Stock market today: S&P 500 ekes gain as hopes for end of shutdown get major boost

Tantalus Systems Holding Inc (TSX:GRID) (OTCQX:TGMPF) reported strong financial results for the second quarter of 2025, with revenue increasing 22% year-over-year to $13.1 million. The company’s latest corporate presentation, released on August 7, 2025, highlights its continued momentum in the grid modernization market and the growing adoption of its TRUSense Gateway technology.

Introduction & Market Context

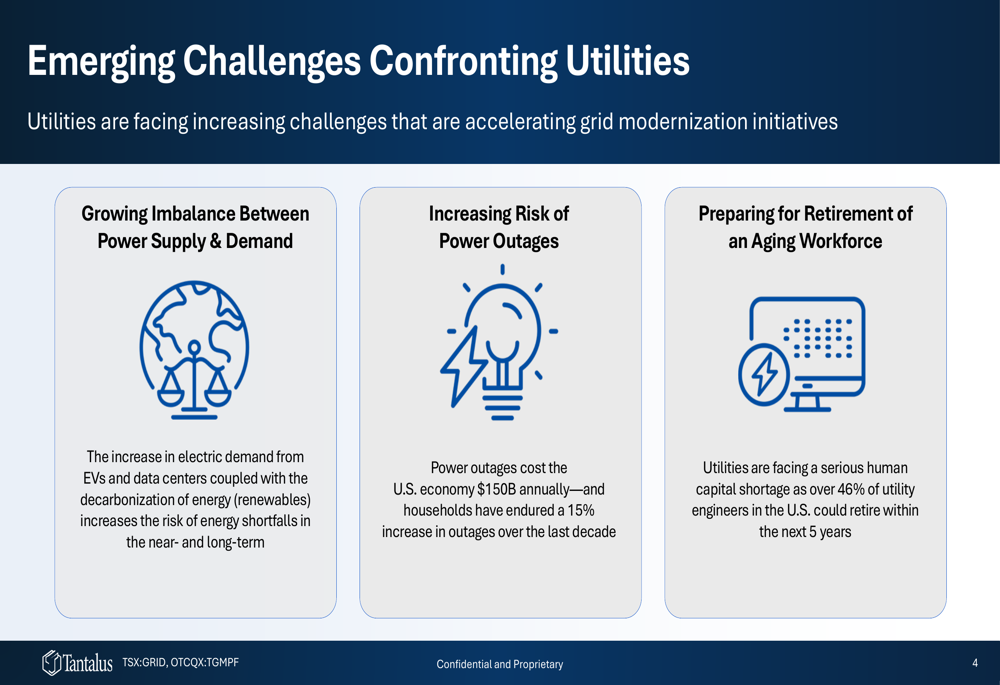

Tantalus positions itself as a "pure-play technology company focused on grid modernization," addressing critical challenges facing utilities today. The company’s presentation identifies three key industry challenges: growing imbalance between power supply and demand, increasing risk of power outages, and the impending retirement of an aging workforce.

According to the presentation, power outages cost the U.S. economy $150 billion annually, with households experiencing a 15% increase in outages over the last decade. Additionally, over 46% of utility engineers in the U.S. could retire within the next five years, creating a significant human capital shortage.

