NHL signs licensing deals with prediction-market startups Kalshi and Polymarket - WSJ

Introduction & Market Context

Teladoc Inc (NYSE:TDOC) released its second quarter 2025 financial results on July 29, showing continued revenue challenges amid a post-pandemic normalization in telehealth demand. The company’s stock fell sharply following the announcement, dropping 8.29% to close at $8.20, with an additional 1.1% decline in after-hours trading, reflecting investor concerns about the company’s growth trajectory and profitability.

The telehealth provider reported a 2% year-over-year revenue decline to $632 million, with its BetterHelp mental health segment continuing to face headwinds while the Integrated Care segment showed modest stability. Despite these challenges, Teladoc demonstrated improved cash flow generation and a reduced net loss compared to the previous quarter.

Quarterly Performance Highlights

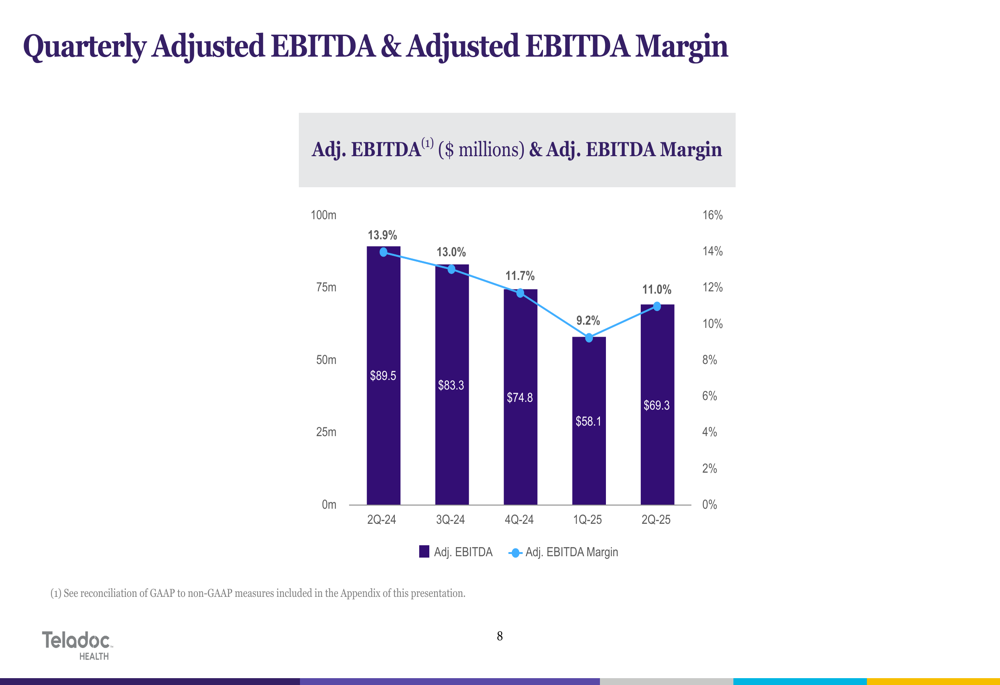

Teladoc reported a net loss per share of $0.19 for Q2 2025, which represents an improvement from the $0.53 loss reported in Q1. The company’s adjusted EBITDA came in at $69.3 million, marking a 23% year-over-year decline, though showing sequential improvement from Q1’s $58.1 million.

