AI is a game of kings, and OpenAI knows it

Introduction & Market Context

TeamViewer AG (ETR:TMV) released its Q1 2025 financial results on May 6, showing solid growth driven primarily by its Enterprise segment, though the market responded negatively with shares dropping 7.4% following the announcement. The remote access and digital workplace solutions provider reported pro forma revenue growth of 7% year-over-year to €190.3 million, maintaining its full-year guidance despite the market’s lukewarm reception.

The company’s stock closed at €13.37 prior to the results and fell to around €12.38 during trading, reflecting investor concerns despite management’s positive narrative about the quarter’s performance and the ongoing integration of its 1E acquisition.

Quarterly Performance Highlights

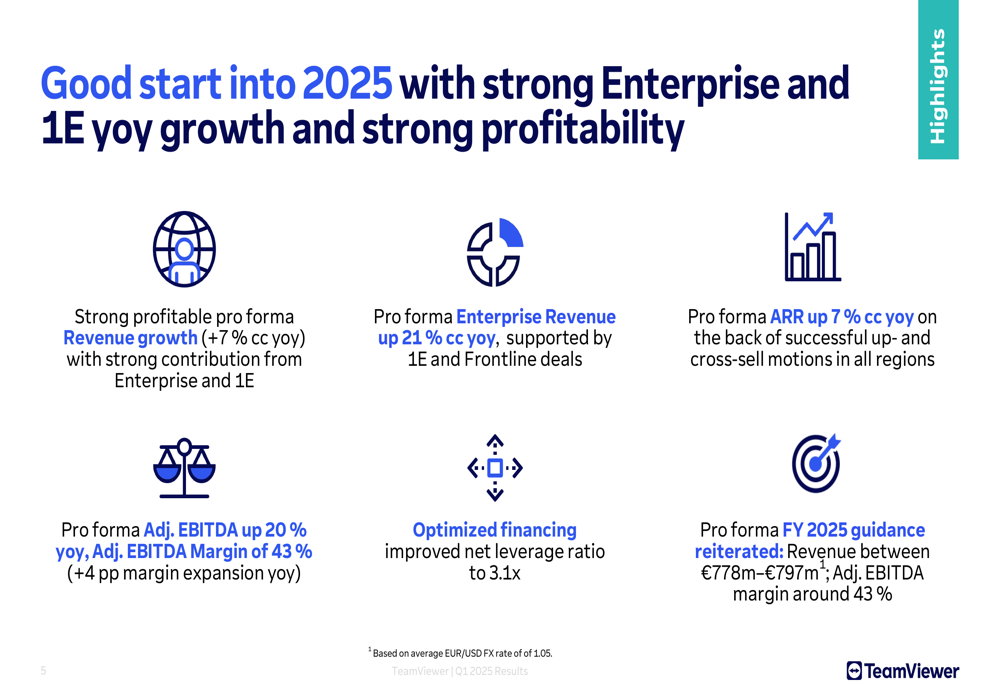

TeamViewer delivered a strong start to 2025 with 7% constant currency revenue growth year-over-year, driven primarily by its Enterprise segment which grew 21% to €59.9 million. The company’s Annual Recurring Revenue (ARR) also increased 7% to €759.5 million, reflecting successful up-selling and cross-selling efforts across all regions.

As shown in the following key highlights chart, profitability improved significantly with Adjusted EBITDA up 20% year-over-year and margin expansion of 4 percentage points:

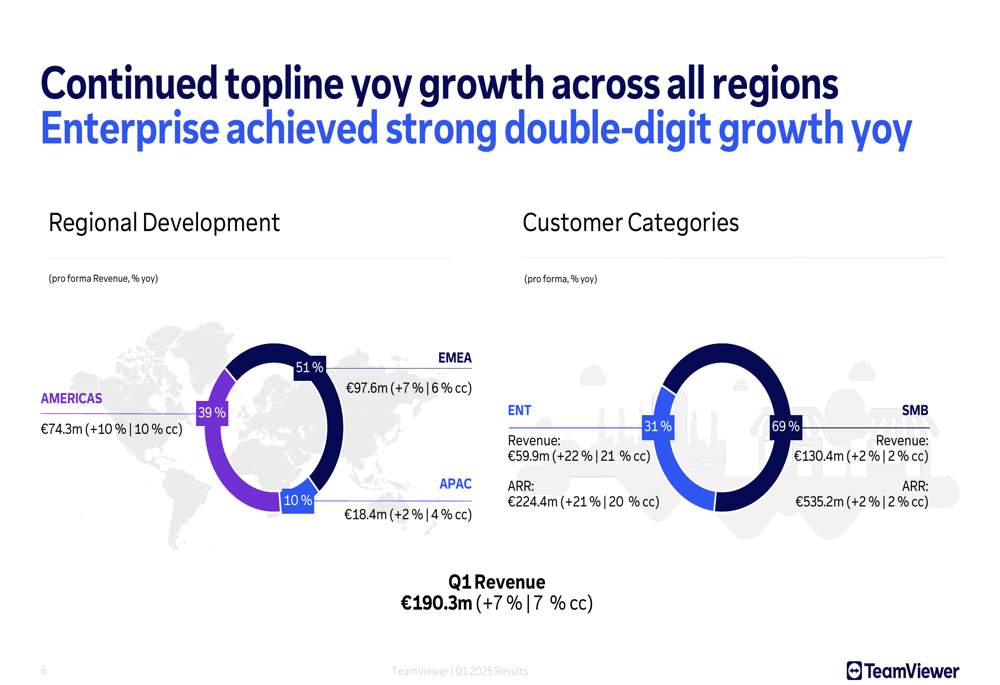

The company’s regional performance remained solid across all major markets, with the Americas showing the strongest growth at 10% (constant currency), followed by EMEA at 6% and APAC at 4%. Enterprise customers now represent 31% of total revenue, up from 28% in the same period last year.

The following regional and customer category breakdown illustrates TeamViewer’s global performance:

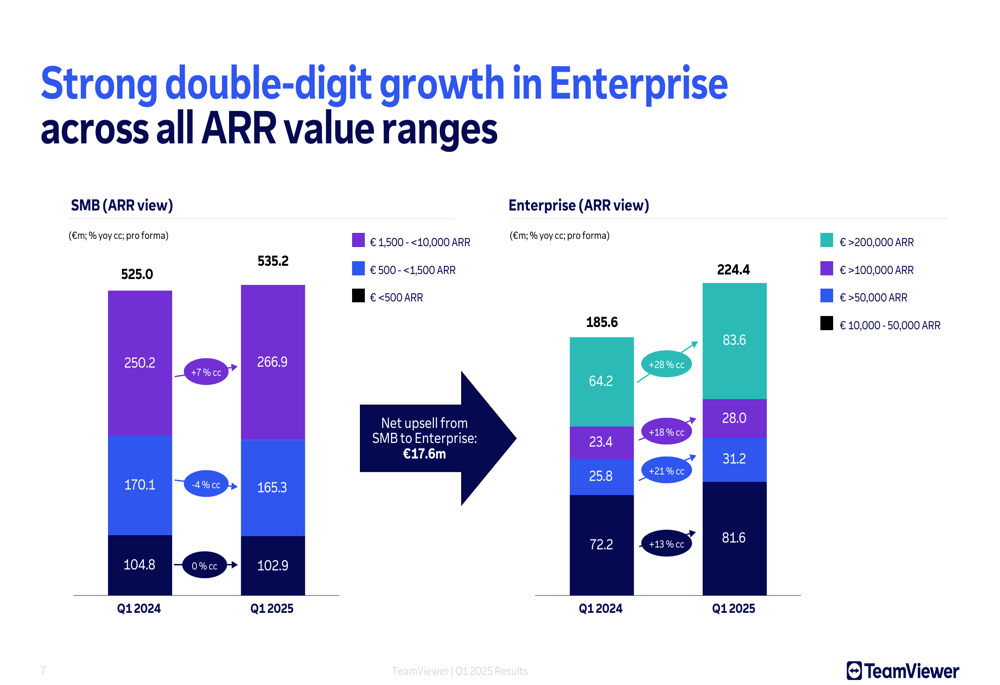

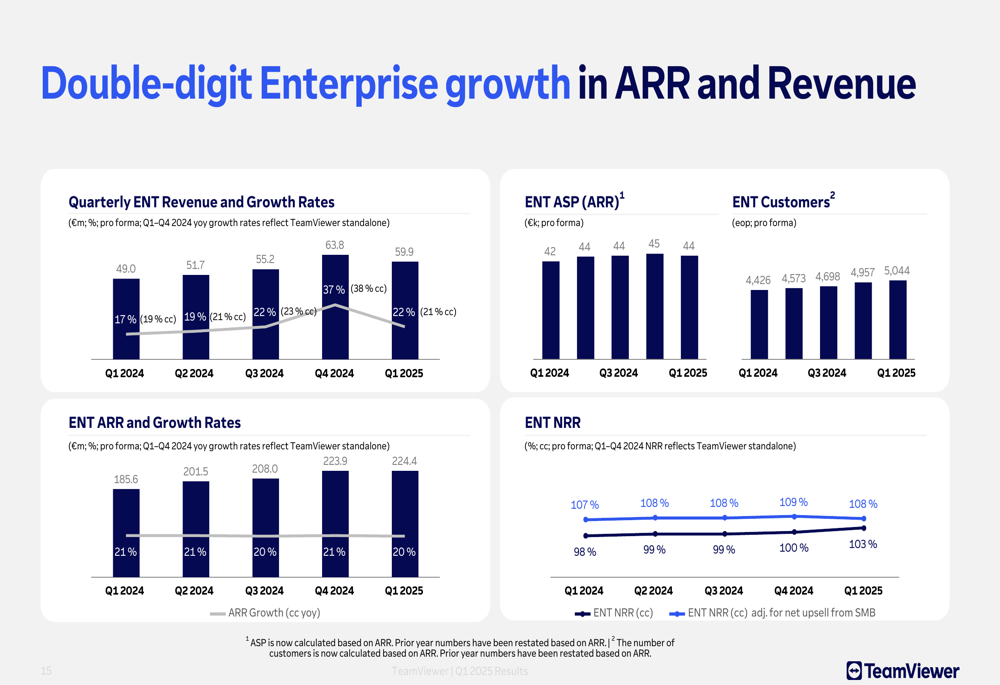

A particularly bright spot in the results was the Enterprise segment’s strong double-digit growth across all ARR value ranges. The highest growth came from customers in the €10,000-50,000 ARR range, which increased 28% year-over-year. Meanwhile, the company reported net upsell from SMB to Enterprise of €17.6 million, indicating successful customer migration to higher-value services.

The following chart demonstrates the strong Enterprise growth across different customer segments:

Detailed Financial Analysis

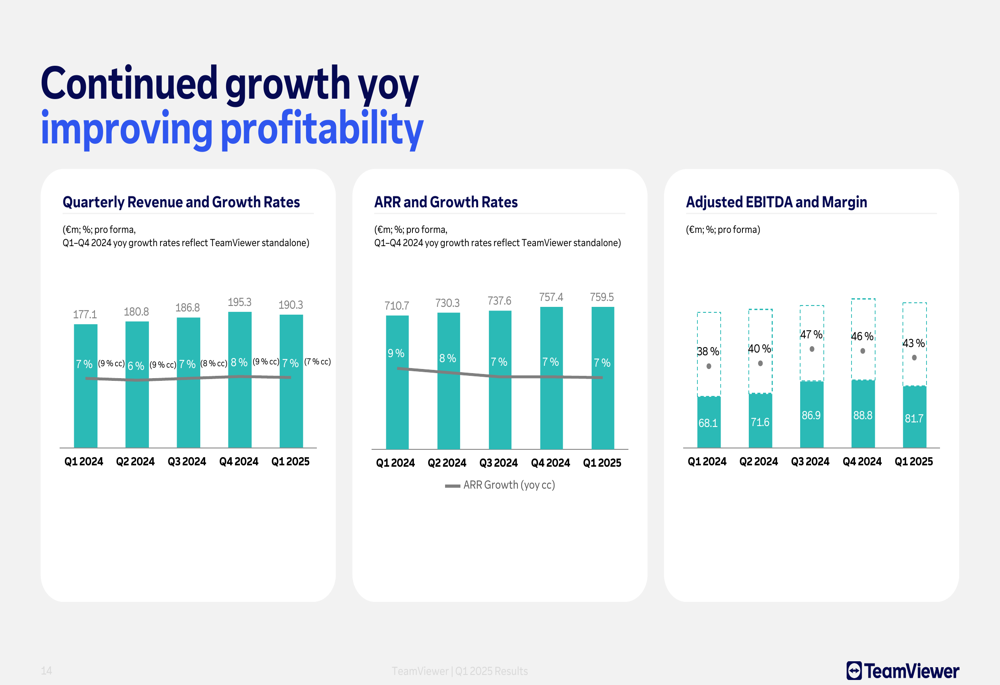

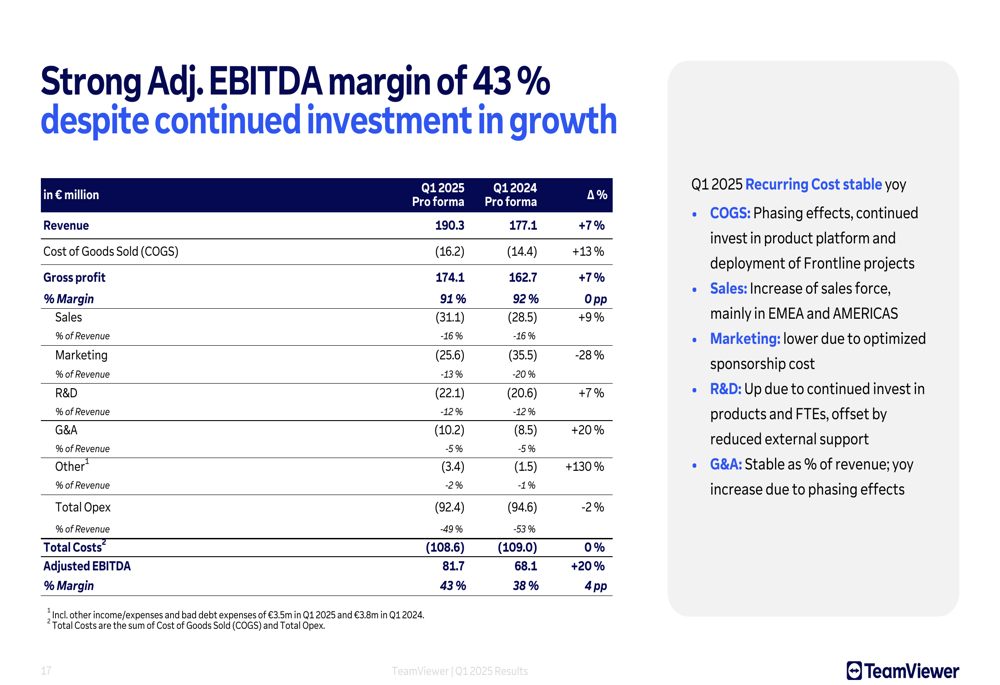

TeamViewer’s quarterly revenue and ARR have shown consistent growth over the past five quarters, while Adjusted EBITDA margins have remained strong in the 38-47% range. The Q1 2025 Adjusted EBITDA margin of 43% represents a significant improvement from 38% in Q1 2024.

