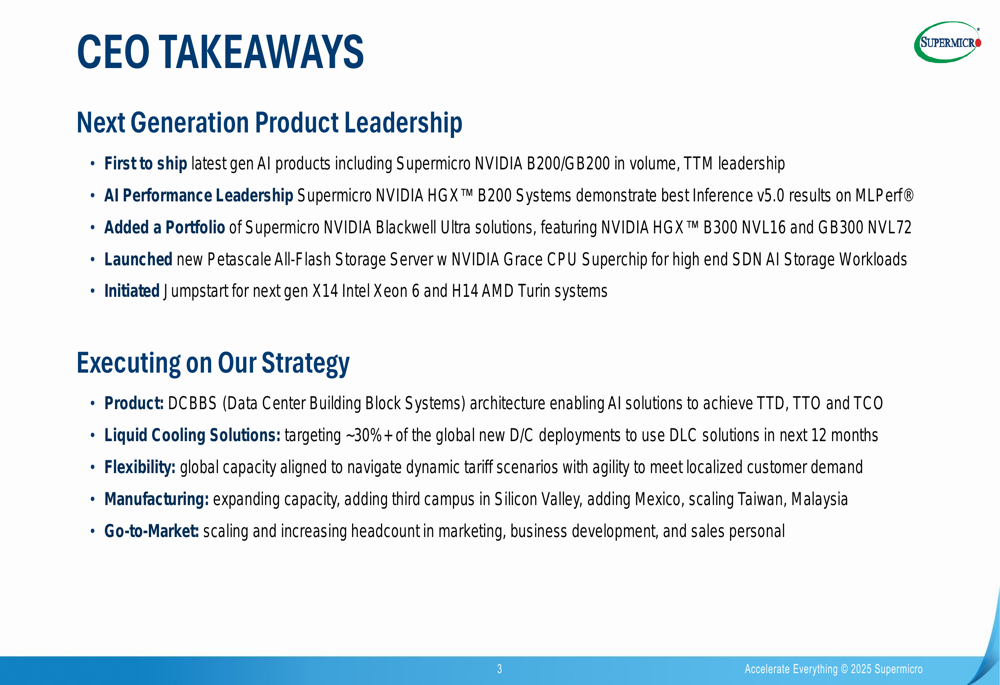

Super Micro’s presentation highlighted several key strategic initiatives centered around AI infrastructure leadership and manufacturing expansion. The company emphasized its first-to-market advantage with next-generation AI products, including being the first to ship the latest NVIDIA (NASDAQ:NVDA) B200/GB200 solutions.

The CEO’s key takeaways slide underscores the company’s focus on AI performance leadership and product innovation:

A significant portion of Super Micro’s strategy involves expanding its liquid cooling solutions, which the company expects to account for over 30% of new datacenter deployments. This focus aligns with the increasing power requirements of AI systems and the need for more efficient cooling solutions.

As illustrated in the following slide, Super Micro has achieved impressive production capacity with 5,000 racks per month, including 2,000+ direct liquid cooling (DLC) racks:

The company’s manufacturing expansion represents another key strategic initiative. Super Micro is enhancing its global footprint with facilities in Silicon Valley, APAC, and Malaysia to meet growing demand and optimize costs:

