Hansen, Mueller Industries director, sells $105,710 in stock

Introduction & Market Context

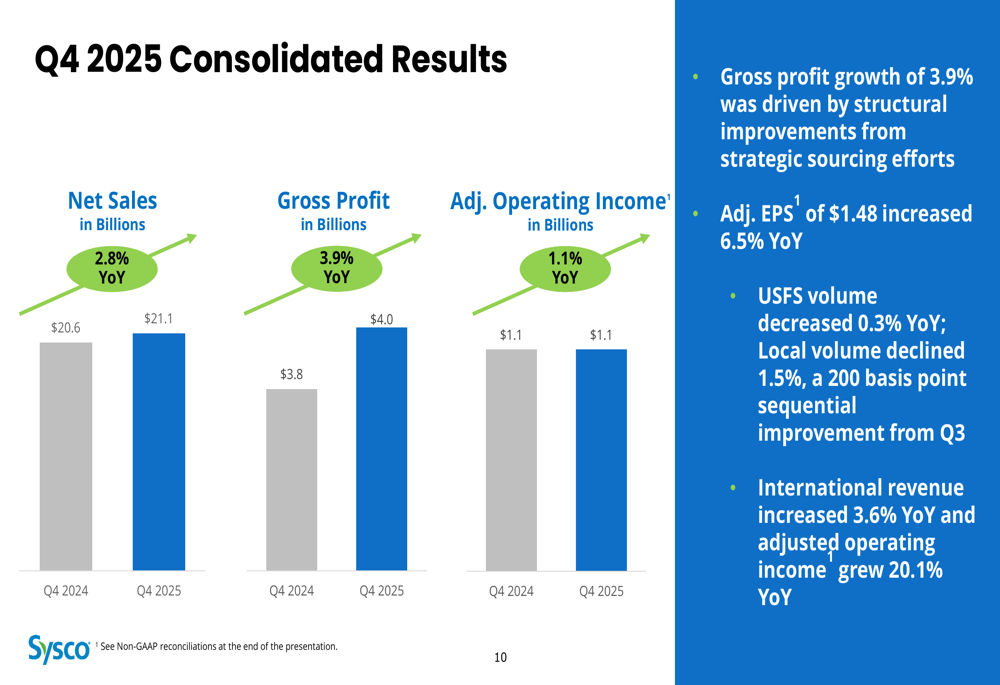

Sysco Corporation (NYSE:SYY) presented its fiscal fourth quarter and full-year 2025 results on July 29, 2025, showcasing a solid performance with notable improvements in key metrics following a challenging third quarter. The foodservice distribution giant reported Q4 revenue growth of 2.8% to $21.1 billion, with adjusted earnings per share rising 6.5% to $1.48.

