Vivek Ramaswamy buys Strive Inc (ASST) stock worth $1.25 million

Introduction & Market Context

SUSS MicroTec SE (XETRA:SMHN) presented its H1 2025 financial results on August 7, 2025, revealing a mixed performance characterized by robust sales growth but tempered by declining order intake amid increasing global economic uncertainties. The company’s stock closed at €31.78, down 1.26% following the presentation, as investors weighed strong current execution against concerns about future demand.

The semiconductor equipment manufacturer highlighted how global tariffs and trade disputes are creating market uncertainty, particularly affecting order momentum. Despite these headwinds, SUSS delivered impressive sales growth while continuing strategic investments in its new Taiwan production facility.

Quarterly Performance Highlights

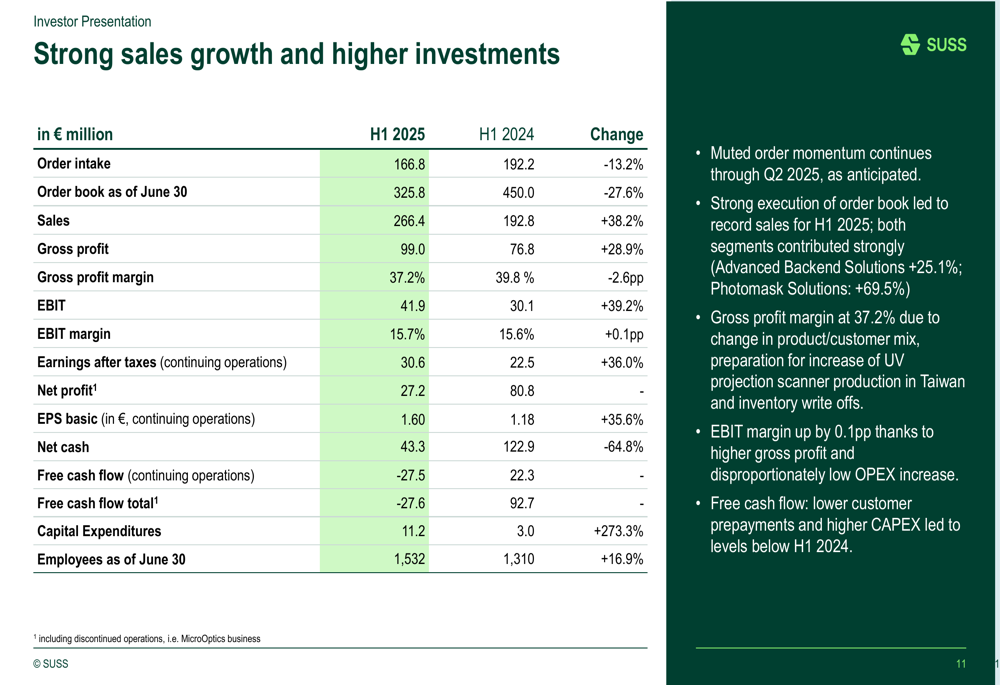

SUSS MicroTec reported sales of €266.4 million for H1 2025, representing a substantial 38.2% increase compared to the same period last year. This strong execution on the existing order book demonstrates the company’s operational capabilities despite challenging market conditions.

