LIVE UPDATES: Fed Chair Jerome Powell to deliver major speech at Jackson Hole

Introduction & Market Context

Tenet Healthcare Corporation (NYSE:THC) reported strong first-quarter 2025 results on April 29, exceeding its guidance and demonstrating continued momentum across both its ambulatory and hospital segments. The healthcare provider’s stock was up 2.49% in premarket trading, reaching $127 per share, as investors responded positively to the quarterly performance.

The results mark a significant improvement from the previous quarter, when Tenet missed revenue forecasts despite beating earnings expectations. The company’s focus on operational efficiency and strategic growth initiatives appears to be yielding positive results, with particular strength in its United Surgical Partners International (USPI) ambulatory segment.

Quarterly Performance Highlights

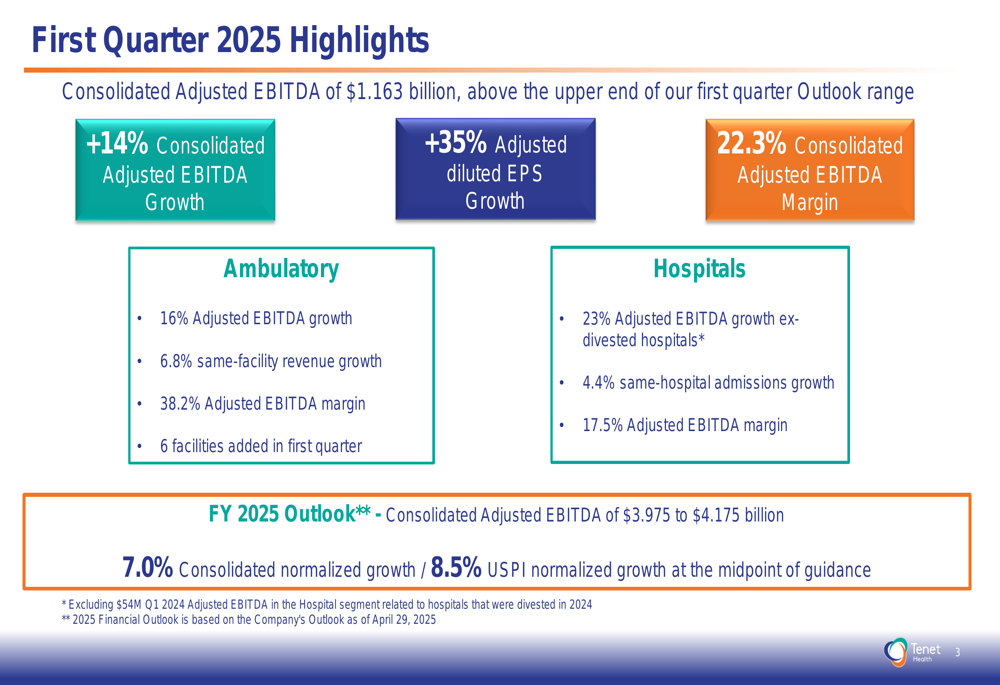

Tenet reported first-quarter 2025 consolidated adjusted EBITDA of $1.163 billion, exceeding the upper end of its outlook range and representing a 14% increase year-over-year. Adjusted diluted earnings per share grew by 35%, while the consolidated adjusted EBITDA margin expanded to 22.3%.

As shown in the following quarterly highlights slide, both key business segments delivered strong results:

The ambulatory segment, operated through USPI, continued its impressive trajectory with 16% adjusted EBITDA growth and a 38.2% adjusted EBITDA margin. Same-facility revenue grew by 6.8%, and the company added six new facilities during the quarter. The hospital segment also performed well, with 23% adjusted EBITDA growth (excluding divested hospitals) and 4.4% growth in same-hospital admissions.

For the full year 2025, Tenet maintained its outlook for consolidated adjusted EBITDA between $3.975 billion and $4.175 billion, representing 7.0% normalized growth at the midpoint. The company expects USPI to deliver 8.5% normalized growth.