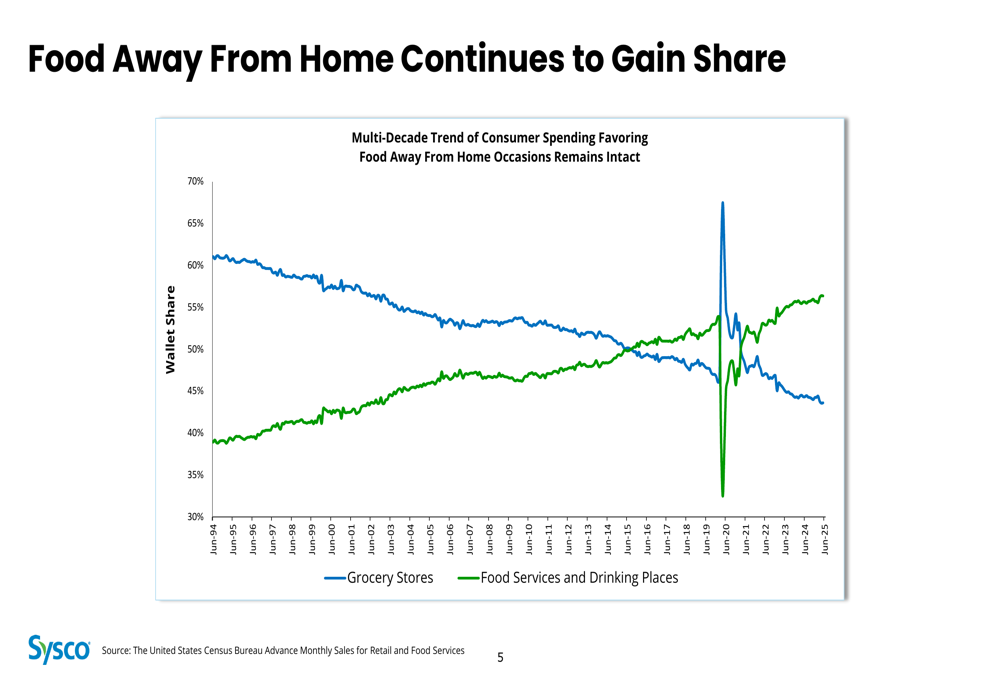

The company continues to benefit from the long-term shift in consumer spending toward food away from home, a trend that has persisted for decades and provides a favorable backdrop for Sysco’s operations.

As shown in the following chart tracking consumer wallet share between grocery stores and food service establishments since 1994:

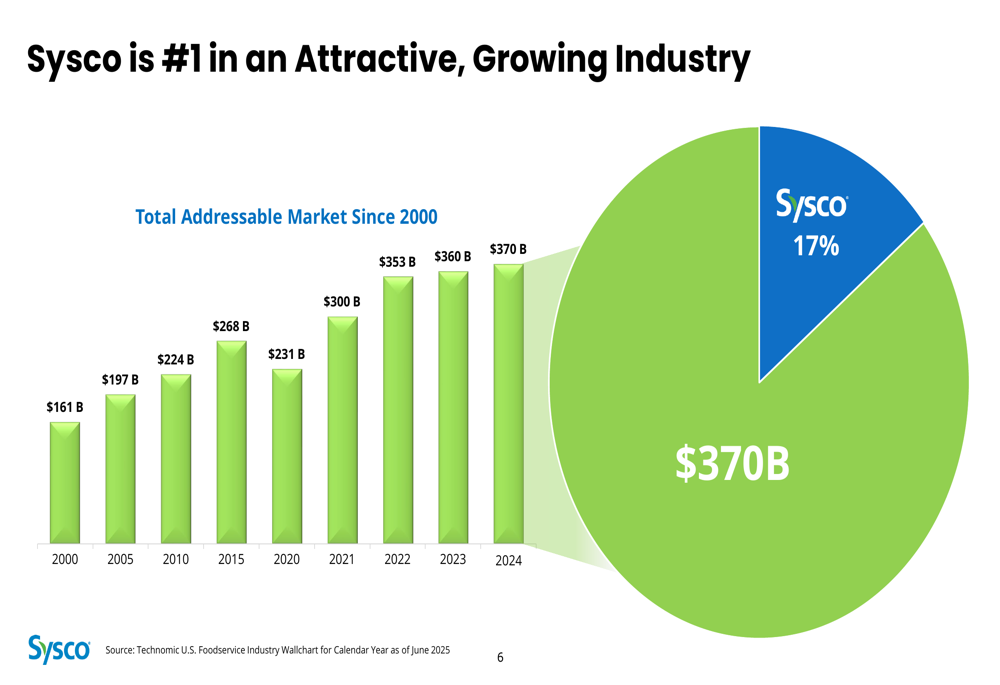

Sysco maintains its leadership position in the foodservice distribution industry, holding 17% market share of a growing total addressable market that has expanded from $161 billion in 2000 to $370 billion in 2024.