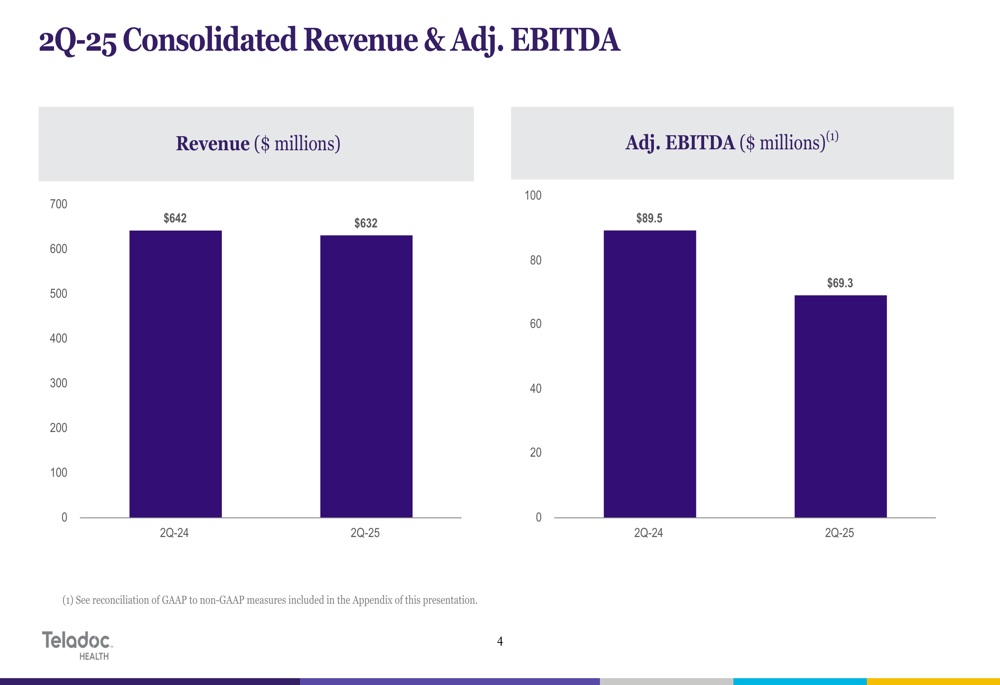

As shown in the following chart of quarterly consolidated revenue and adjusted EBITDA:

Revenue decreased from $642 million in Q2 2024 to $632 million in Q2 2025, while adjusted EBITDA fell from $89.5 million to $69.3 million over the same period. This represents a continued challenge for the company as it navigates the post-pandemic telehealth landscape.

The company’s adjusted EBITDA margin has also shown a declining trend over the past year, though with some sequential improvement in the most recent quarter:

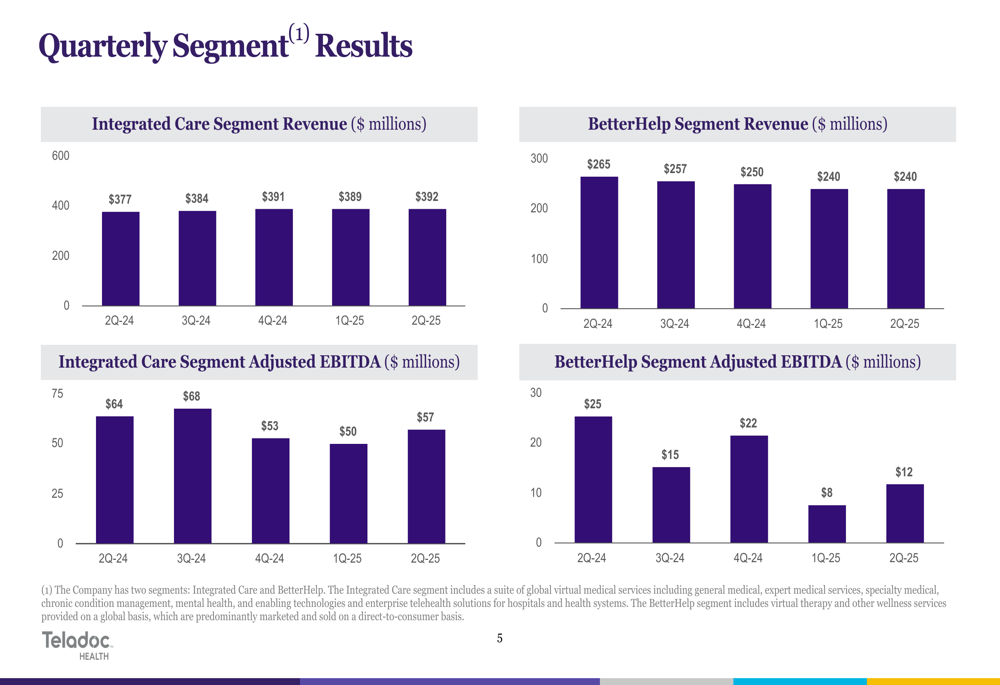

Segment Analysis

Teladoc’s business performance shows a clear divergence between its two main segments. The Integrated Care segment, which includes virtual medical services and enterprise solutions, demonstrated stability with a slight revenue increase to $392 million in Q2 2025 from $377 million in Q2 2024. Meanwhile, the BetterHelp segment, focused on direct-to-consumer mental health services, continued to struggle with revenue declining to $240 million from $265 million a year earlier.