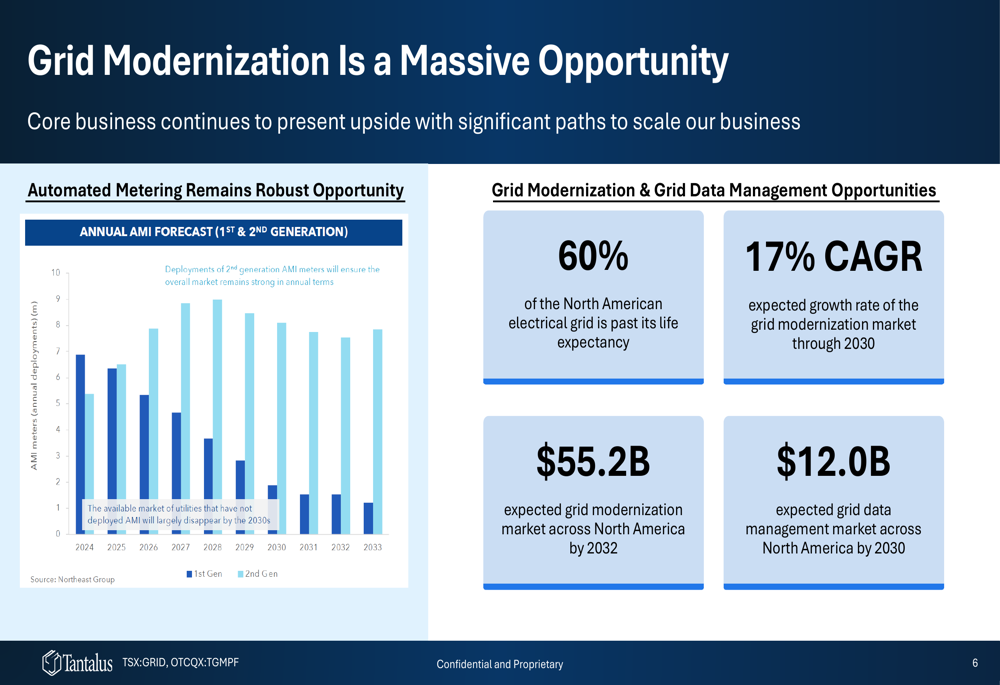

The grid modernization market represents a substantial opportunity, with an expected 17% CAGR through 2030 and a projected North American market size of $55.2 billion by 2032. Tantalus aims to capitalize on this opportunity with its comprehensive platform approach.

Quarterly Performance Highlights

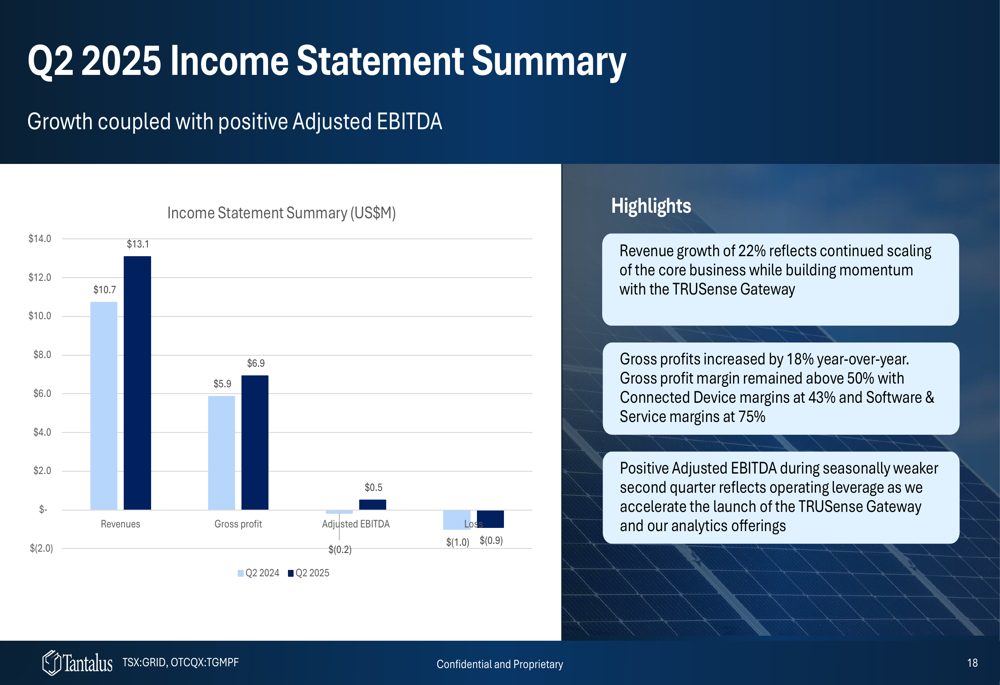

Tantalus reported impressive financial results for Q2 2025, with revenue growing 22% year-over-year to $13.1 million. The company achieved positive Adjusted EBITDA of $0.5 million, a significant improvement from the -$0.2 million reported in Q2 2024. Net loss improved slightly to $0.9 million from $1.0 million in the prior year period.

Gross profit increased by 18% year-over-year to $6.9 million, with gross profit margins remaining above 50%. The company’s Connected Device segment saw margins of 43%, while the higher-margin Software (ETR:SOWGn) & Services segment achieved 75% margins.