The following chart illustrates Sysco’s market position and the growth of the total addressable market:

Quarterly Performance Highlights

Sysco’s fourth quarter results showed meaningful improvement compared to the previous quarter, with revenue growth of 2.8% to $21.1 billion and gross profit increasing 3.9% to $4.0 billion. Adjusted operating income rose 1.1% to $1.1 billion, while adjusted EPS grew 6.5% to $1.48.

The company’s premarket trading indicated a decline of 1.74% to $78.95, suggesting some investor caution despite the improved performance.

The following slide summarizes Sysco’s key Q4 2025 financial metrics:

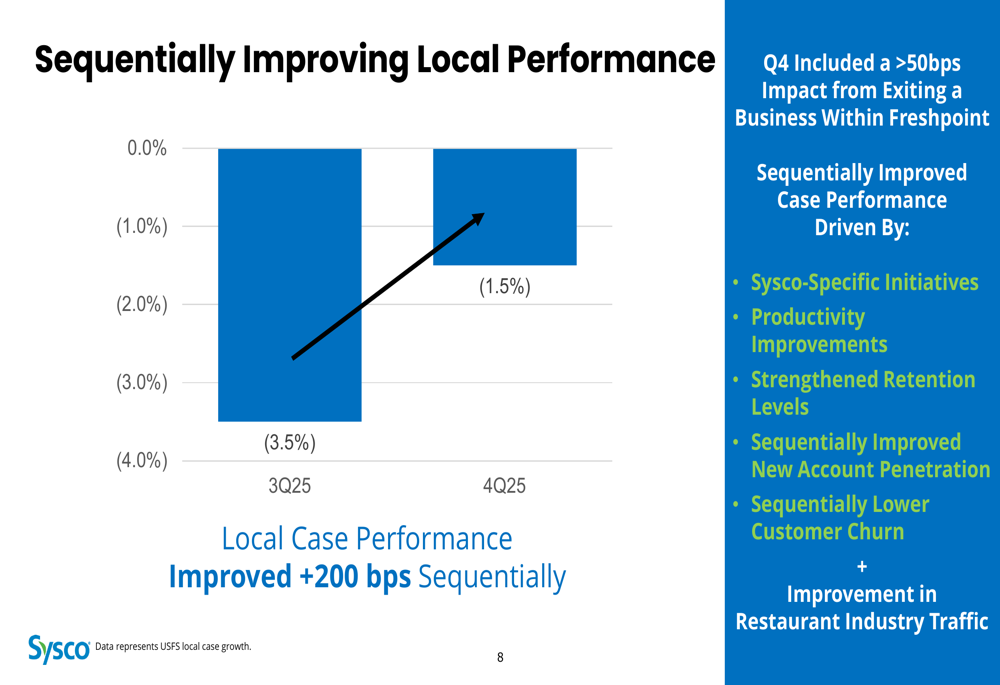

A particularly encouraging sign was the sequential improvement in U.S. Foodservice Solutions (USFS) local case growth, which improved by 200 basis points from Q3 2025 to Q4 2025. While local case volume was still down 1.5% year-over-year in Q4, this represented a significant improvement from the 3.5% decline in Q3.

As illustrated in this chart showing the sequential improvement in local performance:

Segment Analysis

Sysco’s U.S. Foodservice segment, which accounts for the largest portion of the company’s business, reported net sales of $14.8 billion in Q4, up 2.4% year-over-year. However, adjusted operating income for this segment decreased 0.8% to $1.1 billion. Despite the decline in operating income, gross profit dollars increased 2.8% to $2.9 billion, driven by structural improvements from strategic sourcing efforts.

