Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

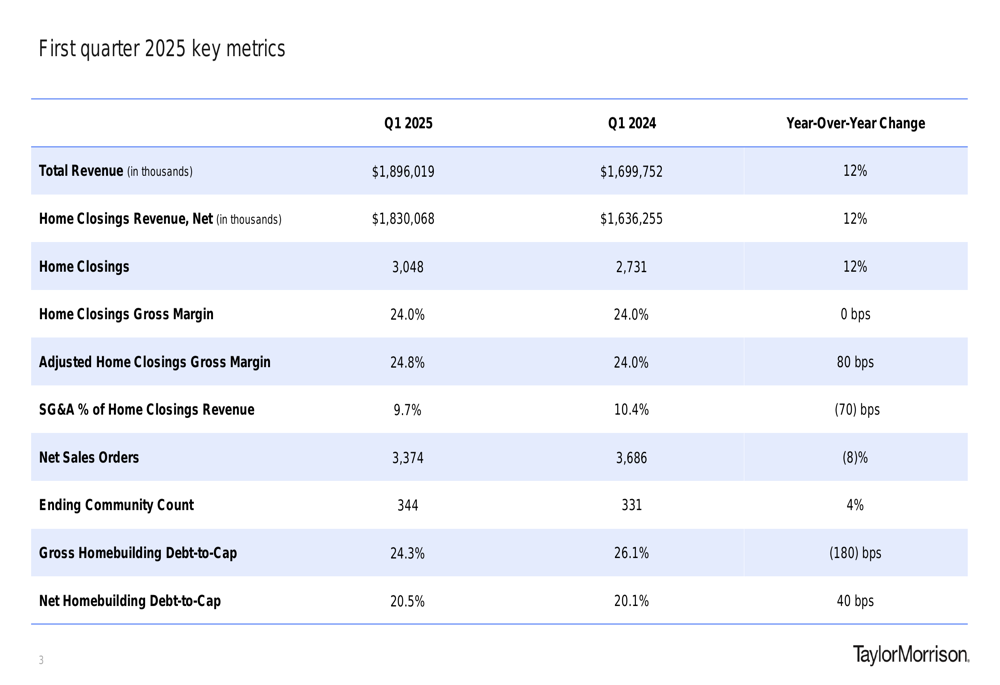

Taylor Morrison Home Corp (NYSE:TMHC) reported strong first-quarter 2025 results on April 23, with performance exceeding analyst expectations across key metrics. The homebuilder delivered 12% year-over-year growth in both revenue and home closings, while expanding its adjusted gross margins by 80 basis points to 24.8%.

The company’s stock responded positively to the earnings beat, rising 1.91% to $59.91, continuing its recovery from a 52-week low of $51.90 while still trading below its 52-week high of $75.49.

Q1 2025 Performance Highlights

Taylor Morrison’s first quarter results demonstrated solid execution across its diversified business model. The company reported total revenue of $1.9 billion, with home closings revenue reaching $1.83 billion, representing a 12% increase compared to Q1 2024.

As shown in the following comprehensive performance comparison:

The company delivered 3,048 homes in Q1 2025, up 12% from the prior year, while maintaining an average closing price of $600,000. Despite the revenue growth, net sales orders declined 8% year-over-year to 3,374 units, though this was partially offset by a 4% increase in community count to 344 active selling communities.

CEO Cheryl Palmer highlighted the company’s diversified consumer strategy during the earnings call, stating, "Our diversified consumer segmentation is critically important." She also noted the favorable market conditions, adding, "We believe the market overall remains undersupplied and demographic supportive."

