IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

Teck Resources Ltd (NYSE:TECK) released its second quarter 2025 earnings presentation on July 24, 2025, reporting higher profitability despite revising down production guidance for its Quebrada Blanca (QB) copper mine. The company’s stock fell 5.53% on the day of the announcement, with the share price closing at $36.46, down from the previous close of $38.59.

The mining company reported a 3% increase in adjusted EBITDA to $722 million and a substantial 525% jump in profit from continuing operations before taxes to $125 million, as it continues to focus on its copper growth strategy while returning cash to shareholders through its buyback program.

Quarterly Performance Highlights

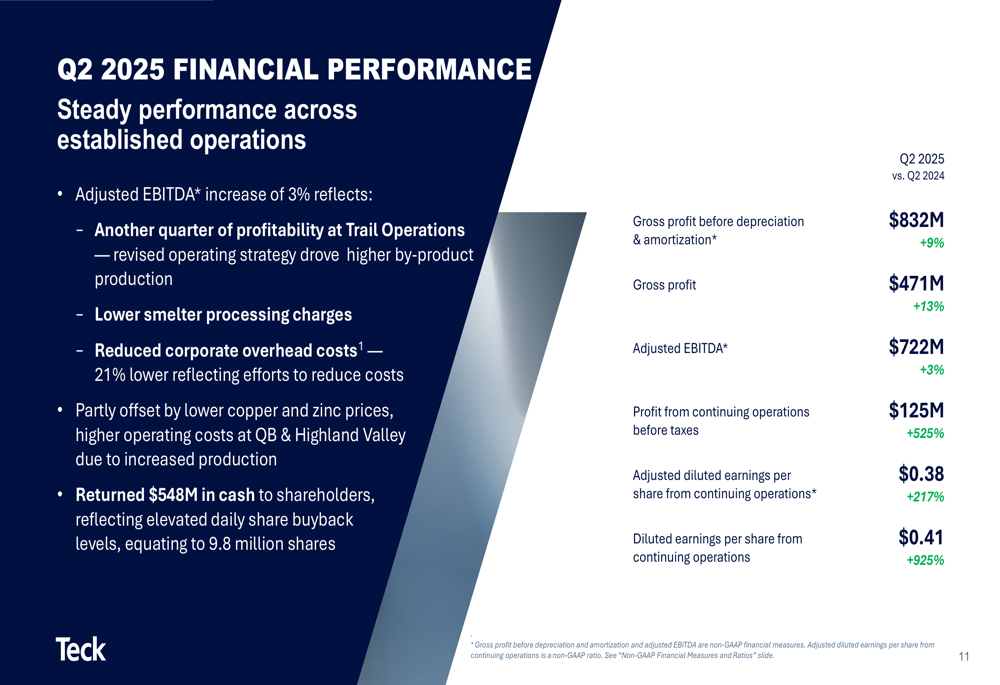

Teck delivered steady performance across its established operations in Q2 2025, with gross profit before depreciation and amortization increasing 9% to $832 million, while gross profit rose 13% to $471 million compared to the same period last year.

The company reported adjusted diluted earnings per share from continuing operations of $0.38, representing a 217% increase year-over-year, while diluted earnings per share from continuing operations jumped 925% to $0.41.

As shown in the following financial performance overview:

Several factors contributed to the improved profitability, including another profitable quarter at Trail Operations, lower smelter processing charges, and reduced corporate overhead costs, which were 21% lower than the previous year. These positive factors were partially offset by lower copper and zinc prices, as well as higher operating costs at QB and Highland Valley due to increased production.

