Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Teck Resources Ltd (NYSE:TECK) presented its first quarter 2025 results on April 24, highlighting significant financial improvements and progress on its strategic copper growth initiatives. The Canadian mining company’s shares rose 4.33% to $36.39 following the presentation, as investors responded positively to the doubled EBITDA and successful ramp-up of its Quebrada Blanca (QB) copper project.

The company’s results come amid strong copper market fundamentals, with concentrate tightness putting financial pressure on smelters and long-term demand expected to be driven by global electrification trends. Teck’s strategic positioning in energy transition metals, particularly copper, appears well-timed as industrial policy, national security concerns, and the digital economy continue to drive robust commodity demand.

Quarterly Performance Highlights

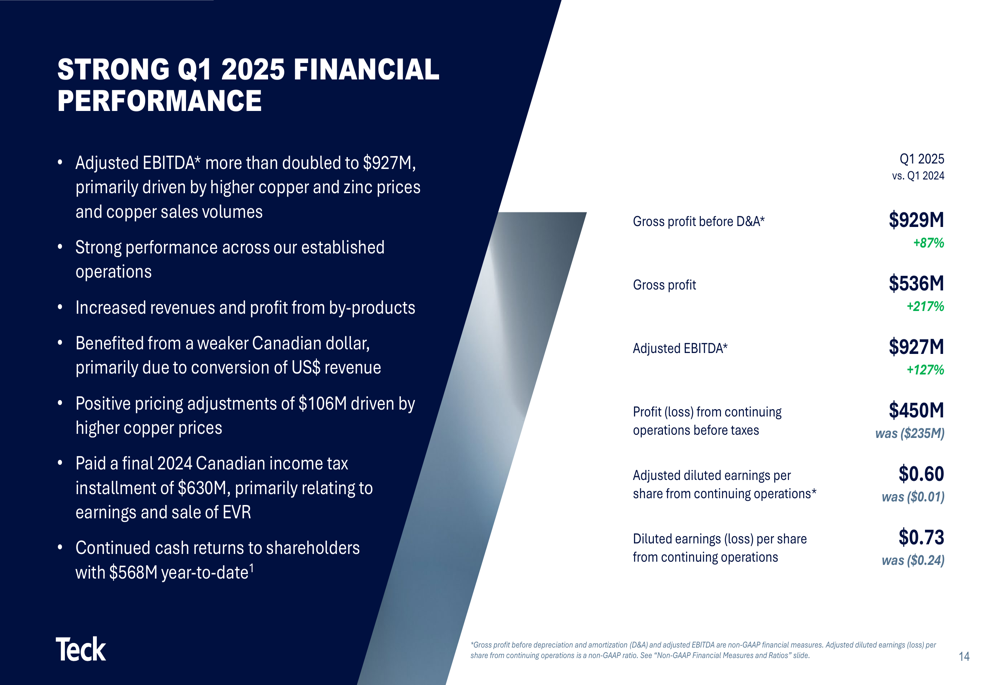

Teck delivered exceptional financial results in Q1 2025, with adjusted EBITDA more than doubling year-over-year to $927 million. The company’s strong operational performance across established operations, combined with favorable pricing and exchange rates, contributed to this significant improvement.

As shown in the following financial performance comparison:

The company reported gross profit before depreciation and amortization of $929 million, an 87% increase from Q1 2024. Gross profit surged 217% to $536 million, while profit from continuing operations before taxes reached $450 million compared to a loss of $235 million in the prior-year quarter. Adjusted diluted earnings per share from continuing operations improved to $0.60 from a loss of $0.01 in Q1 2024.