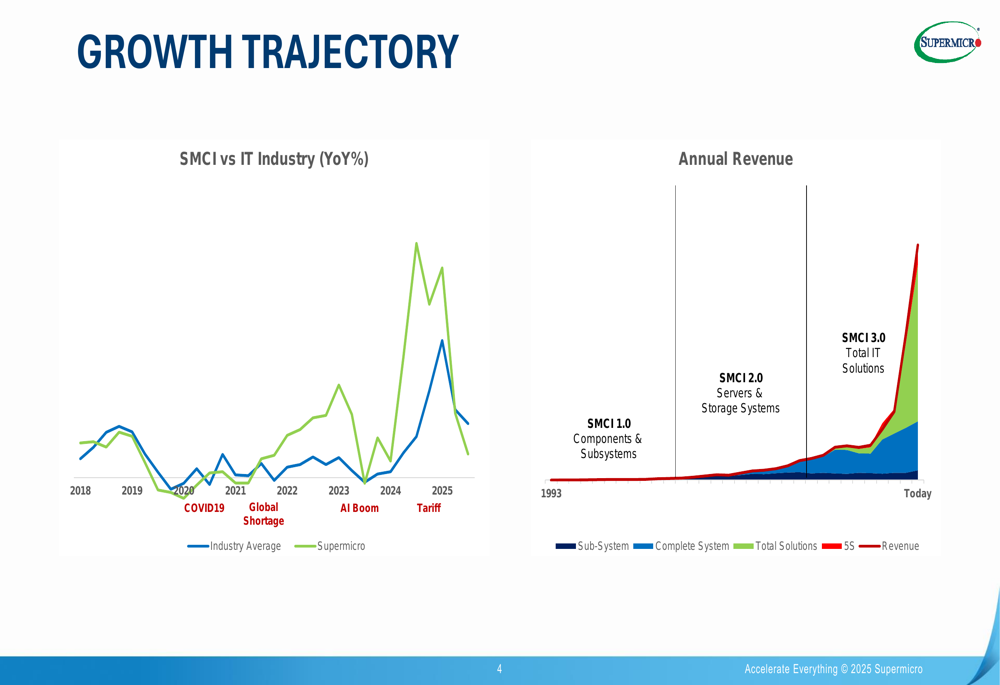

Super Micro’s growth trajectory compared to the broader IT industry demonstrates its successful evolution from a components provider to a total IT solutions company:

Forward-Looking Statements

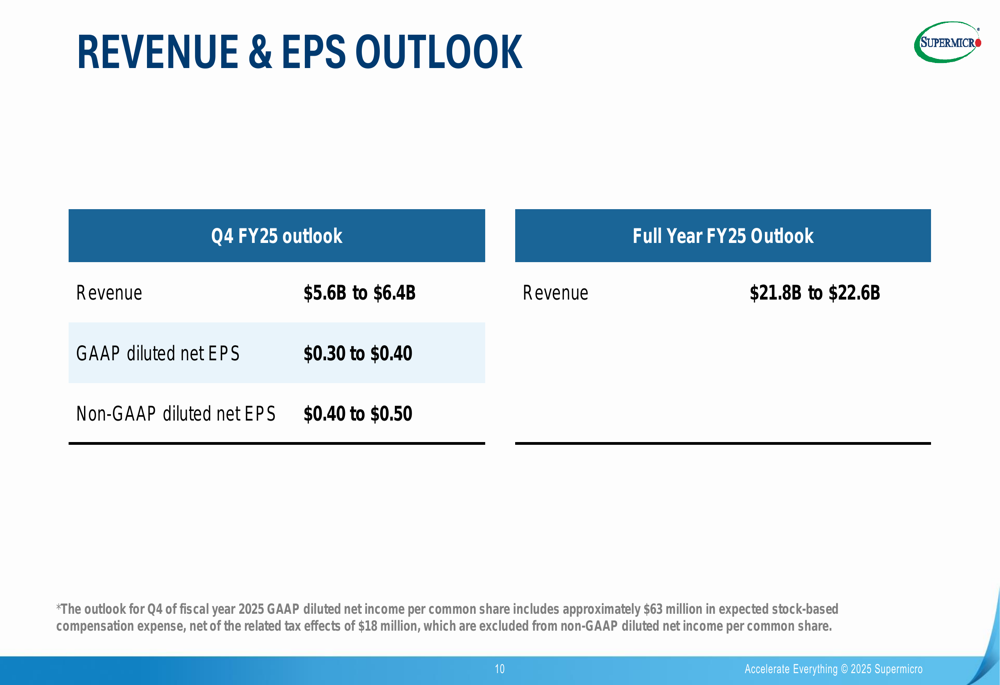

Looking ahead, Super Micro provided guidance for Q4 FY2025, projecting revenue between $5.6 billion and $6.4 billion, with non-GAAP diluted EPS expected to range from $0.40 to $0.50. For the full fiscal year 2025, the company anticipates revenue between $21.8 billion and $22.6 billion.

The following slide details the company’s revenue and EPS outlook:

During the earnings call, CEO Charles Liang expressed confidence in the company’s growth prospects, stating, "We remain very confident with our midterm and long-term growth." He also highlighted advancements in their liquid cooling technology, noting that their second-generation DLC is outperforming the first generation.

However, the company faces several challenges, including macroeconomic uncertainties, potential delays in customer decisions due to technology platform transitions, and tariff impacts that could affect cost structures and pricing. The revenue guidance for Q4 suggests a potential recovery from the Q3 slowdown, though market reception remains cautious as evidenced by the after-hours stock decline.

Super Micro’s emphasis on being a US-based manufacturer could provide advantages amid ongoing global supply chain challenges and increasing focus on domestic production of critical technologies. As the company continues to navigate the competitive AI infrastructure landscape, its ability to maintain technological leadership while addressing margin pressures will be crucial for long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.