Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

TCM Group A/S (CPH:TCM) presented its first quarter 2025 results on May 21, showing modest growth amid challenging market conditions. The Danish kitchen manufacturer’s shares declined 1.8% to DKK 77.8 following the presentation, despite reporting improved margins and continued revenue growth. The stock remains near its 52-week high of DKK 80.2, suggesting overall investor confidence in the company’s trajectory.

Quarterly Performance Highlights

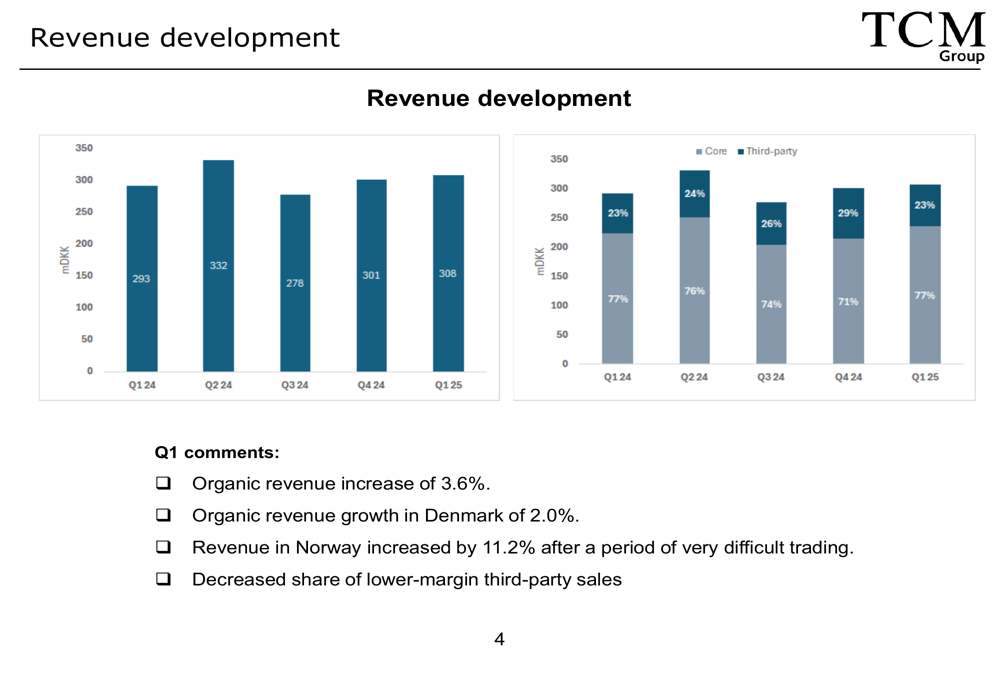

TCM Group reported year-on-year revenue growth of 5.3% for Q1 2025, with organic growth reaching 3.6%. Total (EPA:TTEF) revenue for the quarter stood at DKK 308 million, up from DKK 293 million in the same period last year. The company highlighted robust increases in B2C sales and particularly strong performance in Norway, where sales increased by 11.2% after a period of difficult trading conditions.

As shown in the following revenue development chart, TCM has maintained consistent quarterly performance, with Q1 2025 continuing the positive trend:

The company’s revenue mix remained stable with core sales representing 77% of total revenue, while third-party products accounted for 23%. This represents an improvement in the sales mix compared to previous quarters, particularly Q4 2024 when third-party sales had increased to 29% of revenue.