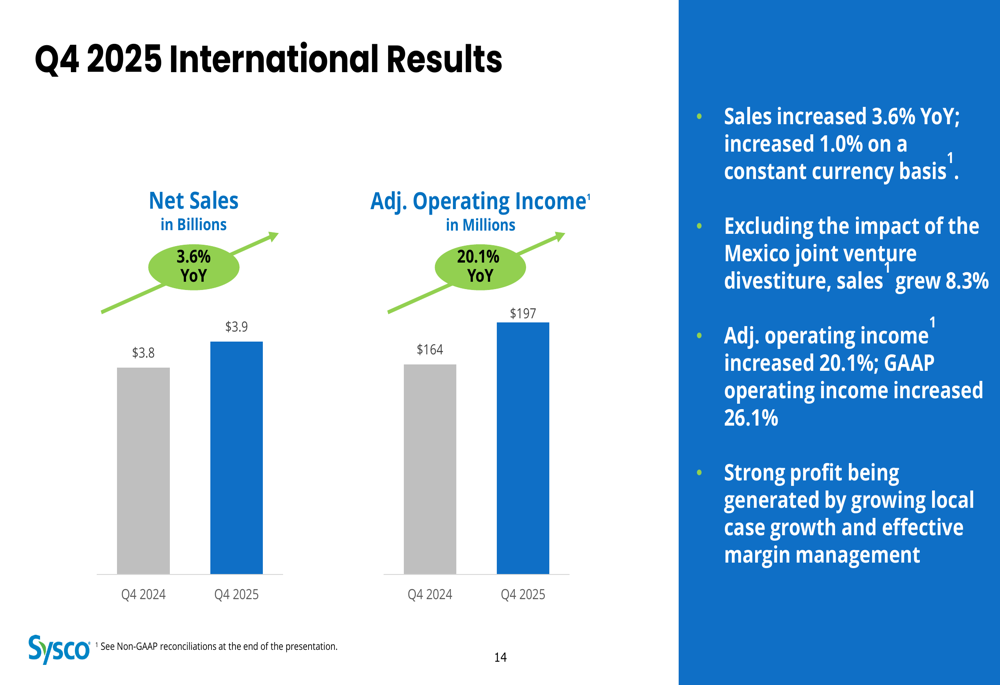

The International segment was the standout performer in Q4, with net sales increasing 3.6% to $3.9 billion (1.0% on a constant currency basis). Excluding the impact of the Mexico joint venture divestiture, international sales grew by an impressive 8.3%. Adjusted operating income for the segment surged 20.1% to $197 million, demonstrating strong profit generation through effective margin management and revenue growth.

The following chart details the International segment’s performance:

The SYGMA segment, which focuses on chain restaurant customers, also performed well with net sales increasing 5.9% to $2.2 billion and operating income rising 3.8% to $27 million. This continued growth follows a strategic shift to a more favorable customer mix within the segment.