Financial Strength and Capital Position

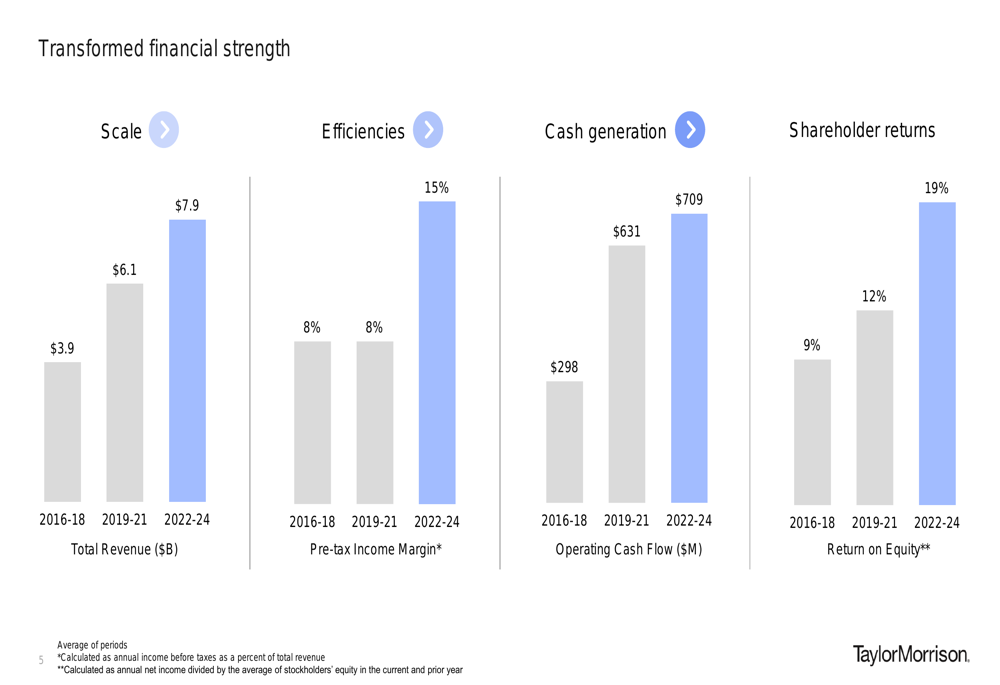

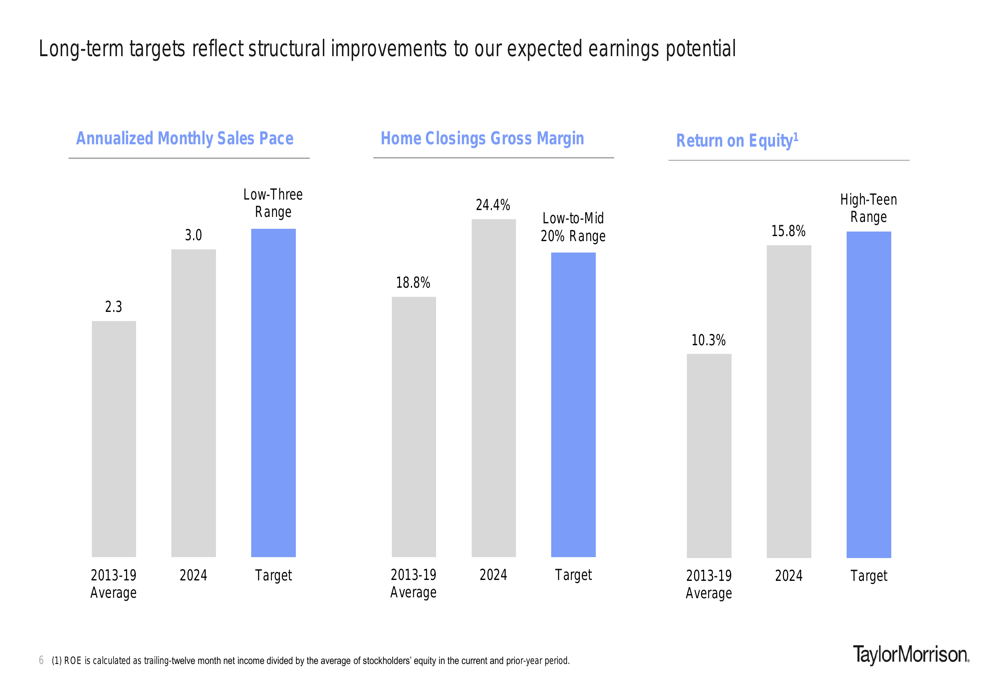

Taylor Morrison has significantly improved its financial position over time, with metrics showing substantial growth across revenue, margins, and returns. The company’s transformation is evident in the following historical comparison:

The homebuilder maintains a strong balance sheet with $1.3 billion in total liquidity, including $378 million in unrestricted cash and $934 million in revolving credit facility capacity. The net homebuilding debt-to-capital ratio stands at 20.5%, slightly higher than the 20.1% reported a year ago.