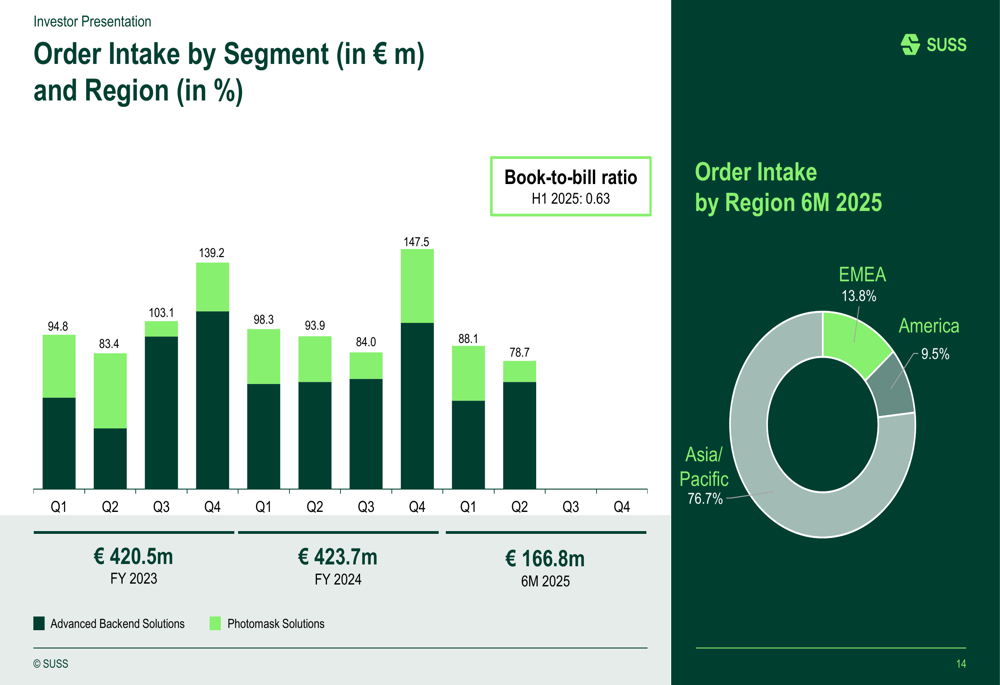

However, order intake declined by 13.2% year-over-year to €166.8 million, resulting in a book-to-bill ratio of just 0.63. This indicates potential challenges for future revenue growth as the company works through its existing backlog.

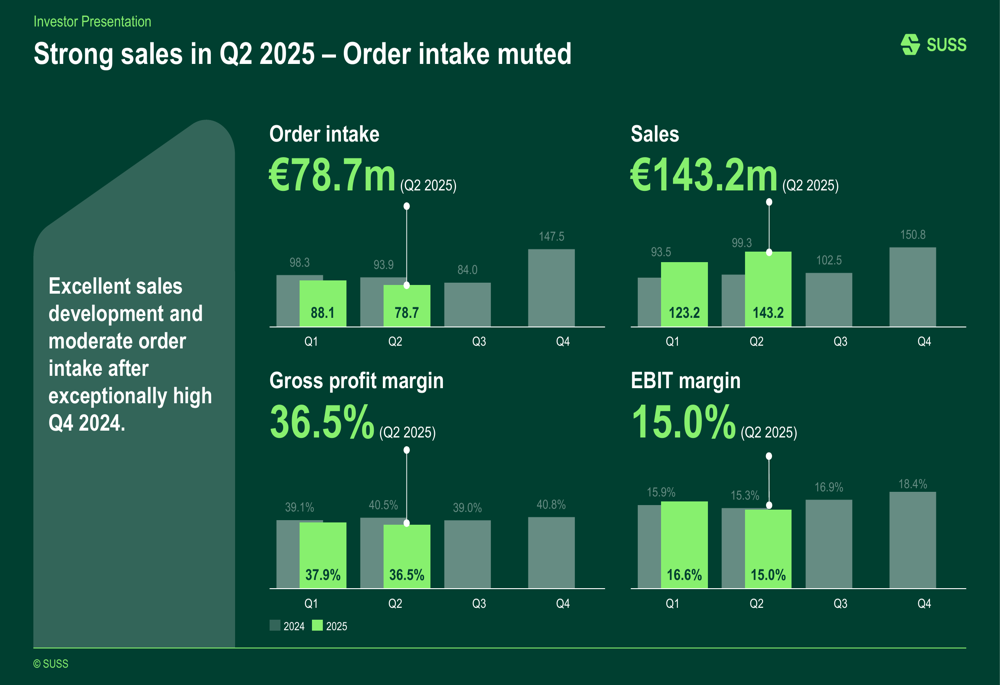

As shown in the following financial results summary:

The company maintained a relatively stable EBIT margin of 15.7%, a slight improvement of 0.1 percentage points year-over-year. However, gross profit margin declined by 2.6 percentage points to 37.2%, which management attributed to product mix changes and one-time effects including training costs and inventory write-downs.