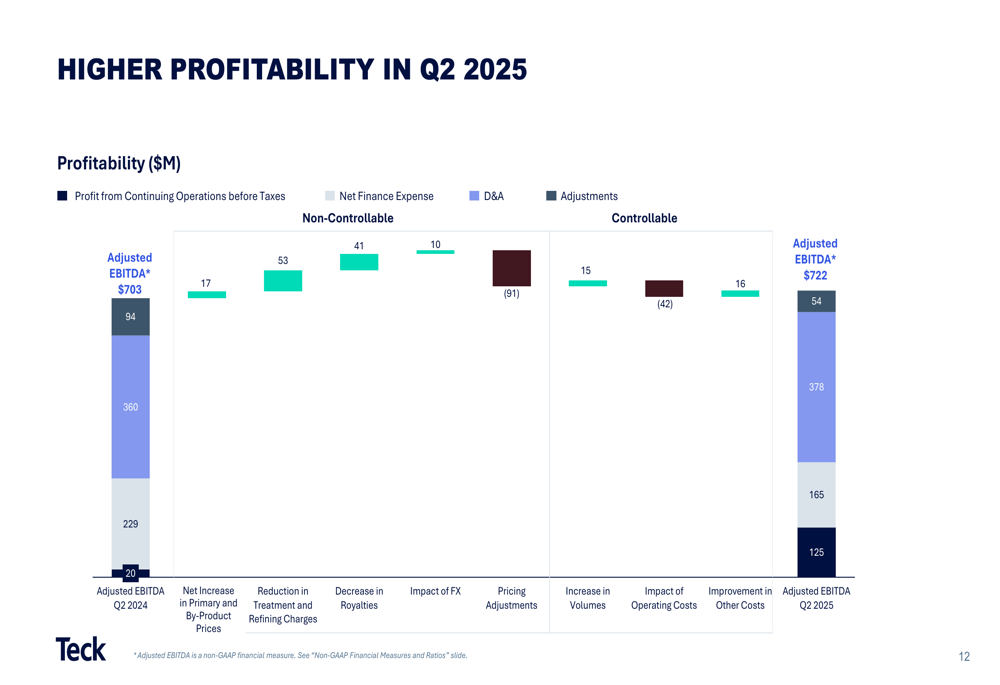

The following waterfall chart illustrates the various factors affecting the company’s profitability:

Detailed Financial Analysis

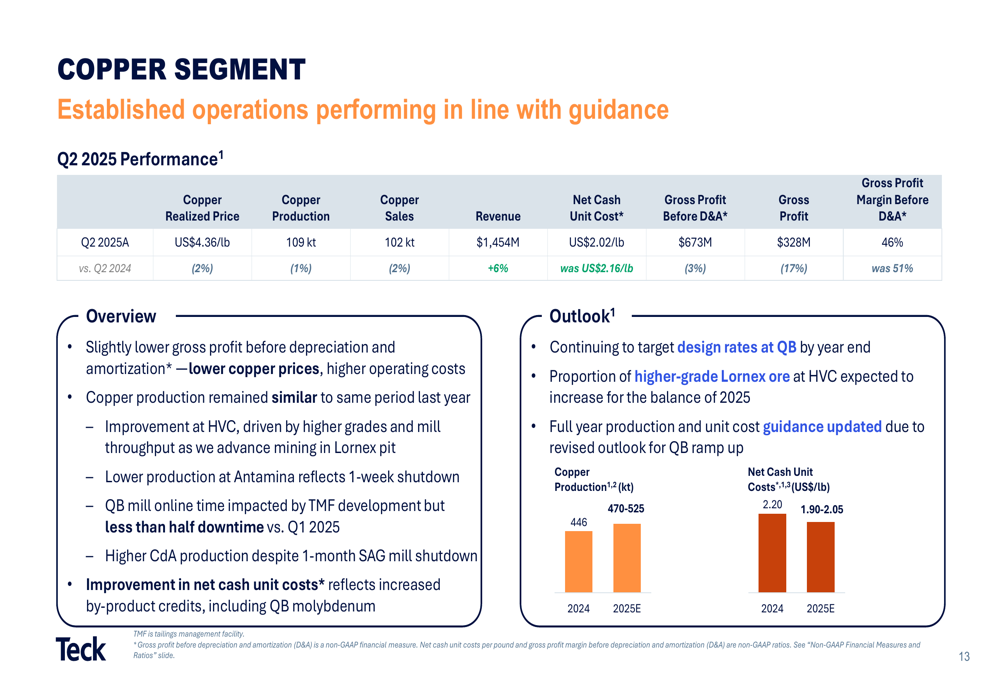

Teck’s Copper segment achieved a realized price of US$4.36/lb with production of 109 kt in Q2 2025, resulting in sales of 102 kt and revenue of $1,454 million. Net cash unit cost was US$2.02/lb, with gross profit before depreciation and amortization of $673 million and gross profit of $328 million, yielding a gross profit margin before depreciation and amortization of 46%.

