Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Tandem Diabetes Care (NASDAQ:TNDM) presented its company overview on August 6, 2025, highlighting its position in the diabetes technology market and strategic initiatives. The presentation comes as the company’s stock trades at $15.15, near its 52-week low of $13.94, despite showing strong revenue growth in recent quarters.

The diabetes technology company emphasized the significant market opportunity, noting that less than 40% of approximately 2 million people with type 1 diabetes in the U.S. use an insulin pump, while the penetration rate is even lower internationally at less than 20%. For people with type 2 insulin-intensive diabetes, only about 5% of more than 2 million patients in the U.S. currently use an insulin pump.

As shown in the following overview of Tandem’s key strengths and market position:

Strategic Initiatives

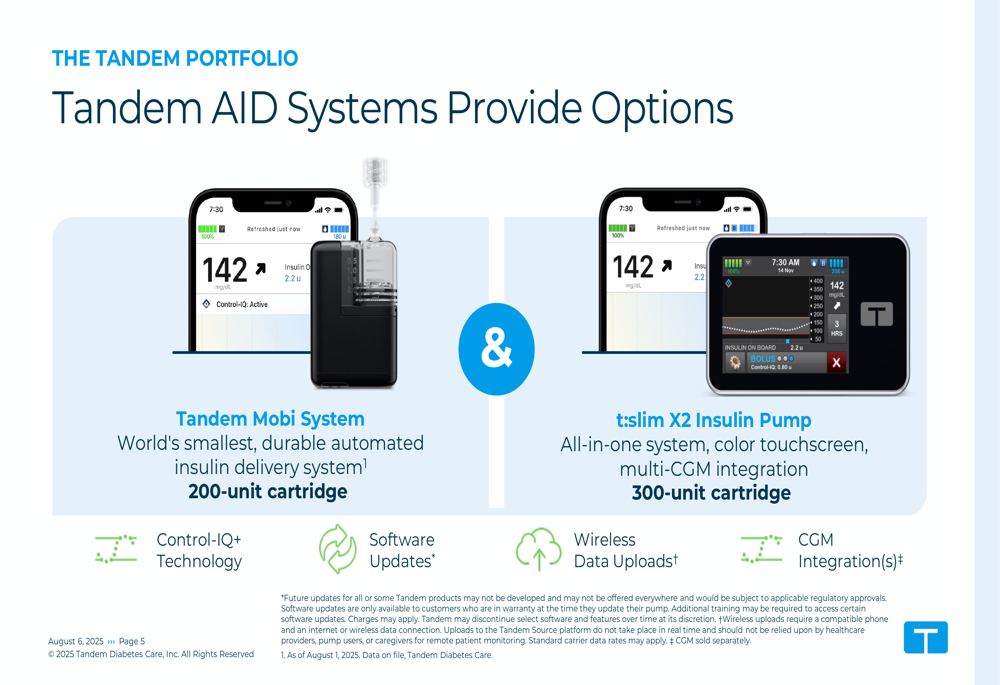

Tandem’s core strategy centers on its dual insulin delivery platform approach, offering both the compact Tandem Mobi system and the feature-rich t:slim X2 insulin pump. This strategy allows healthcare providers and patients to select the device that best fits individual needs and lifestyles.

The Tandem Mobi system, described as the "world’s smallest durable automated insulin delivery system," is 55% smaller than other insulin pumps and offers multiple wearing options. The company reported that 95% of Early Access Participants are satisfied with the product. Meanwhile, the t:slim X2 insulin pump features a color touchscreen and is the first insulin pump in the United States to integrate with three continuous glucose monitoring sensors.