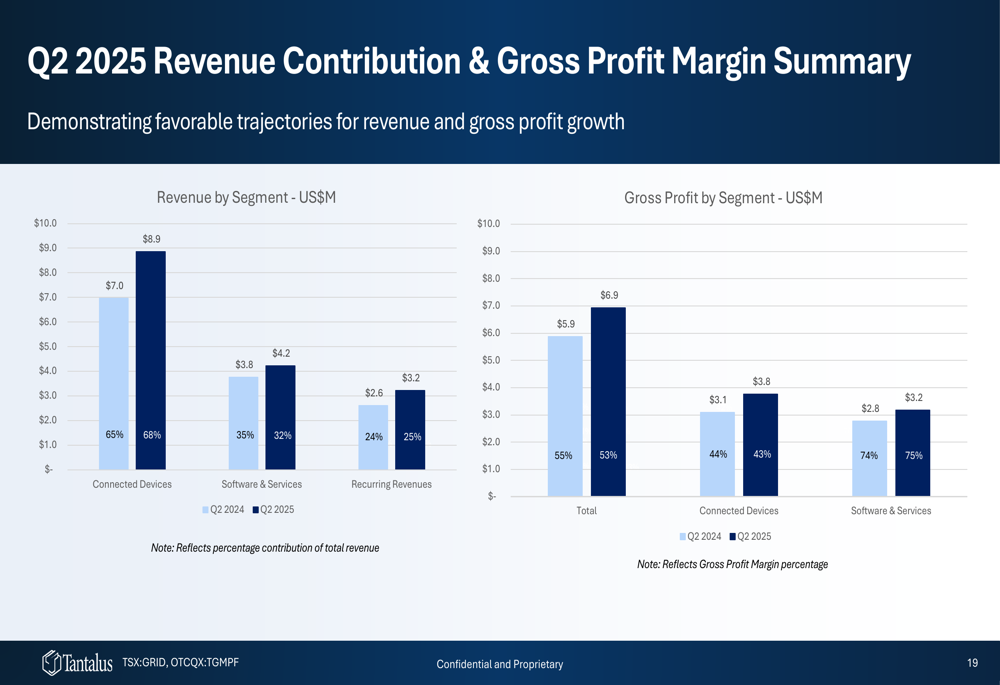

Revenue from Connected Devices grew to $8.9 million (68% of total revenue), while Software & Services revenue remained stable at $4.2 million (32% of total revenue). Recurring revenue represented 25% of total revenue, up from 24% in the prior year period.