The following chart illustrates the quarterly segment performance:

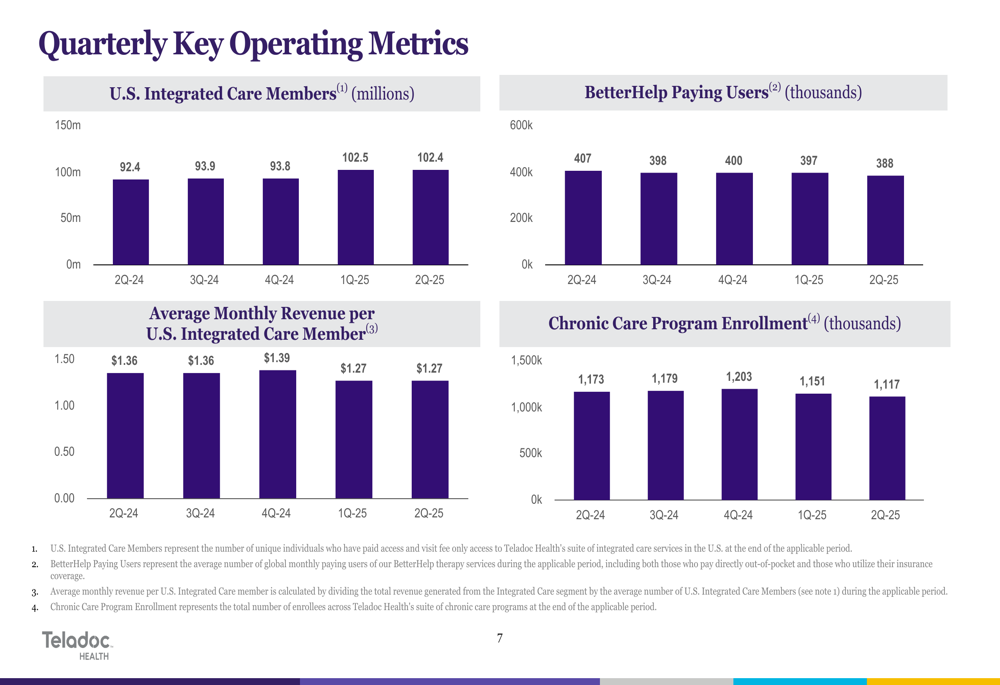

The U.S. Integrated Care membership remained stable at 102.4 million members, showing minimal change from the previous quarter but representing significant growth from 92.4 million in Q2 2024. However, BetterHelp paying users continued to decline, falling to 388,000 from 407,000 a year earlier. Chronic care program enrollment also showed a concerning trend, decreasing to 1.117 million from 1.173 million in Q2 2024.

These key operating metrics are visualized in the following chart:

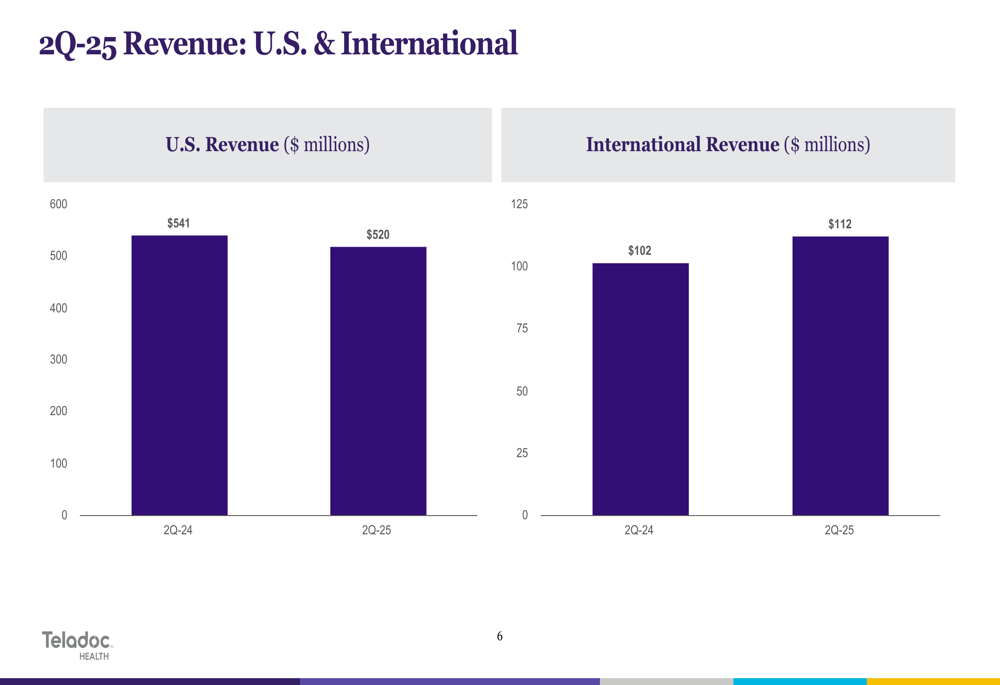

From a geographic perspective, Teladoc’s U.S. revenue declined by 3.9% year-over-year to $520 million, while international revenue showed encouraging growth of 9.8% to $112 million, suggesting potential opportunities in overseas markets.

Financial Position & Cash Flow

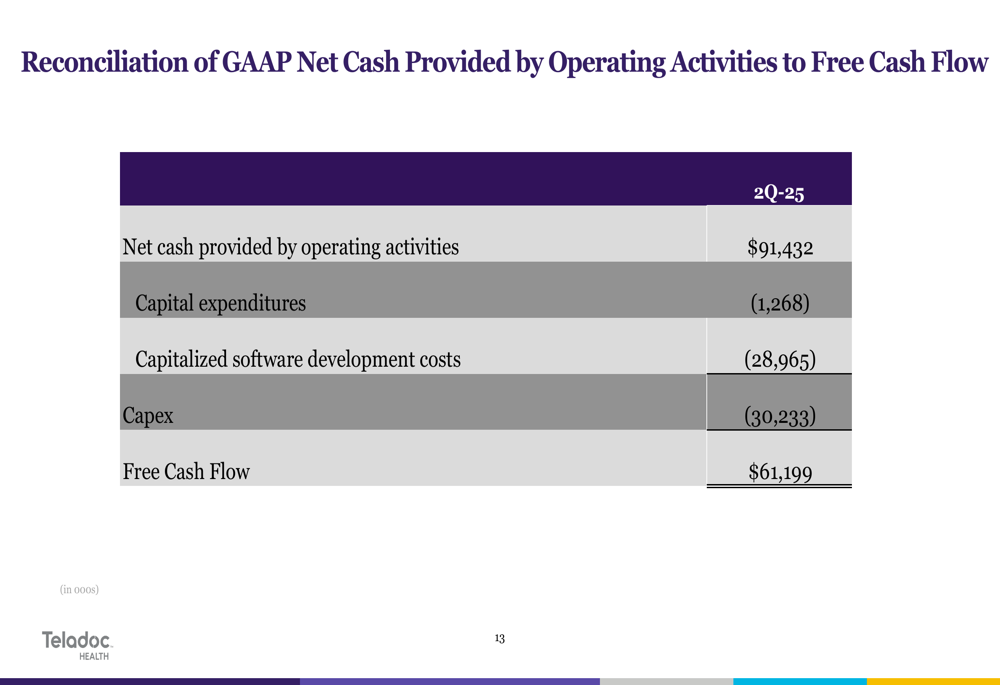

Despite revenue challenges, Teladoc demonstrated strong cash flow generation in Q2 2025, with operating cash flow of $91 million and free cash flow of $61 million. This represents a significant improvement from Q1 2025, which saw a net cash outflow of $16 million.

