Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

TCM Group (CPH:TCM), the Danish kitchen manufacturer, presented its Q2 2025 interim results on August 20, showing solid performance despite early signs of consumer market slowdown. The company’s stock dipped slightly by 0.28% to 71.6 following the presentation, suggesting a neutral market reaction to results that included a minor revenue miss against forecasts but demonstrated strong operational efficiency.

The kitchen and bathroom furniture specialist continues to navigate a mixed market environment, with positive momentum in Norway offsetting early signs of B2C slowdown in its home market. The presentation highlighted both financial achievements and strategic moves, including the acquisition of the remaining stake in online retailer Celebert ApS.

Quarterly Performance Highlights

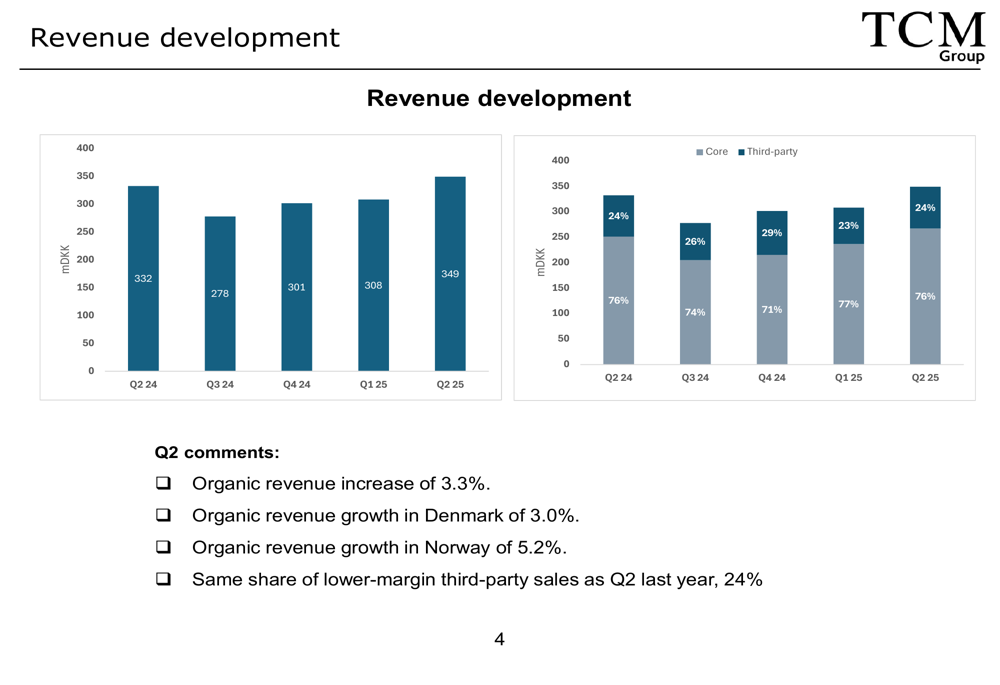

TCM Group reported Q2 2025 revenue of DKK 349 million, representing a 5.1% year-on-year increase from DKK 332 million in Q2 2024. The company achieved organic growth of 3.3%, with particularly strong performance in Norway, where sales increased by 5.2%.

As shown in the following revenue development chart, TCM has maintained consistent growth over recent quarters, with Q2 2025 marking the highest quarterly revenue in the period displayed:

The revenue mix remained stable compared to the same quarter last year, with core sales accounting for 76% of revenue and third-party products making up the remaining 24%. The company noted increased sales in both B2B and B2C segments, though it flagged early warning signs of a potential slowdown in consumer sales.