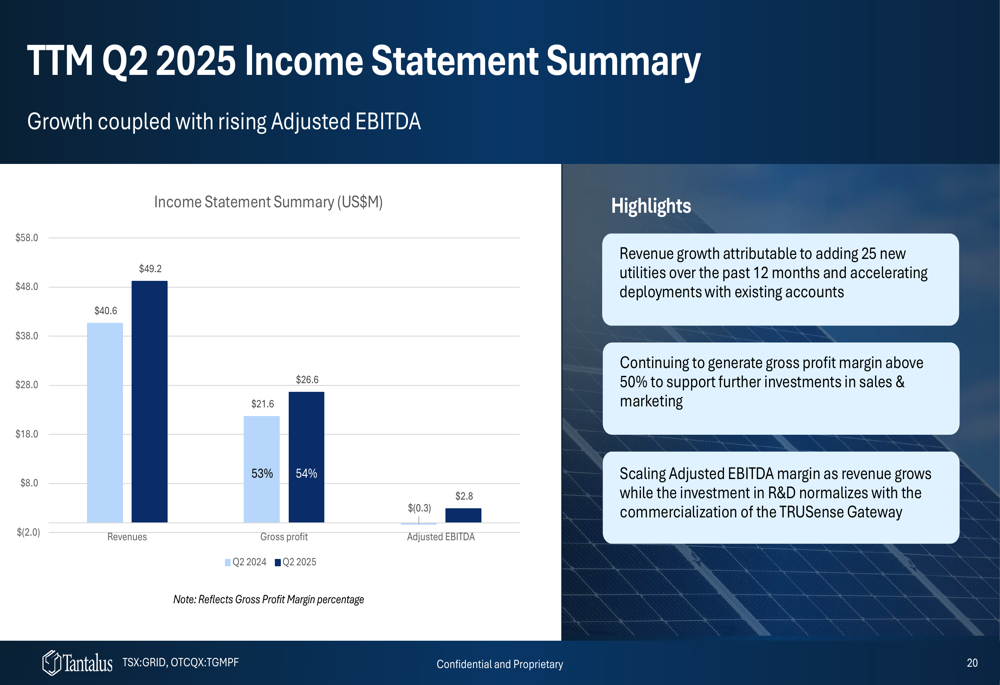

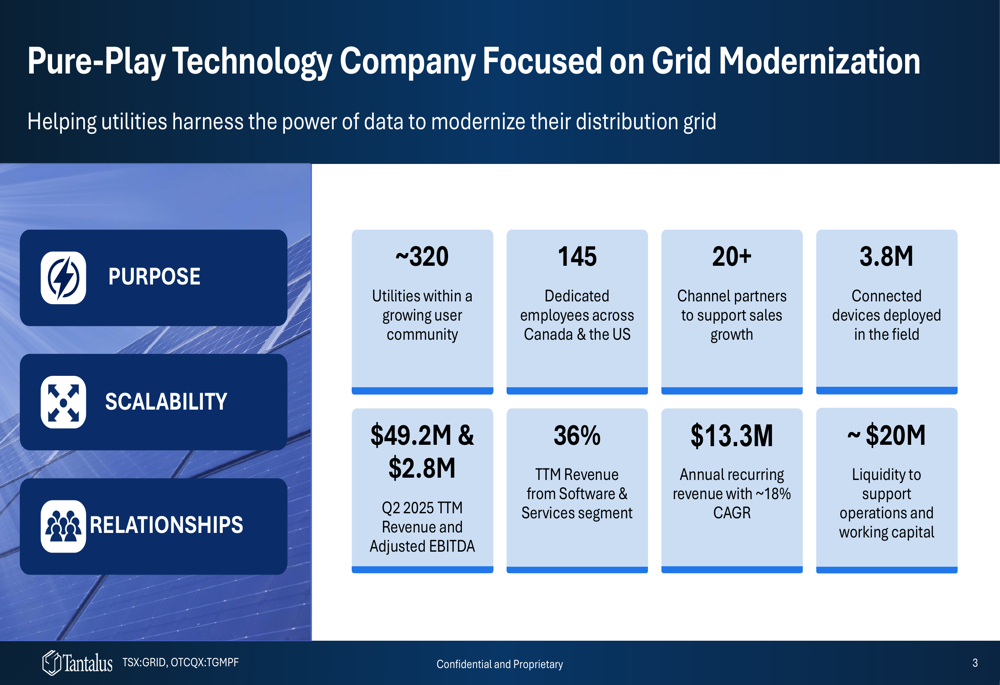

On a trailing twelve-month basis, Tantalus reported revenue of $49.2 million, up 21% from $40.6 million in the prior year period. TTM Adjusted EBITDA improved significantly to $2.8 million from -$0.3 million in the prior year period, with gross profit margins expanding to 54%.