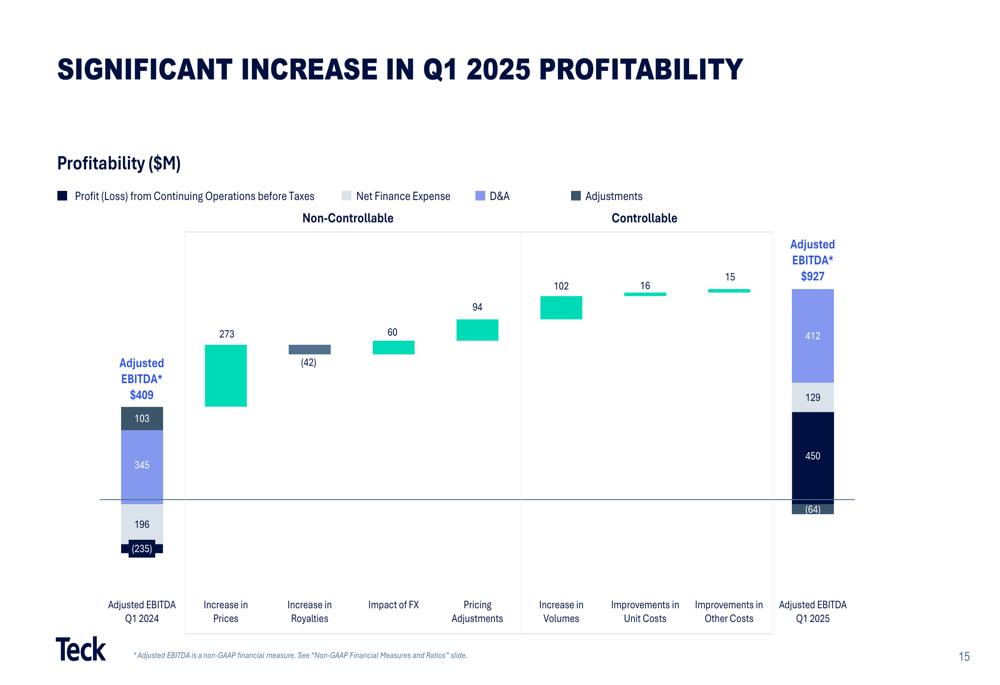

A detailed breakdown of the factors driving this profitability increase is illustrated in this waterfall chart:

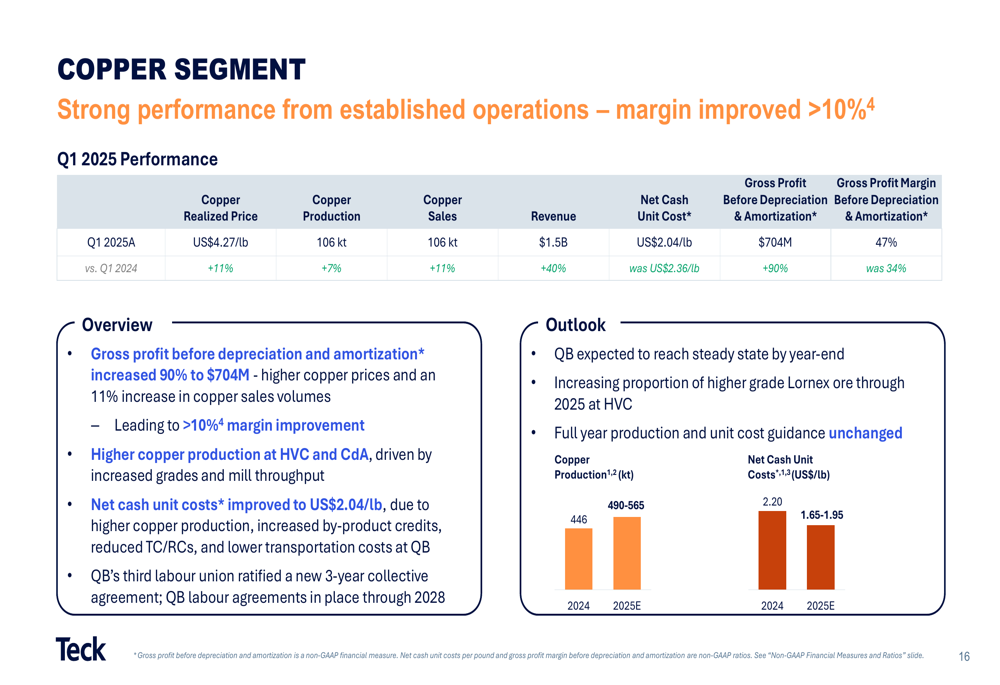

The copper segment delivered particularly strong results, with a gross profit margin before depreciation and amortization of 47%. The realized copper price was US$4.27/lb, with production and sales both at 106 kt for the quarter.