Full-Year 2025 Results

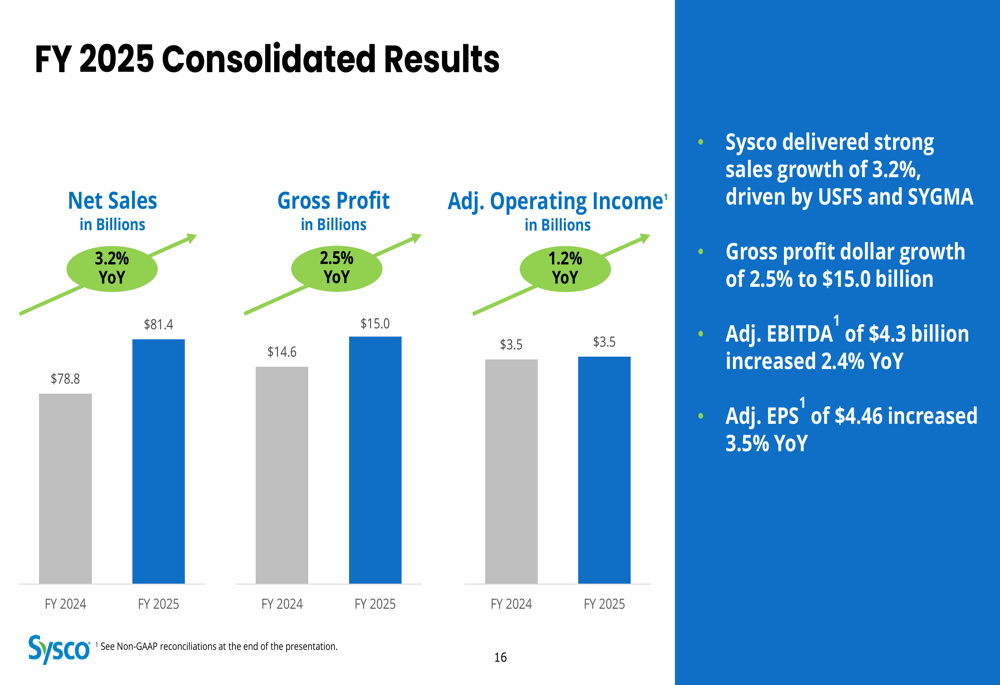

For the full fiscal year 2025, Sysco reported net sales of $81.4 billion, representing growth of 3.2% compared to fiscal 2024. Gross profit increased 2.5% to $15.0 billion, while adjusted operating income rose 1.2% to $3.5 billion. Adjusted EPS for the year was $4.46, up 3.5% year-over-year.

The company’s full-year consolidated results are summarized in the following slide:

Sysco returned $2.25 billion to shareholders through share repurchases and dividends during fiscal 2025, continuing its strong track record of shareholder returns. The company’s net debt to adjusted EBITDA ratio increased slightly from 2.69x in FY24 to 2.85x in FY25, which is marginally above its target range of 2.5-2.75x.

The company remains on track to return approximately $21.5 billion in cumulative cash to shareholders over a 12-year period from FY15 to FY26, underscoring its commitment to delivering shareholder value.

Strategic Initiatives

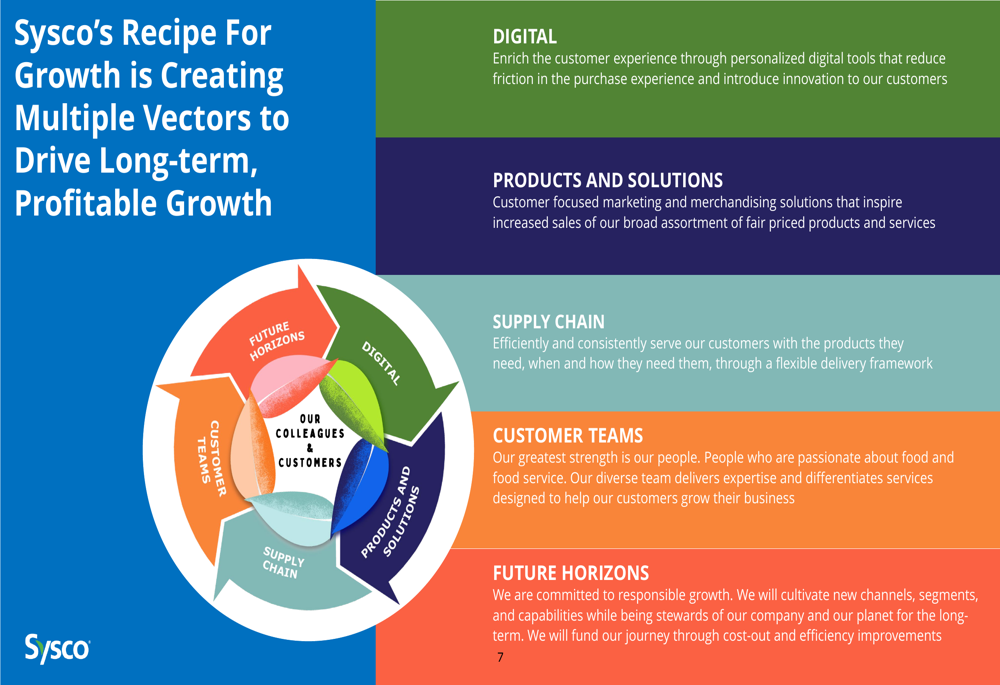

Sysco outlined its "Recipe For Growth" strategy, which focuses on multiple vectors to drive long-term, profitable growth. The strategy encompasses five key areas: digital tools to enhance customer experience, customer-focused marketing and merchandising solutions, supply chain efficiency, customer teams delivering expertise and differentiated services, and future horizons to cultivate new channels and capabilities.