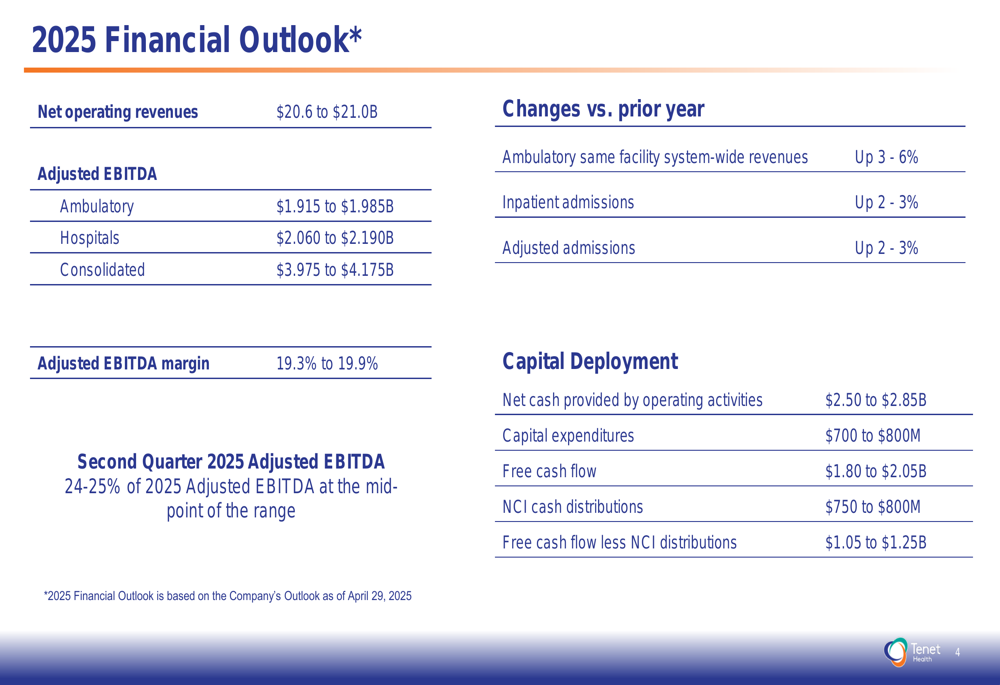

The detailed financial outlook for 2025 provides a comprehensive view of expected performance across key metrics:

USPI Growth Strategy

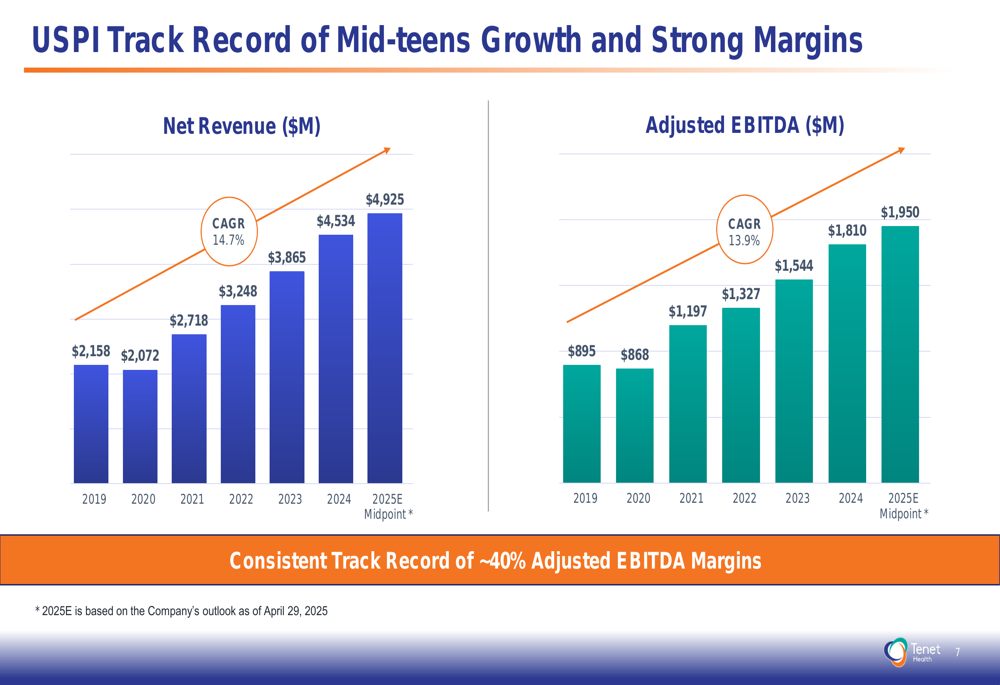

USPI continues to be a significant growth driver for Tenet, with a consistent track record of strong performance. The segment has achieved a 14.7% net revenue CAGR and a 13.9% adjusted EBITDA CAGR from 2019 to 2025 (estimated), while maintaining approximately 40% adjusted EBITDA margins.

The following chart illustrates USPI’s impressive growth trajectory over the past several years:

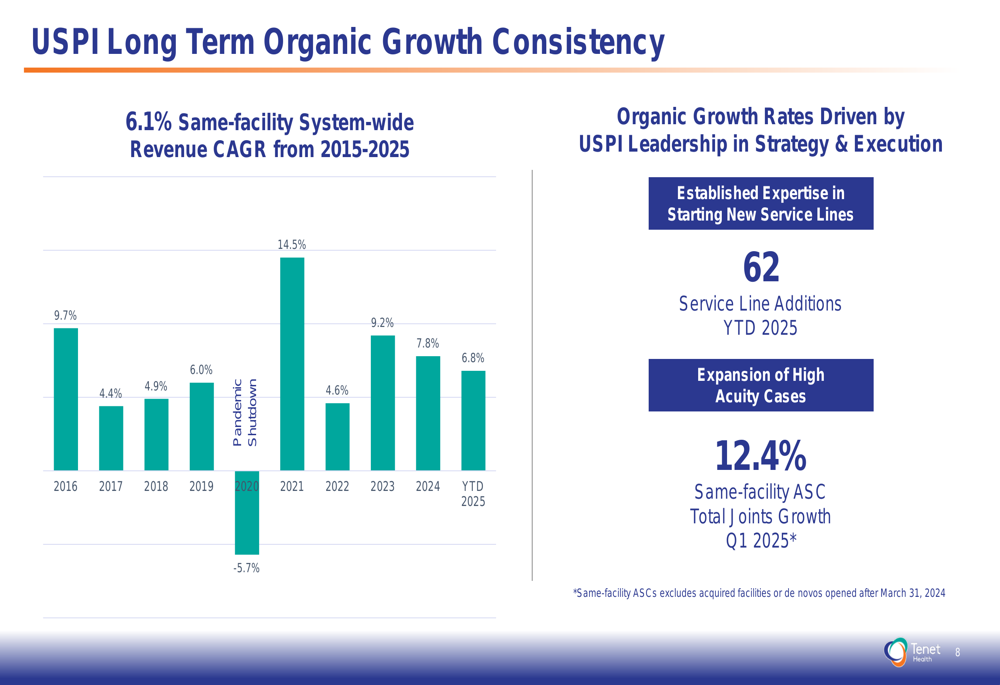

A key strength of USPI has been its consistent organic growth, with same-facility system-wide revenue growth averaging 6.1% annually from 2015 to 2025. This growth is supported by strategic initiatives such as adding new service lines and expanding high-acuity cases. In the first quarter of 2025 alone, USPI added 62 new service lines and achieved 12.4% growth in same-facility ASC total joint procedures.

