Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Targa Resources Inc . (NYSE:TRGP) presented its second-quarter 2025 earnings results on August 7, 2025, showcasing an 18% year-over-year increase in Adjusted EBITDA. The midstream energy company’s stock responded positively, rising 2.62% in premarket trading to $167.32, signaling investor confidence in the quarterly performance.

The company’s strong results come amid continued expansion in the Permian Basin, where Targa has strategically positioned its gathering, processing, and transportation assets. This performance represents a rebound from the previous quarter, when the company beat EPS expectations but fell short on revenue targets.

Quarterly Performance Highlights

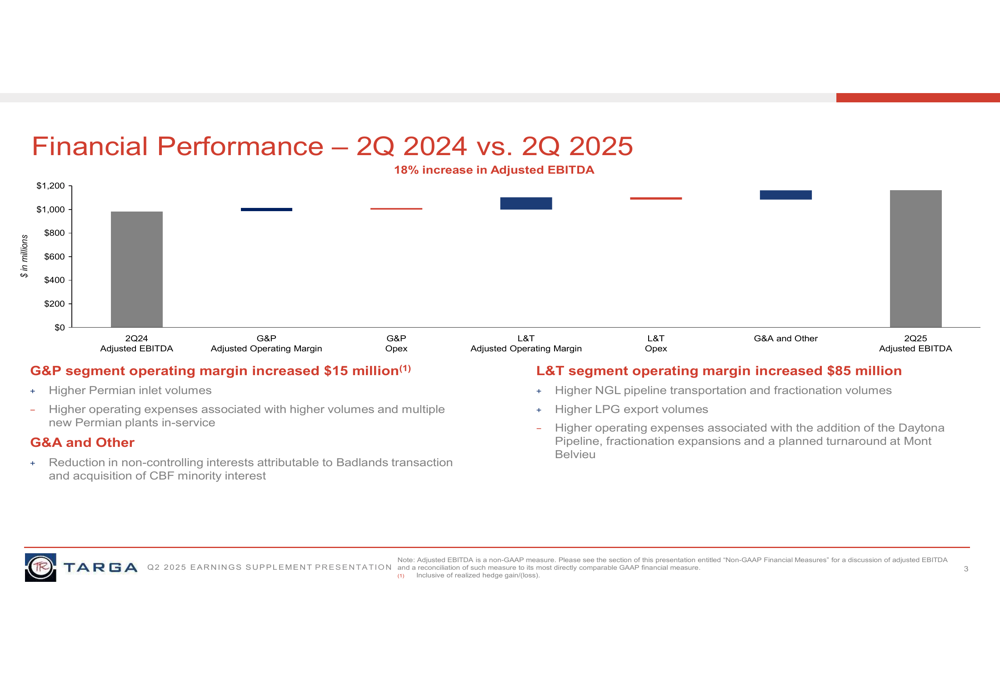

Targa reported Q2 2025 Adjusted EBITDA of $1,163 million, an 18% increase from $980 million in Q2 2024. This substantial year-over-year growth was primarily driven by higher volumes across the company’s integrated midstream system, particularly in the Permian Basin.

As shown in the following chart comparing Q2 2024 to Q2 2025 performance:

The growth in Adjusted EBITDA was driven by several factors:

- Gathering & Processing segment operating margin increased by $15 million year-over-year, supported by higher Permian inlet volumes

- Logistics & Transportation segment operating margin jumped by $85 million, reflecting increased NGL pipeline transportation, fractionation, and LPG export volumes

- Reduced non-controlling interests following the Badlands transaction and acquisition of CBF minority interest