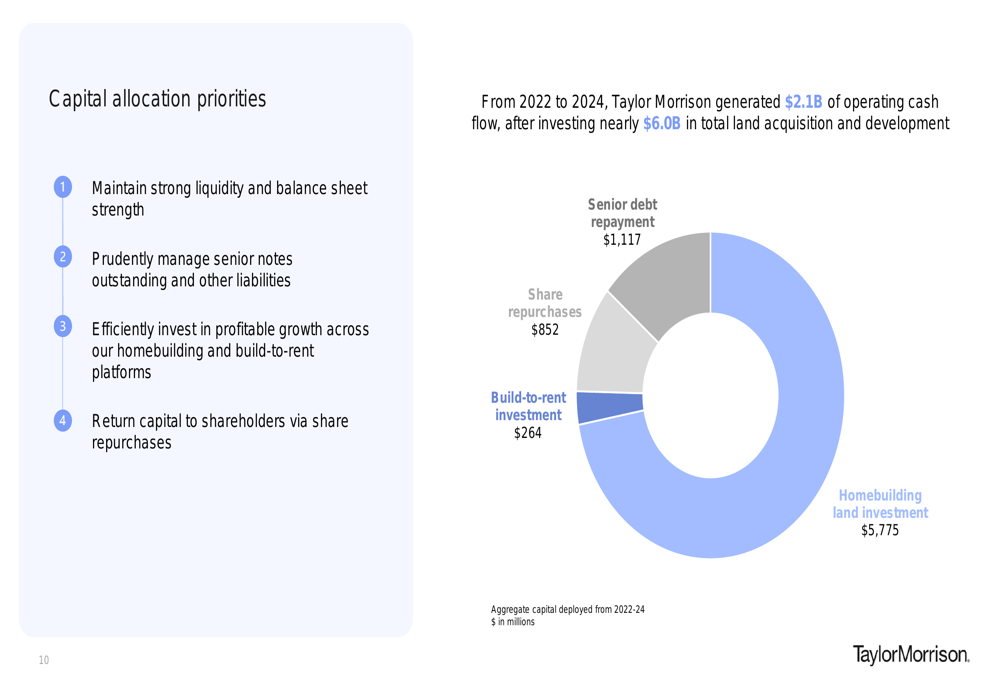

Taylor Morrison’s capital allocation strategy prioritizes maintaining balance sheet strength while investing in growth and returning capital to shareholders. The company expects to repurchase approximately $350 million of common stock in 2025, continuing its track record of significant share repurchases over recent years.

Strategic Initiatives and Competitive Positioning

Taylor Morrison has established itself as a diversified homebuilder operating across 21 markets in 12 states. The company’s product mix is balanced across entry-level (32%), move-up (47%), and resort lifestyle (21%) segments, with geographic diversification spanning the West (35%), Central (29%), and East (36%) regions of the United States.

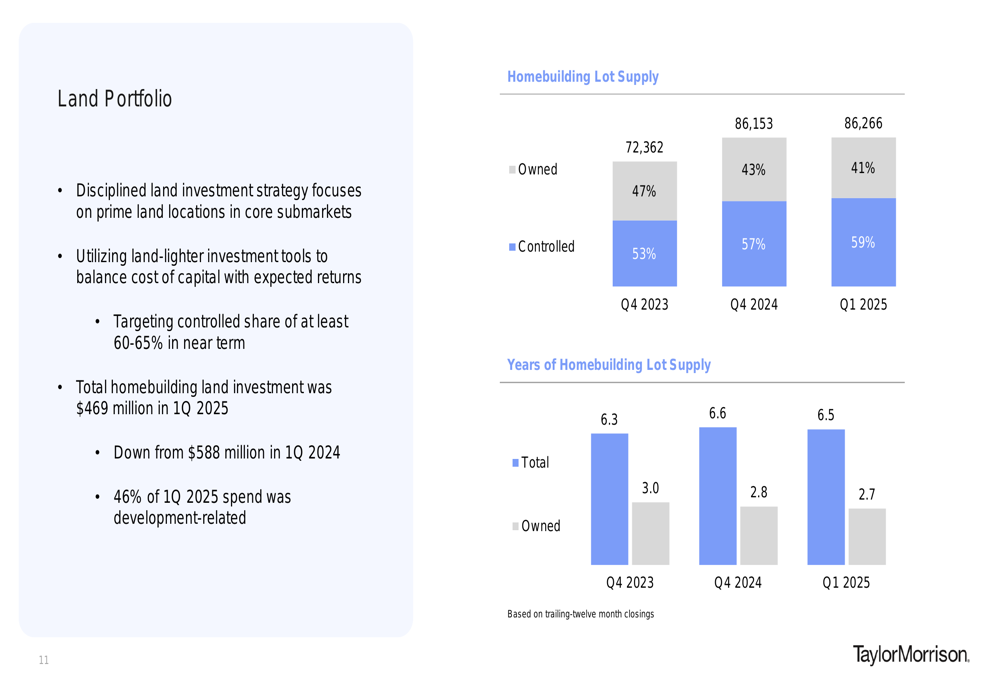

A key component of Taylor Morrison’s strategy is its land portfolio management approach, which has shifted toward a higher proportion of controlled versus owned lots. As of Q1 2025, 59% of the company’s lots were controlled rather than owned, up from 53% in Q4 2023.