The following slide demonstrates USPI’s consistent organic growth performance:

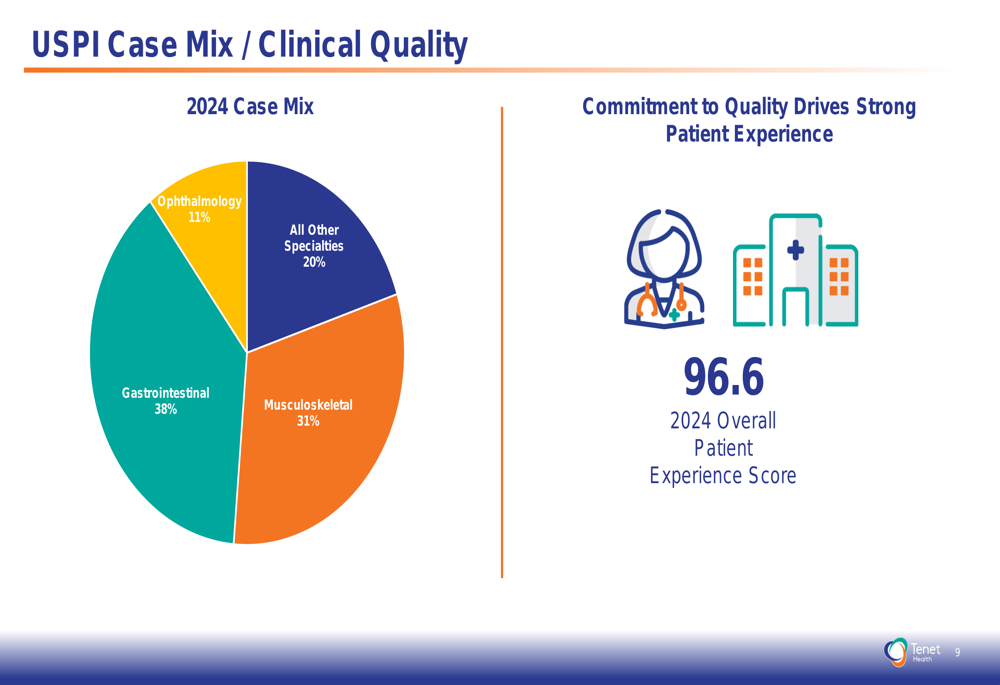

USPI’s case mix is well-diversified across specialties, with gastrointestinal procedures representing 38% of cases, musculoskeletal 31%, ophthalmology 11%, and other specialties 20%. The segment also maintains high clinical quality standards, with a 96.6 overall patient experience score in 2024.

