JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Superior Industries International (NYSE:SUP), a leading manufacturer of aluminum wheels for light vehicles, presented its first quarter 2025 results on May 12, 2025, revealing a mixed financial performance. The company reported improved net loss figures and strong cash flow generation while suspending its full-year guidance amid ongoing market challenges and a potential recapitalization transaction.

The presentation comes as Superior’s stock faces significant pressure, with pre-market trading showing a decline of 48.08% to $1.49 per share, reflecting investor concerns despite management’s emphasis on strategic positioning and favorable tariff dynamics.

Quarterly Performance Highlights

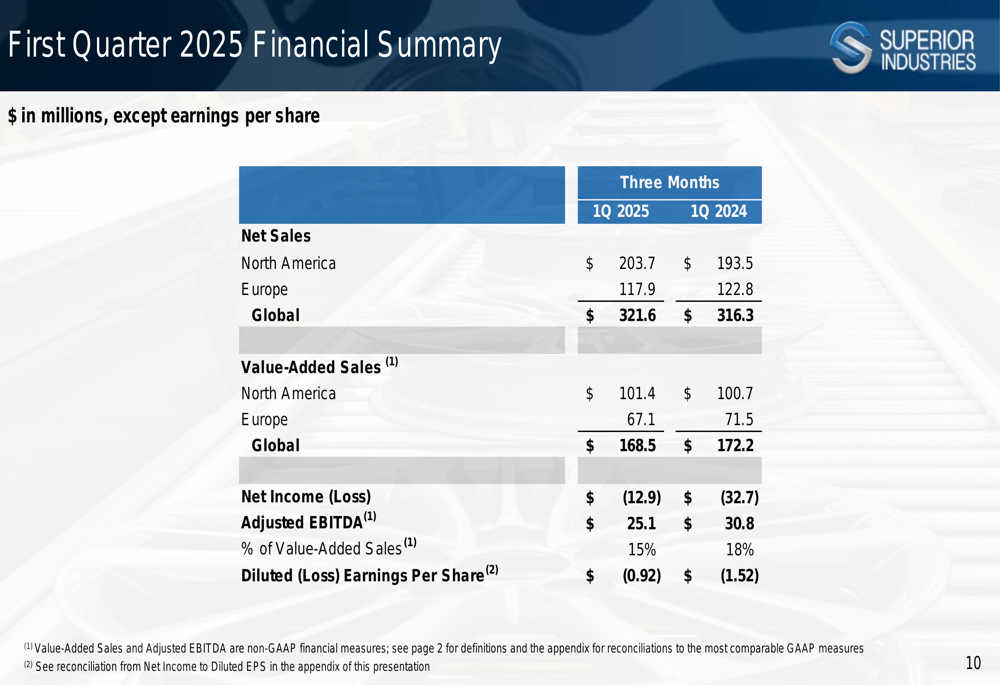

Superior reported Q1 2025 net sales of $321.6 million, a modest 2% increase from $316.3 million in the same period last year. However, value-added sales declined slightly to $168.5 million compared to $172.2 million in Q1 2024.

As shown in the following financial summary:

The company reduced its net loss to $12.9 million in Q1 2025, a significant improvement from the $32.7 million loss recorded in Q1 2024. Diluted loss per share improved to ($0.92) from ($1.52) in the prior year period. However, adjusted EBITDA declined to $25.1 million (15% of value-added sales) from $30.8 million (18% of value-added sales) in Q1 2024.