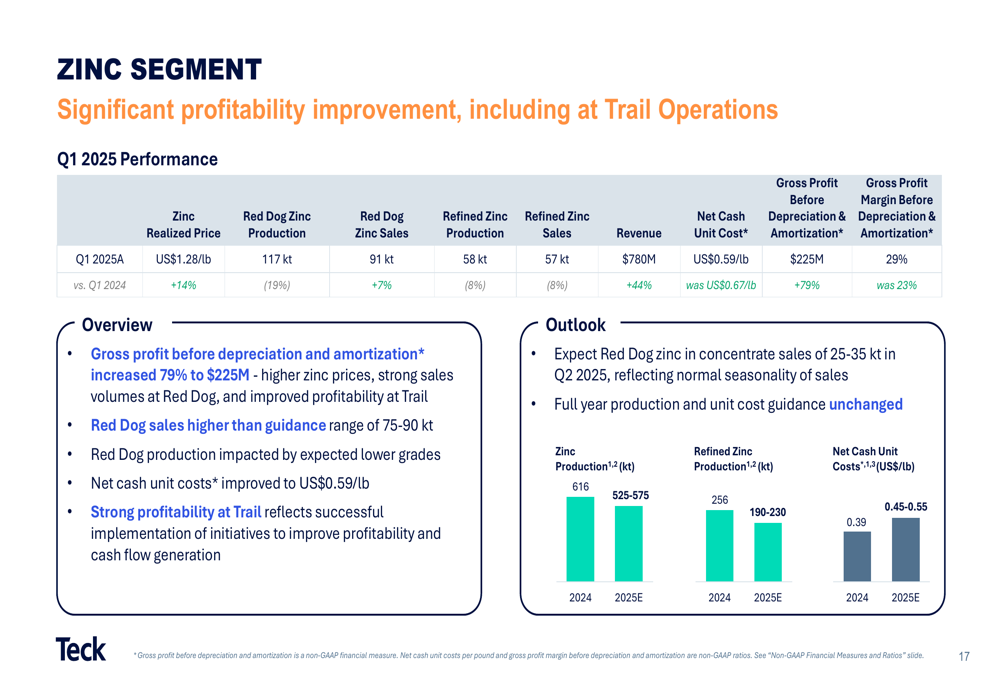

Similarly, the zinc segment showed significant profitability improvement, especially at Trail Operations. With a realized zinc price of US$1.28/lb, Red Dog zinc production reached 117 kt, while sales were 91 kt, reflecting normal seasonality. The segment achieved a gross profit before depreciation and amortization of $225 million, representing a 29% margin.