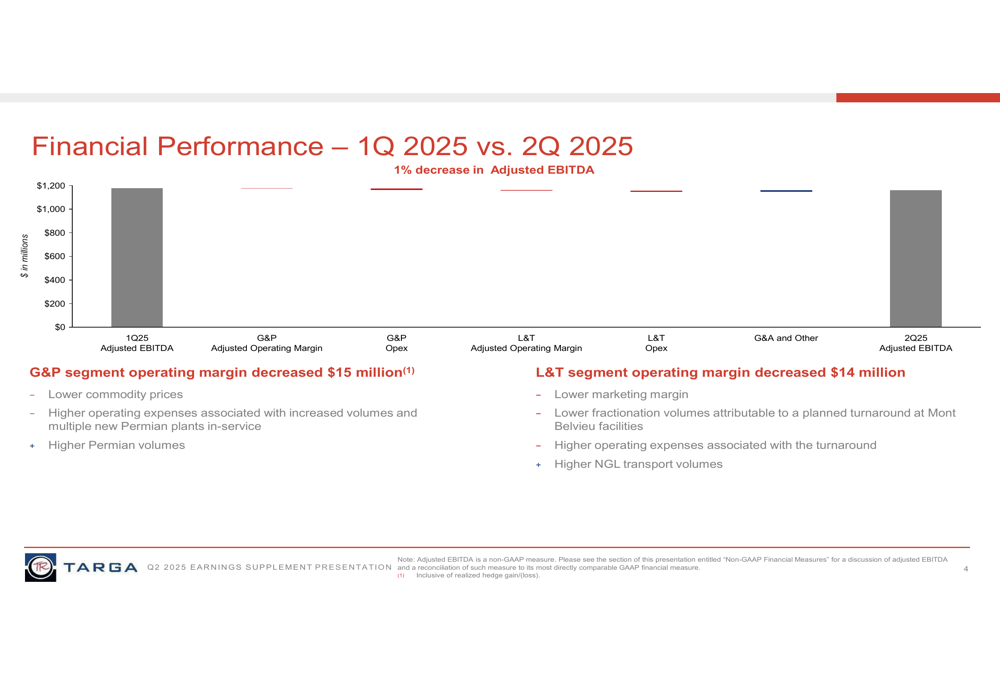

Sequentially, Adjusted EBITDA decreased slightly by 1% from Q1 2025, primarily due to lower commodity prices and planned maintenance activities.

Net income attributable to Targa Resources Corp. for Q2 2025 was $629.1 million, reflecting the company’s strong operational performance during the quarter.

Operational Performance

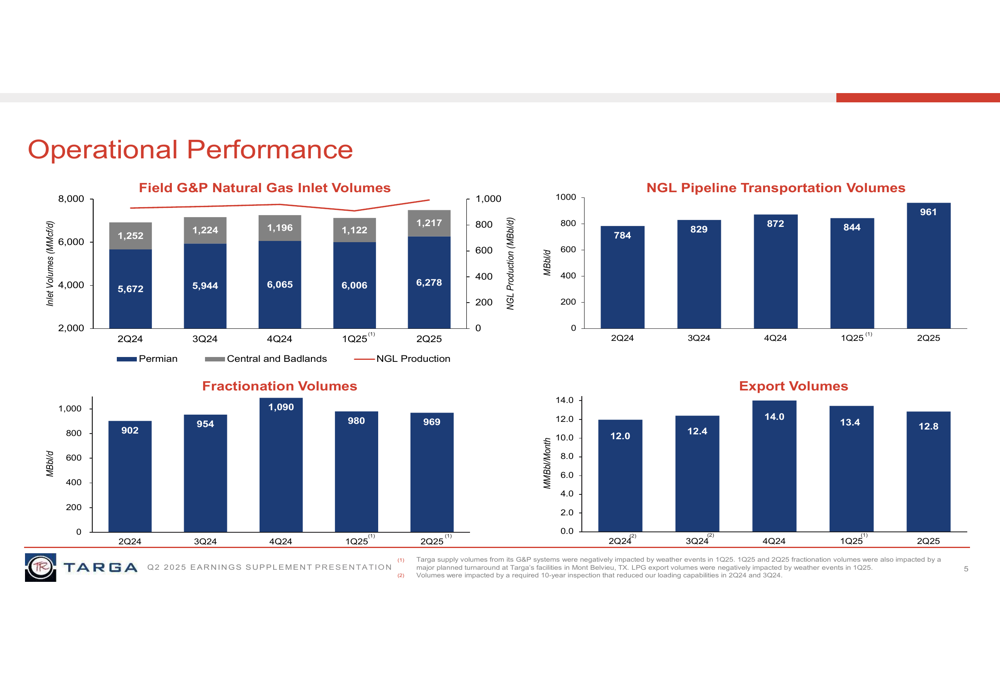

Targa’s operational metrics showed consistent growth across most business segments. The company’s Permian natural gas inlet volumes reached 6,278 MMcf/d in Q2 2025, an 11% increase from 5,672 MMcf/d in Q2 2024, highlighting the company’s expanding footprint in the prolific basin.

The following chart illustrates Targa’s operational performance across key metrics:

Notable operational highlights include:

- NGL Pipeline Transportation volumes surged to 961 MBbl/d, a 23% increase from 784 MBbl/d in Q2 2024

- Fractionation volumes grew to 969 MBbl/d, up from 902 MBbl/d in the same period last year

- Export volumes increased to 12.8 MMBbl/month from 12.0 MMBbl/month in Q2 2024

The company noted that a planned turnaround at its Mont Belvieu facilities impacted fractionation volumes in Q2 2025, which explains the slight sequential decrease from Q1 2025 levels.

