Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Sylvamo Corporation (NYSE:SLVM), the self-described "World’s Paper Company," presented its first quarter 2025 earnings results on May 9, 2025, revealing a period marked by declining financial metrics and significant leadership changes. The company’s stock fell 2.49% in pre-market trading to $58.70, continuing a downward trend that has seen the stock well off its 52-week high of $98.02.

The presentation comes amid challenging conditions in the paper industry, with uncoated freesheet demand declining in Europe (-7%) and North America (-1%), though showing modest growth in Latin America (+3%). The company is navigating these headwinds while implementing price increases in Brazil and North America and addressing operational challenges.

Executive Summary

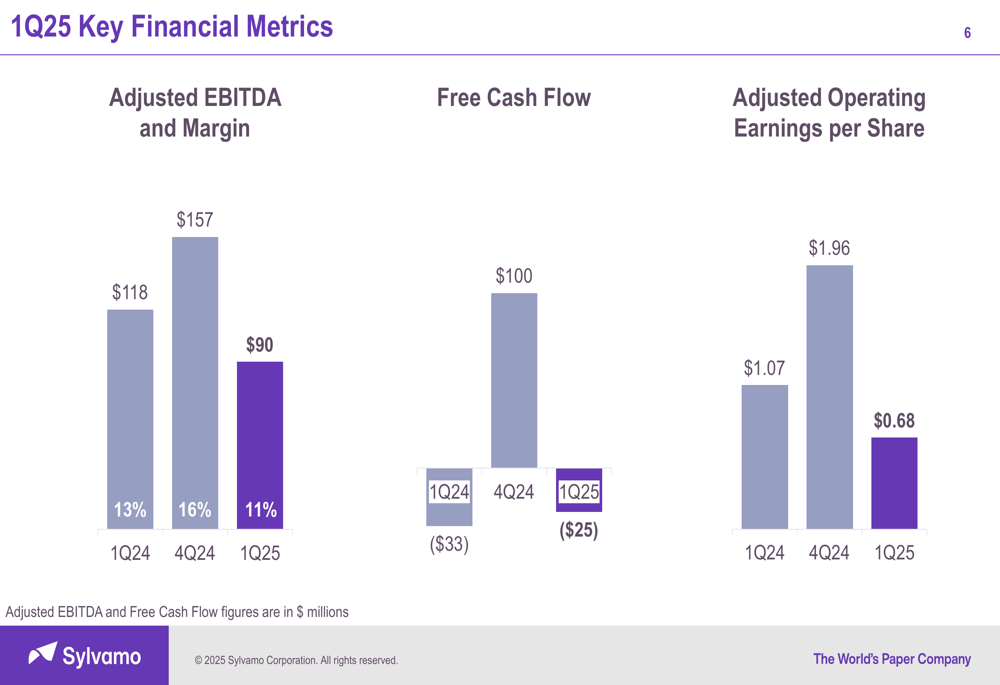

Sylvamo reported first quarter 2025 Adjusted EBITDA of $90 million (11% margin), down from $157 million (16% margin) in Q4 2024 and $118 million (13% margin) in Q1 2024. Free cash flow was negative $25 million, an improvement from negative $33 million in Q1 2024 but a significant drop from the $100 million generated in Q4 2024. Adjusted operating earnings per share fell to $0.68 from $1.96 in the previous quarter and $1.07 in the same quarter last year.

As shown in the following chart of key financial metrics:

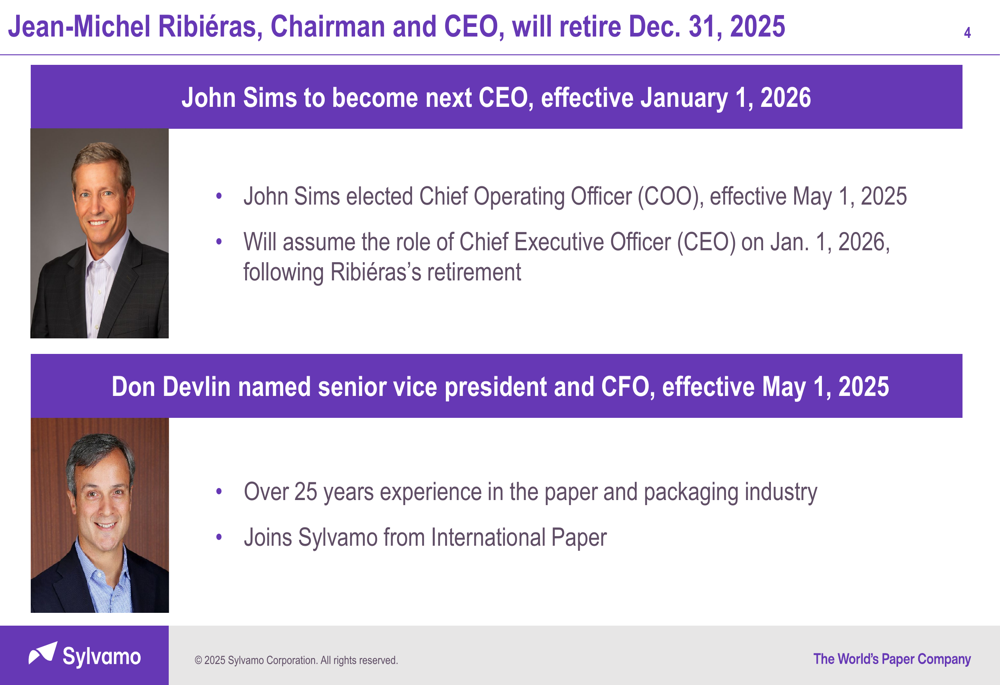

The company also announced significant leadership changes, with current Chairman and CEO Jean-Michel Ribiéras set to retire on December 31, 2025. John Sims, who was elected Chief Operating Officer effective May 1, 2025, will become CEO on January 1, 2026. Additionally, Don Devlin was named Senior Vice President and CFO effective May 1, 2025.

Leadership Transition

The leadership transition represents a significant milestone for Sylvamo. The company provided details on the experience of the incoming executives in its presentation:

John Sims, the incoming CEO, was elected COO on May 1, 2025, and will assume the CEO role at the beginning of 2026. Don Devlin, the new CFO, brings over 25 years of experience in the paper and packaging industry, joining Sylvamo from International Paper.

This leadership change comes at a challenging time for the company as it navigates operational difficulties and implements strategic initiatives to improve performance across its global operations.