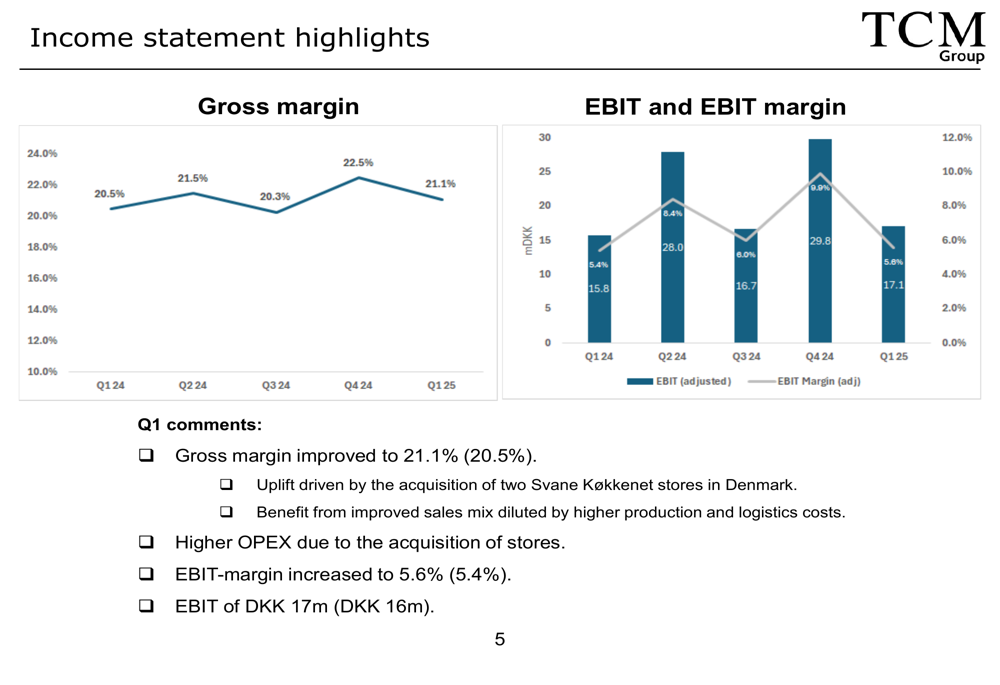

Profitability metrics also showed improvement, with gross margin increasing to 21.1% from 20.5% in Q1 2024. Adjusted EBIT reached DKK 17 million, up from DKK 16 million, resulting in an adjusted EBIT margin of 5.6% compared to 5.4% in the prior year.

The following chart illustrates TCM Group’s gross margin and EBIT trends over the past five quarters:

Detailed Financial Analysis

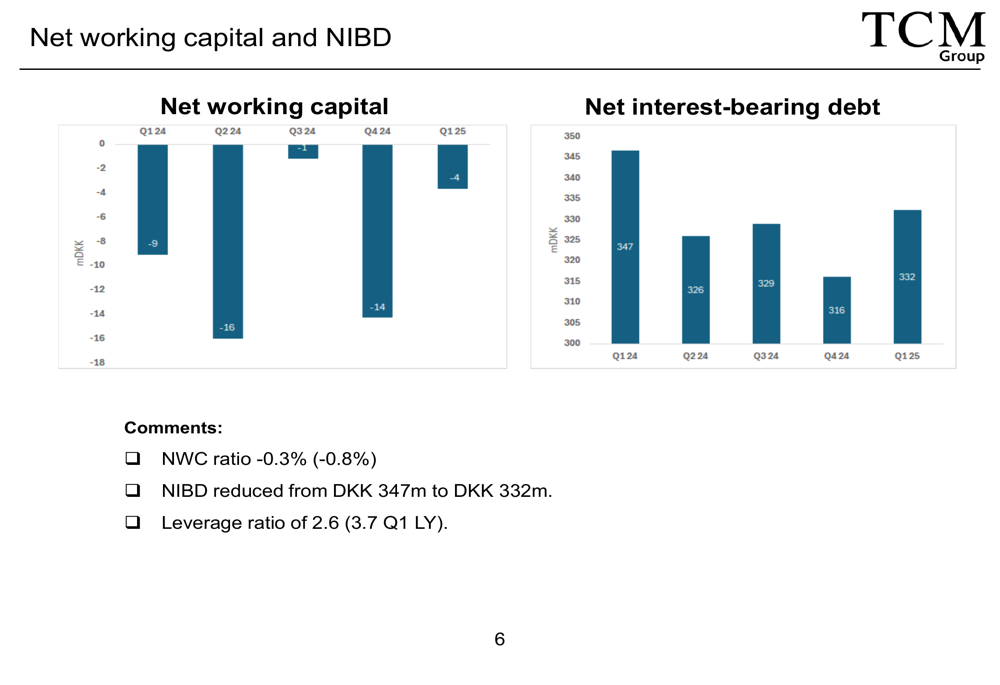

TCM Group’s balance sheet continued to strengthen, with net interest-bearing debt (NIBD) reduced to DKK 332 million from DKK 347 million in Q1 2024. This improvement contributed to a significant reduction in the leverage ratio, which decreased to 2.6 from 3.7 in the previous year.

The company’s net working capital position remained negative at DKK -4 million, representing a ratio of -0.3% of revenue compared to -0.8% in Q1 2024. While still favorable, this indicates a slight reduction in working capital efficiency.

The following chart shows TCM Group’s net working capital and net interest-bearing debt trends:

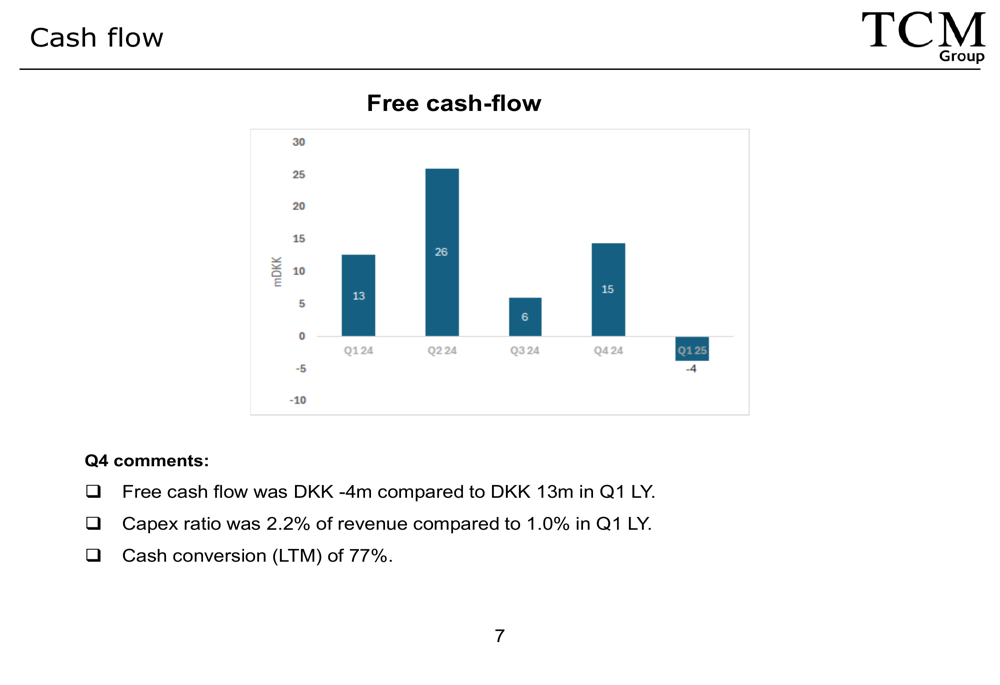

Free cash flow presented a challenge in Q1 2025, turning negative at DKK -4 million compared to a positive DKK 13 million in Q1 2024. The company attributed this partly to increased capital expenditures, with the capex ratio rising to 2.2% of revenue from 1.0% in the prior year. Despite this quarterly setback, TCM maintained a strong cash conversion rate of 76.8% on a last-twelve-months basis, up from 69.1% a year earlier.

The free cash flow trend is illustrated in the following chart:

TCM Group highlighted several operational achievements during the quarter, including two product launches: Sense Truffel in the AUBO brand and Notes Bronze in Svane Køkkenet. The company also noted that the acquisition of two Svane Køkkenet stores in Denmark contributed to the gross margin improvement, though this benefit was partially offset by higher production and logistics costs.

Forward-Looking Statements

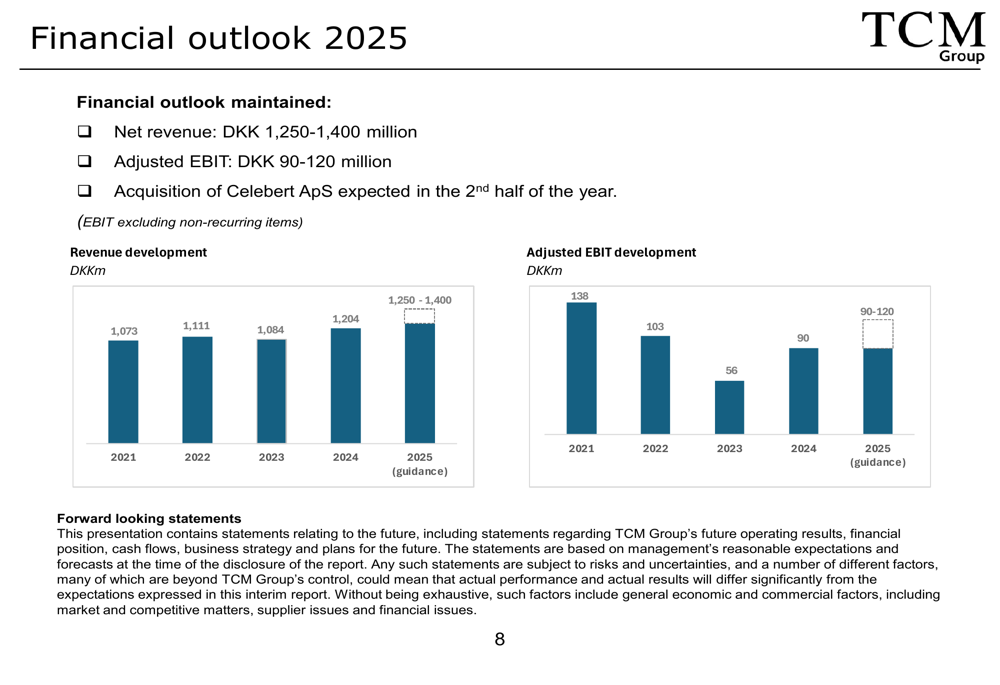

Looking ahead, TCM Group maintained its financial guidance for 2025, projecting net revenue between DKK 1,250-1,400 million and adjusted EBIT of DKK 90-120 million. The company also announced plans to acquire Celebert ApS in the second half of 2025, which is expected to further strengthen its market position.

The following chart shows TCM Group’s historical revenue and EBIT performance along with its 2025 guidance:

The revenue guidance represents potential growth of 3.8% to 16.3% compared to 2024 revenue of DKK 1,204 million. Similarly, the adjusted EBIT guidance suggests that the company expects to maintain or improve upon the DKK 90 million achieved in 2024.

TCM Group’s order intake increased year-over-year in Q1 2025, with growth reported in both B2C and B2B segments across all brands. This positive order trend provides some confidence in the company’s ability to achieve its full-year targets, despite the challenging macroeconomic environment affecting the kitchen furniture industry.

While the company faces ongoing challenges from higher production and logistics costs, its focus on improving sales mix and operational efficiency appears to be yielding positive results. The planned acquisition of Celebert ApS later in the year could provide additional growth opportunities as TCM Group continues to execute its strategic expansion plans.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.