U.S. stock futures slip lower on waning rate cut bets; Applied Materials falls

Introduction & Market Context

Teradata Corporation (NYSE:TDC) released its Q1 2025 earnings results on May 6, 2025, revealing a mixed financial picture characterized by strong cloud growth but overall revenue decline. The company’s stock fell 4.33% in after-hours trading to $21.00, reflecting investor concerns about the revenue miss despite an earnings beat. Teradata continues to position itself as a leader in cloud database management and AI solutions, emphasizing its transformation toward a cloud-focused business model.

Quarterly Performance Highlights

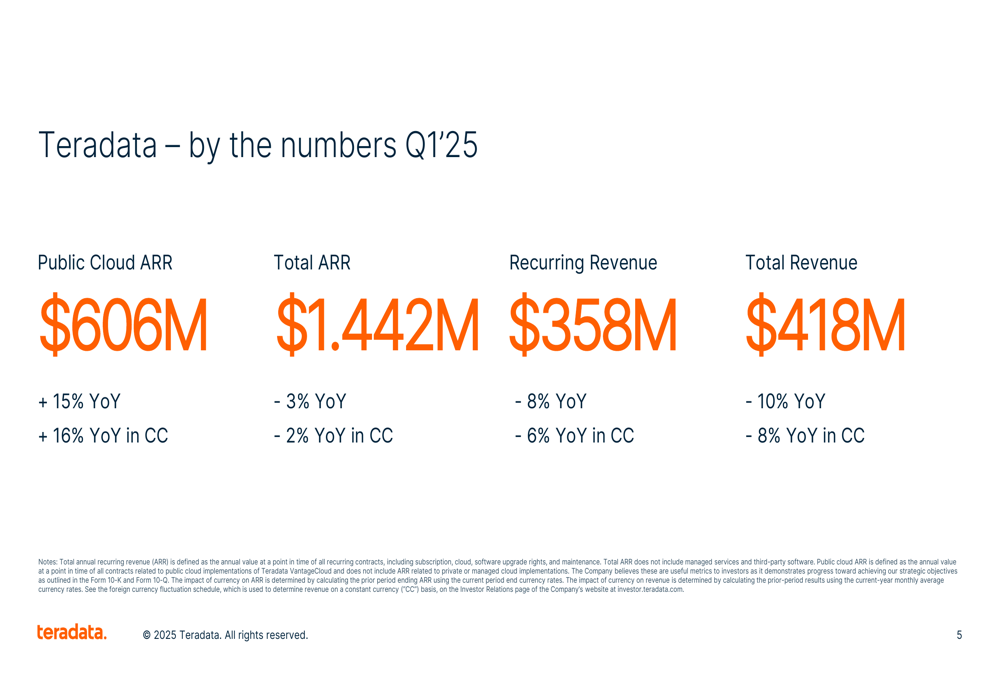

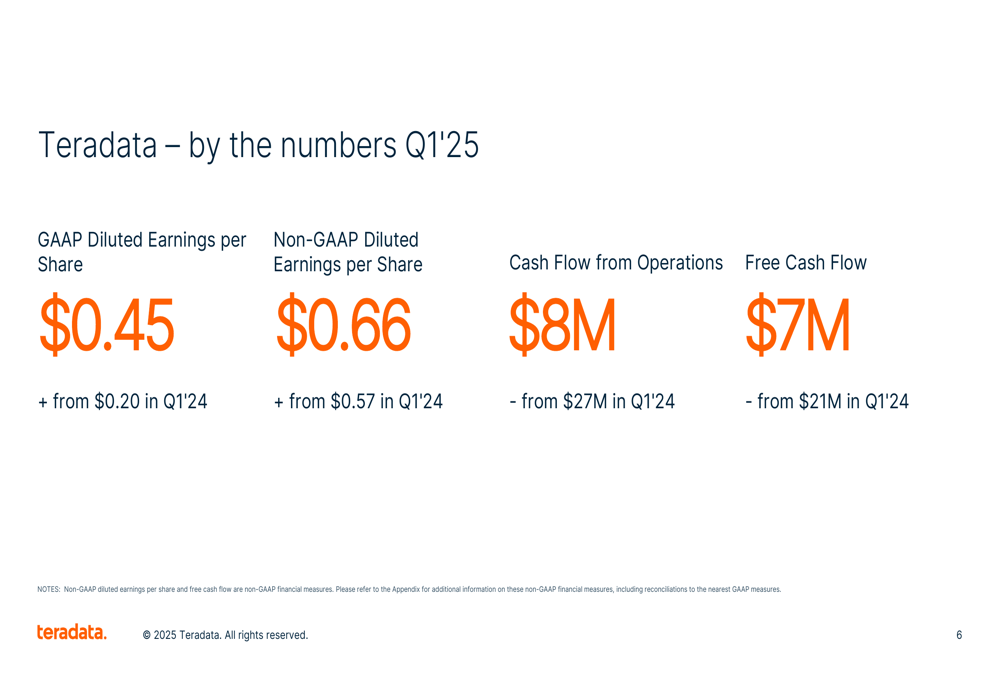

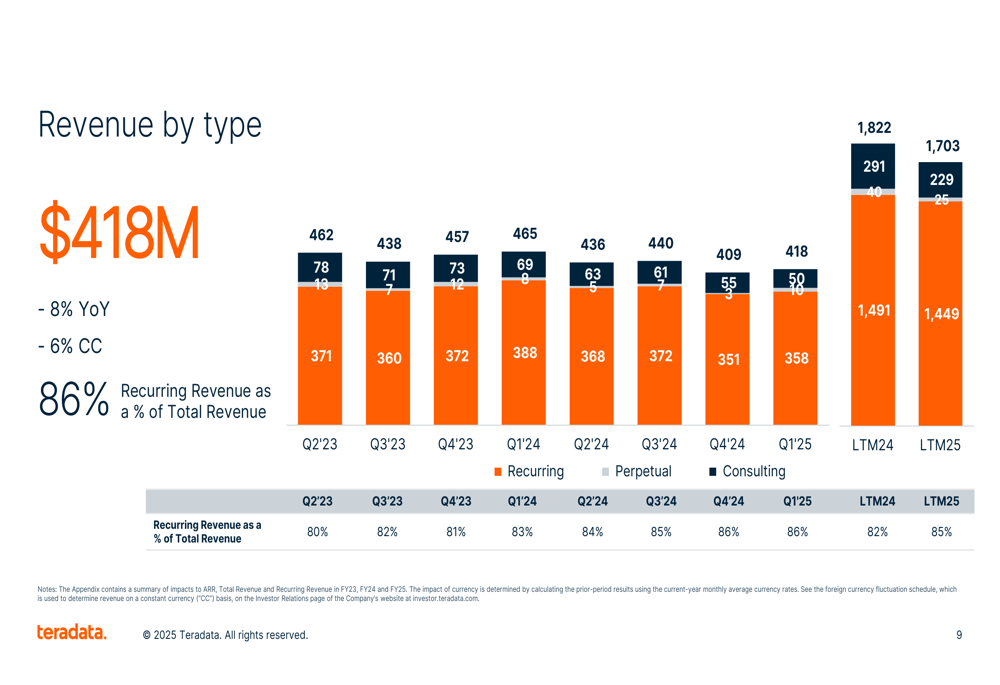

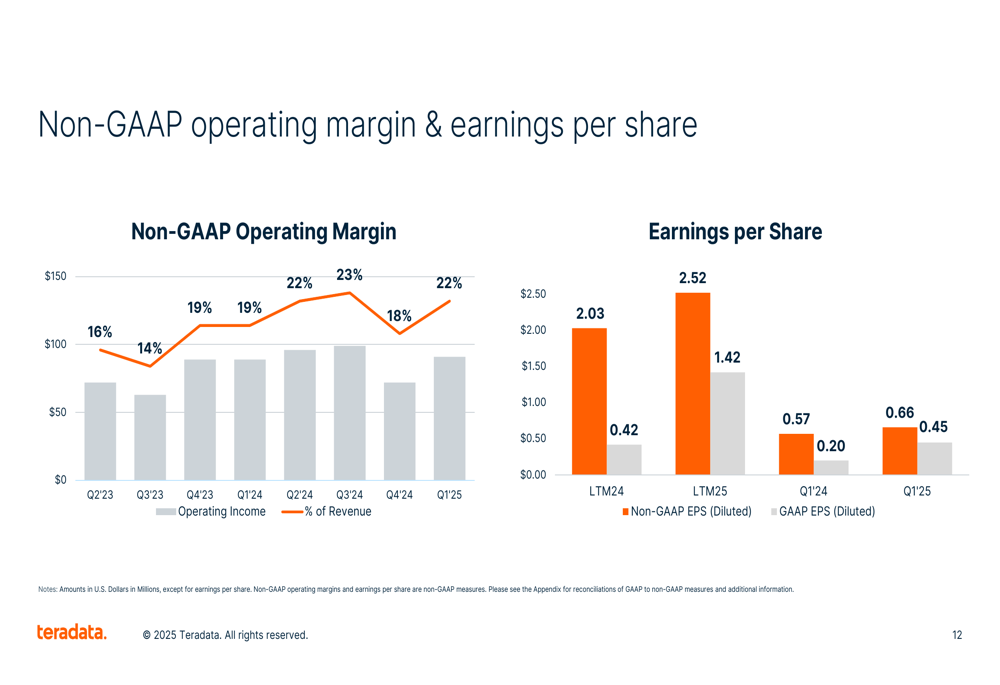

Teradata reported Q1 2025 total revenue of $418 million, representing a 10% year-over-year decline (8% in constant currency), falling short of analyst expectations of $425.42 million. Despite the revenue challenges, the company delivered strong earnings performance with non-GAAP diluted earnings per share of $0.66, up 15% year-over-year and exceeding forecasts of $0.57.

As shown in the following summary of key financial metrics:

The company’s recurring revenue, which now comprises 86% of total revenue, declined 8% year-over-year to $358 million. This shift toward a subscription-based model continues to be a strategic focus, though the overall revenue decline suggests challenges in the transition period.

Earnings metrics showed more positive momentum, with GAAP diluted EPS more than doubling from $0.20 in Q1 2024 to $0.45 in Q1 2025, while non-GAAP operating margin improved by 270 basis points year-over-year to 21.8%.

