Eli Lilly joins $1 trillion club as weight-loss drugs fuel growth

Introduction & Market Context

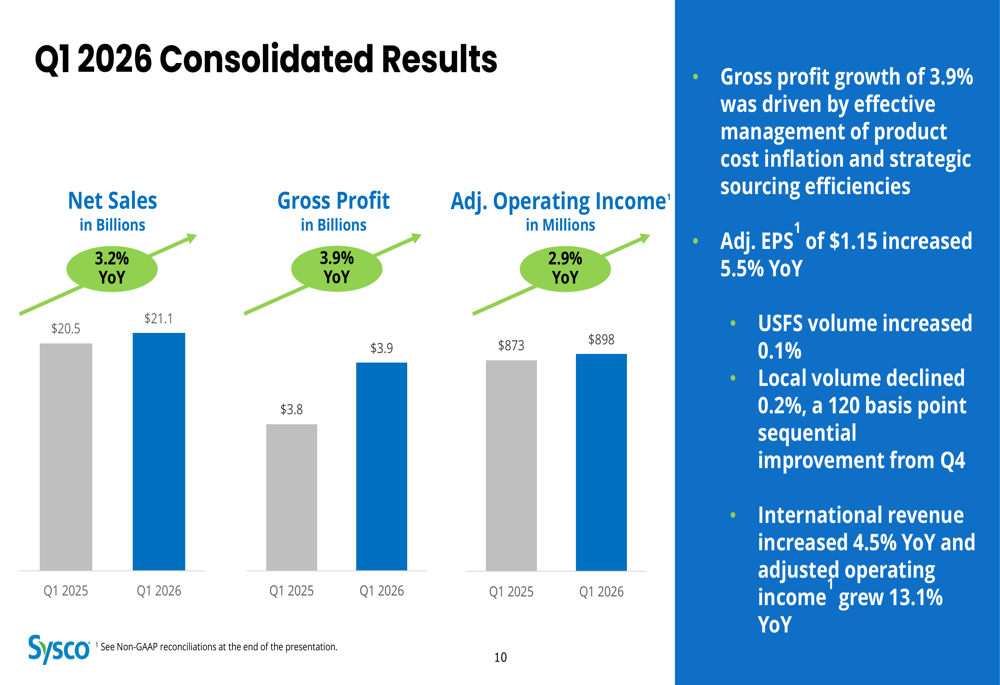

Sysco Corporation (NYSE:SYY) released its fiscal first quarter 2026 earnings presentation on October 28, 2025, reporting revenue growth of 3.2% year-over-year to $21.1 billion, with adjusted earnings per share rising 5.5% to $1.15, exceeding analyst expectations of $1.12. Despite the earnings beat, Sysco's stock dipped 1.08% in regular trading following a 1.28% decline in pre-market activity.