The following chart illustrates these key financial trends:

The Enterprise segment continues to be the company’s growth engine, with both revenue and ARR showing consistent double-digit increases. Enterprise customer count grew to 5,044 by the end of Q1 2025, up from 4,426 a year earlier, while average selling price remained stable at €44,000.

The Enterprise performance metrics demonstrate the segment’s strong momentum:

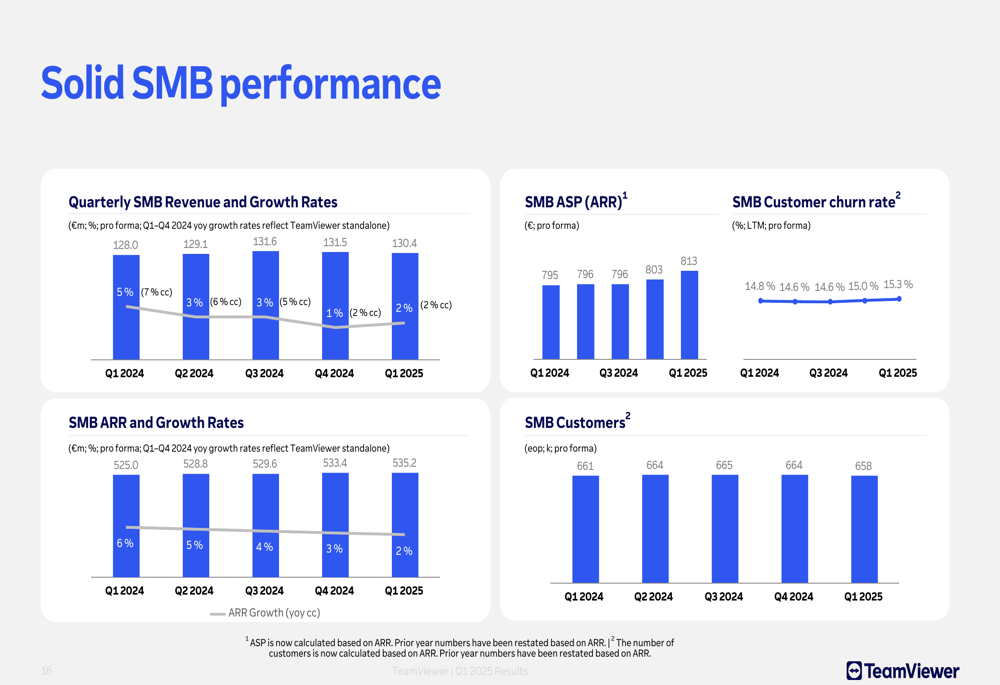

By contrast, the SMB segment showed more modest growth, with revenue up just 2% year-over-year in constant currency to €130.4 million. SMB ARR grew at the same 2% rate to €535.2 million. The company noted a slight increase in customer churn rate to 15.3%, up from 14.8% a year earlier, which may be contributing to the segment’s slower growth.

The following SMB performance metrics highlight the challenges in this segment:

Despite continued investments in growth initiatives, TeamViewer maintained strong profitability with an Adjusted EBITDA margin of 43%. This improvement was primarily driven by more efficient marketing spend, which decreased from 20% of revenue in Q1 2024 to 13% in Q1 2025.

The detailed breakdown of the company’s cost structure shows this efficiency improvement:

Strategic Initiatives

TeamViewer’s Q1 focused on building its Enterprise pipeline and laying the groundwork for accelerated SMB business for the remainder of 2025. A key strategic initiative is the integration of 1E, a digital employee experience (DEX) company acquired recently.