The copper segment performance details are illustrated below:

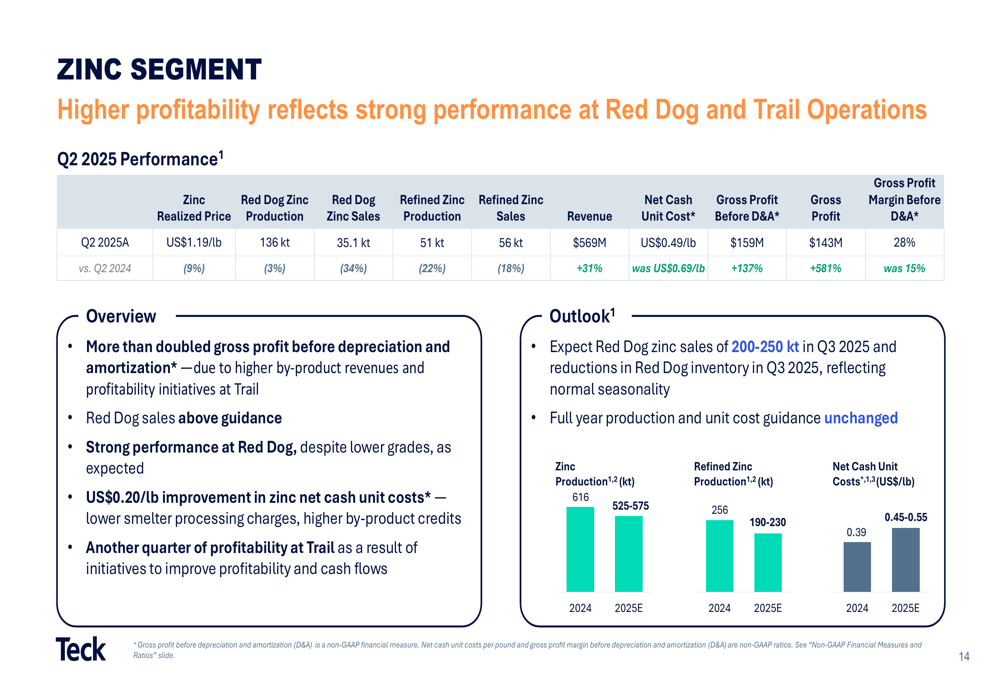

The Zinc segment showed particularly strong performance, with Red Dog sales exceeding guidance and significantly lower net cash unit costs. The segment achieved a realized zinc price of US$1.19/lb with production of 136 kt at Red Dog, resulting in sales of 35.1 kt (Red Dog) and 51 kt (refined), generating revenue of $569 million. Net cash unit cost was US$0.49/lb, with gross profit before depreciation and amortization of $159 million and gross profit of $143 million.

The zinc segment’s strong performance is detailed in the following chart:

Strategic Initiatives

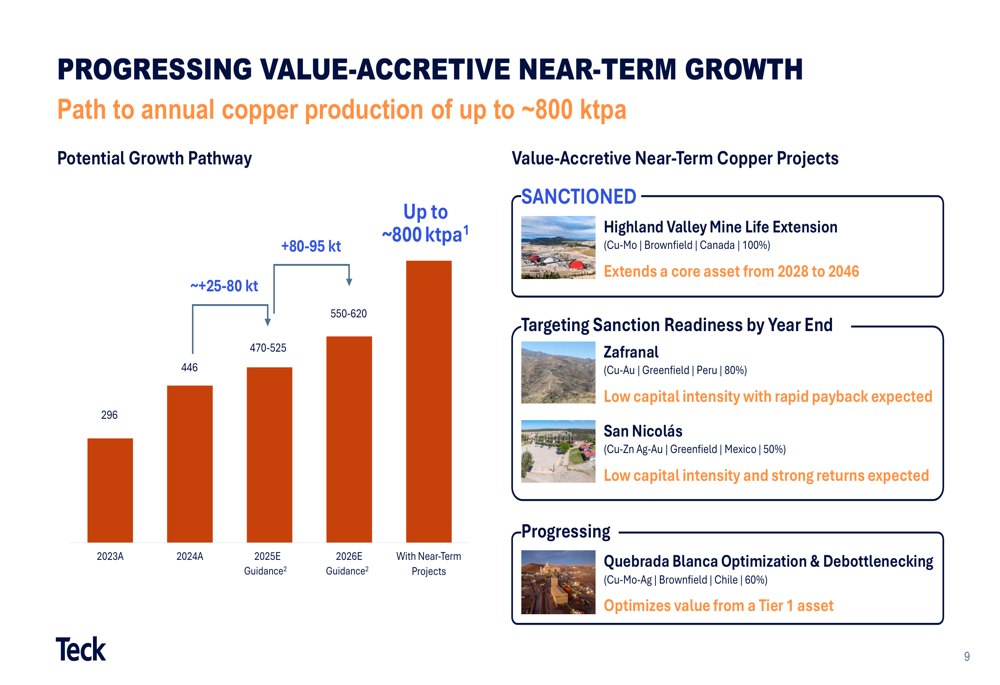

A central element of Teck’s strategy is advancing its copper growth initiatives. The company announced the sanction of the Highland Valley Copper Mine Life Extension (MLE) project, which will extend this core asset’s life from 2028 to 2046. The project has a capital estimate at sanction of C$2.1-2.4 billion and is expected to produce an average of 132 kt of copper annually over the life of mine.

The company is progressing toward its goal of increasing annual copper production to approximately 800 kt, as illustrated in the following chart:

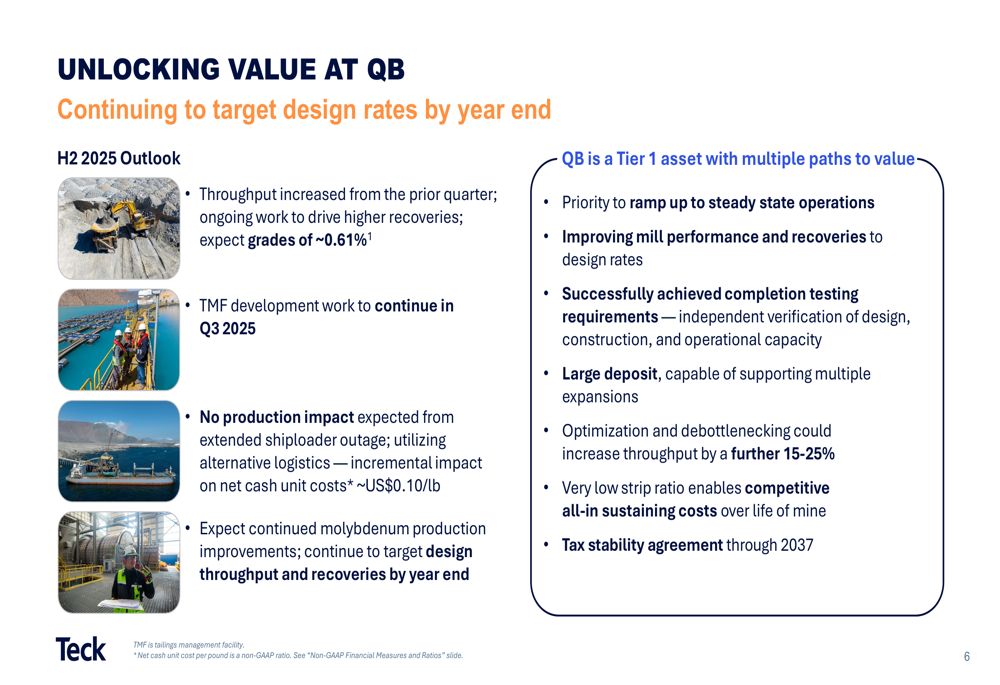

For the Quebrada Blanca (QB) mine, Teck is targeting design rates by year-end 2025, with a focus on increasing throughput and grades of approximately 0.61% in the second half of 2025. The company noted that QB is a Tier 1 asset with potential for optimization and debottlenecking that could increase throughput by a further 15-25%.

The QB strategy is outlined below:

Forward-Looking Statements

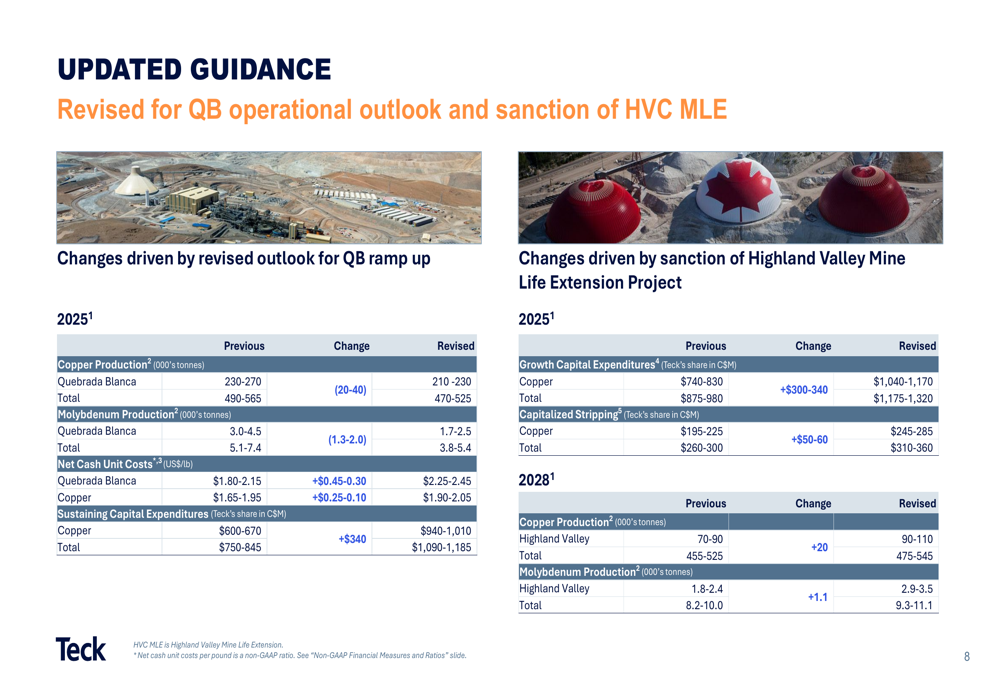

Teck has updated its guidance, revising down copper production estimates for Quebrada Blanca from 230-270 kt to 210-230 kt, and molybdenum production from 3.0-4.5 kt to 1.7-2.5 kt. Net cash unit costs for QB have been revised upward from US$1.80-2.15/lb to US$2.25-2.45/lb.

The company has also updated its capital expenditure guidance, increasing sustaining capital from $600-670 million to $940-1,010 million, growth capital from $740-830 million to $1,040-1,170 million, and capitalized stripping from $195-225 million to $245-285 million.

The updated guidance is presented in detail below:

Looking ahead, Teck is targeting several near-term copper projects to drive growth, including the already sanctioned Highland Valley Mine Life Extension, as well as Zafranal and San Nicolás, which are targeting sanction readiness by year-end. The company is also progressing with Quebrada Blanca optimization and debottlenecking efforts.