The company is also expanding its build-to-rent business, YARDLY, which now operates in 9 markets with approximately 40 owned and controlled communities. Taylor Morrison expects to complete 5 to 7 asset dispositions in this segment during 2025.

Another notable strategic initiative is the company’s growing online sales platform, which now contributes approximately 20% of total sales, with a reservation-to-sales conversion rate exceeding 50% in Q1 2025.

Financial Outlook and Guidance

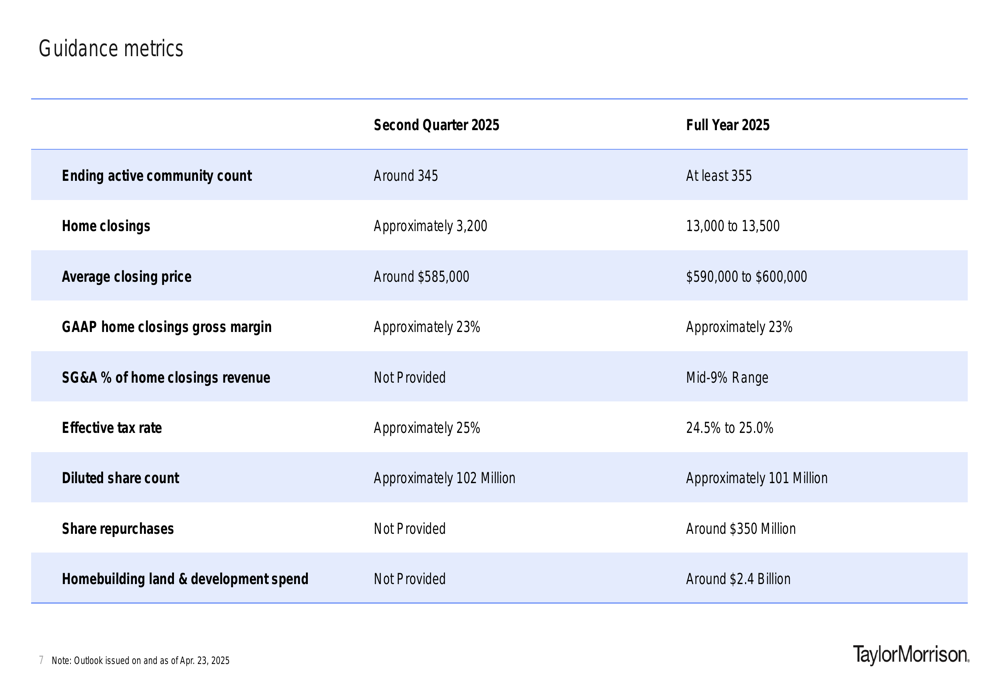

Looking ahead, Taylor Morrison provided detailed guidance for both Q2 and full-year 2025. The company expects to deliver approximately 3,200 homes in Q2 at an average closing price of around $585,000. For the full year, Taylor Morrison projects 13,000 to 13,500 home closings with an average price between $590,000 and $600,000.

As shown in the following guidance metrics:

The company is targeting a GAAP home closings gross margin of approximately 23% for both Q2 and full-year 2025, with SG&A as a percentage of home closings revenue expected to be in the mid-9% range for the full year.

Taylor Morrison has also established long-term targets that exceed its historical averages, aiming for a monthly sales pace in the low-three range, gross margins in the low-to-mid 20% range, and return on equity in the high-teen range.

Conclusion

Taylor Morrison’s Q1 2025 presentation reveals a company executing effectively on its strategic initiatives while delivering strong financial results. The 12% growth in revenue and home closings, combined with expanding margins and a solid balance sheet, positions the homebuilder well despite some moderation in sales order activity.

The company’s focus on diversification across product types and geographies, along with its disciplined approach to land management and capital allocation, provides multiple avenues for continued growth. With a positive outlook for 2025 and clear long-term targets, Taylor Morrison appears well-positioned to navigate the evolving housing market landscape.

Investors responded positively to the results, with the stock gaining 1.91% following the earnings announcement, reflecting confidence in the company’s strategy and execution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.