Detailed Financial Analysis

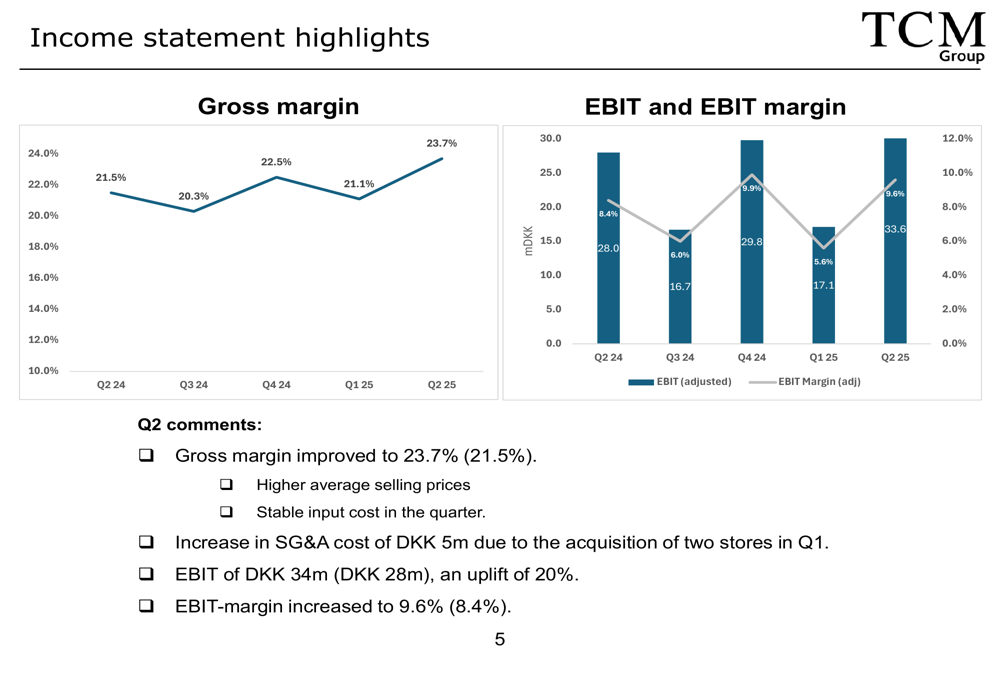

TCM Group’s profitability metrics showed notable improvement in Q2 2025. Gross margin expanded to 23.7%, up from 21.5% in the same period last year, supported by higher average prices and stable input costs during the quarter.

The following chart illustrates the positive trend in gross margin and EBIT performance:

Adjusted EBIT reached DKK 34 million, a significant 20% increase from DKK 28 million in Q2 2024. This improvement drove the adjusted EBIT margin to 9.6%, up from 8.4% in the prior-year period. The company noted a DKK 5 million increase in SG&A costs, attributed to the acquisition of two stores in Q1.

