Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

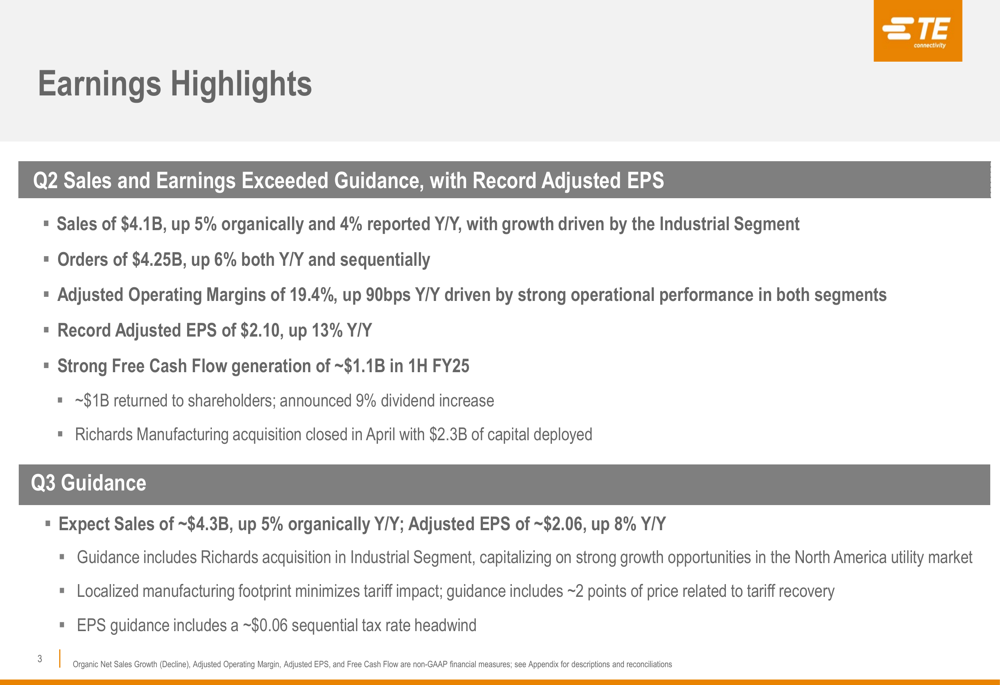

TE Connectivity (NYSE:TEL), a global leader in connectivity and sensor solutions, reported strong second-quarter 2025 results on April 23, exceeding guidance across key metrics. The company achieved record adjusted earnings per share despite mixed segment performance, with robust growth in industrial applications offsetting weakness in transportation markets.

Sales reached $4.1 billion, representing 5% organic growth and 4% reported growth year-over-year, while orders of $4.25 billion increased 6% both annually and sequentially. The company’s adjusted operating margin expanded by 90 basis points to 19.4%, driving a 13% increase in adjusted EPS to a record $2.10.

As shown in the following earnings highlights slide, TE Connectivity also announced a 9% dividend increase and completed its acquisition of Richards Manufacturing, deploying $2.3 billion to strengthen its position in the North American utility market:

Quarterly Performance Highlights

TE Connectivity’s performance reflected divergent trends across its two main segments. The Transportation Solutions segment, which includes automotive, commercial transportation, and sensors businesses, saw sales decline by 4% on a reported basis and 2% organically to $2.31 billion. This weakness was primarily driven by declines in Europe and North America, partially offset by growth in Asia.

Despite the revenue challenges, the Transportation segment maintained strong profitability with adjusted operating margins of 20.7%, slightly above the prior year’s 20.6%. This resilience in margins demonstrates the company’s operational efficiency even in a challenging market environment.

The following slide details the Transportation segment’s performance:

In contrast, the Industrial Solutions segment delivered exceptional results with reported sales growth of 17% and organic growth of 16% to $1.83 billion. This strong performance was accompanied by significant margin expansion, with adjusted operating margins increasing 260 basis points year-over-year to 17.9%.

The standout performer within Industrial Solutions was the Digital Data Networks (DDN) business, which grew 78% organically, driven by strong momentum in artificial intelligence applications across multiple customers. The Energy business also showed solid growth of 8% organically, benefiting from continued demand for grid hardening and renewable energy solutions.