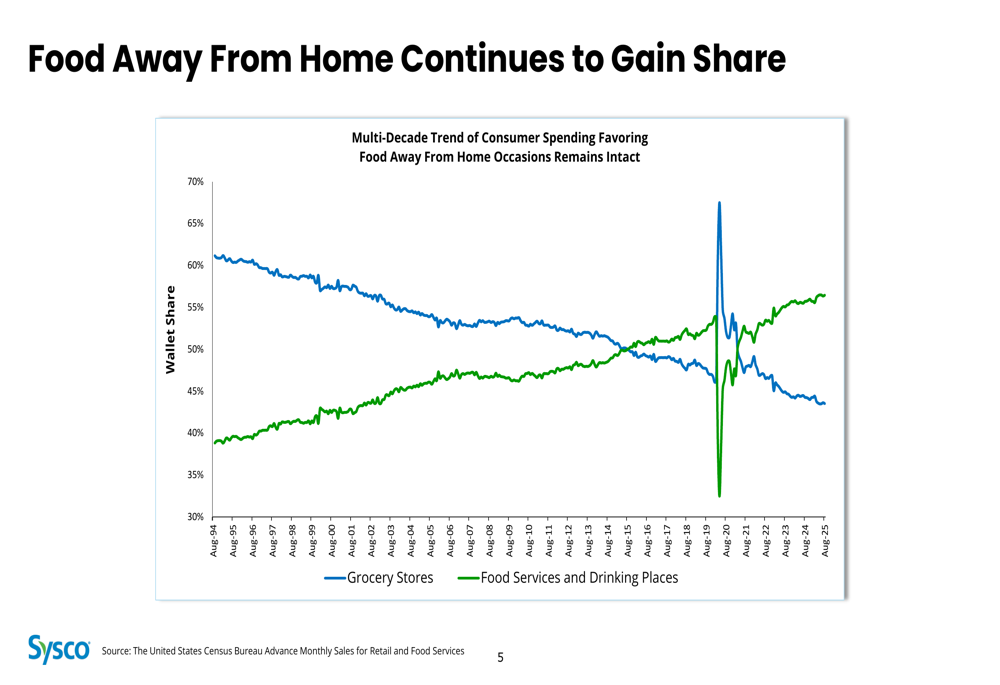

The company continues to benefit from the long-term shift in consumer spending toward food away from home, a multi-decade trend that shows no signs of reversing. As illustrated in the following chart, food services and drinking places have consistently gained wallet share compared to grocery stores:

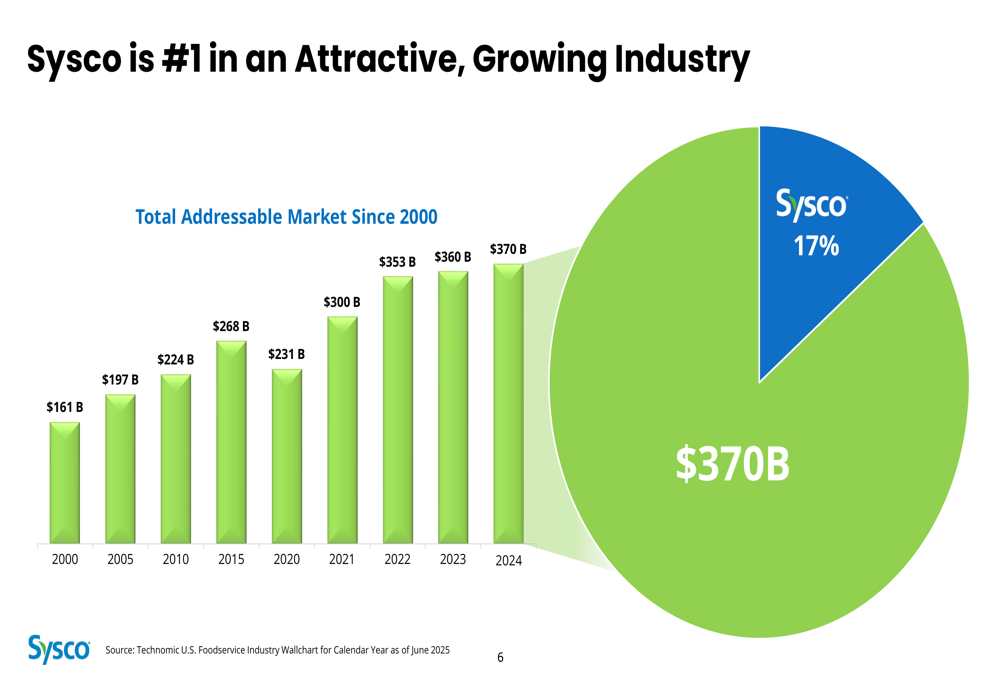

Sysco maintains its position as the dominant player in the foodservice distribution industry with a 17% market share in a growing $370 billion total addressable market. The industry has more than doubled in size since 2000, providing Sysco with substantial runway for continued expansion.

Quarterly Performance Highlights

Sysco delivered solid financial results across key metrics in Q1 2026. Revenue increased 3.2% to $21.1 billion, gross profit rose 3.9% to $3.9 billion, and adjusted operating income grew 2.9% to $898 million. The company's adjusted EPS of $1.15 represented a 5.5% improvement year-over-year, driven by effective product cost management and strategic sourcing initiatives.