Cloud Transformation Progress

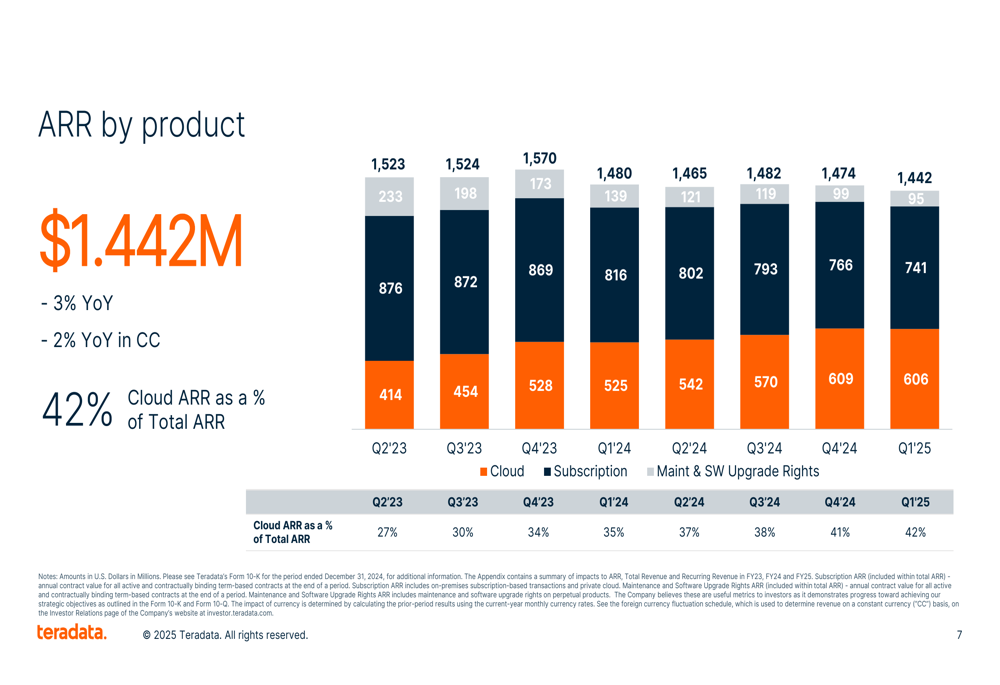

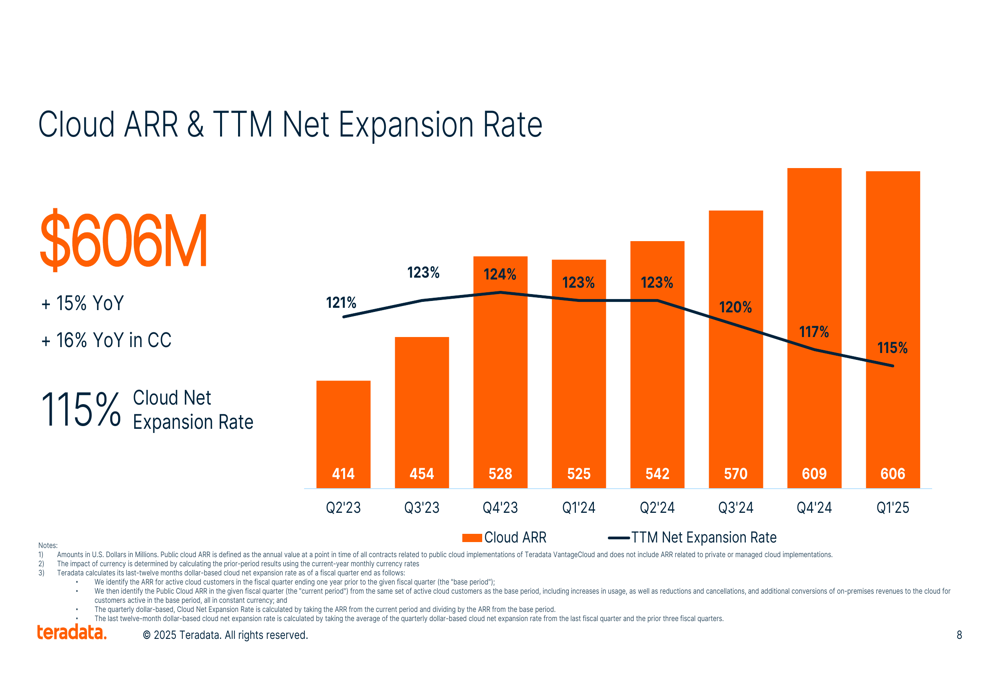

The highlight of Teradata’s Q1 results was the continued strong performance in cloud offerings. Public Cloud Annual Recurring Revenue (ARR) grew 16% year-over-year in constant currency to $606 million, now representing 42% of total ARR compared to 35% a year ago. This growth underscores the company’s successful pivot toward cloud-based solutions.

The following chart illustrates the ongoing shift in Teradata’s revenue mix from traditional on-premises solutions toward cloud offerings:

While cloud ARR continues to grow impressively, the company’s trailing twelve-month net expansion rate of 115% indicates healthy customer spending growth, though this metric has been gradually declining from 123% a year ago. This trend suggests potential challenges in upselling existing cloud customers at the same pace as in previous periods.

Detailed Financial Analysis

Teradata’s revenue composition continues to shift toward recurring revenue streams, which now account for 86% of total revenue compared to 83% a year ago. This transition aligns with the company’s strategic focus on building a more predictable business model, though the overall revenue decline indicates challenges during this transformation.

The following chart shows the evolution of Teradata’s revenue mix over time:

On the profitability front, Teradata has made significant progress in improving operational efficiency. Non-GAAP operating margin reached 21.8% in Q1 2025, up from 19.1% in the same period last year, reflecting effective cost management and operational improvements.