The following slide illustrates the Industrial segment’s impressive performance:

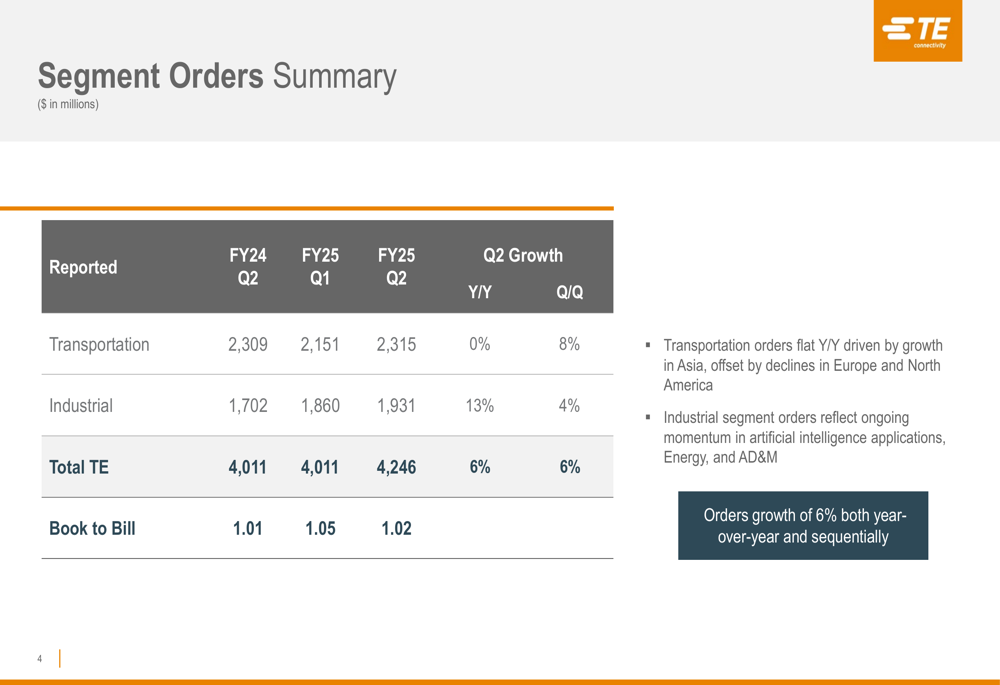

Order trends provide additional insight into the company’s momentum. Total (EPA:TTEF) orders of $4.25 billion represented a book-to-bill ratio of 1.02, indicating continued growth potential. While Transportation orders were flat year-over-year, Industrial segment orders grew 13%, reflecting ongoing strength in artificial intelligence applications, energy, and aerospace, defense, and marine markets.

The order trends by segment are shown in the following table:

Detailed Financial Analysis

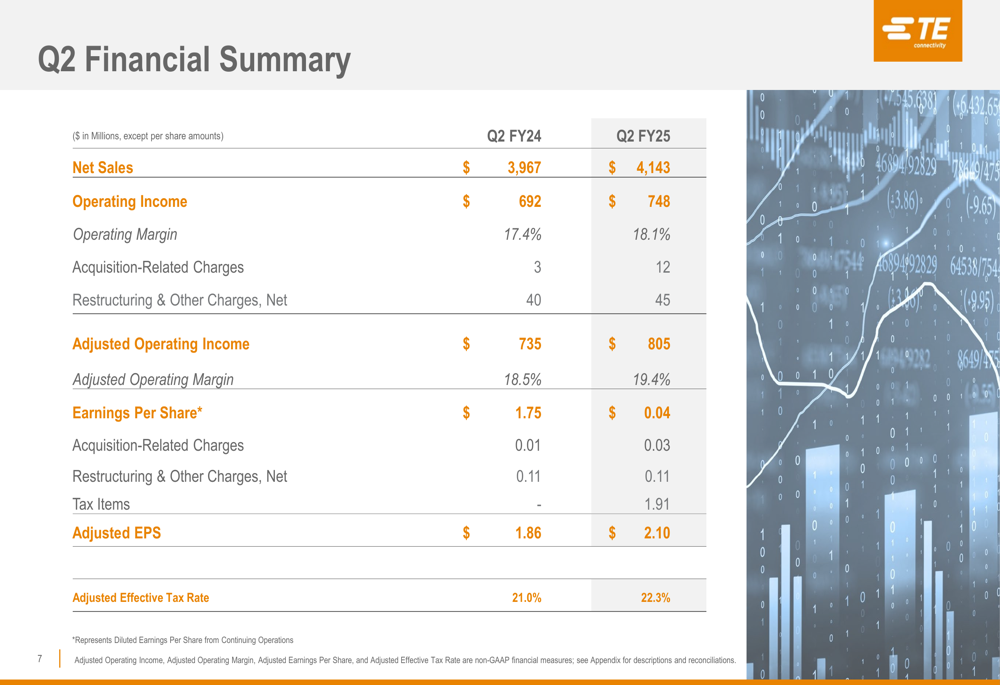

TE Connectivity’s financial performance demonstrated strength across key metrics. The company’s adjusted operating income increased to $805 million from $735 million in the prior year, while adjusted operating margin expanded by 90 basis points to 19.4%.

This margin expansion was primarily driven by higher volume and strong operational performance, particularly in the Industrial segment. The company’s adjusted effective tax rate increased to 22.3% from 21.0% in the prior year.

