JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Tapestry Inc (NYSE:TPR), the luxury fashion holding company behind Coach and Kate Spade, presented its fiscal year 2025 results on August 14, 2025, highlighting record performance while acknowledging upcoming challenges. Despite reporting strong full-year results, Tapestry’s stock fell 6.65% in premarket trading, suggesting investor concerns about the company’s outlook amid global trade tensions.

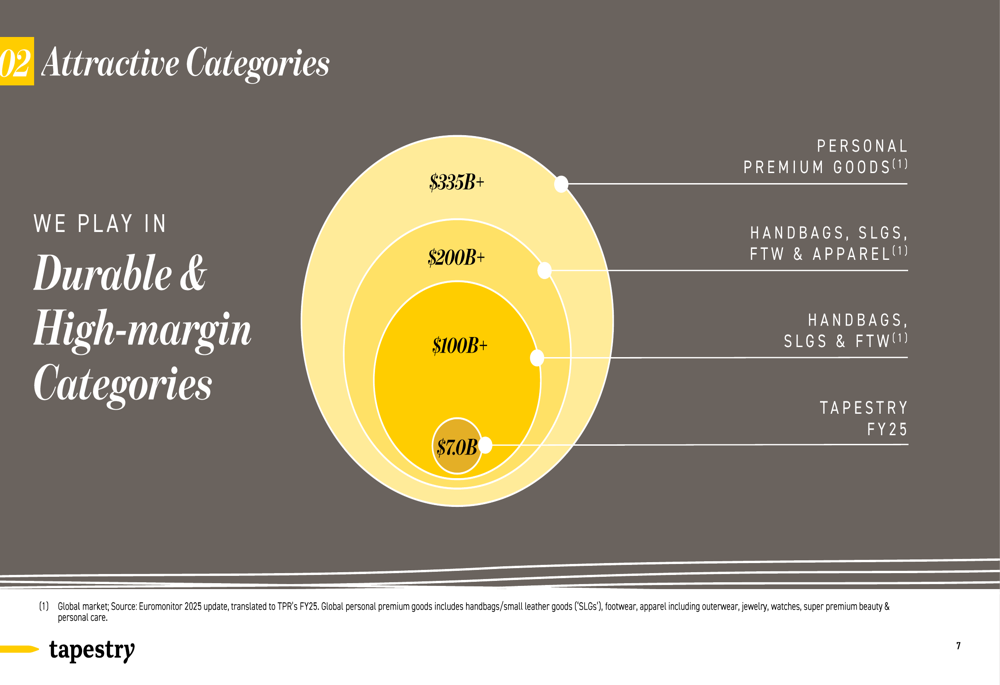

The company operates in the premium personal goods market, which it values at over $335 billion globally. Tapestry’s presentation emphasized its position within this attractive category, with its FY25 revenue of $7.0 billion representing a small but growing slice of the addressable market.

As shown in the following chart detailing Tapestry’s market positioning:

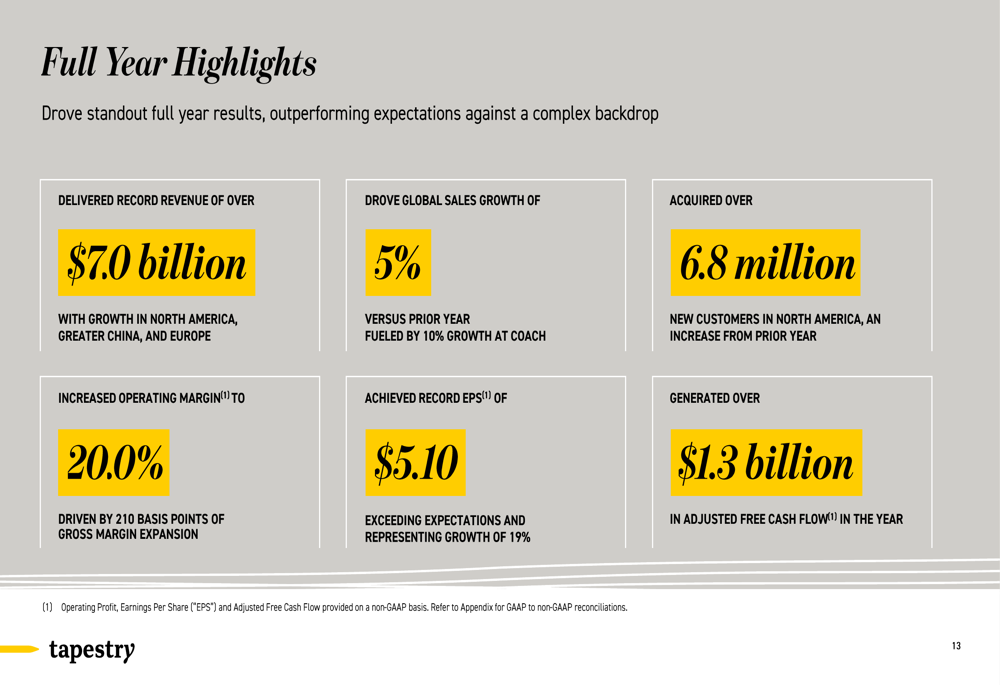

FY25 Performance Highlights

Tapestry delivered record financial results for fiscal year 2025, with revenue reaching $7.0 billion, representing 5% growth compared to the prior year. This growth was primarily fueled by Coach’s strong 10% year-over-year performance. The company achieved an operating margin of 20.0%, driven by 210 basis points of gross margin expansion, and delivered record earnings per share of $5.10, a 19% increase from the previous year.

The company’s key financial achievements for FY25 are summarized in this slide:

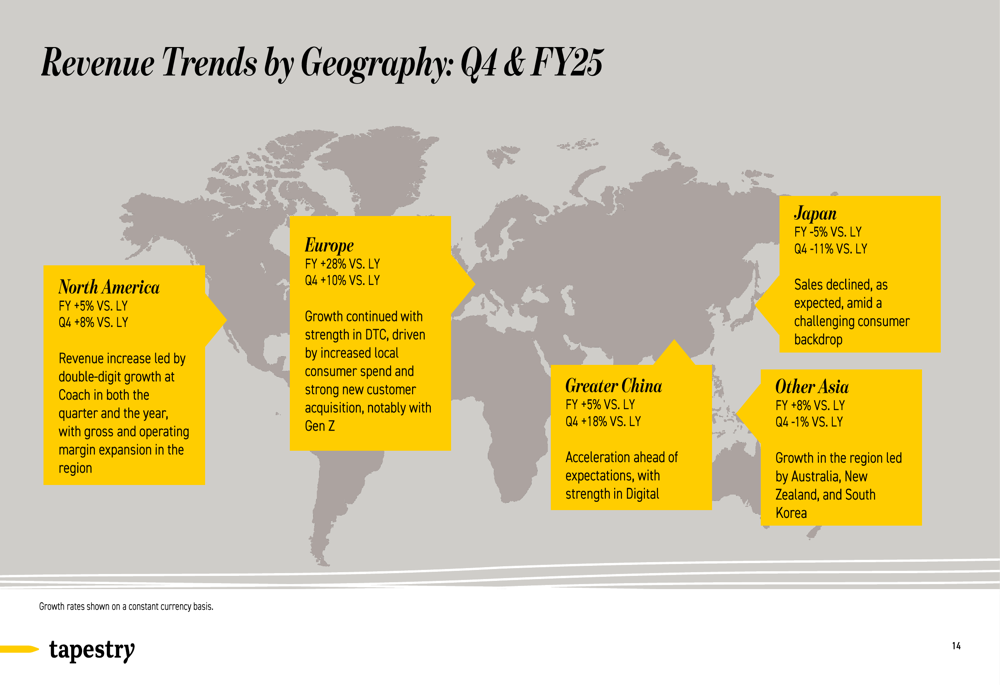

Geographically, Tapestry saw growth across most regions, with particularly strong performance in North America (+5%), Europe (+28%), and Greater China (+5%). The company’s Q4 results showed acceleration in Greater China (+18%) and North America (+8%), though Japan experienced declines amid challenging consumer conditions.