Copper Growth Strategy

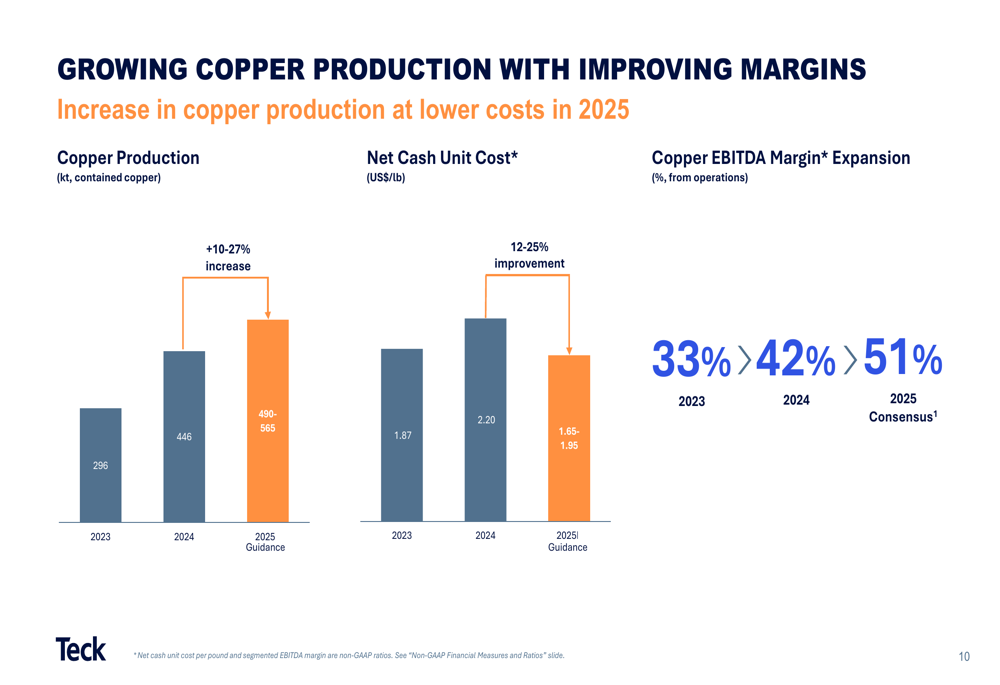

A central theme of Teck’s presentation was its focus on growing copper production with improving margins. The company is targeting increased copper production from 296 kt in 2023 to between 490-565 kt in 2025, while simultaneously reducing net cash unit costs from US$2.20/lb to US$1.65-1.95/lb. This combination is expected to expand copper EBITDA margins from 33% in 2023 to 51% in 2025, based on consensus estimates.

The following chart illustrates this growth trajectory:

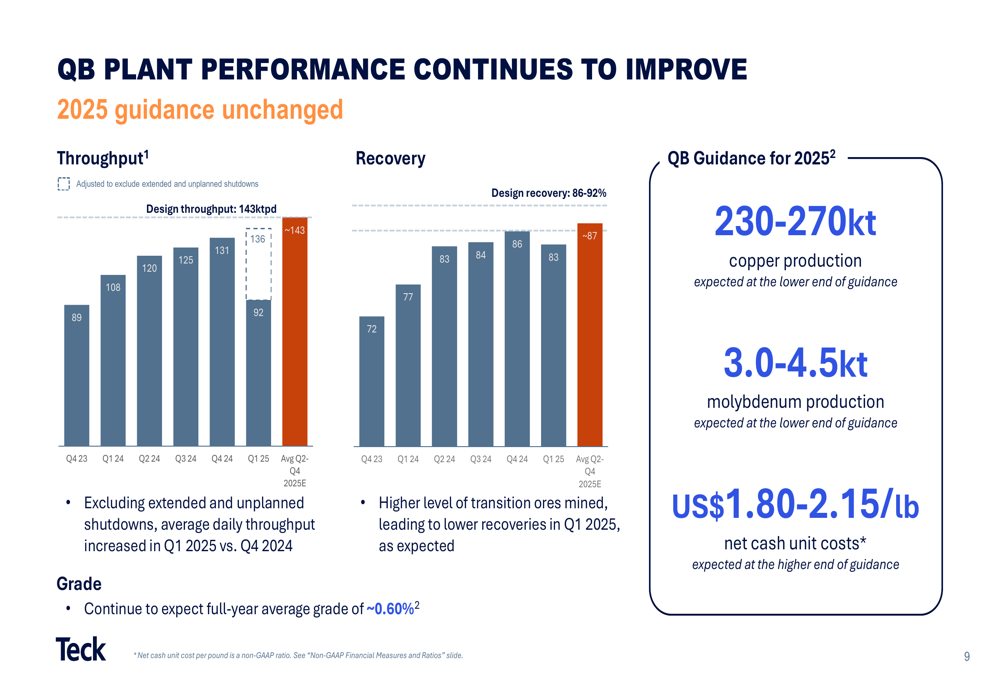

The successful ramp-up of the QB project is a critical component of this strategy. Teck reported that completion testing has been achieved at QB, with plant performance continuing to improve. The company provided guidance for QB of 230-270 kt copper production and 3.0-4.5 kt molybdenum production in 2025, with net cash unit costs of US$1.80-2.15/lb.

As shown in the throughput and recovery charts:

Looking beyond 2025, Teck outlined a path to approximately 800 kt of annual copper production before the end of the decade through several value-accretive growth projects:

These near-term projects include Quebrada Blanca Optimization, Highland Valley Mine Life Extension, Zafranal, and San Nicolás, with potential sanction decisions planned for 2025. The total attributable estimated post-sanction capital for these projects is US$3.2-3.9 billion.