The following financial summary provides a comprehensive view of the quarter’s results:

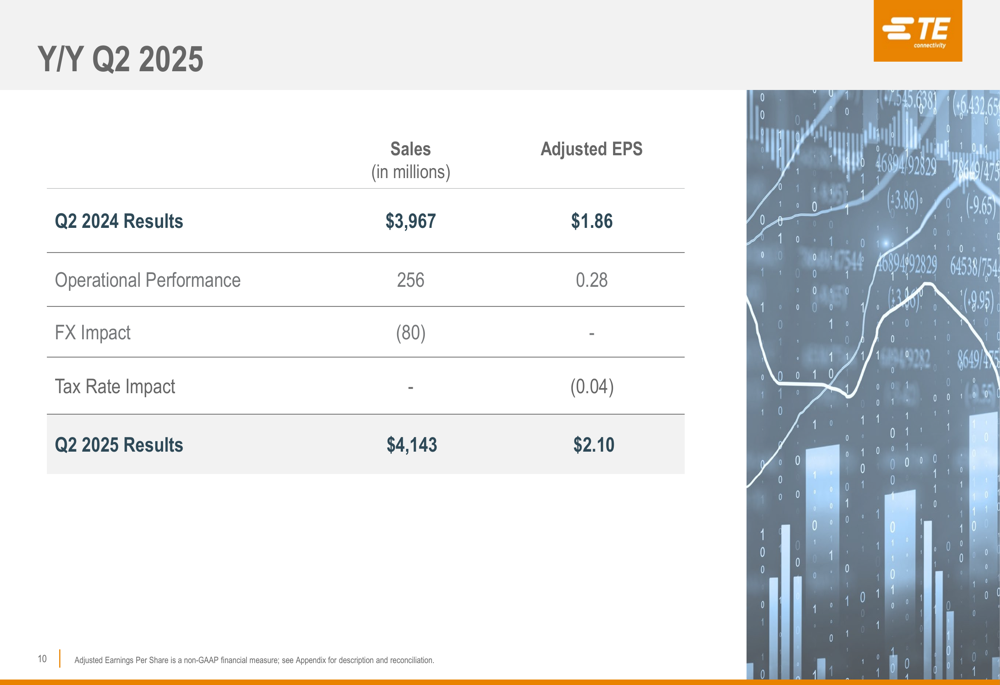

The company’s earnings per share growth of 13% was driven primarily by operational performance, which contributed $0.28 to the year-over-year increase. This was partially offset by a $0.04 headwind from tax rate impacts, as shown in the following reconciliation:

TE Connectivity continued to generate strong cash flow, with free cash flow of approximately $1.1 billion in the first half of fiscal 2025. The company maintained its commitment to shareholder returns, returning approximately $1 billion to shareholders through dividends and share repurchases.

The balance sheet remains solid, with $2.55 billion in cash at the end of the quarter. Total debt increased to $5.61 billion from $4.20 billion in the prior year, primarily due to financing for the Richards Manufacturing acquisition.

Strategic Initiatives

TE Connectivity’s strategic focus remains on high-growth markets, particularly in artificial intelligence infrastructure and energy applications. The company’s Digital Data Networks business is capitalizing on the rapid expansion of AI computing capabilities, delivering 78% organic growth in the quarter.

The acquisition of Richards Manufacturing, which closed in April, represents a significant strategic investment of $2.3 billion to strengthen TE Connectivity’s position in the North American utility market. This acquisition aligns with the company’s focus on grid hardening and renewable energy applications, which continue to show strong growth momentum.

TE Connectivity also highlighted its localized manufacturing footprint, which helps minimize the impact of tariffs. The company noted that its guidance includes approximately 2 percentage points of price related to tariff recovery, demonstrating its ability to navigate trade challenges effectively.

Forward-Looking Statements

Looking ahead to the third quarter of fiscal 2025, TE Connectivity provided a positive outlook with expected sales of approximately $4.3 billion, representing 5% organic growth year-over-year. The company anticipates adjusted earnings per share of approximately $2.06, an 8% increase from the prior year.

This guidance includes the contribution from the Richards Manufacturing acquisition in the Industrial segment and reflects continued momentum in key growth areas. However, the company noted that the EPS guidance includes a sequential tax rate headwind of approximately $0.06.

The following slide details the components of the expected year-over-year EPS growth for Q3:

TE Connectivity’s financial performance in Q2 and its forward guidance demonstrate the company’s ability to deliver strong results despite mixed end-market conditions. The robust growth in industrial applications, particularly in AI and energy markets, is successfully offsetting challenges in transportation markets, while operational excellence continues to drive margin expansion and record earnings.

The company’s strategic focus on high-growth markets and its disciplined approach to capital allocation position it well for continued success in the evolving connectivity landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.