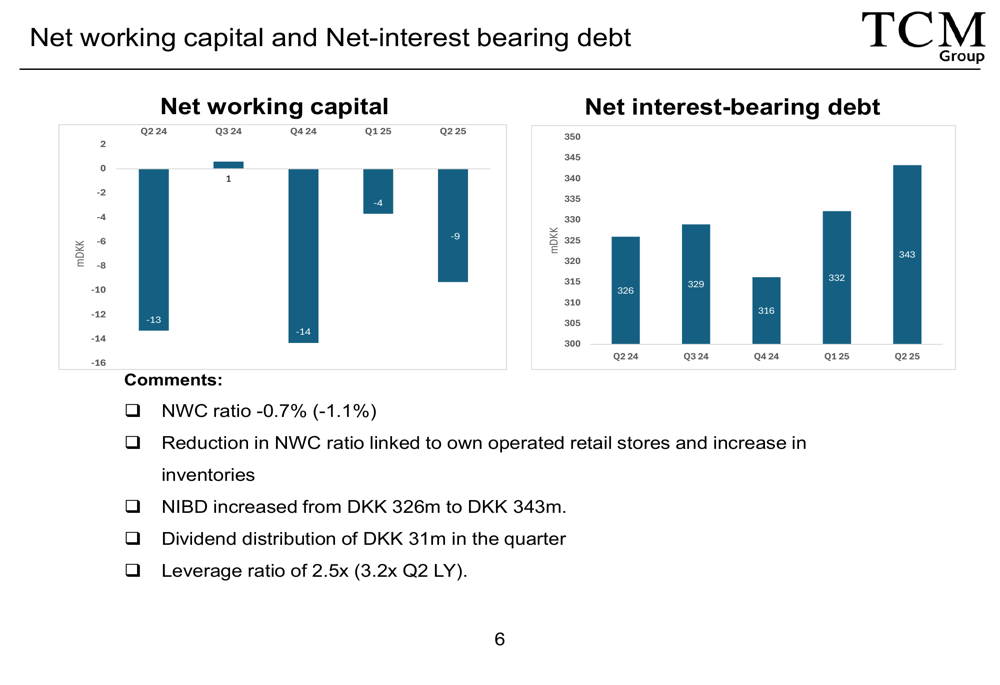

TCM’s working capital position and debt metrics showed mixed results. Net working capital remained negative at -0.7% of revenue (compared to -1.1% in Q2 2024), which the company attributed to own-operated retail stores and increased inventories.

The following chart shows the development of net working capital and net interest-bearing debt:

Net interest-bearing debt increased to DKK 343 million from DKK 326 million in Q2 2024, partly due to a dividend distribution of DKK 31 million during the quarter. Despite this increase, the company’s leverage ratio improved to 2.5x from 3.2x in the same period last year.

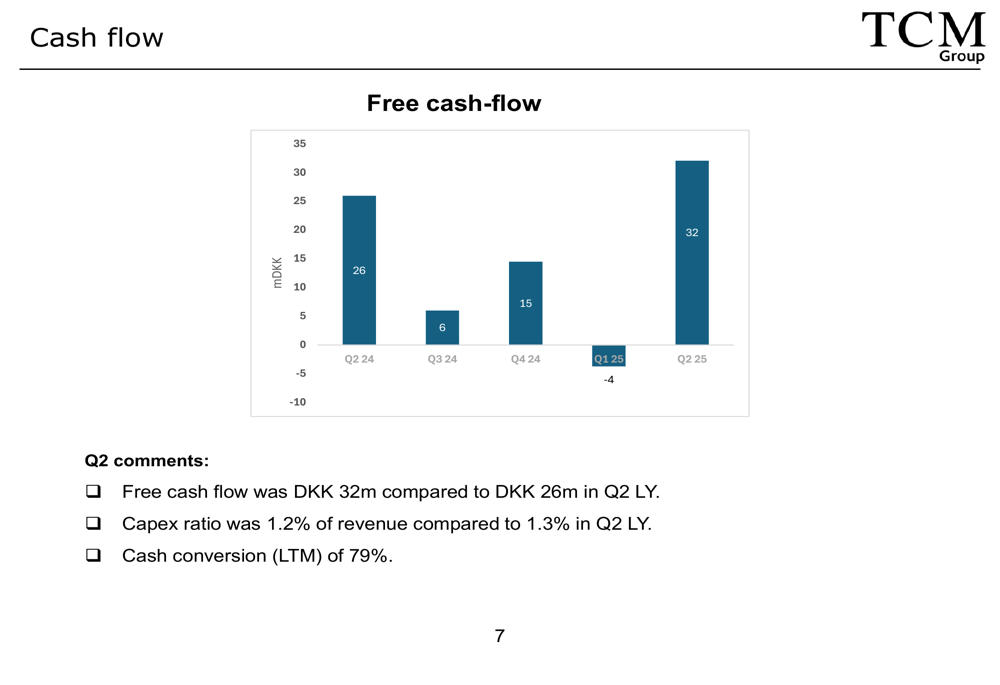

Free cash flow generation remained strong at DKK 32 million, up from DKK 26 million in Q2 2024, with capital expenditure representing 1.2% of revenue. The company’s cash conversion rate (LTM) stood at 78.6%, down from 92.5% in the prior-year period.

