Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Tenet Healthcare Corporation (NYSE:THC) delivered strong second-quarter 2025 results on July 22, with significant growth across key metrics and a substantial increase to its full-year outlook. The healthcare provider’s stock jumped 4.2% in premarket trading to $181.99, building on momentum from its Q1 performance when shares surged 7.74% following better-than-expected results.

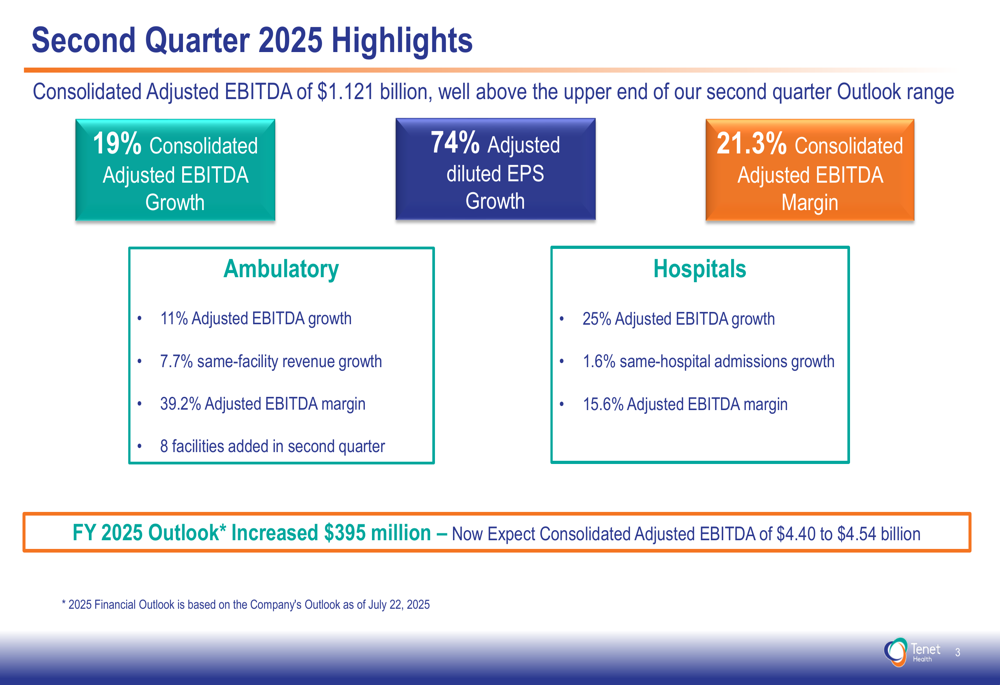

The company’s presentation revealed robust performance across both its hospital and ambulatory care segments, with consolidated adjusted EBITDA reaching $1.121 billion, representing 19% growth year-over-year. This strong performance has enabled Tenet to increase its full-year 2025 adjusted EBITDA guidance by $395 million.

Quarterly Performance Highlights

Tenet’s second quarter results demonstrated substantial improvement across multiple financial metrics. The company achieved 74% growth in adjusted diluted earnings per share, while maintaining a healthy consolidated adjusted EBITDA margin of 21.3%.

The hospital segment showed particularly impressive results with 25% adjusted EBITDA growth and a 15.6% adjusted EBITDA margin. Same-hospital admissions increased by 1.6%, indicating organic growth in Tenet’s core hospital operations.

The ambulatory care segment, operated through United Surgical Partners International (USPI), continued its strong performance with 11% adjusted EBITDA growth and an impressive 39.2% adjusted EBITDA margin. Same-facility revenue growth reached 7.7%, and the company added 8 new facilities during the quarter.