Q2 2025 showed particularly strong performance with sales of €143.2 million and an EBIT margin of 15.0%, as illustrated in the quarterly breakdown:

Earnings after taxes increased by 36.0% to €30.6 million, with basic earnings per share rising to €1.60, up 35.6% compared to H1 2024. Despite these positive earnings metrics, free cash flow turned negative at -€27.6 million, compared to a positive €92.7 million in the prior year period, primarily due to fewer customer prepayments and higher capital expenditures.

The comprehensive financial comparison reveals both strengths and challenges:

Segment Analysis

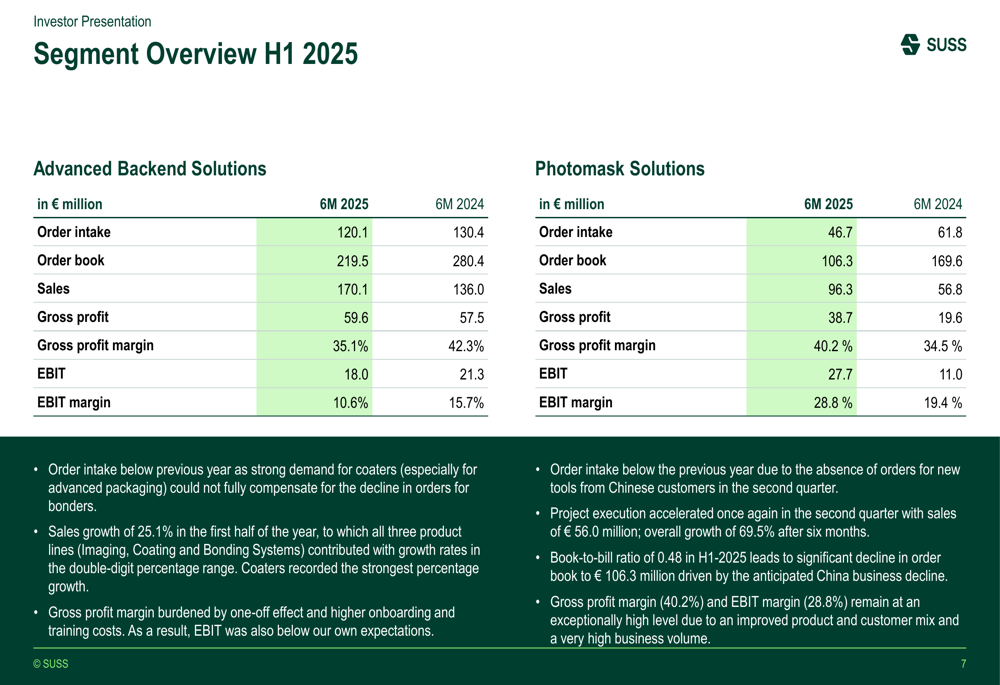

SUSS MicroTec’s two main business segments showed divergent performance trends in H1 2025. The Photomask Solutions segment demonstrated exceptional growth and profitability improvement, while Advanced Backend Solutions faced margin pressure despite sales growth.

The segment breakdown reveals these contrasting trajectories:

Photomask Solutions emerged as the standout performer with sales surging 69.5% to €96.3 million and EBIT margin climbing to an impressive 28.8%, up 9.4 percentage points year-over-year. This segment’s gross profit margin also improved significantly to 40.2%.

In contrast, Advanced Backend Solutions, while still delivering 25.1% sales growth to €170.1 million, saw its gross profit margin decline by 7.2 percentage points to 35.1% and EBIT margin fall to 10.6% from 15.7% in the prior year.