Product Strategy and Innovation

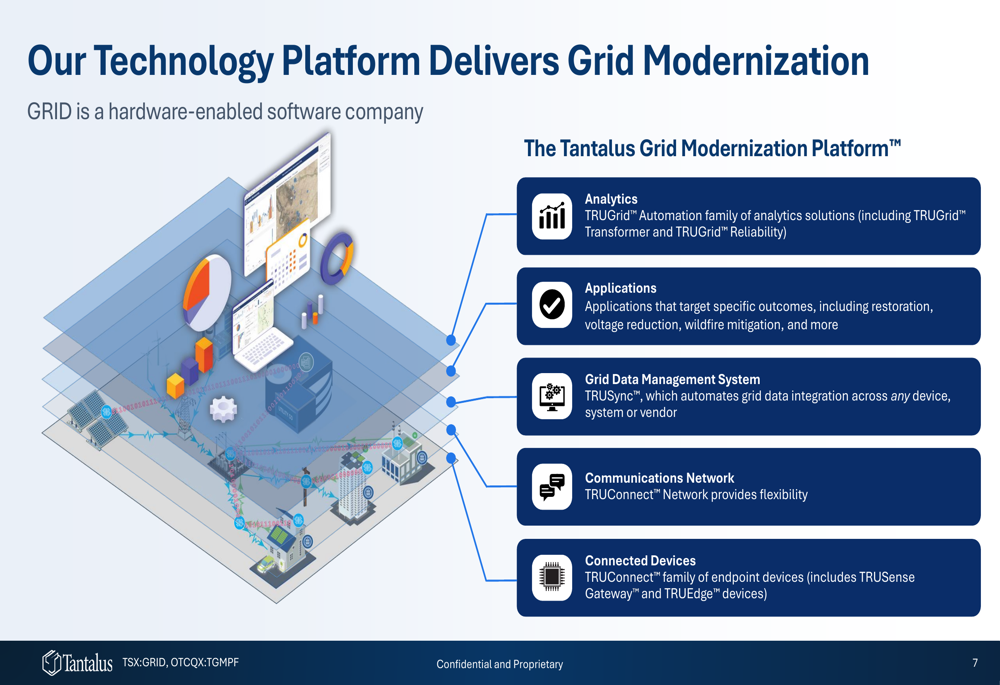

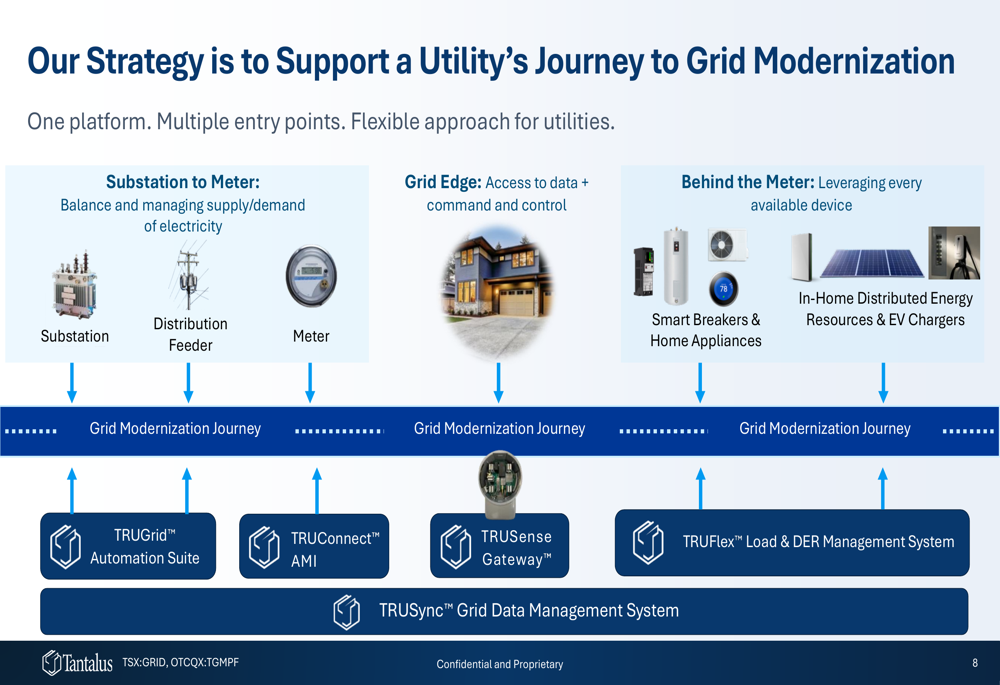

Tantalus’s growth strategy centers around its Grid Modernization Platform, which includes analytics, applications, grid data management, communications networks, and connected devices. The platform is designed to provide utilities with a comprehensive solution for modernizing their grid infrastructure.