USPI Growth Strategy

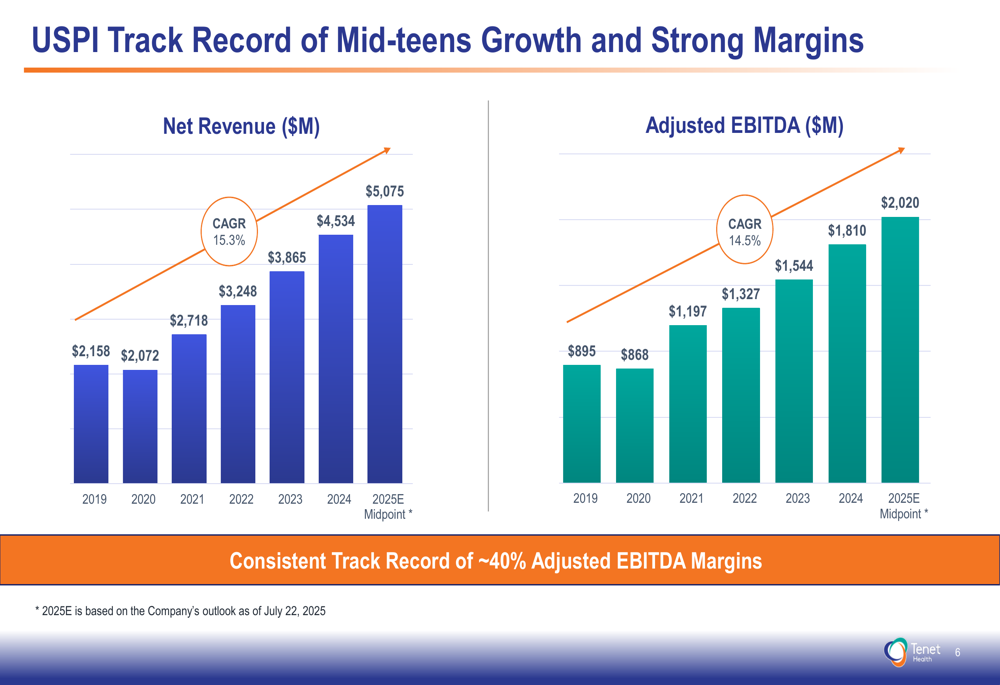

USPI remains a cornerstone of Tenet’s growth strategy, demonstrating consistent long-term performance. The presentation highlighted USPI’s track record of mid-teens growth and consistently strong margins of approximately 40%.

From 2019 to the projected midpoint of 2025, USPI’s net revenue has grown at a compound annual growth rate (CAGR) of 15.3%, increasing from $2.16 billion to an estimated $5.08 billion. Similarly, adjusted EBITDA has grown at a 14.5% CAGR over the same period.