The following geographical breakdown illustrates these regional trends:

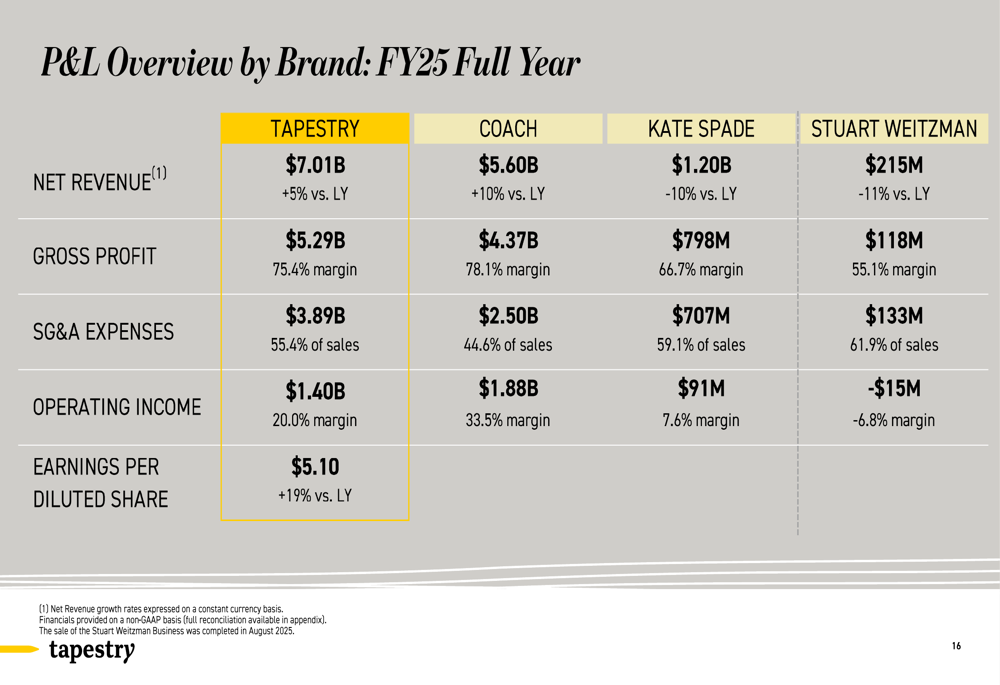

Brand-Specific Performance

Tapestry’s portfolio showed divergent performance across its brands. Coach delivered exceptional results with 10% revenue growth for the full year, reaching $5.6 billion. The brand’s gross profit margin expanded to 78.1%, demonstrating its premium positioning and operational efficiency.

In contrast, Kate Spade struggled with a 10% revenue decline to $1.2 billion, though it maintained a respectable gross margin of 66.7%. Stuart Weitzman, which Tapestry divested in August 2025, saw an 11% revenue decline to $215 million.

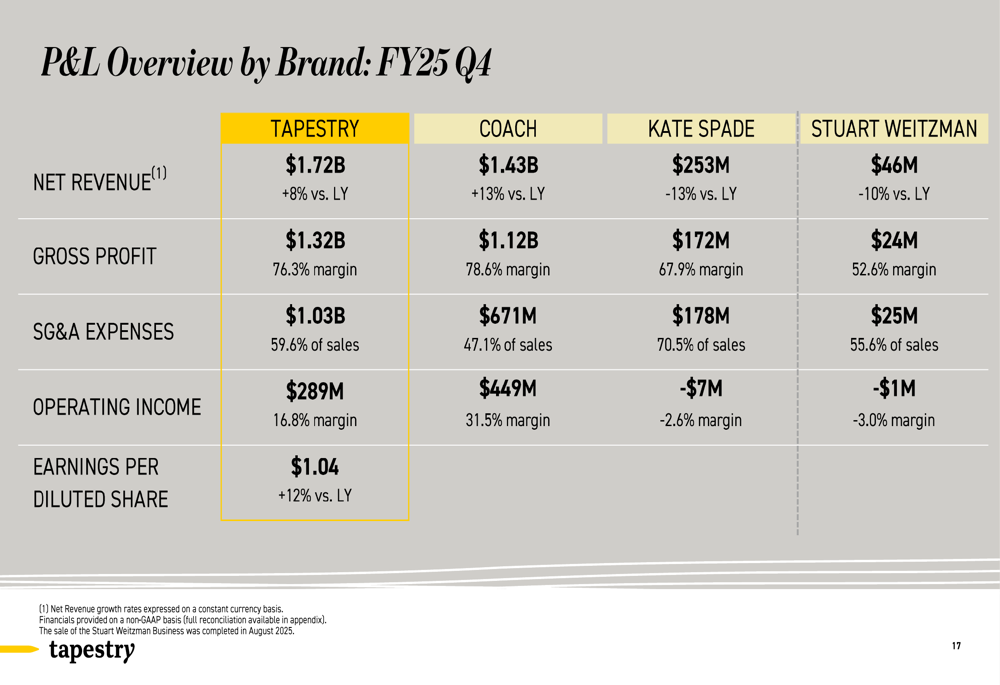

The detailed financial breakdown by brand is illustrated in this comprehensive P&L overview:

For the fourth quarter specifically, Coach continued its strong momentum with 13% revenue growth, while Kate Spade’s challenges persisted with a 13% decline:

Coach’s success was attributed to its distinctive "Expressive Luxury" positioning and strong appeal to younger consumers. The brand welcomed over 4.6 million new customers in North America during FY25, with nearly 70% being Gen Z and Millennials who transacted at higher average unit retail prices than other customer segments.

Coach’s revenue is well-diversified across categories, geographies, and channels, as shown in this breakdown:

Meanwhile, Kate Spade has been implementing strategic initiatives to strengthen its position, including launching campaigns featuring Gen Z celebrities Ice Spice and Charli D’Amelio to drive brand engagement. The brand’s revenue distribution shows a heavier concentration in North America compared to Coach:

Fiscal 2026 Outlook & Challenges

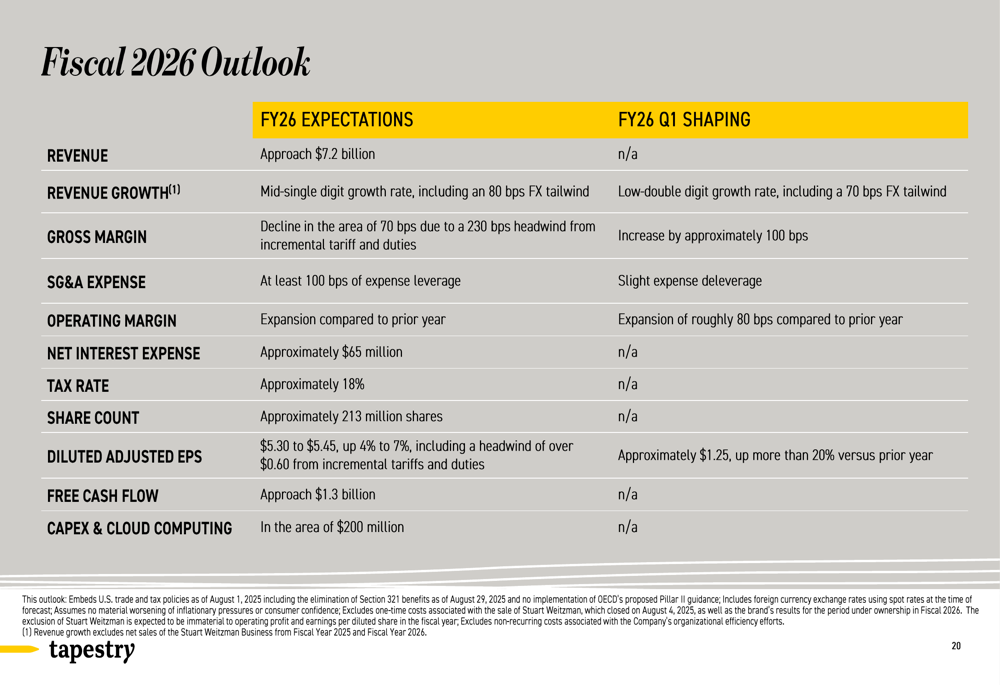

Looking ahead to fiscal 2026, Tapestry expects revenue to approach $7.2 billion, representing mid-single-digit growth including an 80 basis point foreign exchange tailwind. However, the company anticipates gross margin pressure due to a 230 basis point headwind from incremental tariffs and duties.

Despite these challenges, Tapestry projects earnings per share of $5.30 to $5.45, representing 4% to 7% growth, and expects to generate approximately $1.3 billion in free cash flow.

The detailed FY26 outlook is presented in this comprehensive guidance slide:

CEO Joanne Crevoiserat emphasized the company’s resilience: "Fiscal 2025 was a breakout year for Tapestry as our systemic approach to brand-building is capturing a new generation of consumers around the world. Our strong growth, capped by our fourth quarter outperformance, reinforces that our strategies are working."