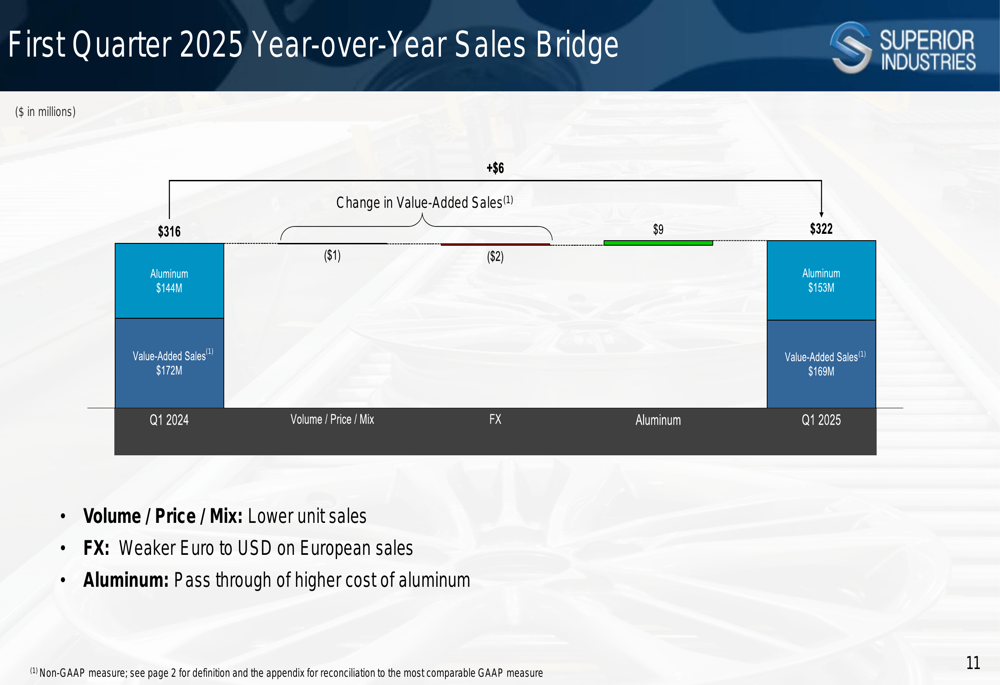

The year-over-year sales bridge reveals the factors affecting Superior’s revenue performance:

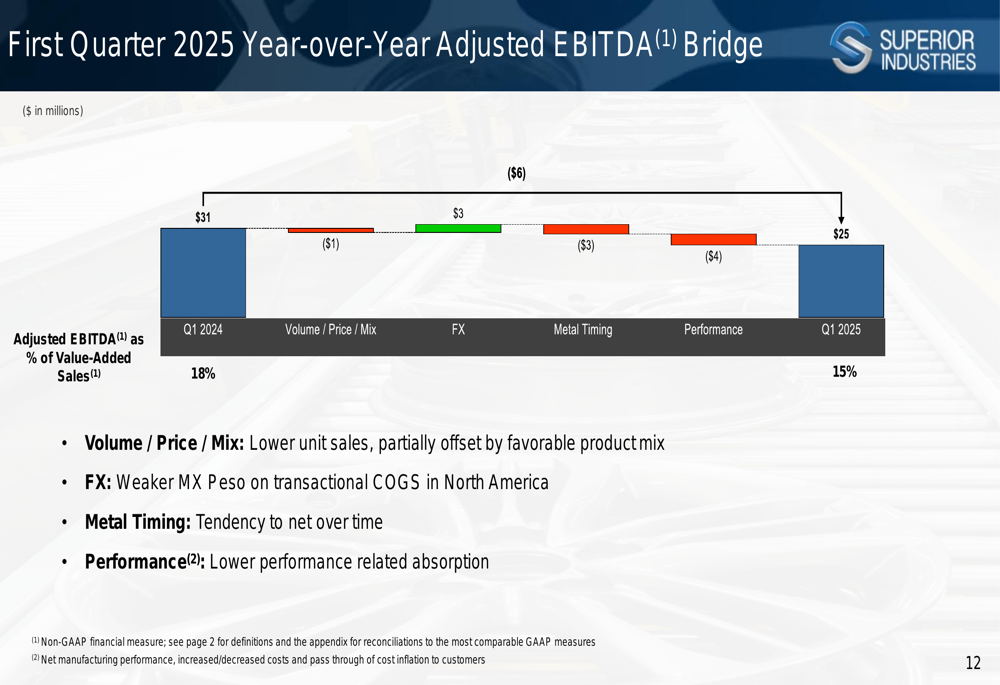

Similarly, the adjusted EBITDA bridge illustrates the pressures on profitability:

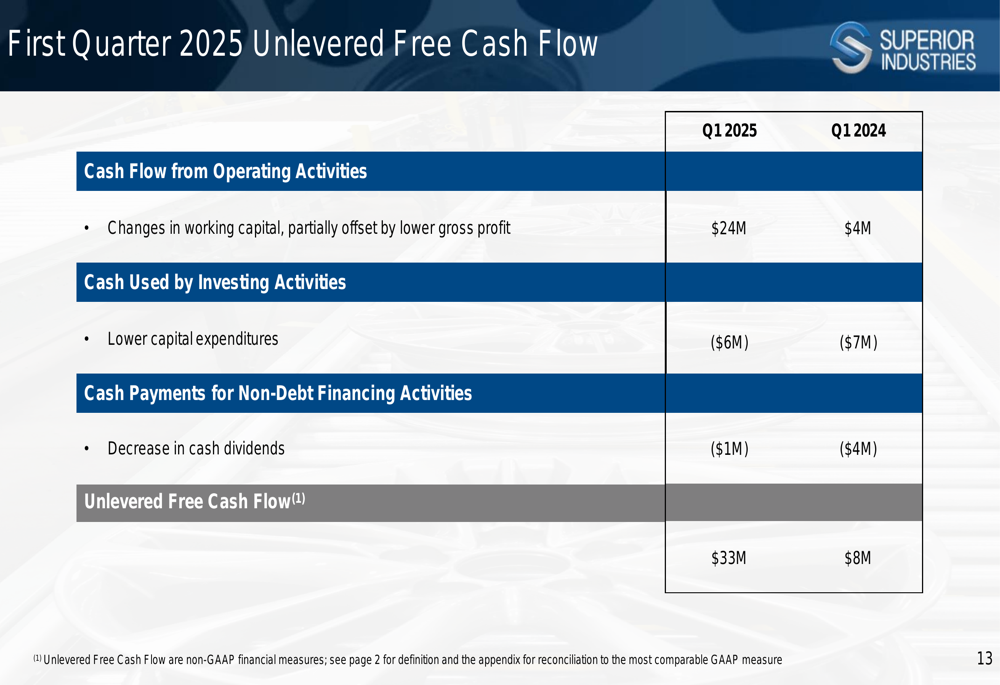

A notable bright spot was the company’s cash flow performance, with unlevered free cash flow increasing to $33 million in Q1 2025 from $8 million in the prior year period, driven primarily by improved operating cash flow.