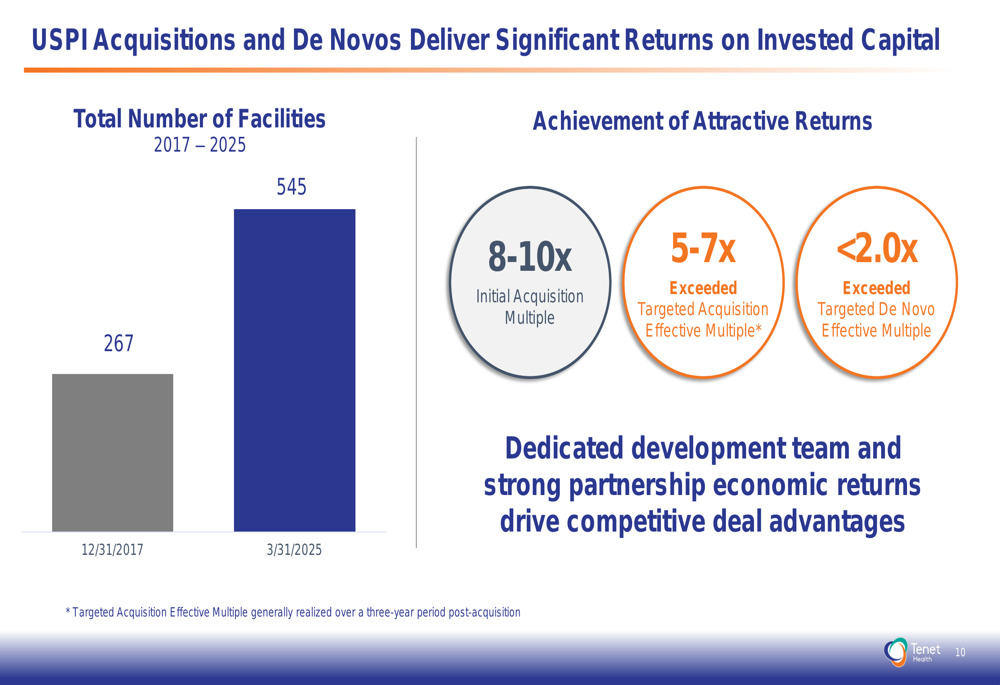

The company has significantly expanded its ambulatory footprint, growing from 267 facilities at the end of 2017 to 545 by March 31, 2025. This expansion has delivered attractive returns, with initial acquisition multiples of 8-10x being reduced to effective multiples of 5-7x, while de novo facilities achieve effective multiples below 2.0x.

Financial Position and Capital Allocation

Tenet has substantially strengthened its financial position, generating $642 million in free cash flow during the first quarter of 2025 ($453 million after non-controlling interests). The company reported $3.0 billion in cash on hand as of March 31, 2025, with an additional $1.5 billion in unused credit line capacity.

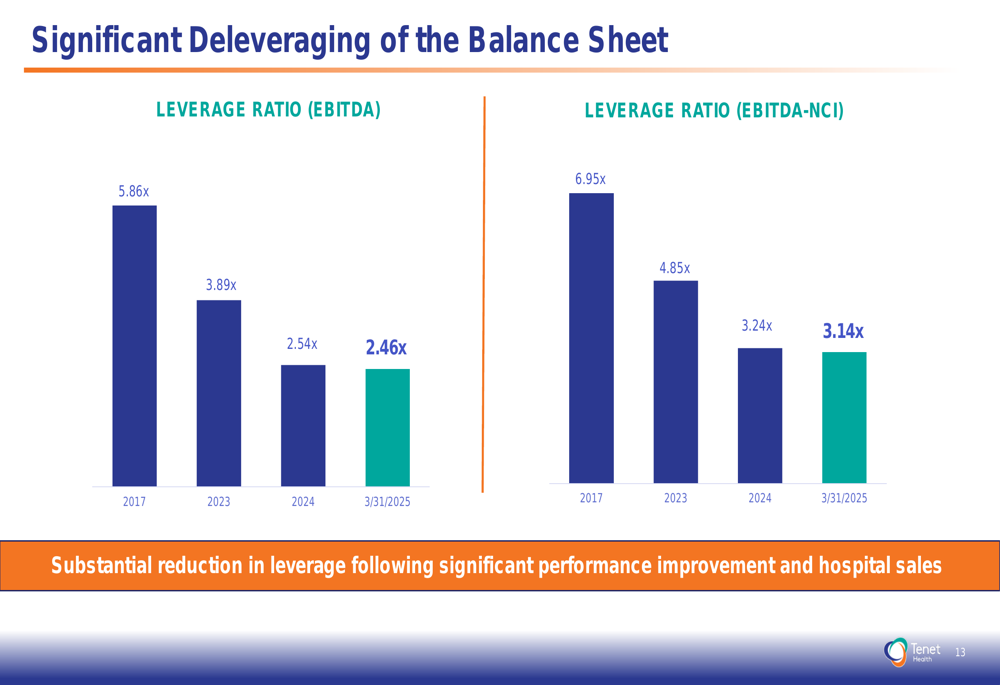

The company has made significant progress in deleveraging its balance sheet, reducing its leverage ratio from 5.86x EBITDA in 2017 to just 2.46x by the end of the first quarter of 2025. This improved financial flexibility positions Tenet well for strategic investments and shareholder returns.