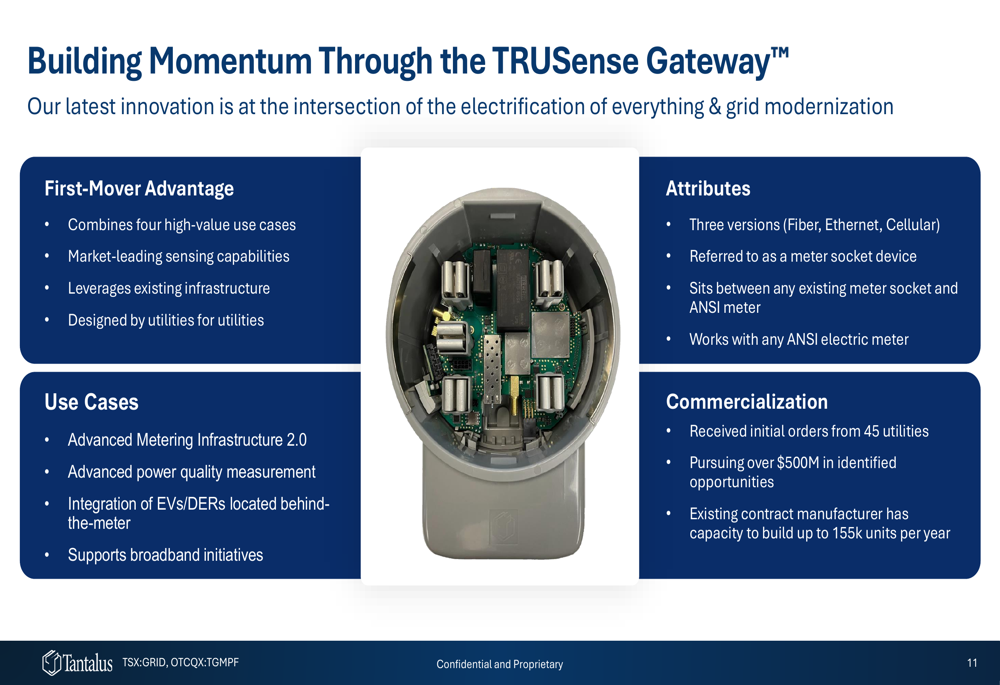

The company’s TRUSense Gateway product represents a significant growth opportunity. This device sits between any existing meter socket and ANSI meter, providing advanced metering infrastructure, power quality measurement, integration of EVs/DERs, and support for broadband initiatives. According to the presentation, Tantalus has received initial orders from 45 utilities and is pursuing over $500 million in identified opportunities for this product.

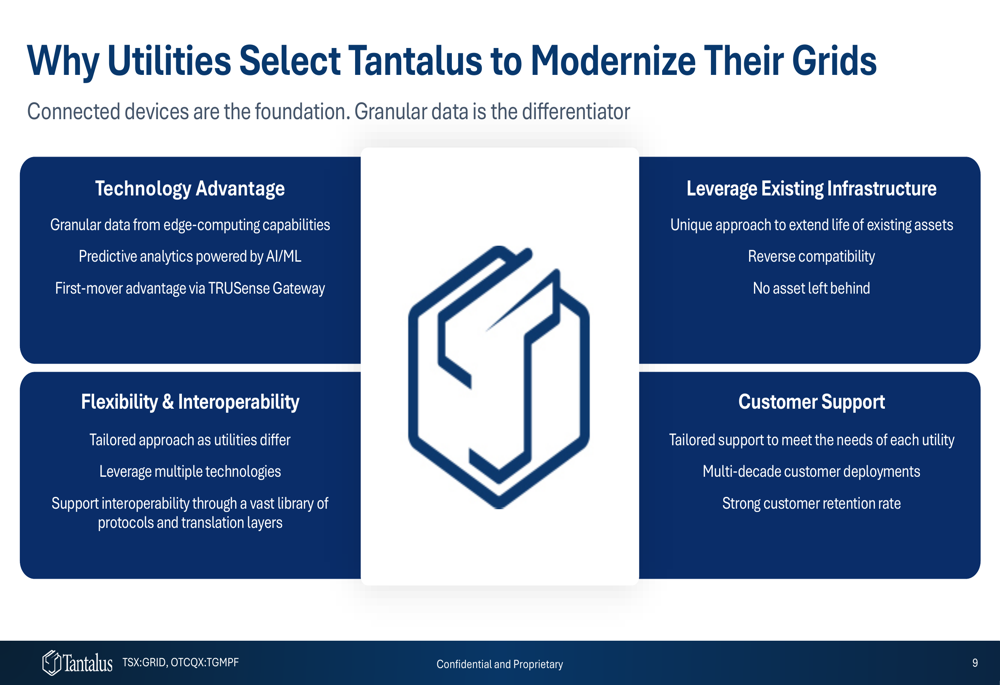

Tantalus differentiates itself through its technology advantage, ability to leverage existing infrastructure, flexibility and interoperability, and customer support. The company’s approach allows utilities to extend the life of existing assets rather than requiring complete replacement.