Debt Reduction and Recapitalization Efforts

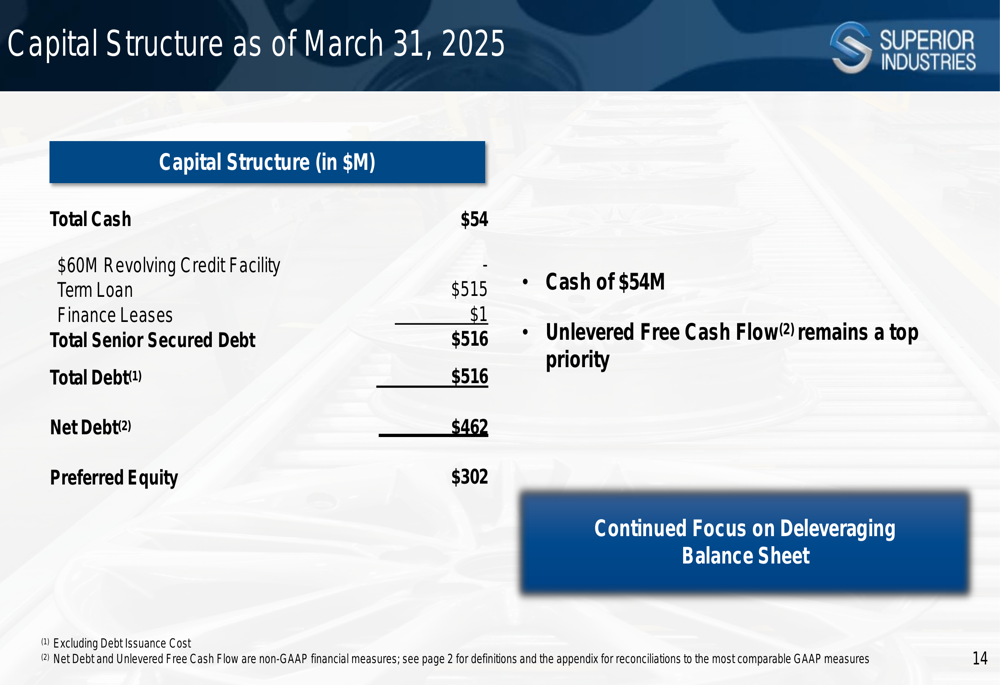

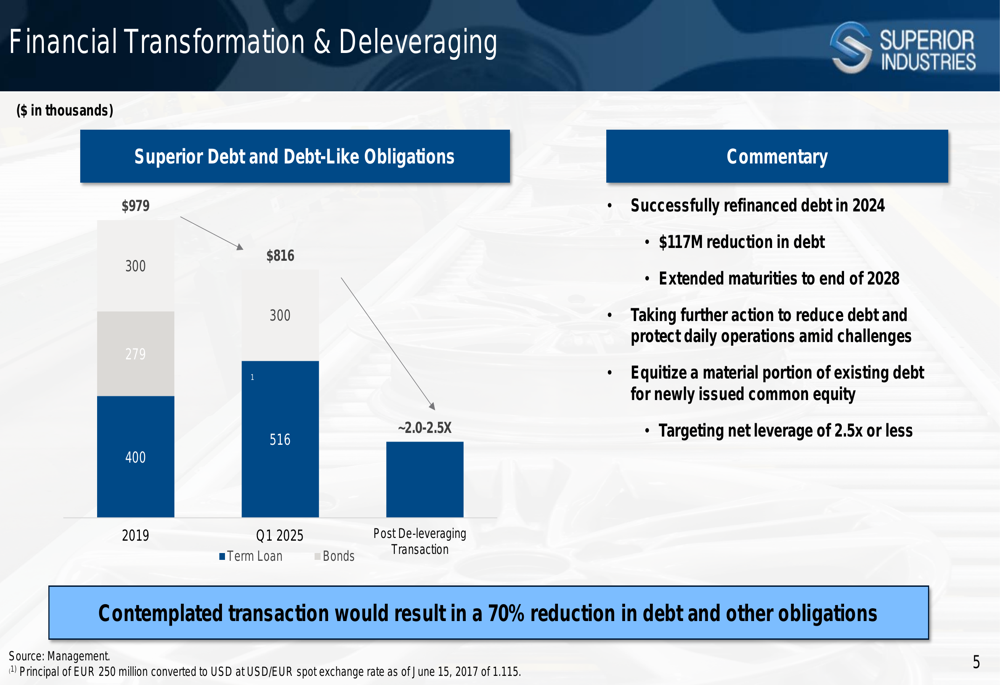

Superior continues to make progress on its debt reduction journey, decreasing total debt to $516 million as of March 31, 2025, down $113 million year-over-year. The company’s capital structure shows a cash position of $54 million and net debt of $462 million.