The company's gross margin expanded by 13 basis points to 18.5%, reflecting Sysco's ability to manage inflationary pressures effectively. During the quarter, Sysco returned $259 million to shareholders through dividends, continuing its long history of shareholder returns.

CEO Kevin Hourican noted during the earnings call, "We are building momentum across sales, merchandising, and operations," highlighting the company's strategic focus on growth and operational efficiency.

Segment Analysis

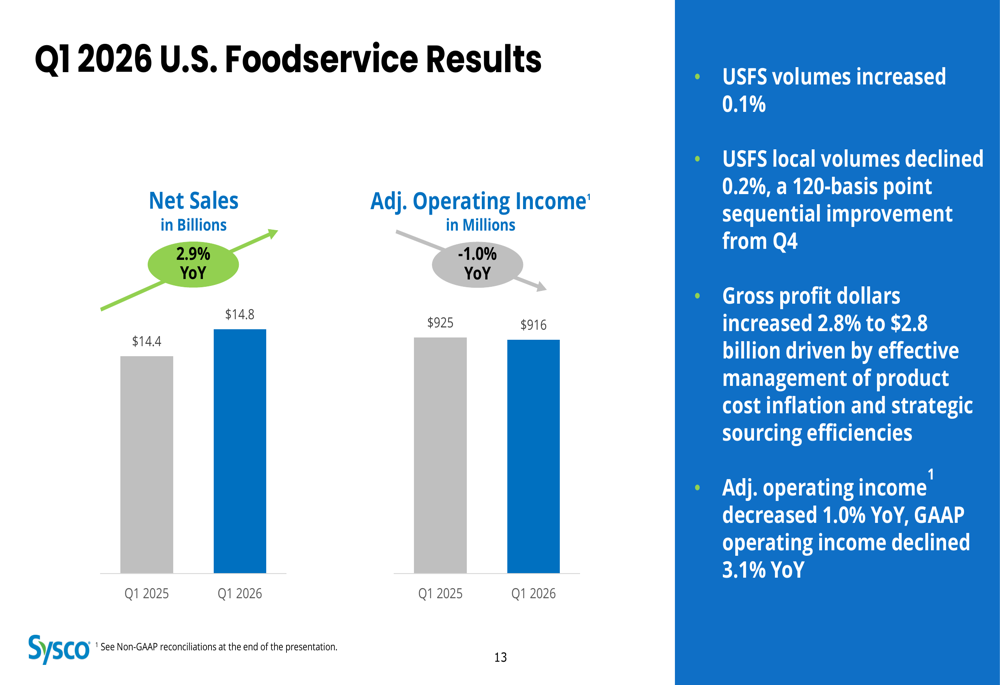

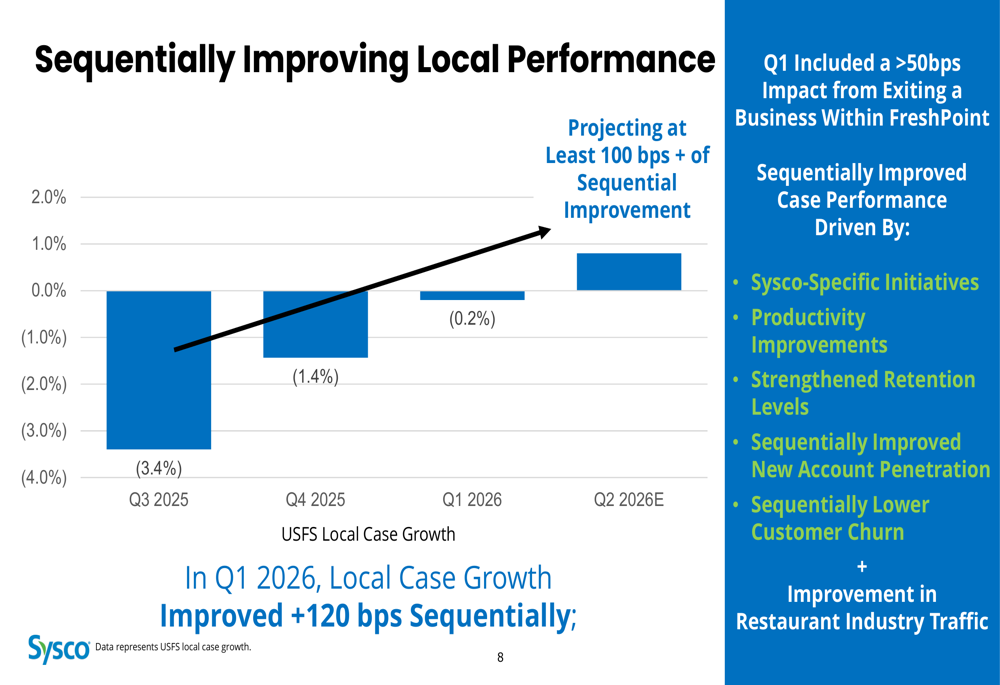

U.S. Foodservice Operations (USFS), Sysco's largest segment, saw sales increase by 2.9% to $14.8 billion. However, adjusted operating income decreased slightly by 1.0% to $916 million. While overall USFS volumes increased by a