Quarterly Performance Highlights

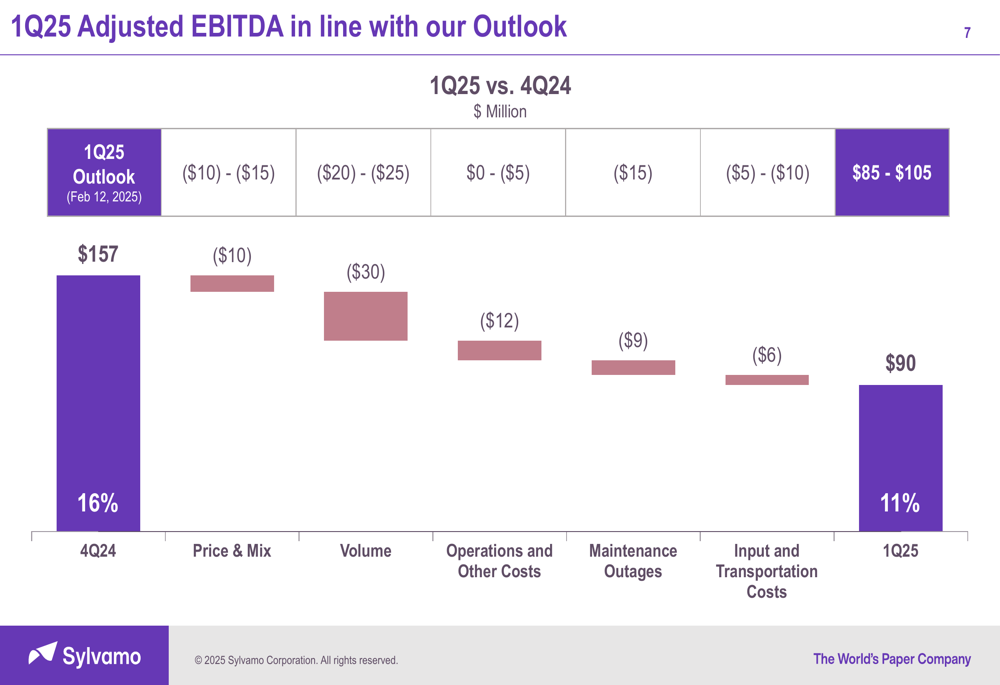

Sylvamo’s Q1 2025 performance was impacted by several factors, including heavy planned maintenance outages and operational challenges. The company successfully executed its planned maintenance schedule but noted that operational issues affected results. The following waterfall chart illustrates the factors contributing to the decline in Adjusted EBITDA from Q4 2024 to Q1 2025:

The $67 million quarter-over-quarter decline in Adjusted EBITDA was driven by lower volume (-$30 million), operational and other costs (-$12 million), price and mix (-$10 million), maintenance outages (-$9 million), and higher input and transportation costs (-$6 million).

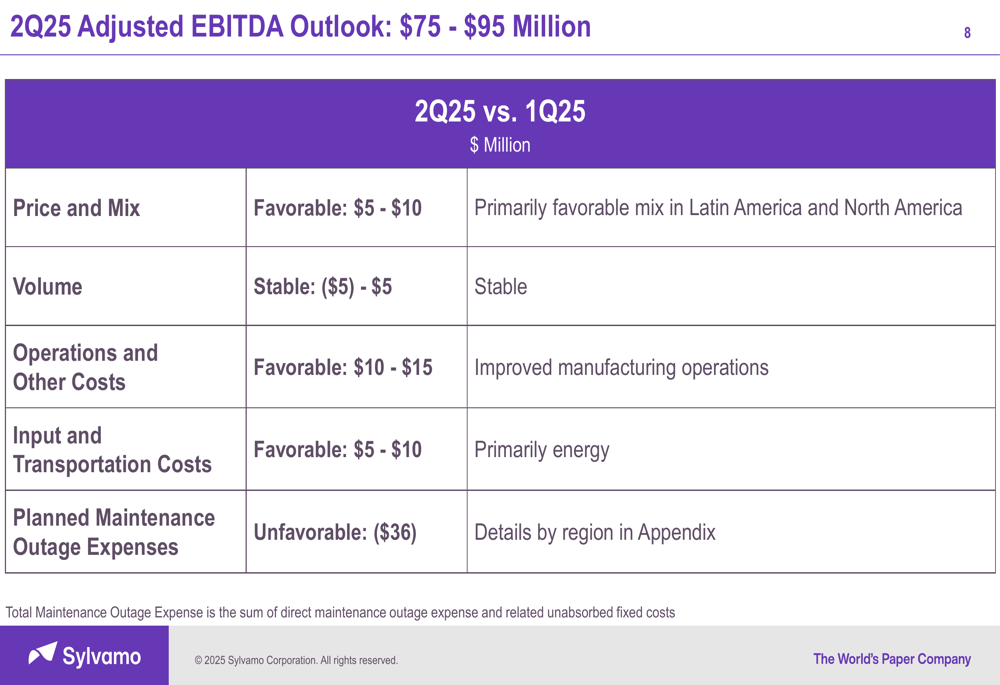

For Q2 2025, Sylvamo provided an Adjusted EBITDA outlook of $75-95 million, with the following factors expected to impact performance:

Regional Performance & Challenges

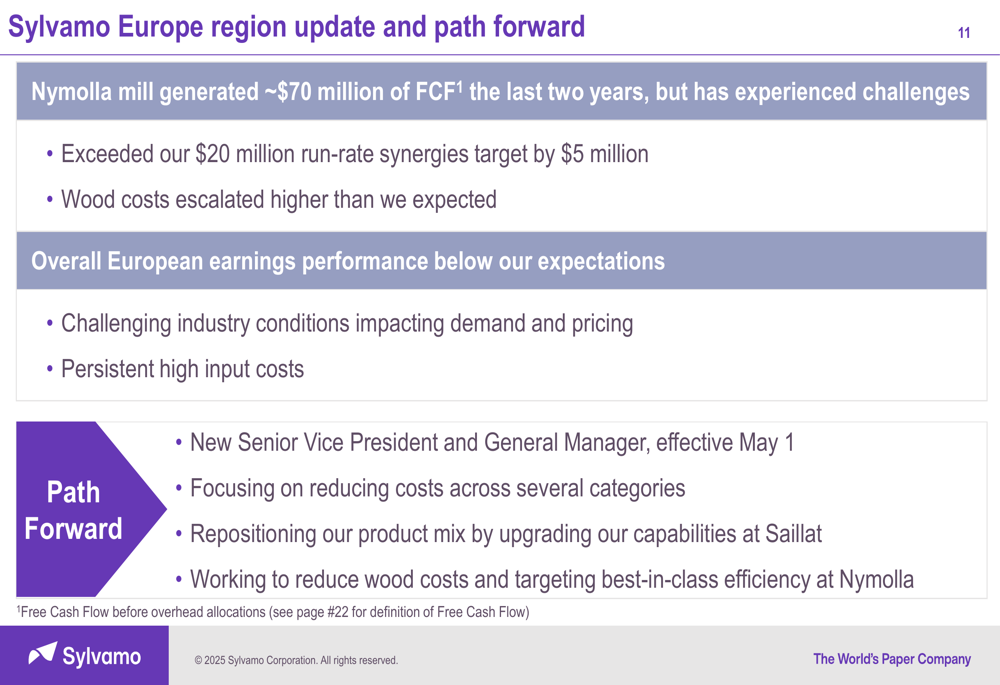

Sylvamo’s European operations face particular challenges. The company disclosed that while the Nymolla mill generated approximately $70 million in free cash flow over the past two years, European earnings performance is below expectations due to challenging industry conditions and high input costs.

The company outlined its strategy to address these issues:

In response to these challenges, Sylvamo has appointed a new Senior Vice President and General Manager for the European region (effective May 1) and is focusing on cost reduction, product mix repositioning, and operational efficiency improvements.

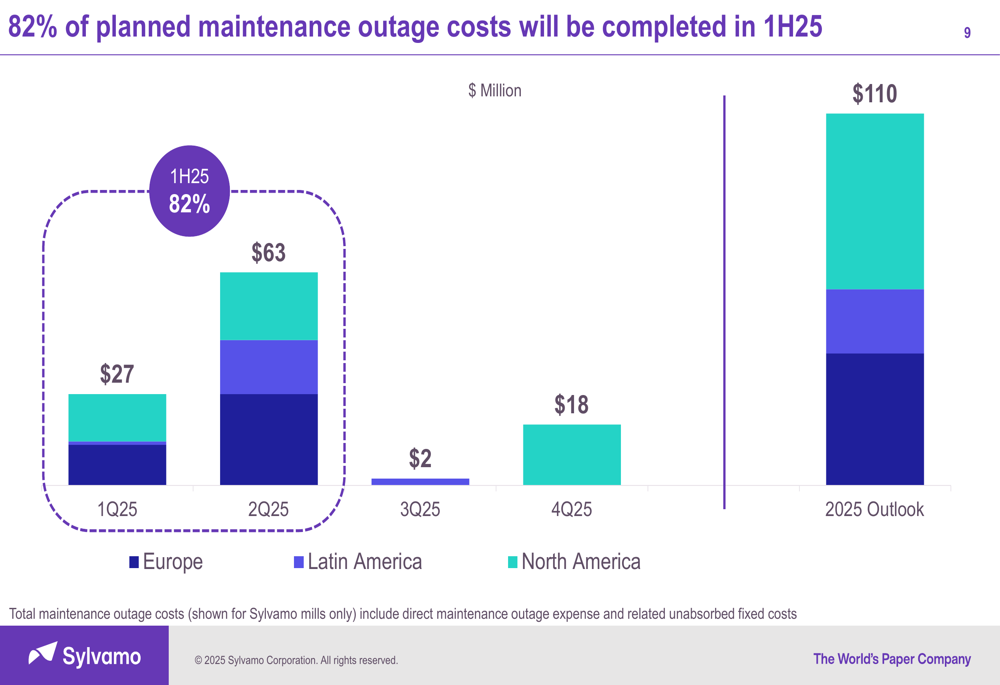

The company also highlighted its planned maintenance outage costs for 2025, noting that 82% of these costs will be incurred in the first half of the year:

Financial Position & Capital Allocation

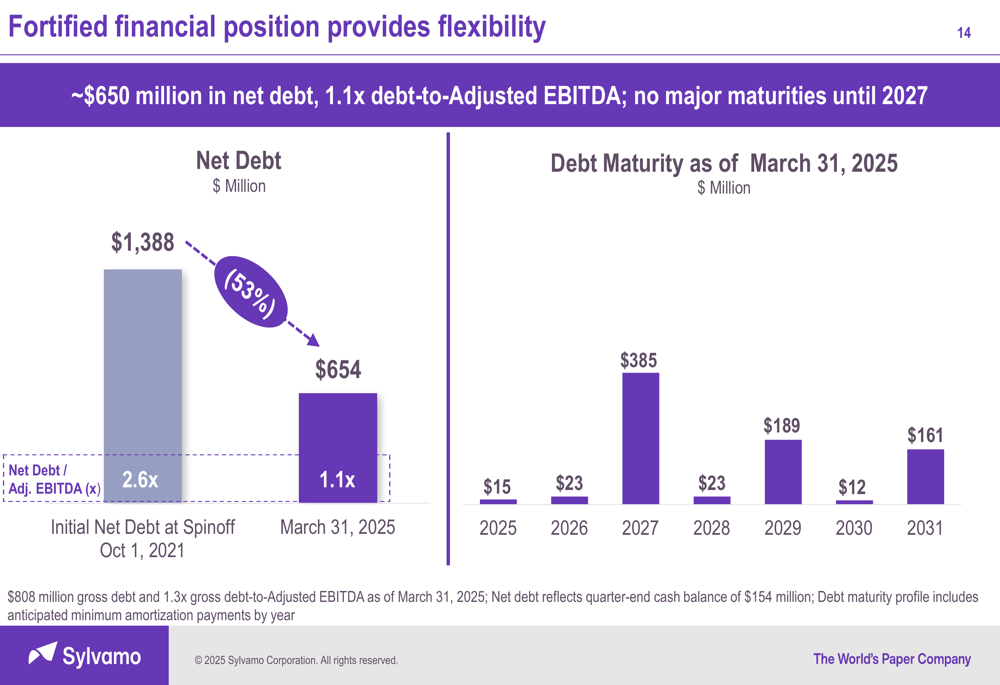

Despite the operational challenges, Sylvamo emphasized its strong financial position with approximately $650 million in net debt and a 1.1x debt-to-Adjusted EBITDA ratio. The company has no major debt maturities until 2027, providing financial flexibility.

As illustrated in the following chart, Sylvamo has significantly reduced its debt since the spinoff:

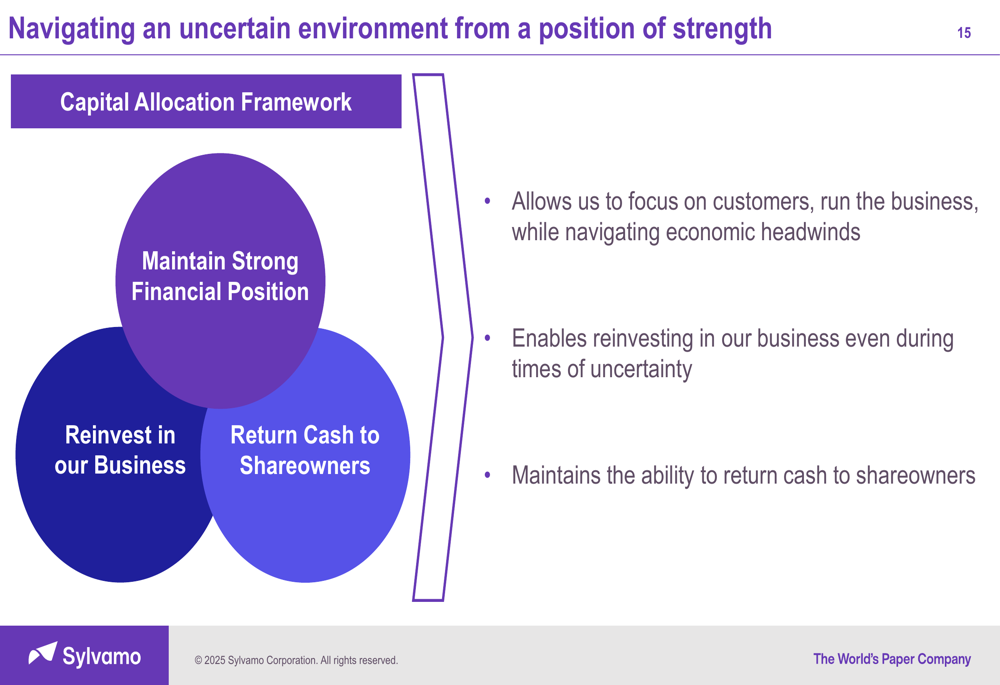

The company outlined its capital allocation framework, focusing on maintaining a strong financial position, reinvesting in the business, and returning cash to shareholders:

Forward-Looking Statements

Looking ahead, Sylvamo provided guidance for 2025, including total maintenance outage costs of $110 million (up from $73 million in 2024) and capital spending of $220-240 million. The company expects Q2 2025 Adjusted EBITDA to range from $75-95 million, reflecting continued pressure from planned maintenance outages ($63 million expected in Q2).

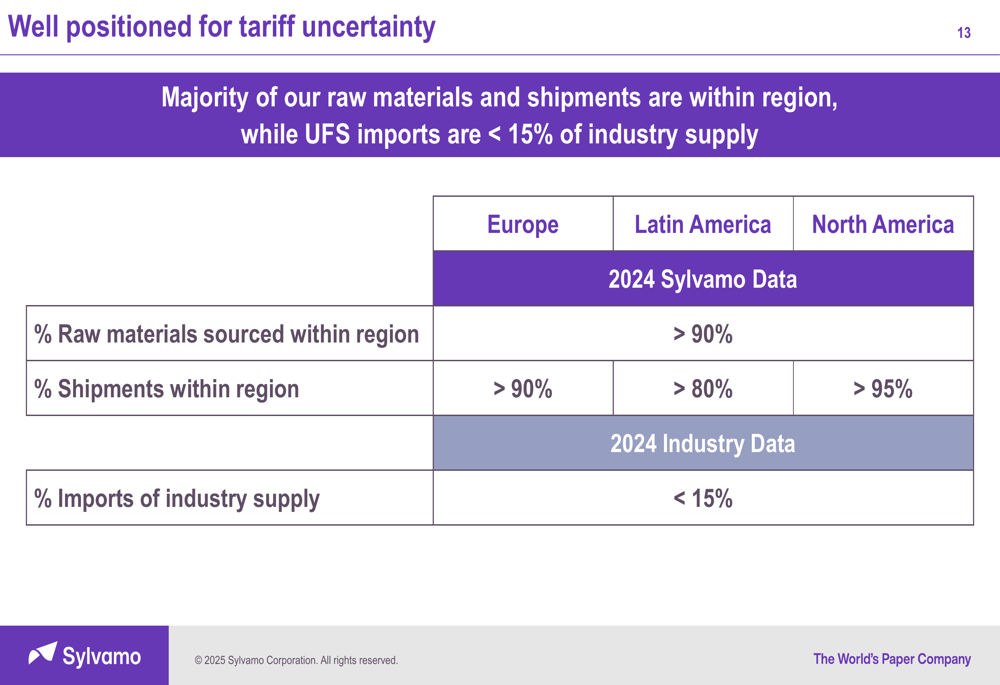

The company highlighted potential challenges from tariff risks but emphasized its strong positioning with the majority of raw materials and shipments within regions:

Sylvamo expressed confidence in its future, citing its strong financial position, ability to navigate tariff uncertainty, ongoing business reinvestment, and disciplined capital allocation. The company also emphasized the seamless execution of its CEO and CFO succession plan.

In conclusion, while Sylvamo faces near-term challenges from maintenance costs, operational issues, and regional market conditions, particularly in Europe, the company maintains that its strong financial position and strategic initiatives position it well for long-term success. Investors will be watching closely to see if the leadership transition and operational improvements can reverse the declining earnings trend in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.