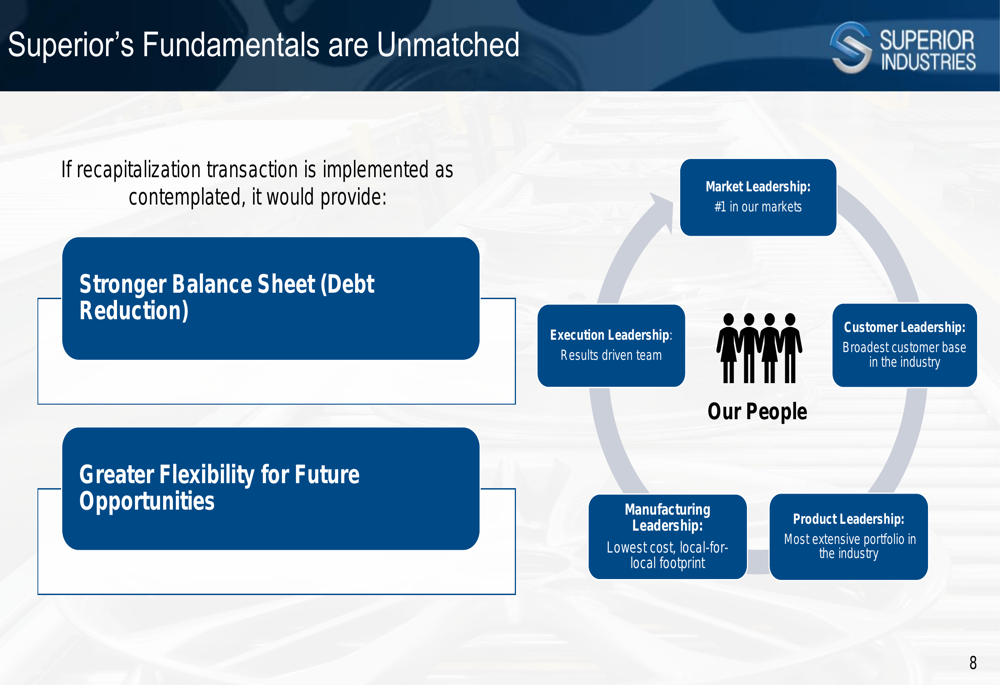

The company highlighted its financial transformation efforts, showing how debt has decreased from $979 million in 2019 to $816 million in Q1 2025, with plans to further reduce it to approximately $516 million through a deleveraging transaction. Management indicated they are in advanced discussions to recapitalize the balance sheet, targeting net leverage of 2.5x or less.

The debt maturity profile shows the bulk of Superior’s debt ($501 million) coming due in 2028, providing near-term breathing room as the company works through its recapitalization plans.

Tariff Dynamics and Market Opportunities

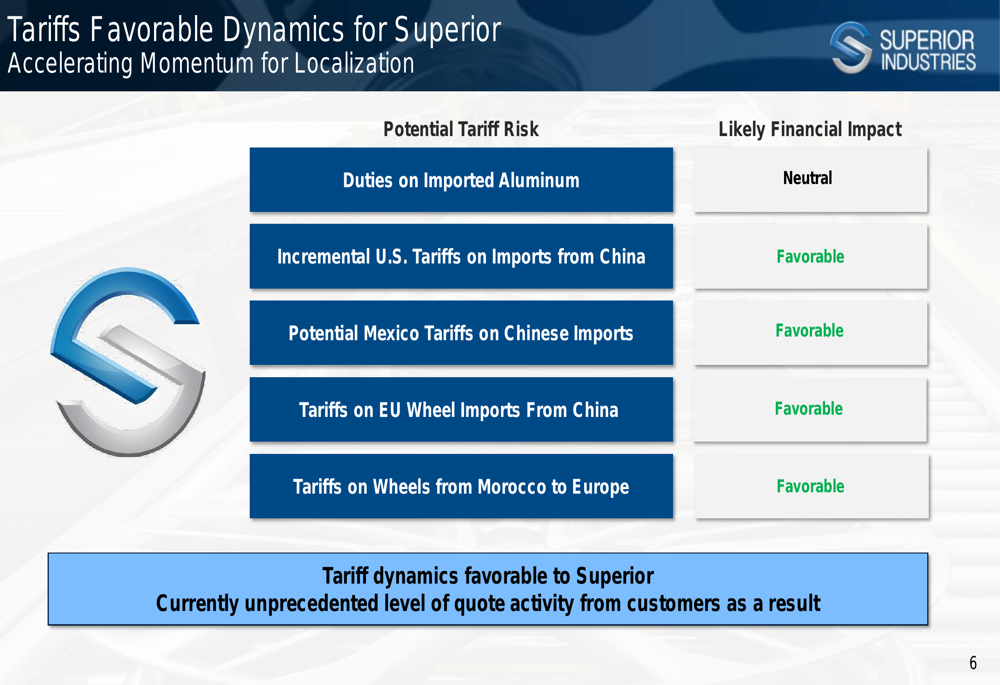

A key focus of Superior’s presentation was the favorable impact of various tariffs on the company’s competitive position. Management detailed how recent and potential tariff actions across multiple markets would benefit Superior’s manufacturing footprint.