modest 0.1%, the company highlighted a significant sequential improvement in local case growth, which declined by only 0.2% compared to a 1.4% decline in the previous quarter.

This 120 basis point sequential improvement in local case growth represents a positive trend for Sysco, as the company continues to focus on its local customer base. The improvement is particularly noteworthy given that it includes a greater than 50 basis point impact from exiting a business within FreshPoint.

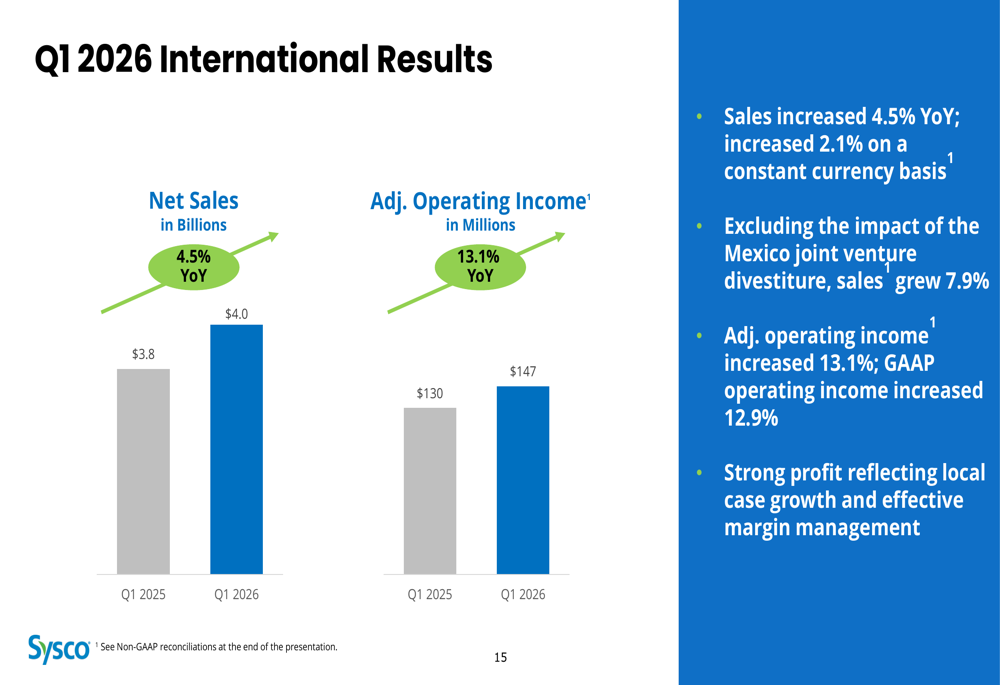

The International segment delivered strong results, with sales increasing 4.5% to $4.0 billion and adjusted operating income rising 13.1% to $147 million. This robust performance reflects local case growth and effective margin management across Sysco's international operations.

