EUR/USD likely to find a peak near 1.25: UBS

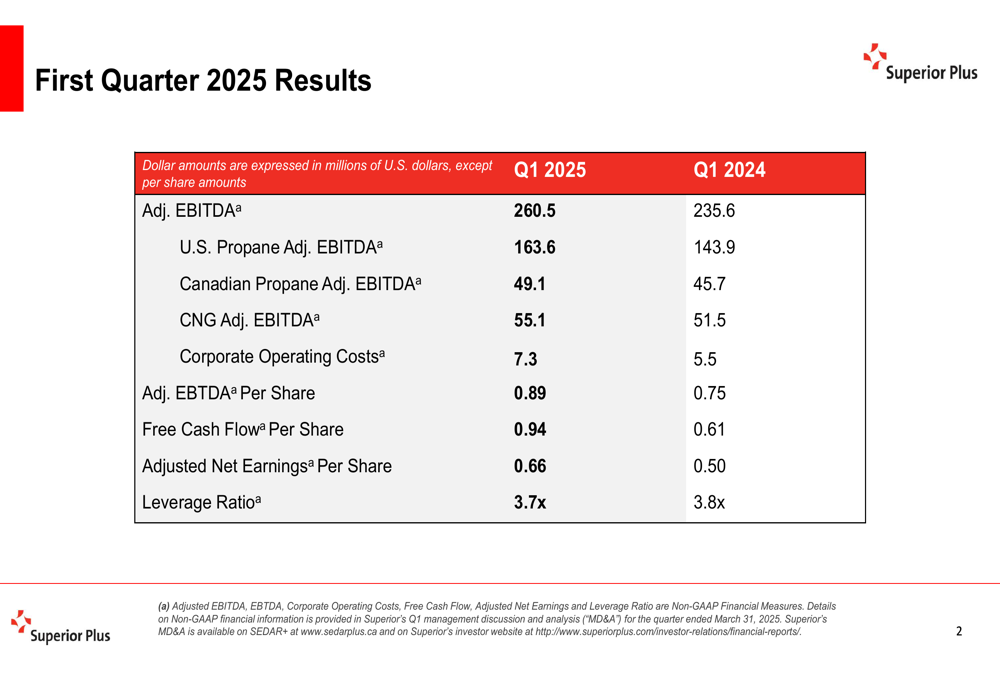

Superior Plus Corp (TSX:SPB) reported strong first-quarter 2025 results on May 14, showing significant improvement across all business segments and substantial growth in key financial metrics. The company’s presentation revealed a 10.6% year-over-year increase in adjusted EBITDA, reaching $260.5 million, while free cash flow per share surged by 54.1%.

The positive results come after a challenging period for the company, which had previously implemented strategic changes including a dividend reduction to redirect cash toward growth initiatives and share repurchases. Superior’s stock closed at $7.26 on May 13, up 2.4% ahead of the earnings announcement.

Quarterly Performance Highlights

Superior Plus demonstrated robust performance across all its business segments in the first quarter of 2025. The U.S. Propane division led the growth with adjusted EBITDA of $163.6 million, representing a 13.7% increase from the same period last year. The Canadian Propane segment generated $49.1 million in adjusted EBITDA, up 7.4% year-over-year, while the Compressed Natural Gas (CNG) division contributed $55.1 million, a 7.0% increase from Q1 2024.

The company’s financial results table shows significant improvements in profitability and cash generation metrics:

The results represent a notable turnaround from the company’s performance in the third quarter of 2024, when it reported challenges in its propane business and revised its full-year EBITDA growth expectations downward. The U.S. propane business, which had reported negative adjusted EBITDA in Q3 2024, has now rebounded strongly to become the primary growth driver.

Detailed Financial Analysis

Superior’s adjusted EBITDA per share increased by 18.7% to $0.89 compared to $0.75 in the first quarter of 2024. This improvement outpaced the overall EBITDA growth, suggesting effective capital allocation and possibly the impact of the company’s share repurchase program initiated after the dividend reduction announced in late 2024.

The most dramatic improvement came in free cash flow per share, which jumped 54.1% to $0.94 from $0.61 in the prior-year period. This substantial increase likely reflects the benefits of the company’s "Superior Delivers" transformation strategy, which was designed to improve operational efficiency and cash generation.

Adjusted net earnings per share rose 32.0% to $0.66, compared to $0.50 in Q1 2024, indicating stronger underlying profitability. Meanwhile, corporate operating costs increased by 32.7% to $7.3 million, potentially reflecting investments in the transformation initiatives.

The company’s leverage ratio improved slightly to 3.7x from 3.8x a year earlier, moving closer to the long-term target of 3.0x mentioned in previous communications. This improvement suggests that Superior is making progress in strengthening its balance sheet while simultaneously growing its business.

Forward-Looking Statements

While the Q1 2025 presentation did not include specific forward guidance, the strong results appear to validate the company’s transformation strategy announced in 2024. The "Superior Delivers" plan had aimed to generate at least $50 million in incremental EBITDA by the end of 2027, and the current performance trajectory suggests the company may be on track to achieve or exceed this target.

The significant improvement in free cash flow is particularly noteworthy, as it provides Superior with increased financial flexibility to fund growth initiatives, reduce leverage, and continue its share repurchase program. The company had previously indicated it would pursue an aggressive share repurchase strategy following its dividend reduction.

Superior Plus is scheduled to hold an Investor Day in April 2025, where it is expected to provide deeper insights into its long-term strategies and performance targets. The strong Q1 2025 results position the company favorably heading into this event and may help rebuild investor confidence following the challenges experienced in 2024.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.