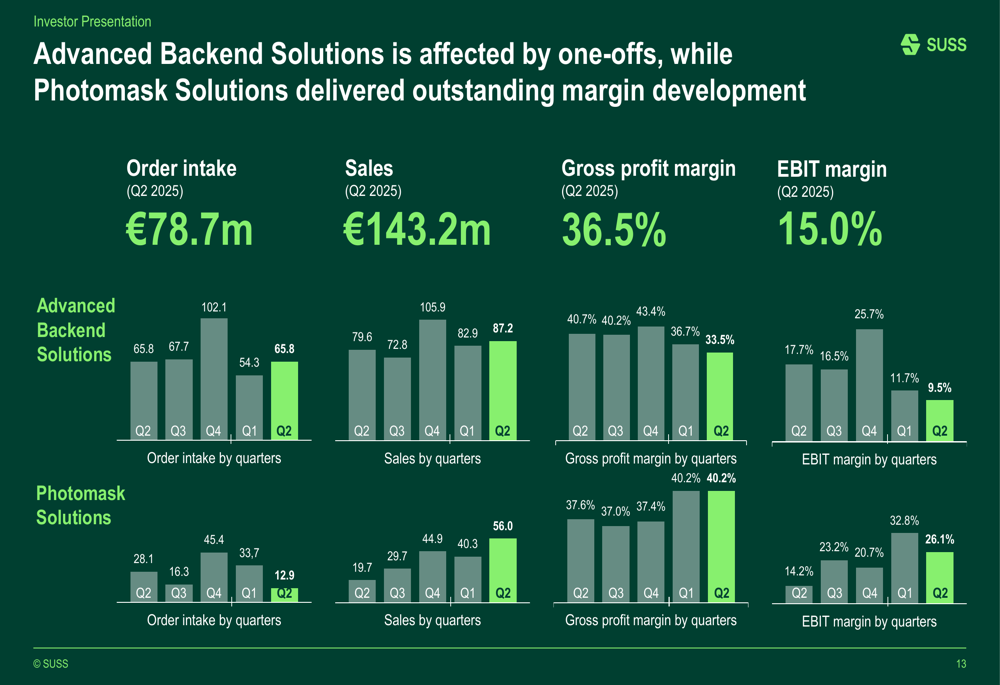

The quarterly segment performance illustrates these trends over time:

Regional analysis of order intake shows SUSS MicroTec’s continued strong dependence on the Asia/Pacific region, which accounted for 76.7% of orders in H1 2025, followed by EMEA at 13.8% and America at 9.5%.

Strategic Initiatives

Despite market uncertainties, SUSS MicroTec continues to invest in its future growth with significant progress on its new production site in Zhubei, Taiwan. The facility is advancing according to plan with an official opening scheduled for late October 2025.

The company has completed installations for clean room manufacturing and warehouse facilities, with interior outfitting of offices well advanced. Investment volume has reached €9.4 million so far, with total capital expenditure for the new site expected to reach €14.5 million in 2025.

The following image shows the progress of the Zhubei production site:

The new facility includes a 2,600m² scanner cleanroom with Class 10000 specifications, ESD protection flooring, and ±3mm flatness requirements. This strategic expansion strengthens SUSS MicroTec’s manufacturing capabilities in a key semiconductor market region.