Financial Position and Capital Allocation

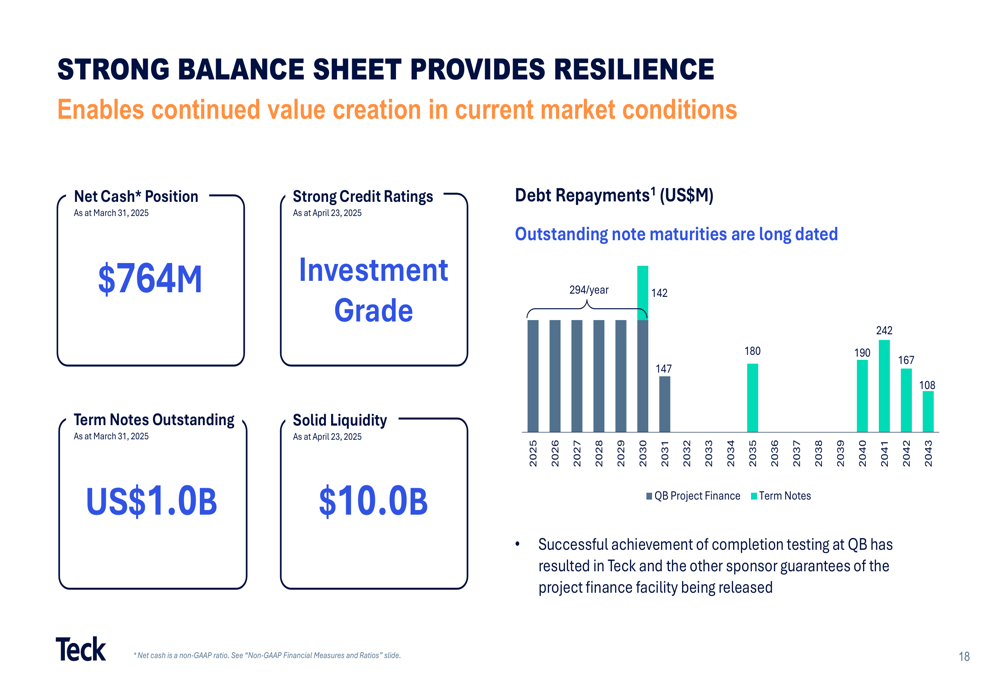

Teck’s strong balance sheet provides resilience for both growth investments and shareholder returns. The company reported a net cash position of $764 million, with solid liquidity of $10.0 billion. The successful achievement of completion testing at QB has resulted in the release of Teck and other sponsor guarantees of the project finance facility.