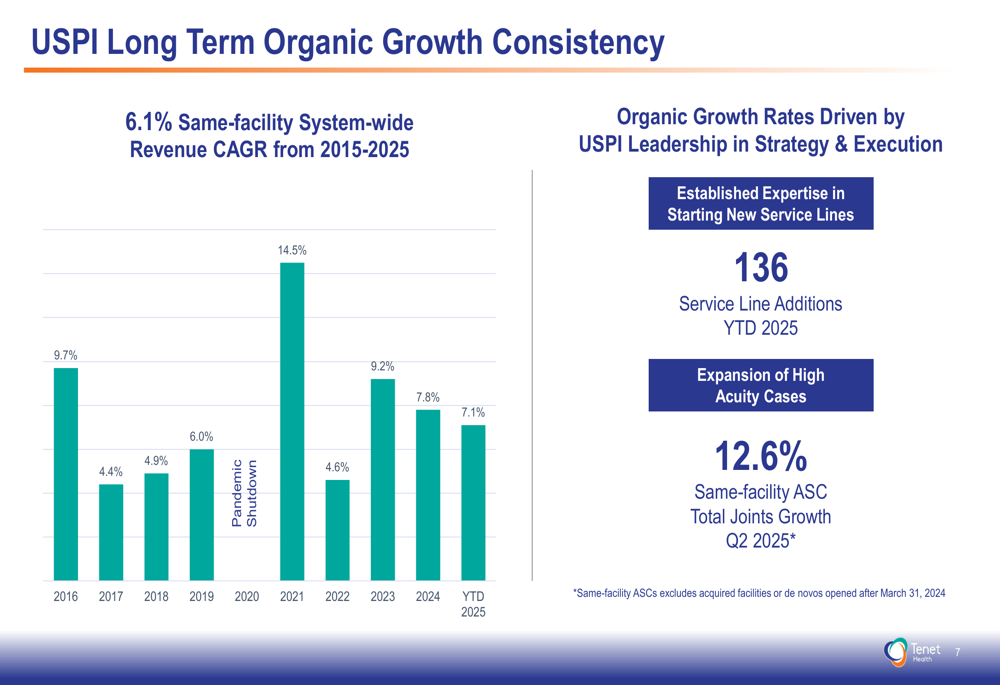

The ambulatory segment has demonstrated remarkable organic growth consistency, with a same-facility system-wide revenue CAGR of 6.1% from 2015 to 2025, despite pandemic-related disruptions in 2020.

USPI’s growth is supported by a diversified case mix, with gastrointestinal procedures representing 38% of cases, musculoskeletal 31%, ophthalmology 11%, and other specialties 20%. The company reported a strong patient experience score of 96.6 in 2024, underscoring its focus on clinical quality.

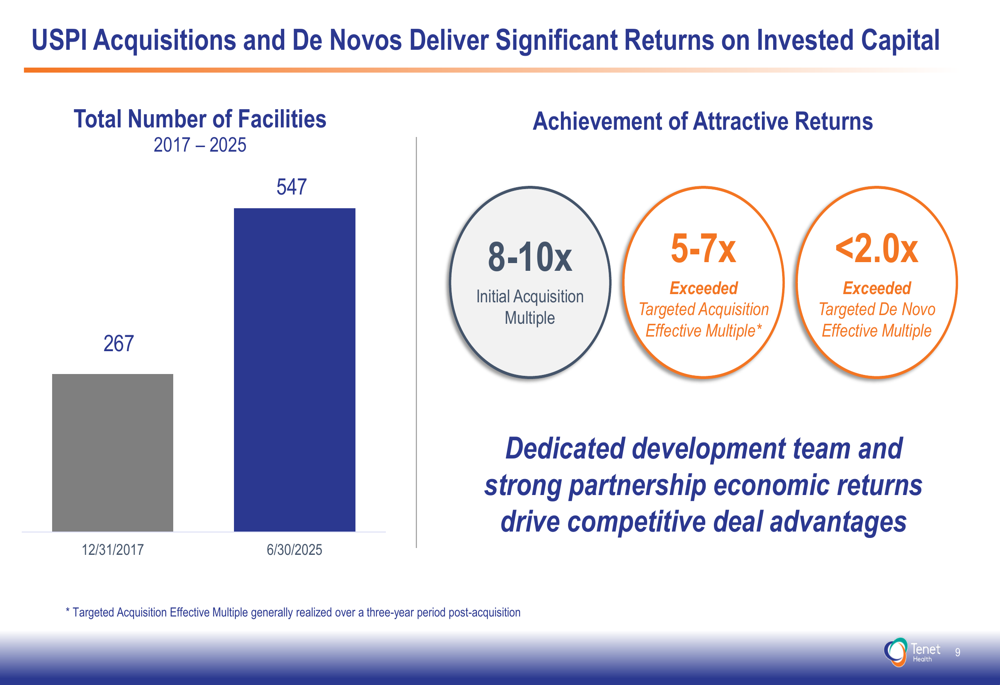

The ambulatory care platform has expanded significantly, growing from 267 facilities at the end of 2017 to 547 as of June 30, 2025. This expansion has been driven by both acquisitions and de novo development, with acquisitions delivering 8-10x initial acquisition multiples.