Strategic Initiatives

A significant development announced in the presentation was TCM Group’s acquisition of the remaining 55% stake in Celebert ApS. The company had previously merged its online activities with Celebert in 2021, acquiring a 45% stake at that time.

Celebert has established itself as a pioneer in online retailing of kitchens, bathroom interiors, wardrobes, and white goods, operating several e-commerce platforms including kitchn.dk, billigskabe.dk, and justwood.dk. The business has demonstrated strong revenue growth since 2021, reaching approximately DKK 150 million in 2024.

TCM Group estimates the purchase price for the remaining stake at DKK 60-85 million, with the transaction expected to close toward the end of 2025, subject to regulatory approval. This acquisition represents a strategic move to strengthen TCM’s online presence and expand its digital sales channels.

Forward-Looking Statements

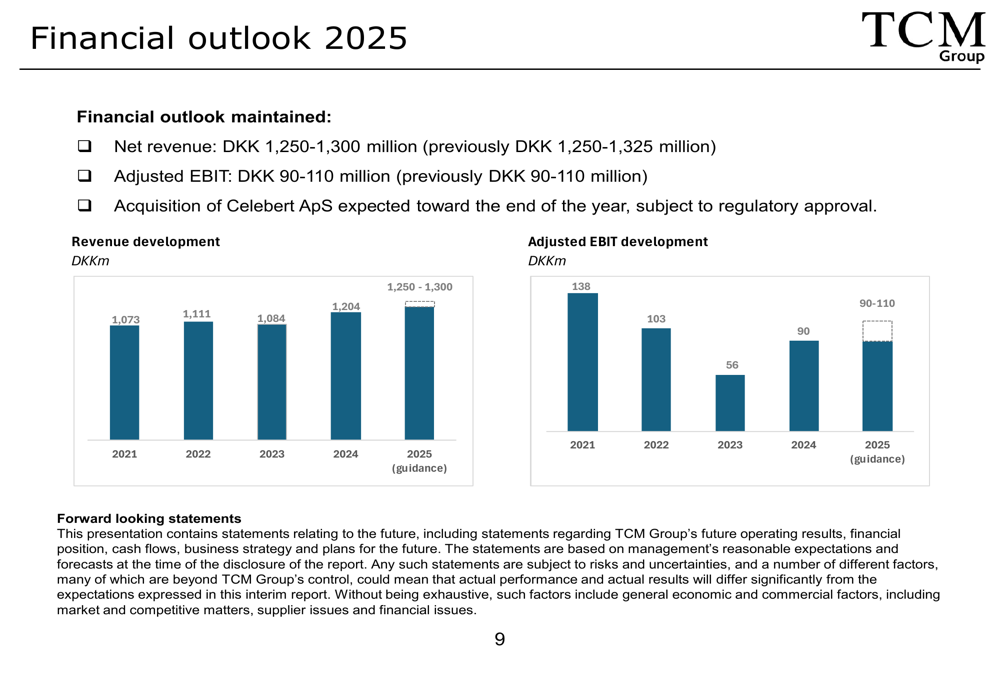

TCM Group revised its full-year 2025 revenue guidance to DKK 1,250-1,300 million, narrowing the previous range of DKK 1,250-1,325 million. The company maintained its adjusted EBIT guidance at DKK 90-110 million.

The following chart illustrates TCM’s historical performance and 2025 guidance:

The slight narrowing of revenue guidance may reflect the early signs of B2C slowdown mentioned in the presentation. During the earnings call, CEO Torben Paulin noted that "Traffic is better than the actual order intake," suggesting potential for future growth despite current challenges.

The company expects the acquisition of Celebert ApS to close toward the end of the year, subject to regulatory approval, which could provide additional revenue streams in 2026.

TCM Group faces several challenges in the coming quarters, including slower order intake in Q2 that could affect future revenue, and shifting consumer spending patterns toward travel and leisure that might impact sales. However, the company’s strong operational performance, improved margins, and strategic acquisition position it to navigate these challenges while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.