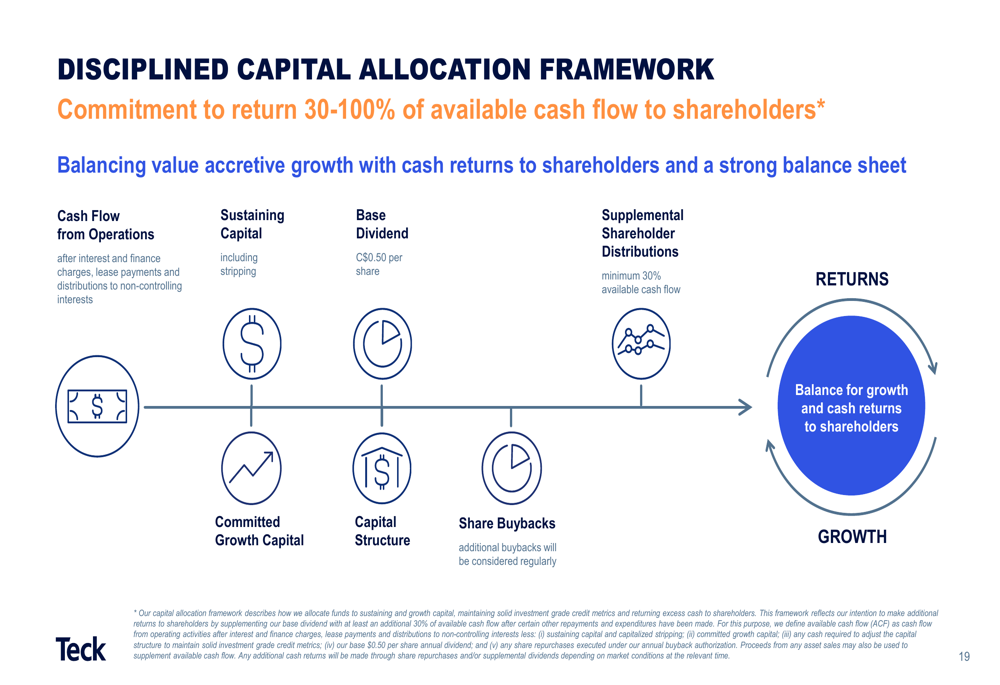

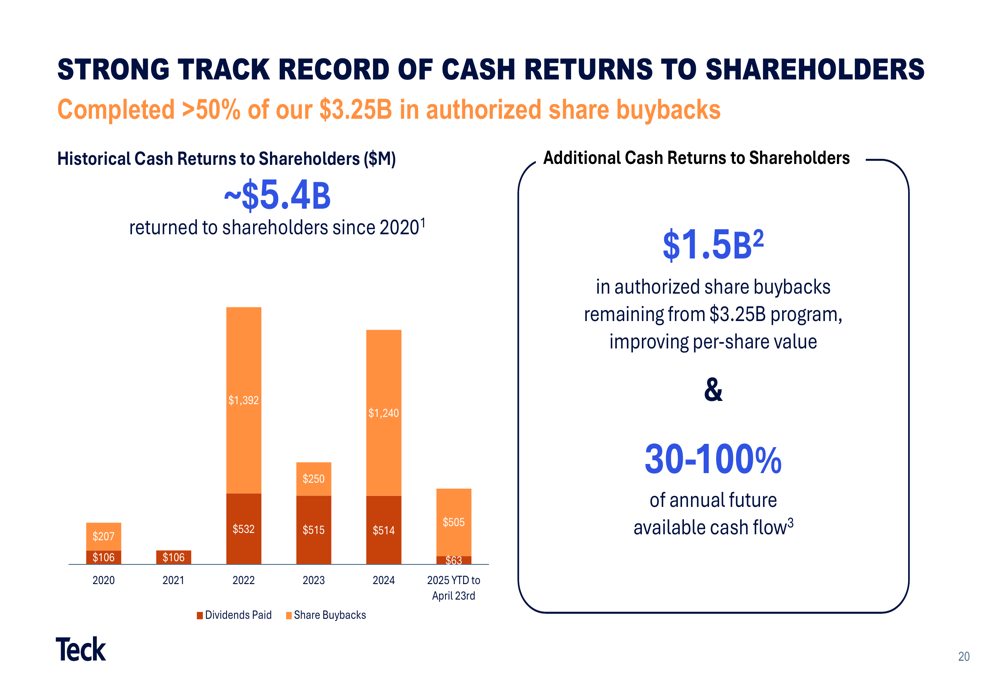

The company’s disciplined capital allocation framework balances growth investments with shareholder returns:

Teck has demonstrated a strong track record of cash returns to shareholders, with approximately $5.4 billion returned since 2020. The company has completed more than 50% of its $3.25 billion in authorized share buybacks and remains committed to returning 30-100% of annual available cash flow to shareholders.