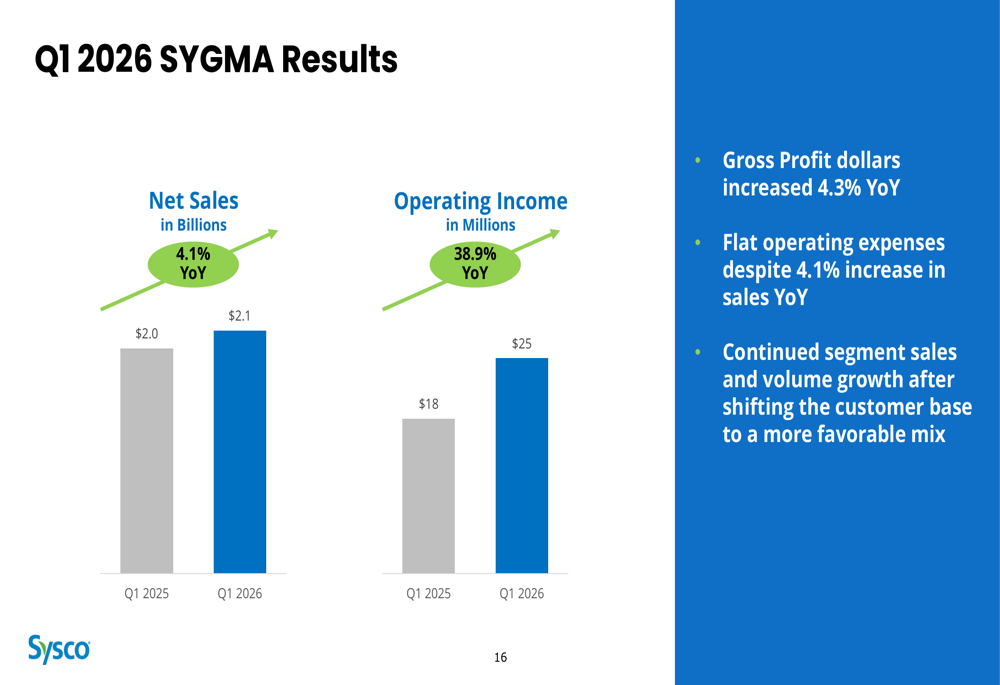

SYGMA, Sysco's chain restaurant distribution segment, reported impressive growth with sales up 4.1% to $2.1 billion and operating income surging 38.9% to $25 million. This substantial profit improvement resulted from flat operating expenses despite the sales increase, demonstrating effective cost control and a more favorable customer mix.

Strategic Initiatives

Sysco's "Recipe for Growth" strategy continues to guide the company's long-term approach to sustainable, profitable growth. The strategy encompasses five key pillars: Customer Teams, Supply Chain, Digital, Products and Solutions, and Future Horizons.

For fiscal year 2026, Sysco is focusing on several key growth initiatives, including "Sysco Perks!" (a customer loyalty program), "AI360" (artificial intelligence tools), "Pricing Agility" (dynamic pricing capabilities), and "Your Way" (customized solutions). These initiatives are designed to enhance customer experience, drive operational efficiency, and support market share gains.

CFO Kenny Cheung emphasized the company's focus on profitable growth during the earnings call, stating, "We are taking share profitably," underscoring Sysco's commitment to balancing growth with margin protection.