Financial Analysis and Outlook

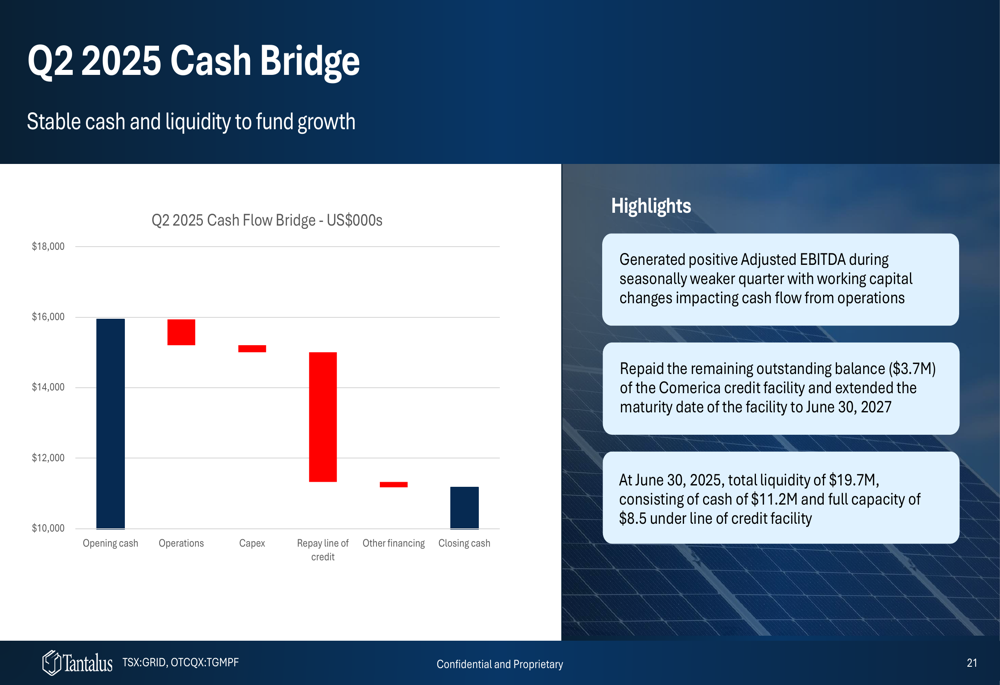

Tantalus maintained a strong liquidity position at the end of Q2 2025, with total liquidity of $19.7 million, consisting of $11.2 million in cash and $8.5 million available under its line of credit facility. The company repaid the remaining $3.7 million of its Comerica (NYSE:CMA) credit facility and extended the maturity date to June 30, 2027.

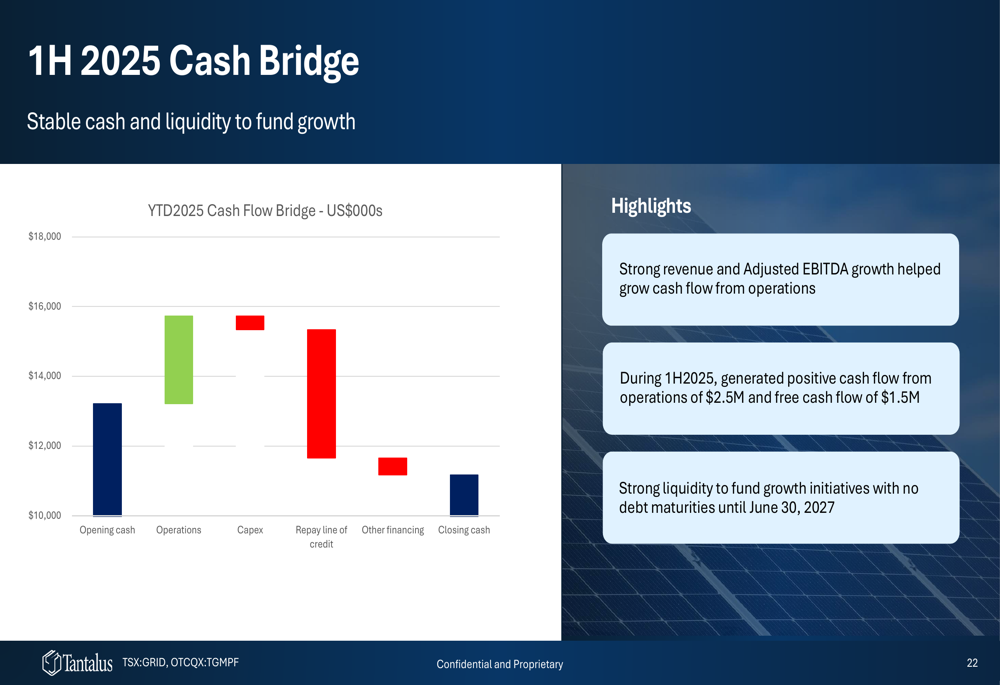

For the first half of 2025, Tantalus generated positive cash flow from operations of $2.5 million and free cash flow of $1.5 million. This strong cash position provides the company with flexibility to fund its growth initiatives.