Shareholder Returns and Balance Sheet

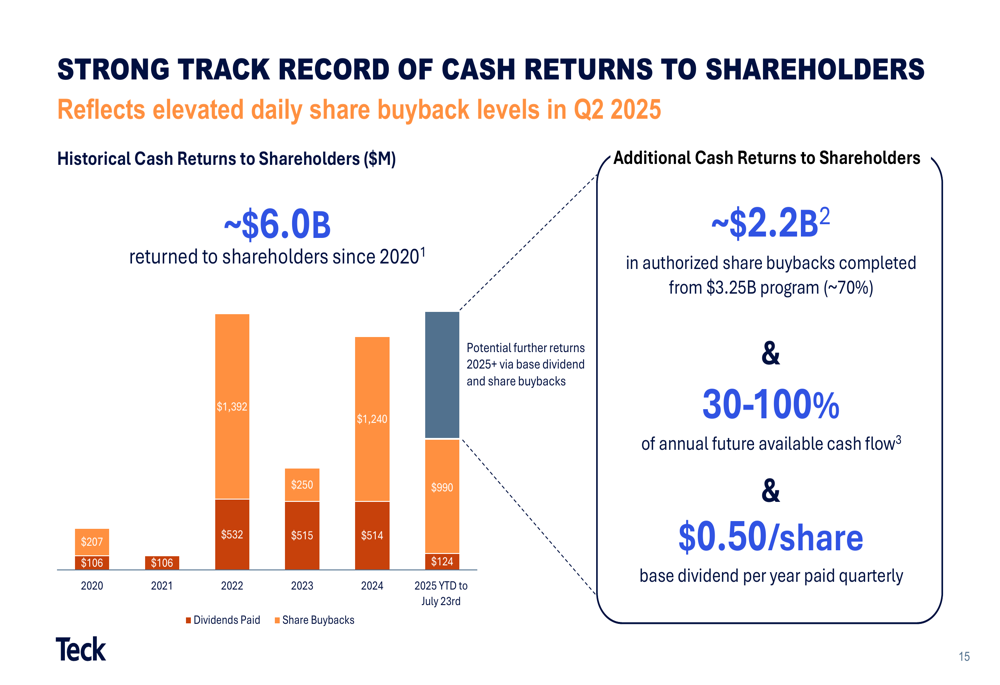

Teck continues to demonstrate a strong commitment to returning cash to shareholders. The company has completed approximately $2.2 billion of its $3.25 billion authorized share buyback program (about 70%) and maintains a base dividend of $0.50 per share per year, paid quarterly. In Q2 2025 alone, Teck returned $548 million in cash to shareholders.

Since 2020, Teck has returned approximately $6.0 billion to shareholders through dividends and share buybacks, as illustrated in the following chart:

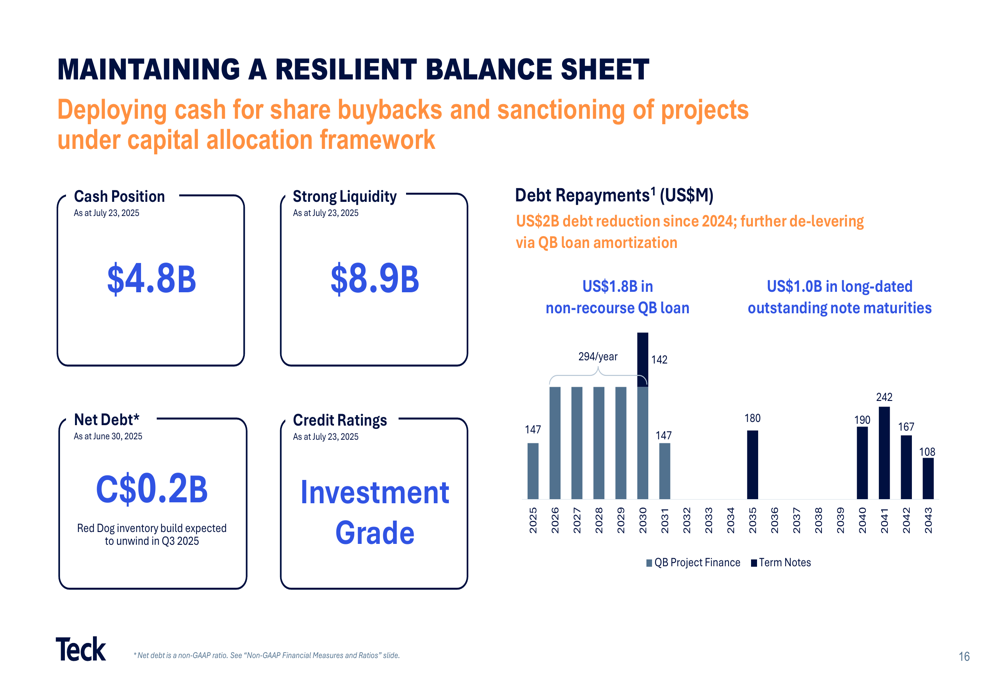

The company maintains a resilient balance sheet with a cash position of $4.8 billion as of July 23, 2025, strong liquidity of $8.9 billion, and net debt of just C$0.2 billion as of June 30, 2025. Teck’s credit ratings remain at investment grade levels.

The company’s debt repayment schedule is shown below:

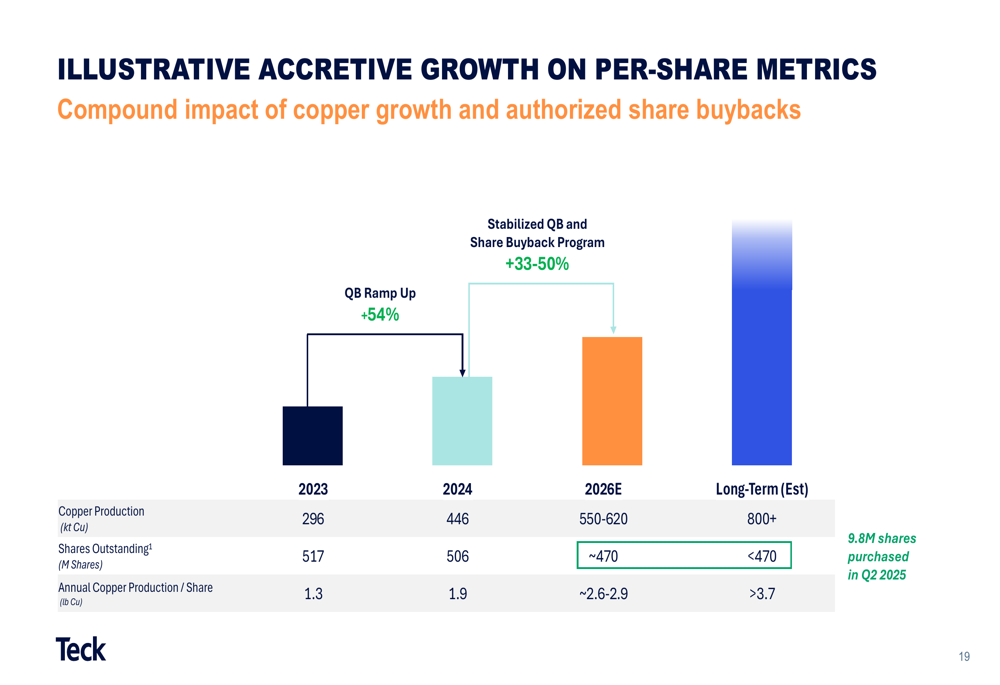

Teck is also focusing on accretive growth on a per-share basis, with the compound impact of copper growth and authorized share buybacks expected to significantly increase annual copper production per share from 1.9 in 2024 to approximately 2.6-2.9 in 2026, and potentially over 3.7 in the long term.

This per-share growth is illustrated in the following chart:

In conclusion, while Teck Resources faces challenges with its QB ramp-up, necessitating revised production guidance, the company delivered strong financial results in Q2 2025 and continues to advance its copper growth strategy while maintaining its commitment to shareholder returns and balance sheet strength.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.