The following diagram illustrates Sysco’s growth strategy framework:

For fiscal 2026, Sysco is focusing on three key growth initiatives: Sysco Perks!, AI360, and Pricing Agility. These initiatives are designed to enhance customer loyalty, leverage artificial intelligence for operational improvements, and optimize pricing strategies to drive profitability.

FY 2026 Outlook & Guidance

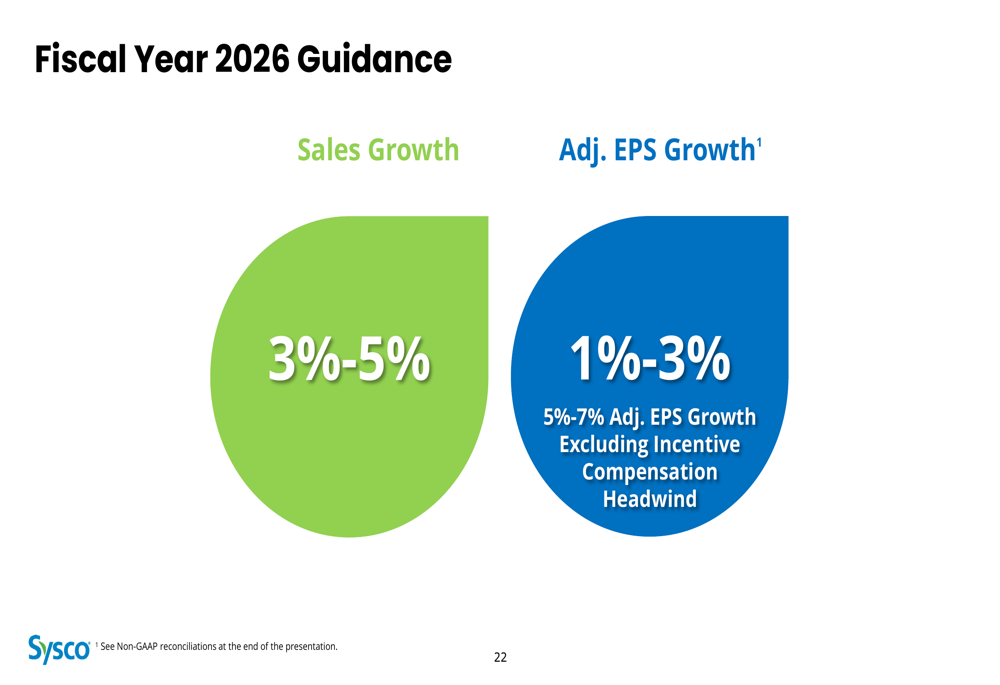

Looking ahead to fiscal 2026, Sysco provided guidance for sales growth of 3-5% and adjusted EPS growth of 1-3%. However, the company noted that excluding the approximately $100 million impact from incentive compensation headwinds, adjusted EPS growth would be in the range of 5-7%, which aligns with its long-term growth algorithm.

The following slide outlines Sysco’s fiscal 2026 guidance:

The incentive compensation headwind is expected to affect each quarter of fiscal 2026, with the most significant impact of $63 million occurring in the third quarter.

This outlook represents a recovery from the challenges faced in the third quarter of fiscal 2025, when Sysco missed both EPS and revenue forecasts. The sequential improvement in local case growth and strong international performance suggest that the company’s strategic initiatives are gaining traction as it enters fiscal 2026.

Sysco’s position as the market leader in foodservice distribution, combined with the ongoing shift toward food away from home and its focused growth initiatives, positions the company to continue delivering value to shareholders despite near-term challenges in the U.S. market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.