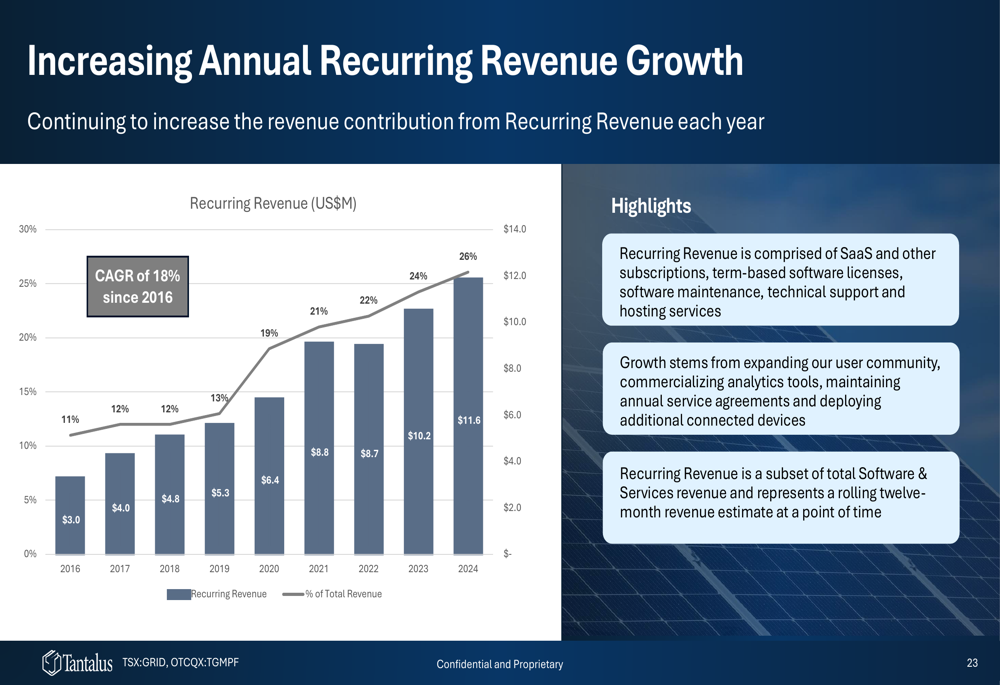

Recurring revenue continues to be a focus for Tantalus, with annual recurring revenue reaching $13.3 million and growing at an 18% CAGR since 2016. Recurring revenue is comprised of SaaS and other subscriptions, term-based software licenses, software maintenance, technical support, and hosting services.

Market Opportunity (SO:FTCE11B) and Positioning

Tantalus has built a user community of approximately 320 utilities and deployed 3.8 million connected devices in the field. The company’s platform approach allows it to address the entire utility grid, from substation to meter, grid edge, and behind the meter.

The company’s strategy involves supporting utilities’ journey to grid modernization through multiple entry points, allowing for a tailored approach that meets the specific needs of each utility. This flexibility has contributed to Tantalus’s strong customer retention rate.

Looking ahead, Tantalus is well-positioned to benefit from the growing demand for grid modernization solutions. The company’s recent stock performance reflects this positive outlook, with shares trading at $3.26 as of August 7, 2025, near the upper end of its 52-week range of $1.25 to $3.68.

The Q2 2025 results build on the momentum seen in Q1, when the company reported a 27% revenue increase to $11.9 million. While the Q1 earnings call mentioned potential tariff impacts of $700,000 to $800,000 on EBITDA for 2025, the Q2 presentation did not address this issue, suggesting the company may have found ways to mitigate these impacts.

As utilities continue to face challenges related to grid reliability, operational costs, and renewable integration, Tantalus’s data-driven approach to grid modernization positions it well for continued growth in this expanding market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.