Financial Position & Capital Allocation

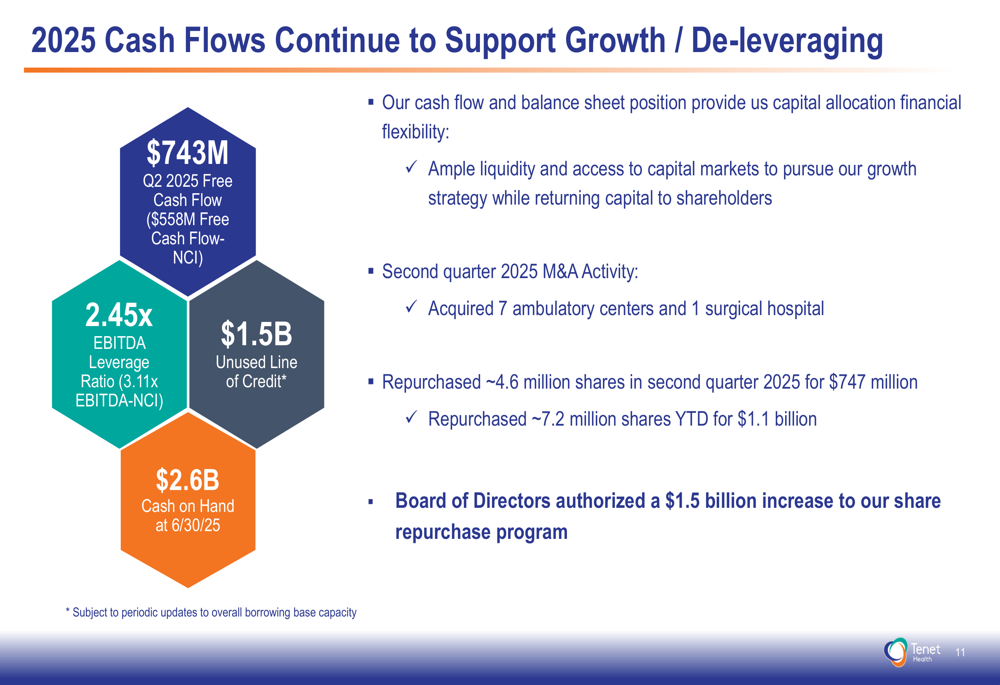

Tenet’s strong operational performance has translated into robust cash flow generation, with second quarter free cash flow of $743 million ($558 million after accounting for noncontrolling interests). This financial strength has enabled the company to pursue multiple capital allocation priorities while maintaining a strong balance sheet.

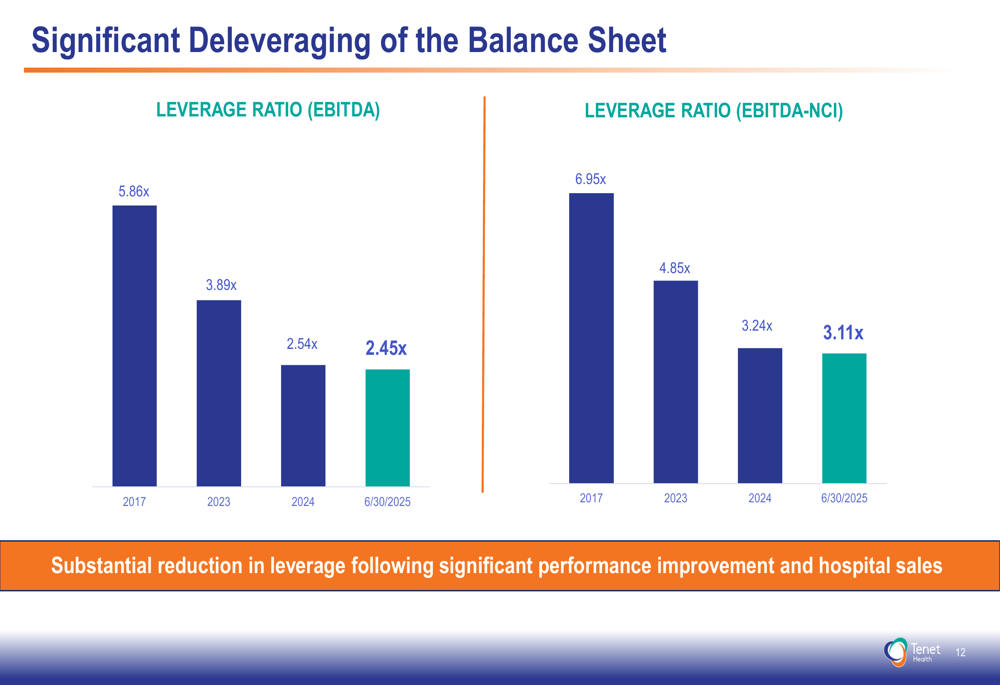

The company has made significant progress in deleveraging, reducing its EBITDA leverage ratio from 5.86x in 2017 to 2.45x as of June 30, 2025. This represents a substantial improvement in financial flexibility and reduced financial risk.