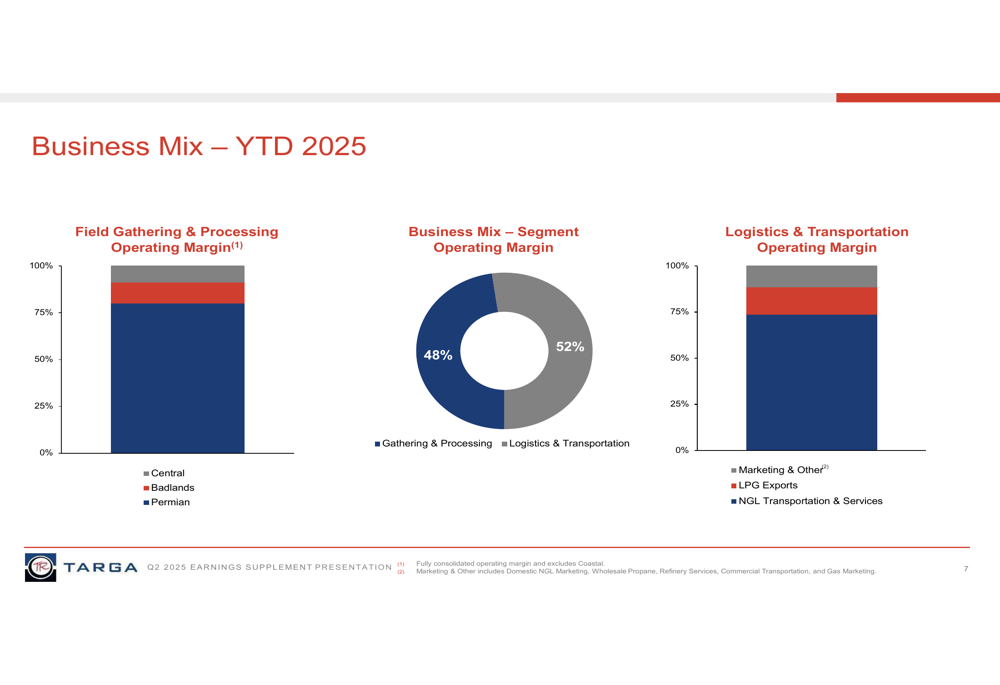

Business Mix Analysis

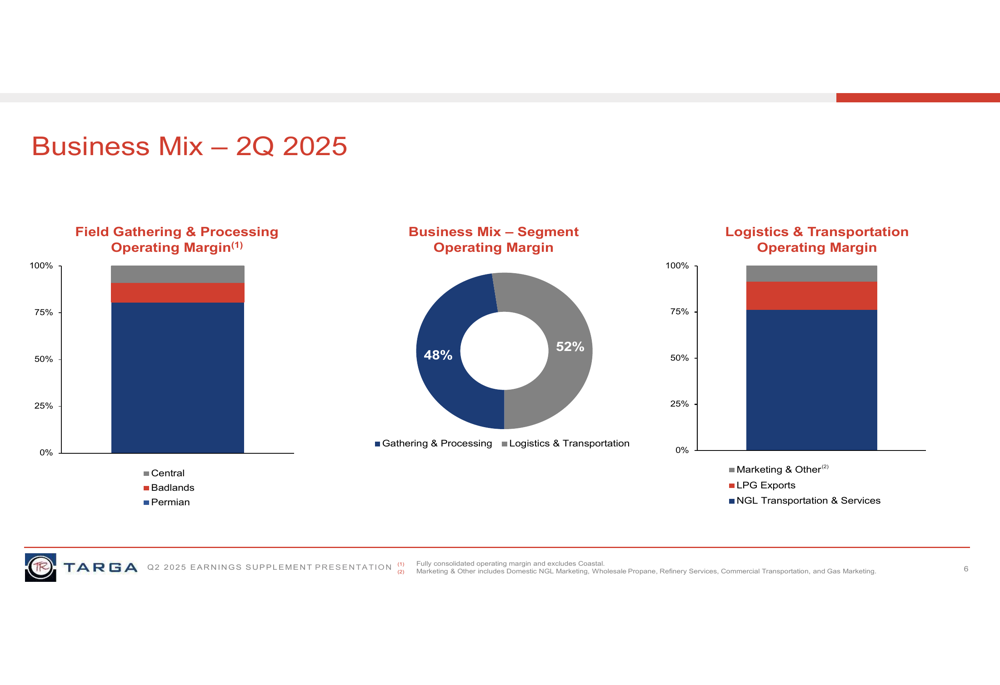

Targa’s business mix for Q2 2025 reflects the company’s evolving strategy, with the Logistics & Transportation segment now representing 52% of the company’s operating margin, while Gathering & Processing accounts for 48%.

