Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Tennant Company (NYSE:TNC) presented its second quarter 2025 results on August 7, 2025, revealing a 4.5% organic sales decline but maintaining its full-year guidance despite ongoing macroeconomic challenges. The stock reacted negatively to the results, declining 2.97% to close at $80.13, continuing a challenging year that has seen the stock trade closer to its 52-week low of $67.32 than its high of $98.52.

The Q2 results follow a disappointing first quarter when Tennant missed both EPS and revenue projections, causing a 5.43% stock drop. Despite these consecutive quarterly challenges, management expressed confidence in the company’s trajectory for the remainder of 2025, pointing to strong order growth and momentum in its autonomous cleaning solutions.

Quarterly Performance Highlights

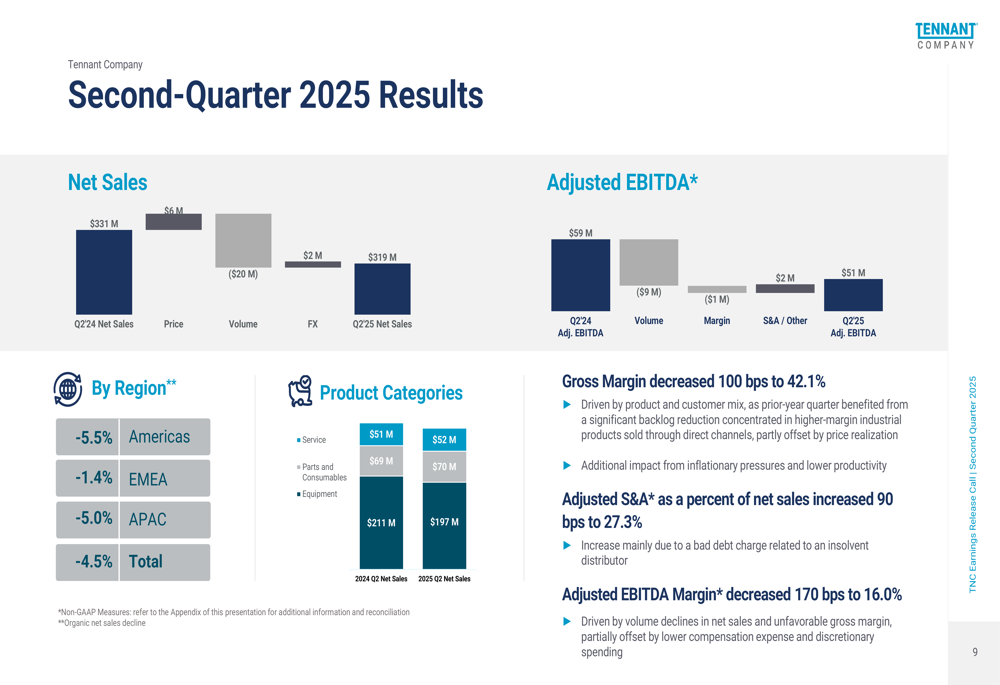

Tennant reported Q2 2025 net sales of $318.6 million, representing a 4.5% organic decline compared to the same period last year. Adjusted EBITDA came in at $51.0 million with a 16.0% margin, while adjusted diluted EPS reached $1.49 per share, down from $1.83 in Q2 2024.

As shown in the following financial performance summary:

The company attributed much of the year-over-year decline to lapping a significant backlog-reduction benefit from the prior year, which had contributed approximately $26 million to Q2 2024 results. Net income for the quarter was $20.2 million, compared to $27.9 million in the prior year period, with the effective tax rate increasing to 26.0% from 24.4% due to a prior-year discrete tax benefit that did not recur.

A more detailed breakdown of the quarterly results shows pressure across all regions:

Gross margin decreased 100 basis points to 42.1%, while adjusted S&A as a percentage of net sales increased 90 basis points to 27.3%. These factors contributed to a 170 basis point decrease in adjusted EBITDA margin to 16.0%. By region, organic sales declined across all geographies: Americas (-5.5%), EMEA (-1.4%), and APAC (-5.0%).

Strategic Initiatives

Despite the challenging quarter, Tennant highlighted several strategic initiatives aimed at driving future growth. The company’s enterprise growth strategy update showcased progress in pricing excellence, product innovation, and autonomous mobile robot (AMR) adoption:

A key bright spot in the results was the continued momentum in orders, which grew 4% during the second quarter and 8% year-to-date, with a book-to-bill ratio above 1.0. This suggests potential revenue improvement in coming quarters.

The company also emphasized its expanding AMR portfolio, which now accounts for 6% of net sales, up from previous quarters. Tennant has delivered over 10,000 AMR units to more than 1,000 customers, positioning the company as a leader in autonomous cleaning solutions.

Product innovation remained a focus, with the successful launch of the X6 ROVR mid-sized robotic scrubber early in the quarter and the introduction of the Z50 Citadel Outdoor Sweeper in late Q2. The Z50 Citadel targets industrial sites such as mining, manufacturing, logistics, and municipal settings:

Detailed Financial Analysis

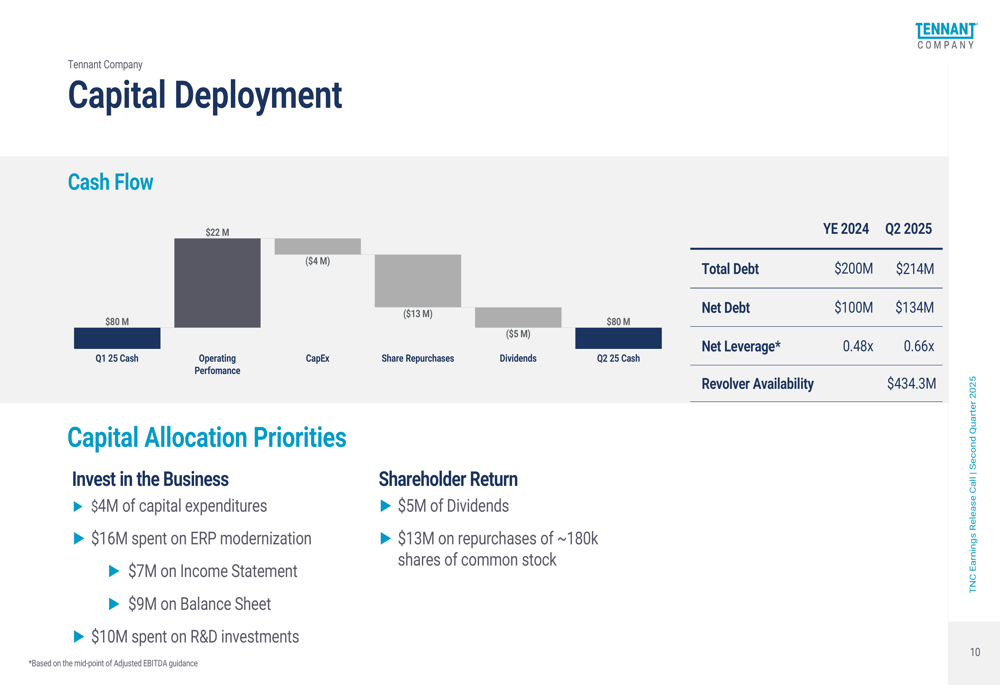

Tennant’s capital deployment strategy balanced investments in the business with shareholder returns during the quarter. The company spent $4 million on capital expenditures and $16 million on ERP modernization, while returning $18 million to shareholders through dividends ($5 million) and share repurchases ($13 million for approximately 180,000 shares).

The following chart illustrates the company’s capital deployment for the quarter:

The company’s balance sheet showed a slight increase in leverage, with net debt rising to $134 million from $100 million at year-end 2024, resulting in a net leverage ratio of 0.66x compared to 0.48x. Revolver availability remained strong at $434.3 million, providing ample financial flexibility.

Forward-Looking Statements

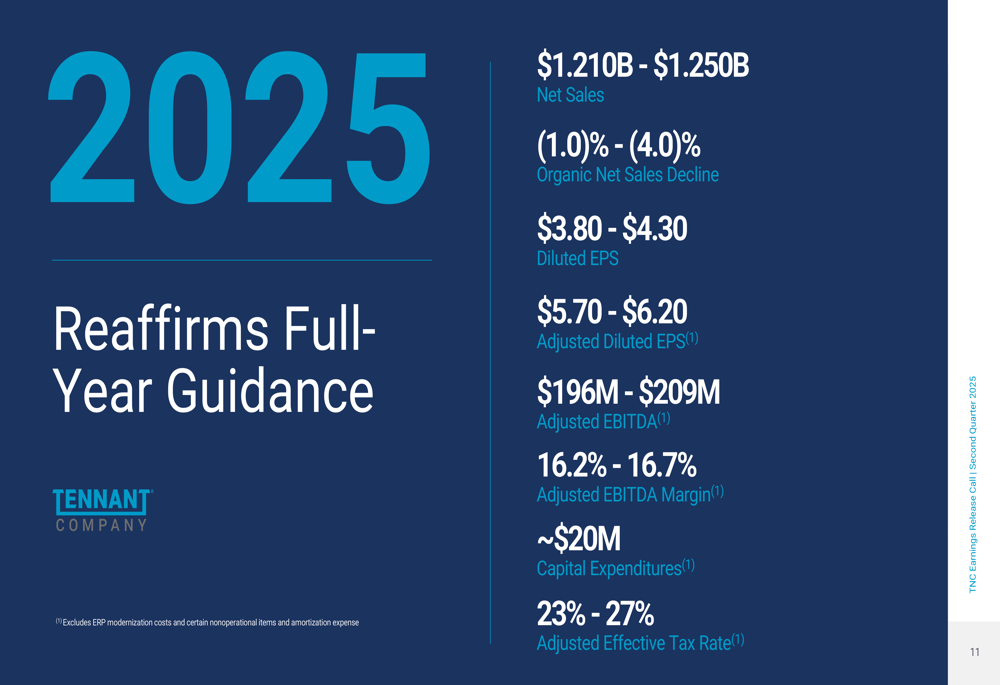

Despite the challenging Q2 results, Tennant reaffirmed its full-year 2025 guidance:

The company expects an organic net sales decline of 1.0% to 4.0% for the full year, while projecting order growth rates of 3.5% to 7.0%. Adjusted EBITDA margin expansion is anticipated to be 0 to 50 basis points.

Management addressed the impact of tariffs, noting limited effect on first-half results and expressing confidence that mitigation strategies including pricing and supply-chain actions would effectively offset full-year tariff-related cost inflation.

"Second-quarter performance reinforces our confidence in full-year trajectory," the company stated in its presentation, maintaining its outlook despite external headwinds. This stance contrasts with the consecutive quarterly declines and suggests management believes the company has weathered the worst of its challenges.

Executive Summary

Tennant’s Q2 2025 results present a mixed picture for investors. While financial metrics showed year-over-year declines, positive indicators such as strong order growth, increasing AMR adoption, and new product launches provide some optimism for future performance. The company’s decision to maintain full-year guidance despite two challenging quarters reflects management’s confidence in its strategic direction and ability to execute through the remainder of 2025.

The market’s negative reaction to the results suggests investors may require more concrete evidence of a turnaround before regaining confidence. With the stock trading significantly below its 52-week high, upcoming quarters will be crucial for Tennant to demonstrate that its strategic initiatives can translate into improved financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.