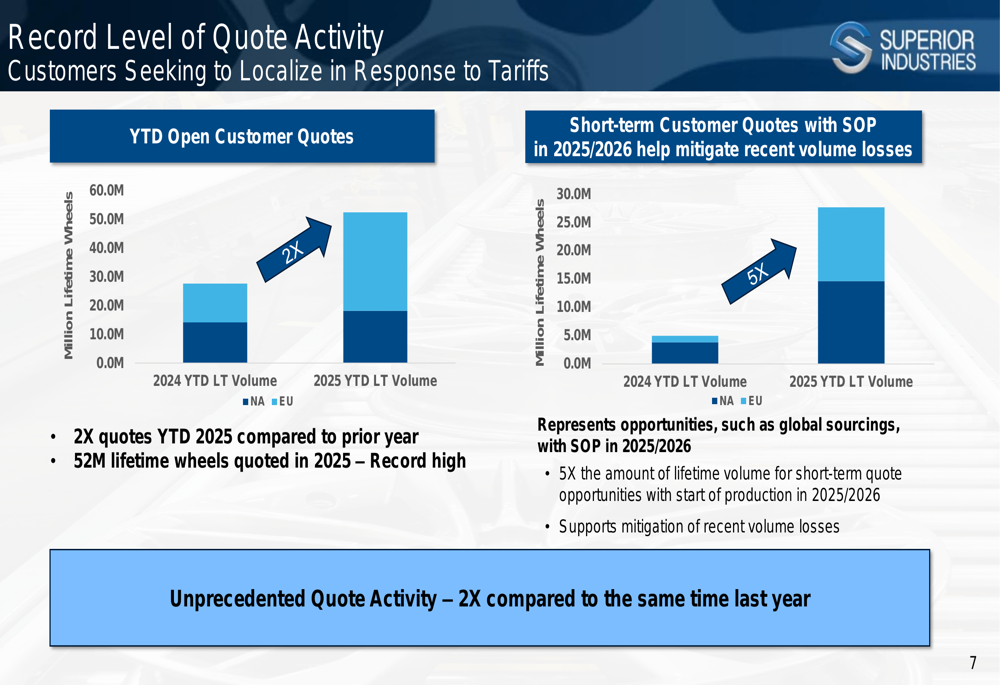

This advantageous tariff environment has contributed to what the company described as "unprecedented" quote activity. Superior reported a doubling of year-to-date open customer quotes compared to 2024 and a five-fold increase in short-term customer quotes with start of production in 2025/2026, representing 52 million lifetime wheels quoted in 2025 – a record high.

Forward-Looking Statements

Despite the positive developments in quote activity and cash flow, Superior announced it is suspending its 2025 guidance. This decision comes amid ongoing challenges in the North American market and as the company works through its recapitalization plans.

The company emphasized its fundamental strengths, including market leadership, execution capabilities, manufacturing expertise, and product innovation, suggesting these factors would position Superior favorably once its balance sheet concerns are addressed.

The suspension of guidance marks a shift from the company’s previous outlook provided in its Q4 2024 earnings, where it had projected 2025 net sales between $1.3 billion and $1.4 billion with adjusted EBITDA ranging from $160 million to $180 million.

While Superior highlighted record quote activity and favorable tariff dynamics, the significant pre-market stock decline suggests investors remain concerned about the company’s financial position and the potential terms of any recapitalization transaction. The coming quarters will be critical as Superior works to convert its quote pipeline into firm orders while addressing its capital structure challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.