Forward-Looking Statements

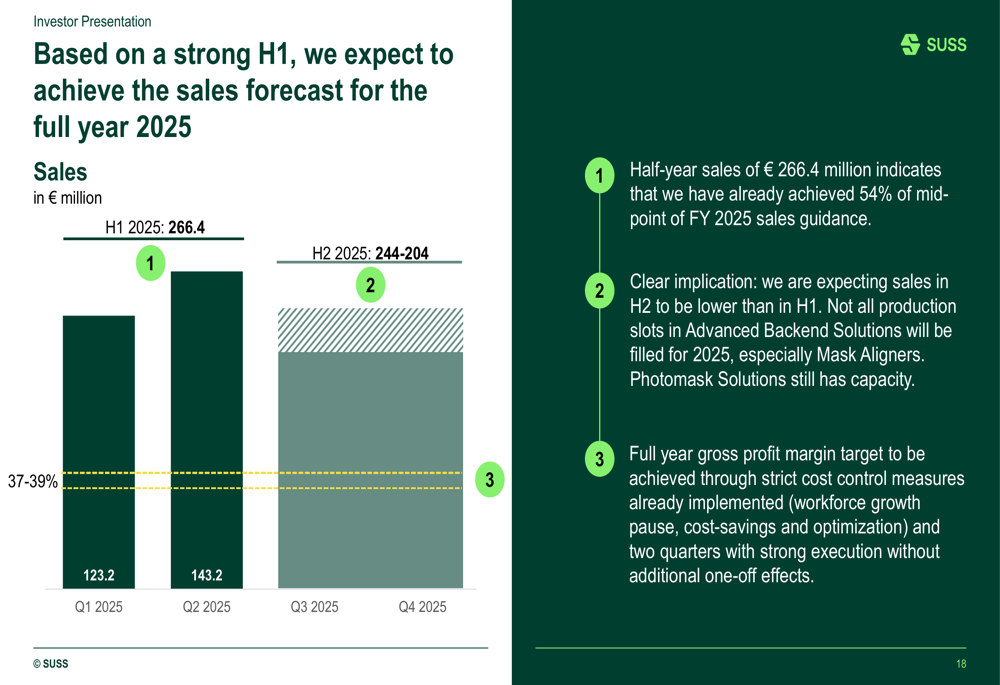

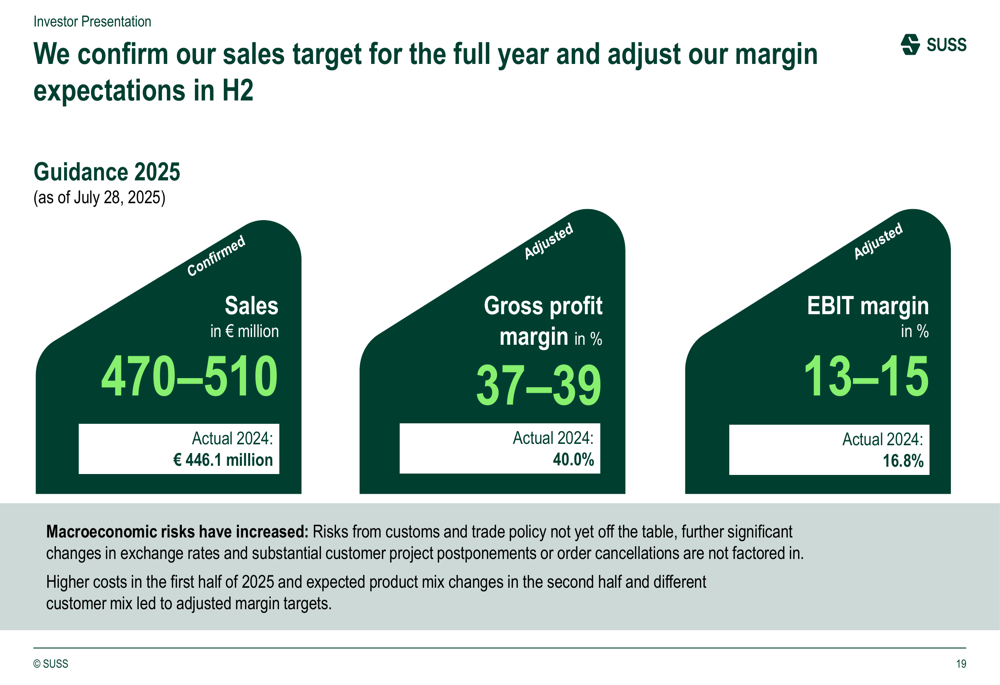

Looking ahead, SUSS MicroTec maintained its 2025 guidance but noted that macroeconomic risks have increased. The company expects full-year sales between €470-510 million, representing growth from €446.1 million in 2024. However, management explicitly stated that they anticipate lower sales in the second half of 2025 compared to the strong first half.

As illustrated in the sales forecast:

The company has already achieved 54% of the mid-point of its full-year sales guidance in the first half, indicating a significant expected slowdown in the second half. Management noted that not all production slots in Advanced Backend Solutions will be filled for 2025, especially for Mask Aligners, though Photomask Solutions still has available capacity.

SUSS MicroTec also adjusted its margin expectations, with gross profit margin guidance of 37-39% (down from 40.0% in 2024) and EBIT margin of 13-15% (down from 16.8% in 2024). The company plans to implement strict cost control measures, including a pause in workforce growth and various cost-saving initiatives, to achieve these targets.

The full 2025 guidance is summarized as follows:

Despite near-term challenges, SUSS MicroTec remains focused on its long-term strategic positioning in specialized semiconductor equipment markets, with its expanded manufacturing footprint in Taiwan expected to support future growth opportunities once market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.