The company reported $680 million in cash and cash equivalents as of June 30, 2025, a notable decrease from the "nearly $1.2 billion" reported at the end of Q1 2025. Convertible senior notes stood at $993 million.

The following reconciliation shows how Teladoc calculated its free cash flow for the quarter:

Outlook & Guidance

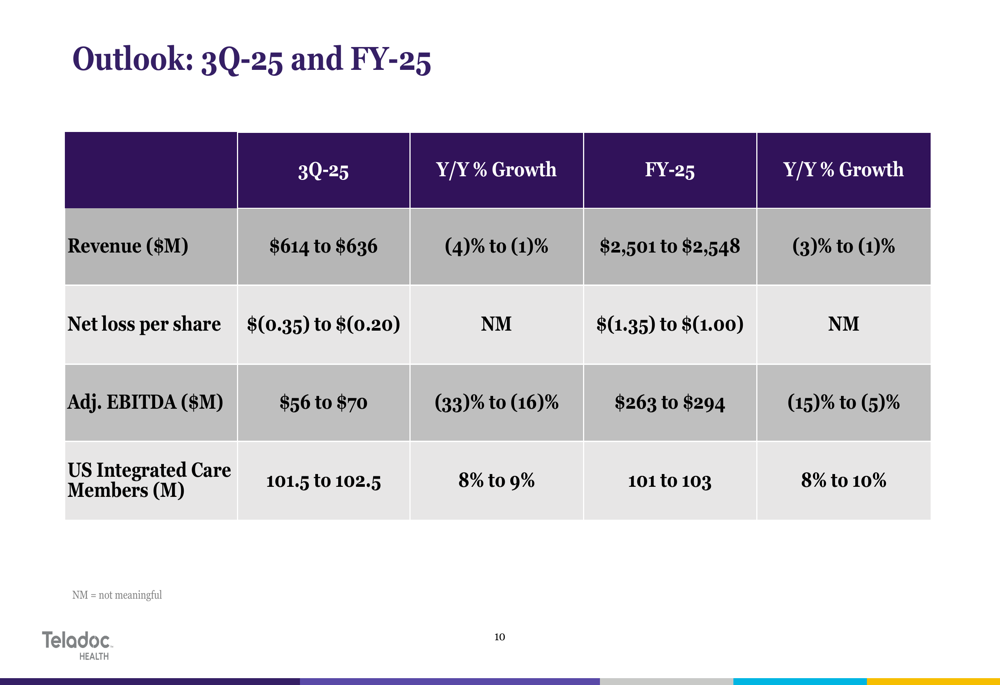

Teladoc provided guidance for both Q3 2025 and the full fiscal year, projecting continued revenue challenges but maintaining its commitment to profitability improvement. For Q3 2025, the company expects revenue between $614 million and $636 million, representing a year-over-year decline of 1% to 4%. Full-year revenue is projected at $2,501 million to $2,548 million, a decrease of 1% to 3% compared to fiscal 2024.

The company’s detailed outlook is presented in the following table:

Adjusted EBITDA is expected to continue facing pressure, with Q3 guidance of $56 million to $70 million (a decline of 16% to 33% year-over-year) and full-year guidance of $263 million to $294 million (a decline of 5% to 15%).

Market Reaction

Investors responded negatively to Teladoc’s Q2 results and outlook, sending shares down 8.29% in regular trading to $8.20, with further declines in after-hours trading. The stock is now trading closer to its 52-week low of $6.35 than its high of $15.21, reflecting ongoing concerns about the company’s growth trajectory and profitability challenges.

The market appears particularly concerned about the continued decline in BetterHelp subscribers and the overall revenue contraction, despite the company’s improved cash flow generation and reduced net loss compared to Q1. With guidance suggesting continued revenue and EBITDA declines through the remainder of 2025, Teladoc faces significant challenges in rebuilding investor confidence while navigating the competitive telehealth landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.