The following slide illustrates the company’s two primary insulin delivery systems:

A key competitive advantage for Tandem is its integration with multiple continuous glucose monitoring (CGM) systems. The t:slim X2 pump is compatible with Dexcom (NASDAQ:DXCM) G6, Dexcom G7, and Abbott FreeStyle Libre 2 Plus, while the Tandem Mobi supports Dexcom G6 and G7. This compatibility matrix provides patients with more choices in their diabetes management:

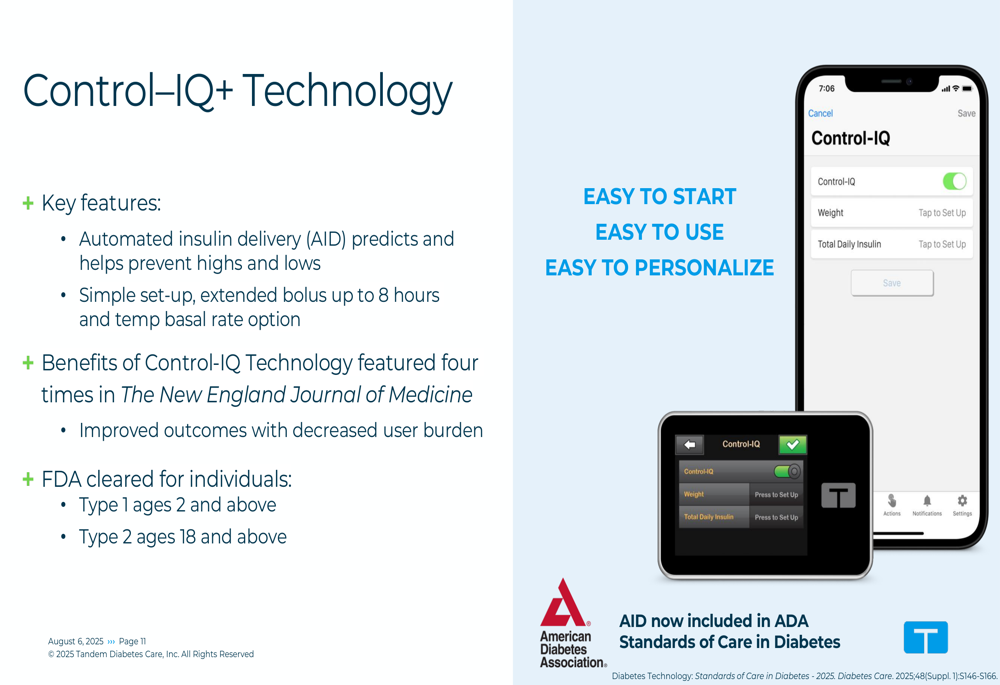

Both systems are powered by Tandem’s Control-IQ+ Technology, an automated insulin delivery system that predicts and helps prevent high and low blood glucose levels. The technology has been featured four times in The New England Journal of Medicine and is FDA-cleared for individuals with type 1 diabetes ages 2 and above and type 2 diabetes ages 18 and above.

The following slide details the key features and benefits of Control-IQ+ Technology:

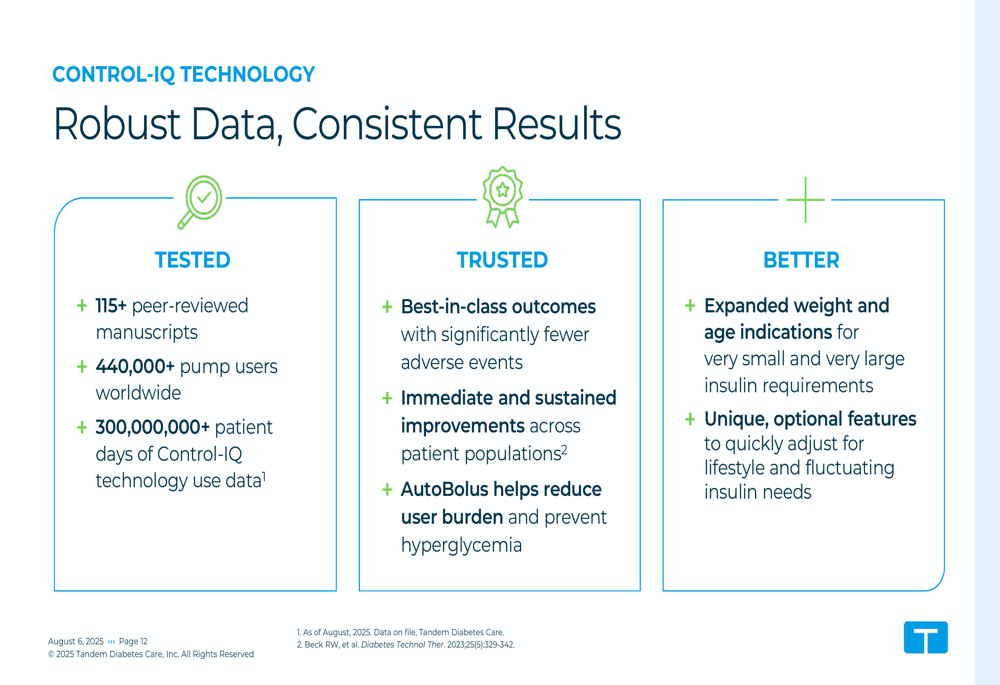

Tandem emphasized the robust clinical validation behind its technology, with over 115 peer-reviewed manuscripts and data from more than 300 million patient days of Control-IQ technology use:

Financial Performance & Targets

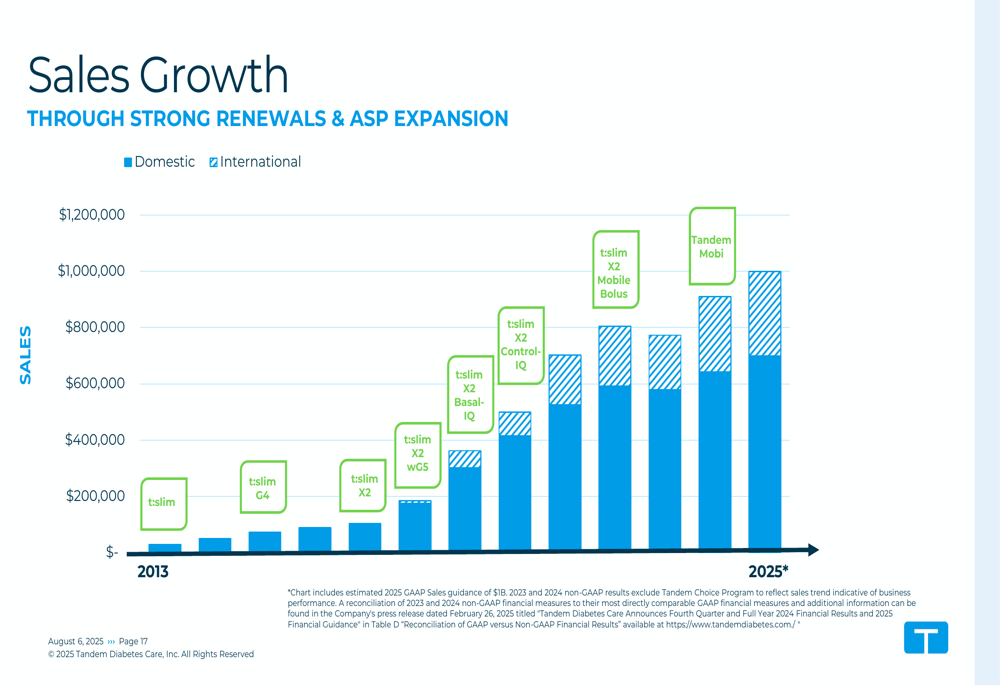

While the presentation focused primarily on product innovation and market opportunity, it’s worth noting that Tandem’s Q1 2025 financial results showed mixed performance. The company reported revenue of $234 million, representing a 22% year-over-year increase, with U.S. sales up 15% to $151 million and international sales surging 35% to $84 million. However, the company posted an EPS of -1.97, significantly missing the forecast of -0.6.

The company’s historical sales growth chart shows steady expansion, with particular acceleration in international markets:

Tandem outlined its long-term financial targets of 65% gross margin and 25% operating margin, though current performance remains below these goals. As of Q1 2025, the company reported a gross margin of 51% with a target of 54% for the full year 2025.

The company’s pricing model generates approximately $7-8K per patient in a four-year reimbursement cycle, with revenue split between the initial pump purchase (reimbursed every 4 years) and ongoing supplies (cartridges and infusion sets).