Forward Guidance

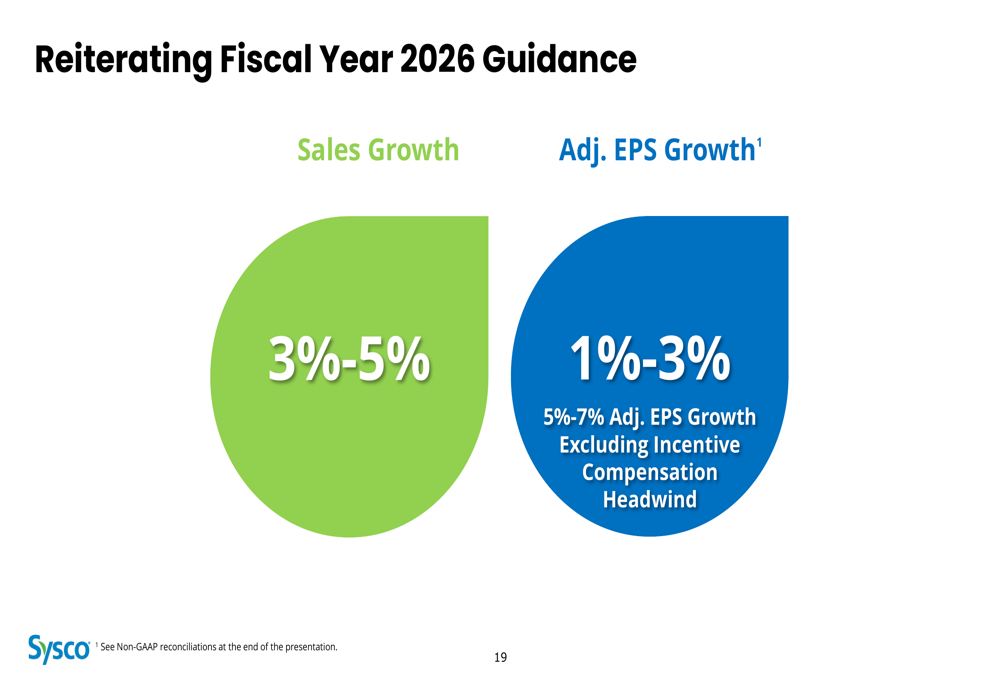

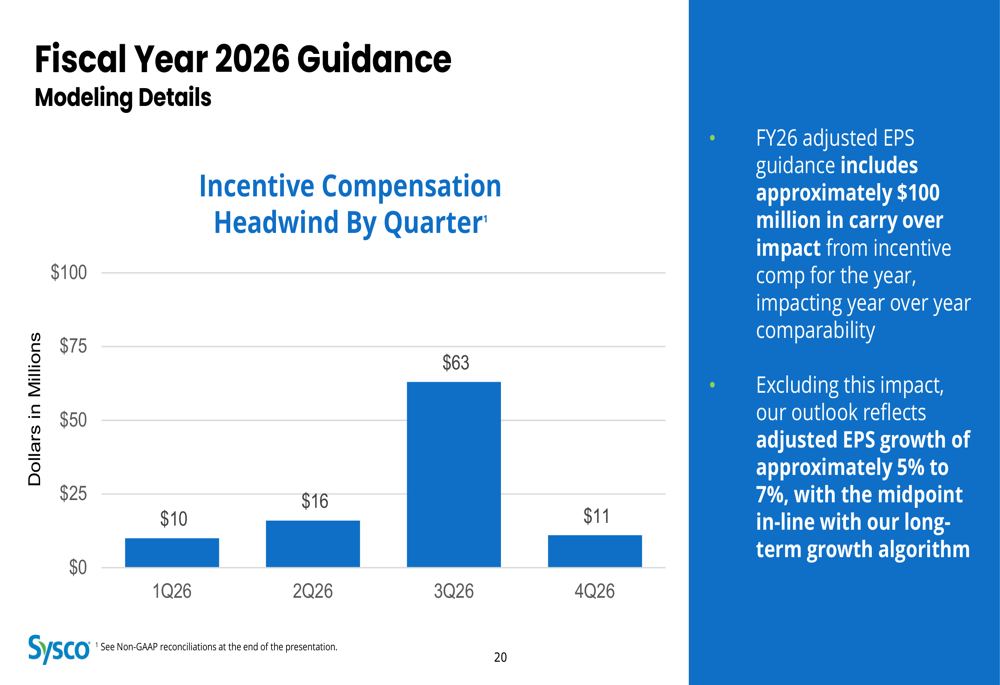

Sysco reiterated its fiscal year 2026 guidance, projecting sales growth of 3-5% and adjusted EPS growth of 1-3%, or 5-7% when excluding the approximately $100 million headwind from incentive compensation. This guidance reflects management's confidence in the company's ability to continue executing its growth strategy despite market challenges.