The following chart illustrates Tenet’s deleveraging progress:

Tenet’s capital deployment priorities include continued investment in its ASC platform, with a baseline intention to invest $250 million annually in M&A and de novo facilities. The company also plans to invest in its hospital business, focusing on technology, robotics, and targeted surgical hospital expansion for higher-acuity services.

Forward-Looking Statements

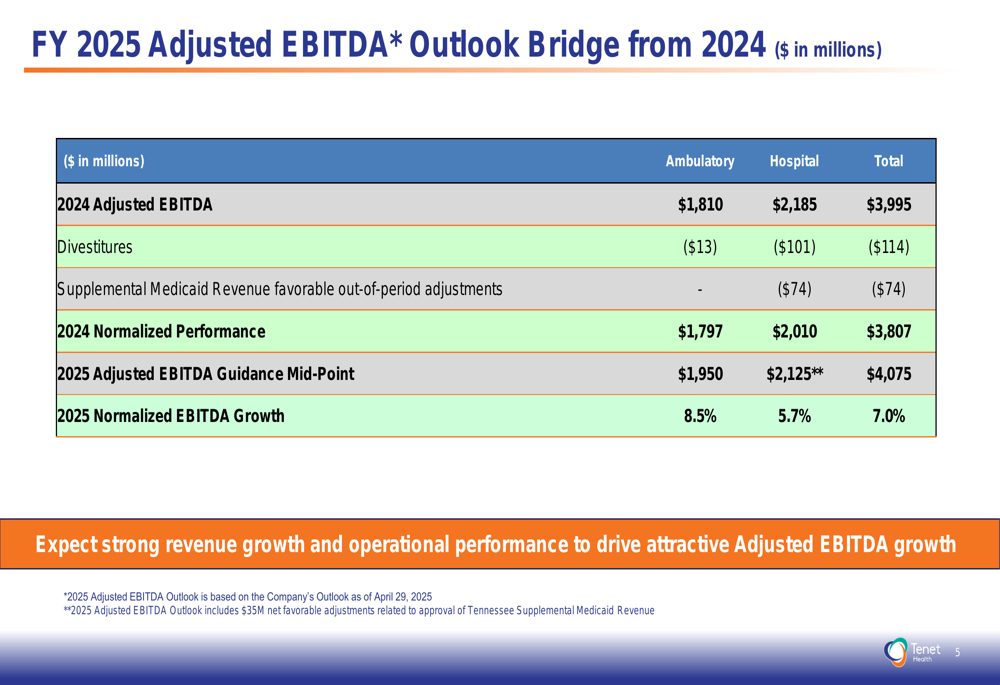

Looking ahead, Tenet provided a detailed bridge from its 2024 performance to its 2025 outlook, accounting for divestitures and one-time items. The company expects normalized EBITDA growth of 7.0% overall, with USPI leading at 8.5% growth and hospitals contributing 5.7% growth.

For the second quarter of 2025, Tenet expects adjusted EBITDA to represent 24-25% of its full-year projection at the midpoint of the range. The company anticipates ambulatory same-facility system-wide revenues to increase by 3-6% for the full year, with inpatient and adjusted admissions both projected to grow by 2-3%.

Tenet’s strong cash flow generation is expected to continue, with projected net cash from operating activities between $2.50 billion and $2.85 billion for 2025, resulting in free cash flow of $1.80 billion to $2.05 billion. After accounting for non-controlling interest distributions, free cash flow is expected to be $1.05 billion to $1.25 billion.

The company’s improved financial position and strong operational performance provide it with significant flexibility for strategic investments while maintaining its commitment to a deleveraged balance sheet and continuing its share repurchase program, which had $1.03 billion remaining in its authorization as of the end of the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.