Growth Drivers & Pipeline

Tandem identified several key growth drivers for the near term, including scaling the launch of Tandem Mobi (with Android and international availability beginning in 2025), worldwide integration with Abbott FreeStyle Libre 3 Plus, an expanded U.S. sales force, and increasing pharmacy channel access.

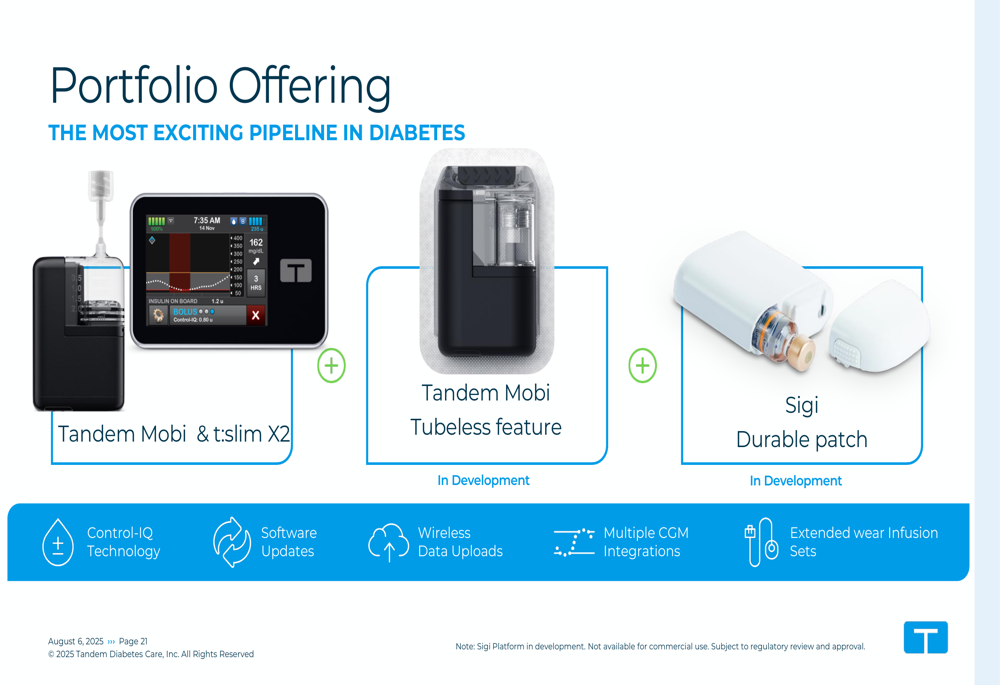

The company’s product pipeline includes further innovations such as a tubeless version of Tandem Mobi and the Sigi Durable patch, as illustrated in this portfolio roadmap:

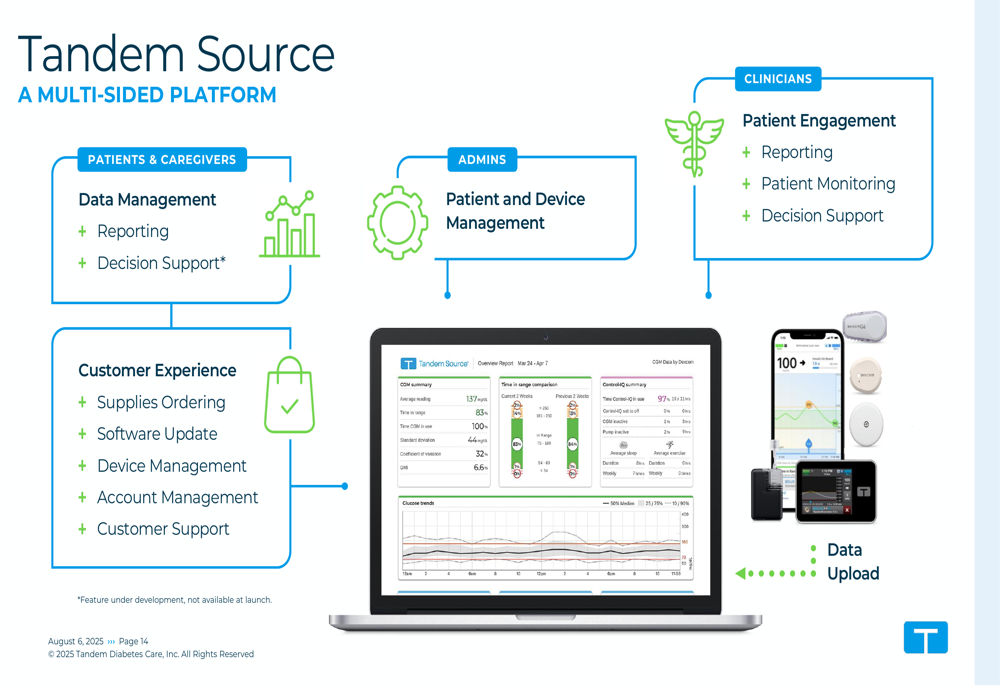

Tandem is also expanding its digital ecosystem through the Tandem Source platform, which serves as a multi-sided platform connecting patients, caregivers, clinicians, and administrators. The platform facilitates data management, reporting, decision support, and customer experience functions:

Forward-Looking Statements

Looking ahead, Tandem projects 2025 worldwide sales between $997 million and $1 billion, with U.S. sales expected to range from $725 million to $730 million and international sales anticipated to reach $272 million to $277 million. The company aims to achieve a gross margin of 54% in 2025 and return to positive free cash flow in the second half of the year.

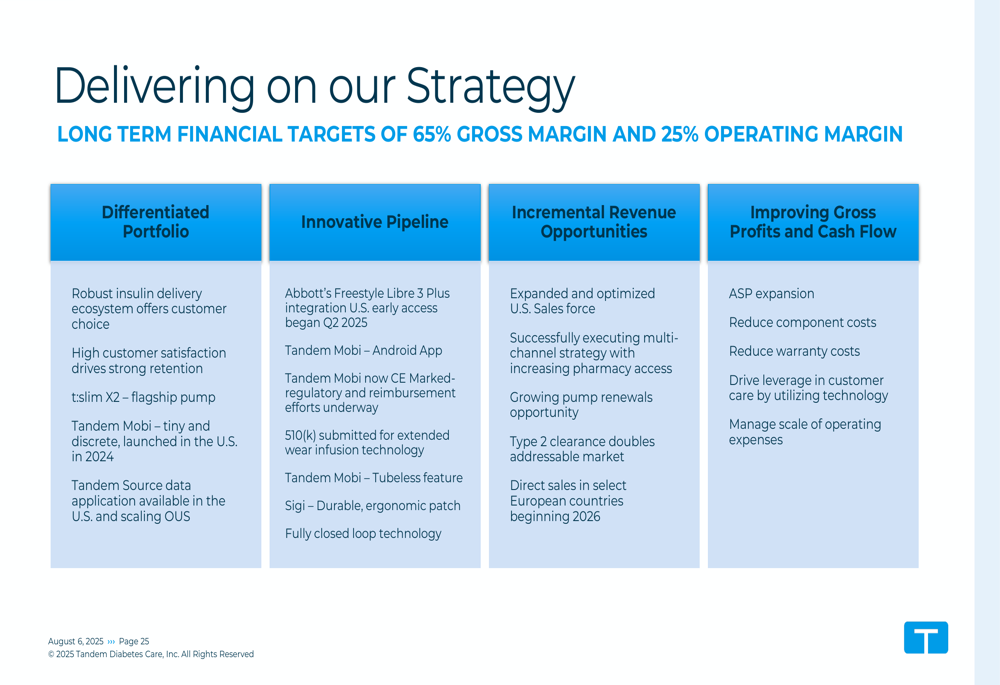

The company’s strategic framework focuses on four core elements: differentiated portfolio, innovative pipeline, incremental revenue opportunities, and improving gross profits and cash flow:

Despite the optimistic outlook presented, investors should note the significant EPS miss in Q1 2025 and the stock’s current trading near 52-week lows, suggesting challenges in translating revenue growth into profitability. The company’s success will depend on efficient execution of its dual-platform strategy, international expansion, and progress toward its stated margin targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.