The company provided additional detail on the quarterly distribution of the incentive compensation headwind, with the most significant impact of $63 million expected in the third quarter of fiscal 2026.

Sysco's balance sheet remains strong with an investment-grade credit rating, though the net debt to adjusted EBITDA ratio increased slightly to 2.90x in Q1 2026 from 2.74x in Q1 2025. The company targets a leverage ratio range of 2.5-2.75x, indicating a commitment to disciplined financial management.

Conclusion

Sysco's Q1 2026 results demonstrate the company's resilience and operational momentum in a challenging market environment. The sequential improvement in local case growth, strong international performance, and impressive SYGMA results offset slight weakness in U.S. Foodservice operating income. With continued execution of its strategic initiatives and a strong financial foundation, Sysco appears well-positioned to maintain its industry leadership.

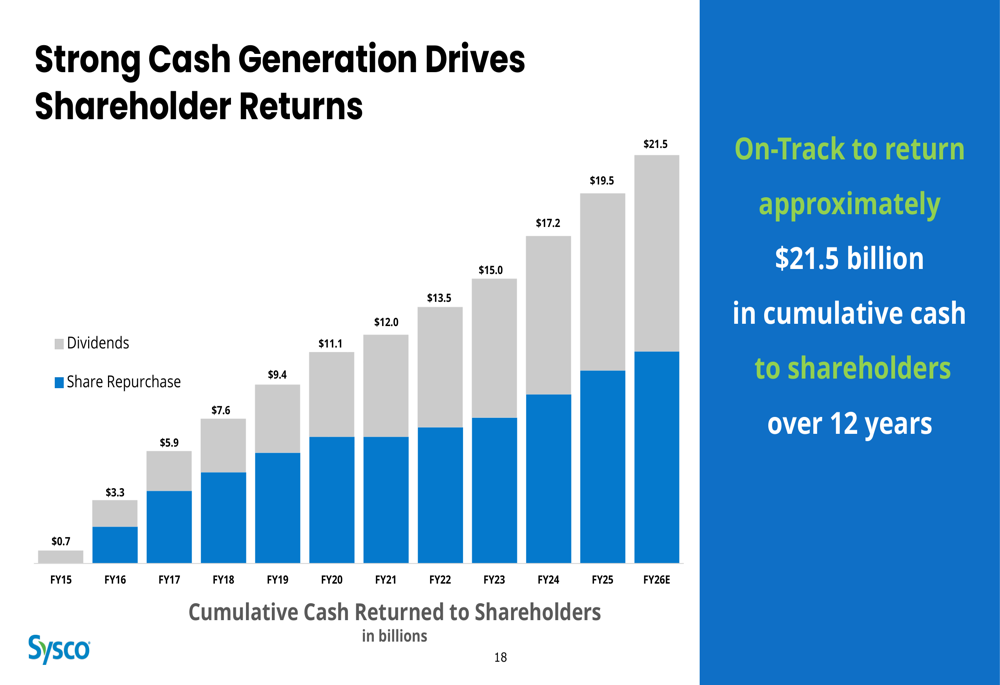

The company's long-term track record of returning cash to shareholders remains impressive, with Sysco on pace to return approximately $21.5 billion cumulatively over a 12-year period through fiscal year 2026.

While the market's initial reaction to the earnings was slightly negative despite the beat on expectations, Sysco's fundamental business performance and strategic positioning suggest continued strength in the quarters ahead as the company capitalizes on the ongoing shift toward food away from home and executes its comprehensive growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.