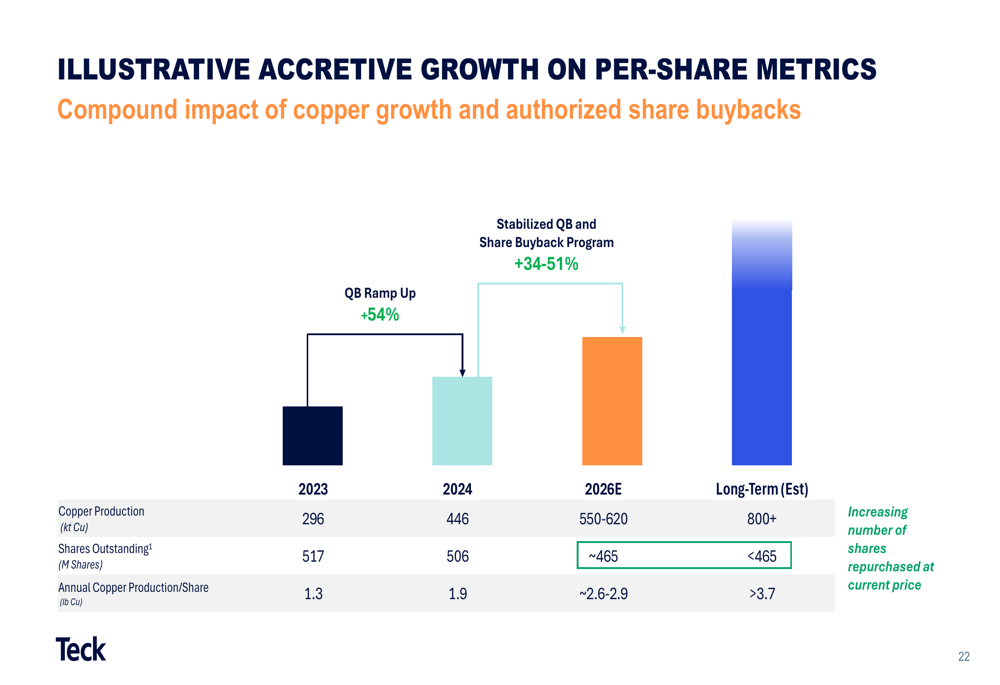

This strategy is expected to drive accretive growth on per-share metrics, with stabilized QB operations and the share buyback program projected to increase annual copper production per share from 1.3 lb in 2023 to more than 3.7 lb in the long term.

Forward-Looking Statements

Looking ahead, Teck is focused on five key value creation priorities: ramping up QB to steady state, growing copper production, continuing to execute the share buyback program, progressing value-accretive copper growth projects, and enabling resilience.

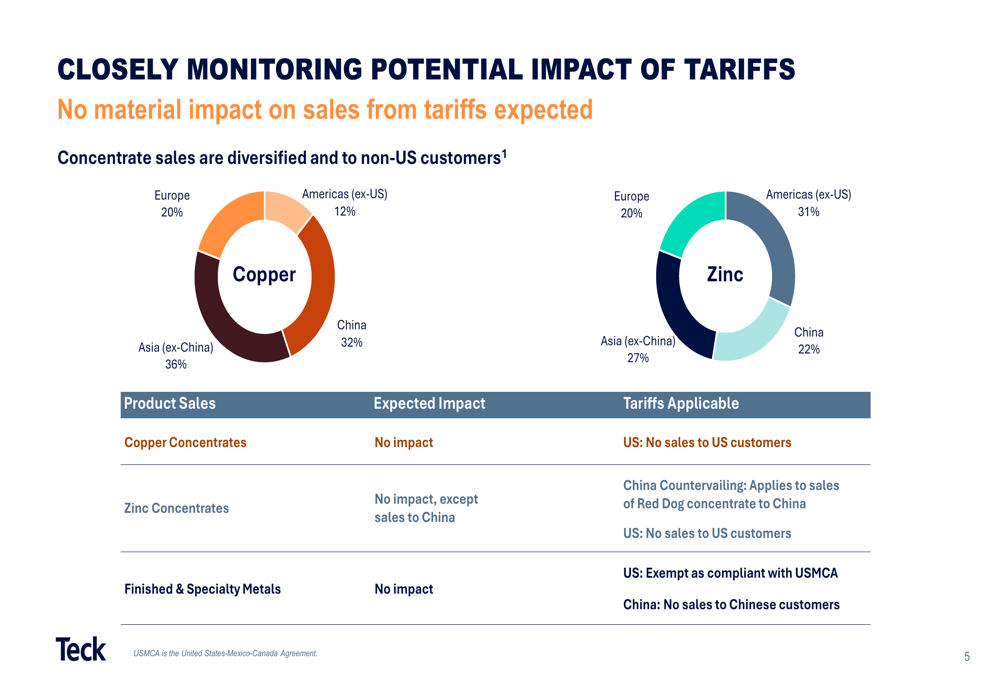

The company is closely monitoring the potential impact of tariffs but expects no material effect on its business, as concentrate sales are diversified and directed to non-US customers. Copper concentrate sales are distributed across Europe (20%), Asia excluding China (36%), Americas excluding US (12%), and China (32%), while zinc concentrate sales follow a similar pattern of geographical diversification.

For 2025, Teck has provided copper production guidance of 490-565 kt and zinc production guidance of 525-575 kt from Red Dog. The company expects to maintain its strong financial position while advancing its growth projects and continuing its share buyback program at approximately the same pace as in recent quarters.

With robust commodity fundamentals, a growing copper production profile, and a disciplined approach to capital allocation, Teck appears well-positioned to deliver on its strategy of responsible growth and value creation in the energy transition metals sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.