The following chart breaks down Targa’s business mix for Q2 2025:

This shift toward Logistics & Transportation highlights Targa’s successful integration of its midstream value chain, from wellhead gathering to export terminals. The Permian region continues to dominate the Gathering & Processing segment, while NGL Transportation & Services represents the largest component of the Logistics & Transportation segment.

The year-to-date business mix for 2025 shows a similar distribution:

This consistent business mix throughout 2025 demonstrates the stability of Targa’s integrated business model and the complementary nature of its various segments.

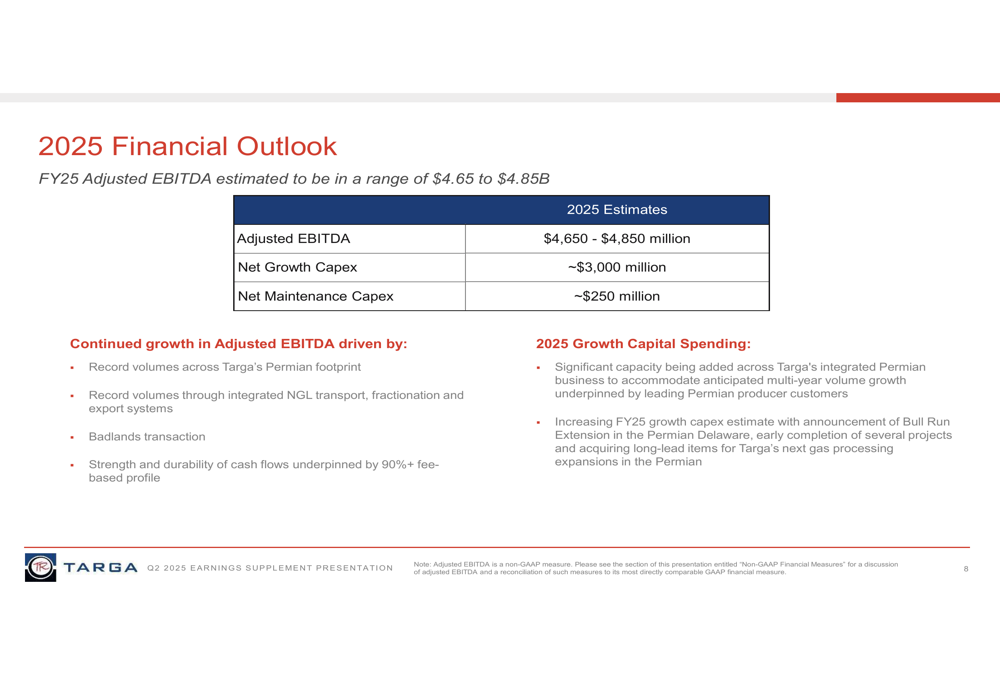

Financial Outlook & Guidance

Targa reaffirmed its full-year 2025 Adjusted EBITDA guidance of $4.65 billion to $4.85 billion, consistent with the outlook provided in the previous quarter. The company continues to invest heavily in growth projects, with approximately $3 billion allocated to net growth capital expenditures and $250 million to maintenance capital for 2025.

The following slide outlines Targa’s financial outlook for 2025:

Key drivers for continued growth include:

- Record volumes across Targa’s Permian footprint

- Integrated NGL transport, fractionation, and export systems

- Benefits from the Badlands transaction

- Strong and durable cash flows underpinned by a 90%+ fee-based profile

The company highlighted significant capacity additions across its integrated Permian business and announced the Bull Run Extension in the Permian Delaware as part of its growth strategy.

Forward-Looking Statements

Looking ahead, Targa is well-positioned to capitalize on continued production growth in the Permian Basin. The company’s integrated midstream model provides multiple avenues for growth, from gathering and processing at the wellhead to transportation, fractionation, and ultimately export services.

The company’s substantial capital investment program underscores management’s confidence in future growth opportunities. With approximately $3 billion allocated to growth projects in 2025, Targa is expanding capacity across its value chain to accommodate increasing volumes.

Targa’s strong operational performance in Q2 2025 and reaffirmed guidance suggest the company is successfully executing its strategy despite challenges such as commodity price fluctuations and planned maintenance activities. The positive premarket stock reaction indicates investor confidence in Targa’s ability to deliver on its growth objectives while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.