The company highlighted its structural advantages to navigate trade challenges, including a flexible direct-to-consumer model, global scale, and an agile supply chain. These factors are expected to help mitigate the impact of increased tariffs and duties in the coming year.

Shareholder Value & Capital Allocation

Tapestry demonstrated its commitment to shareholder returns by executing a $2 billion Accelerated Share Repurchase program expected to be completed in Q1 FY26, with an estimated average purchase price of approximately $78 per share. The company plans to repurchase an additional $800 million in shares during FY26.

Additionally, Tapestry increased its dividend by 14% to an annual rate of $1.60 per share for FY26, following $300 million in dividend payments during FY25. In total, the company returned $2.3 billion to shareholders in FY25 alone.

The following slide details Tapestry’s shareholder return initiatives:

Strategic Initiatives & Competitive Positioning

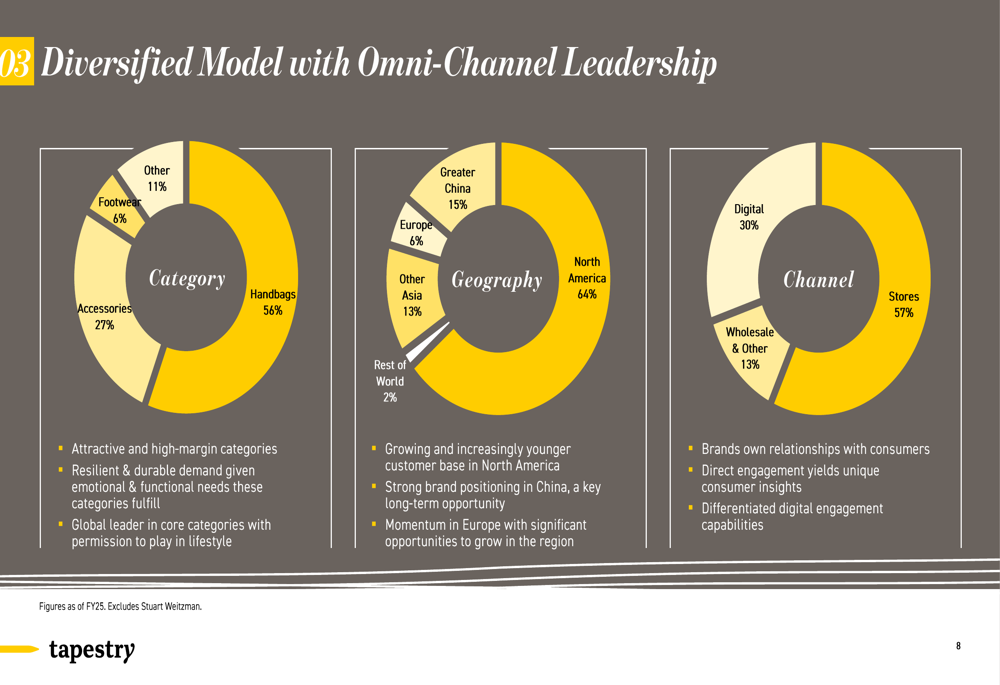

Tapestry’s presentation highlighted five key competitive advantages: iconic brands, attractive categories, omni-channel leadership, global platform, and talented team. The company emphasized its diversified business model across product categories, geographies, and sales channels.

The company’s channel mix shows a strong direct-to-consumer focus, with 57% of sales through stores and 30% through digital channels, demonstrating its omni-channel capabilities:

Tapestry also highlighted its corporate responsibility initiatives under the ambition "Make Every Beautiful Choice a Responsible Choice," including workplace recognition, environmental commitments, community service, and sustainable materials development:

CFO and COO Scott Roe expressed confidence in the company’s outlook: "We delivered another record-breaking quarter and year, highlighted by strong top and bottom-line growth. Importantly, we’ve started the Fiscal 2026 year strong, with revenue trends accelerating led by Coach."

While Tapestry’s FY25 results exceeded expectations, the market reaction suggests investor concerns about future performance amid global trade tensions and potential margin pressure. The company’s strategic focus on brand building, digital capabilities, and operational efficiency will be crucial as it navigates these challenges in fiscal 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.