The company launched its first integration of 1E’s DEX capabilities into TeamViewer’s Remote Monitoring and Management (RMM) product in March, providing deeper endpoint visibility and proactive troubleshooting for customers. Additionally, TeamViewer introduced "DEX Essentials" as a new add-on for SMB customers, currently available in an early-access program.

To support its SMB focus, TeamViewer appointed new leadership, including Debbie Lillitos as Chief Customer Officer and Rolf Anweiler as SVP SMB. The company also launched a new brand campaign in late April with the tagline "Make work work better."

Forward-Looking Statements

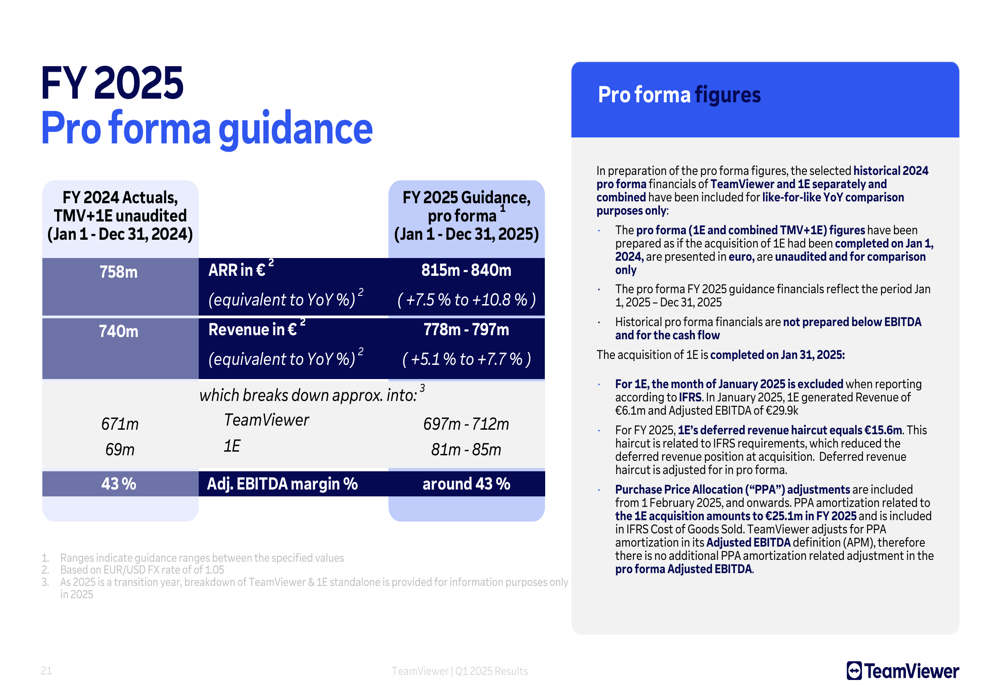

TeamViewer reiterated its full-year 2025 guidance, projecting pro forma revenue between €778 million and €797 million, representing growth of 5.1% to 7.7% compared to 2024. The company expects ARR to reach €815-840 million, growing 7.5% to 10.8% year-over-year, with an Adjusted EBITDA margin of around 43%.

The guidance breakdown shows expectations for both TeamViewer’s core business and the 1E acquisition:

Management expects the 1E business to contribute €81-85 million to total revenue in 2025, up from €69 million in 2024, indicating strong growth from the acquisition. The core TeamViewer business is projected to grow from €671 million to €697-712 million.

The company’s net leverage ratio improved to 3.1x, down from previous quarters, reflecting optimized financing following the 1E acquisition. TeamViewer continues to focus on debt reduction while maintaining investments in growth initiatives.

Despite the solid results and maintained guidance, the market’s negative reaction suggests investors may have had higher expectations or concerns about the slower growth in the larger SMB segment, which still accounts for 69% of total revenue. The company’s ability to accelerate SMB growth while maintaining Enterprise momentum will be crucial for meeting its full-year targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.