Tenet has been aggressive with share repurchases, buying back approximately 4.6 million shares in the second quarter for $747 million and 7.2 million shares year-to-date for $1.1 billion. The Board of Directors authorized a $1.5 billion increase to the share repurchase program, signaling confidence in the company’s future prospects.

The company outlined its capital deployment priorities, focusing first on investments in the ASC platform through M&A and de novo development, with a baseline intention to invest $250 million per year. Secondary priorities include investments in the hospital business, maintaining a deleveraged balance sheet, and continuing the share repurchase program.

Forward-Looking Statements

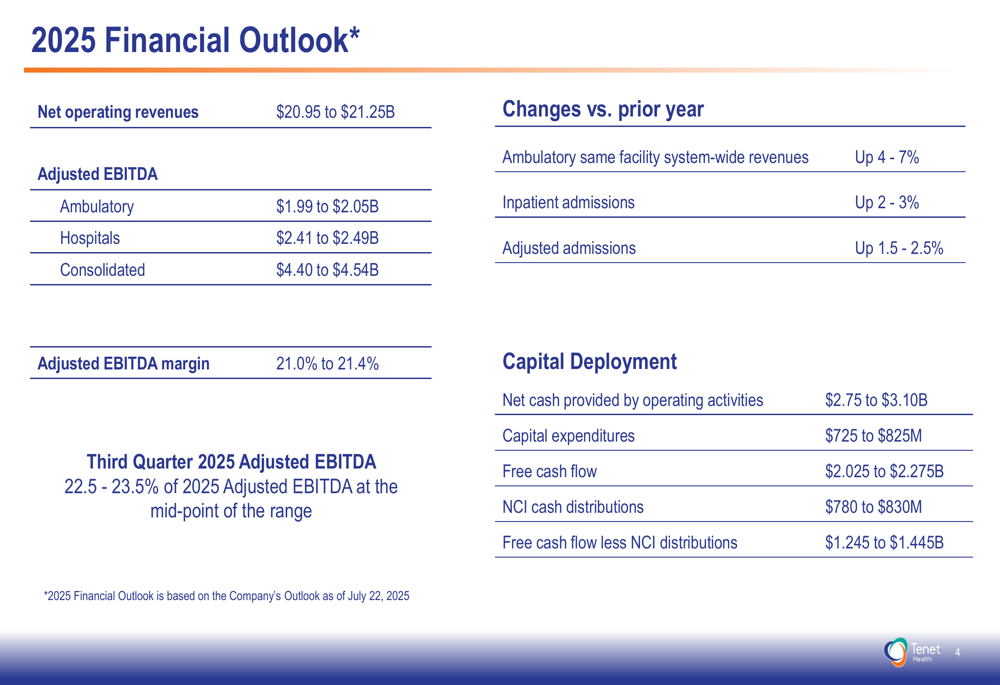

Based on its strong first-half performance, Tenet raised its full-year 2025 outlook. The company now projects net operating revenues of $20.95 to $21.25 billion and consolidated adjusted EBITDA of $4.40 to $4.54 billion, representing a $395 million increase from previous guidance.

For the full year 2025, Tenet expects adjusted diluted earnings per share between $15.55 and $16.21, with free cash flow projected between $2.03 and $2.28 billion. The company anticipates ambulatory same-facility system-wide revenue growth of 4-7% and inpatient admissions growth of 2-3%.

This positive outlook builds on Tenet’s Q1 2025 performance, when the company reported earnings per share of $4.36, significantly exceeding analyst expectations of $3.17. The continued strong performance and raised guidance suggest Tenet’s strategic focus on expanding its ambulatory surgery centers while improving hospital operations is yielding positive results.

With $2.6 billion in cash on hand and an unused line of credit of $1.5 billion as of June 30, 2025, Tenet appears well-positioned to continue executing its growth strategy while returning capital to shareholders through its expanded share repurchase program.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.