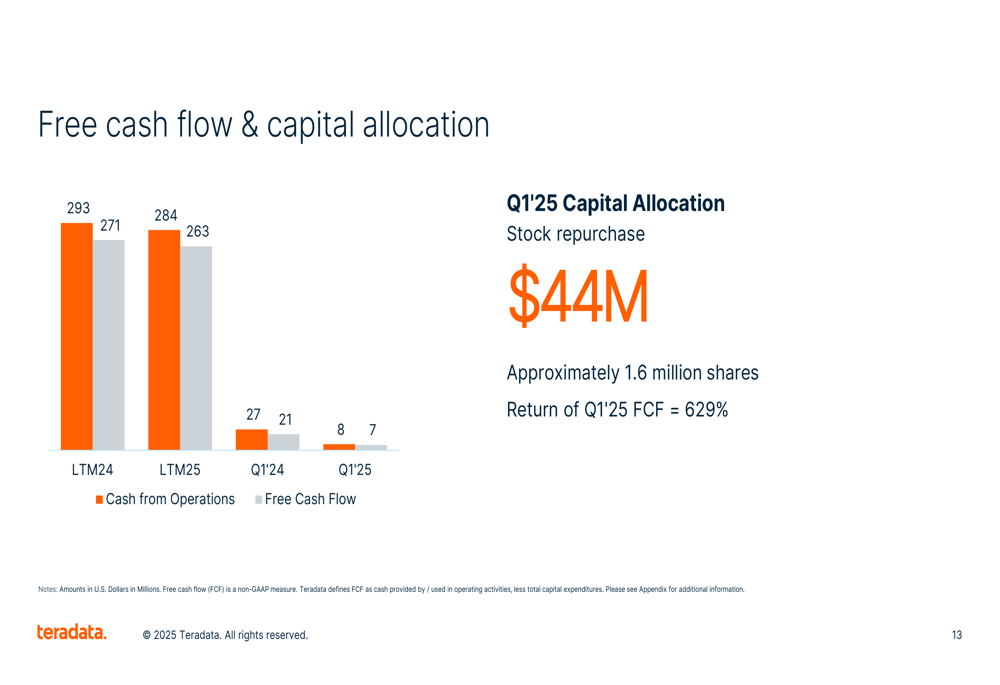

However, cash flow metrics showed weakness compared to the prior year. Cash flow from operations declined to $8 million from $27 million in Q1 2024, while free cash flow fell to $7 million from $21 million. Despite the lower cash generation, Teradata maintained its commitment to shareholder returns, repurchasing $44 million in stock during the quarter, representing 629% of the quarter’s free cash flow.

Forward-Looking Statements

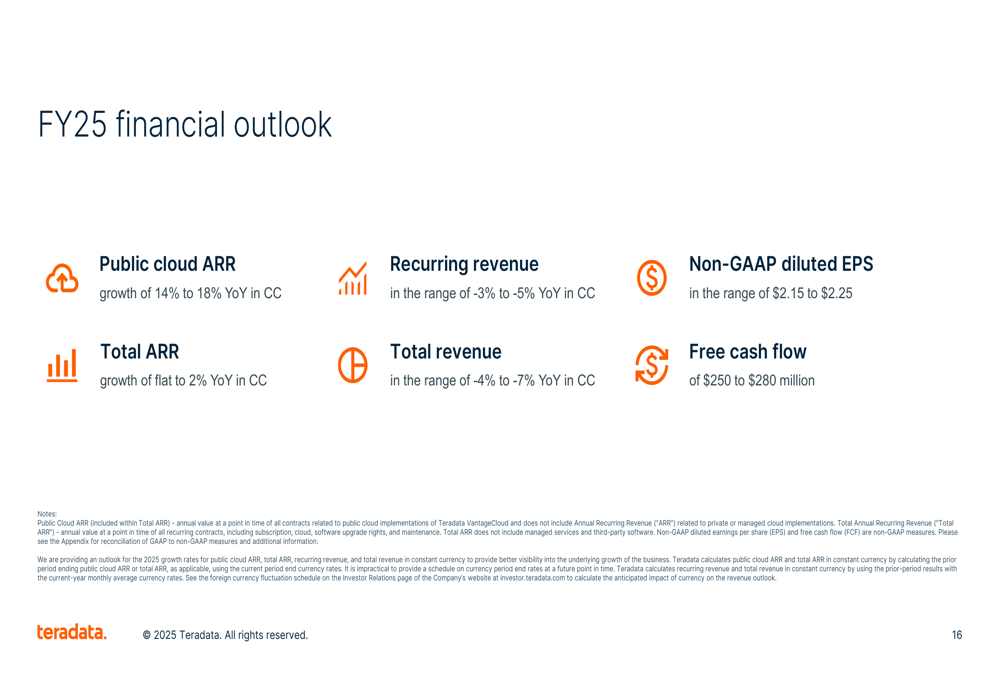

Looking ahead, Teradata provided guidance for both Q2 2025 and the full fiscal year. For Q2, the company expects recurring revenue to decline 5-7% year-over-year in constant currency and total revenue to decline 7-9%, with non-GAAP diluted EPS projected between $0.37 and $0.41.

For the full fiscal year 2025, Teradata forecasts:

The guidance reflects continued strong growth in cloud ARR (14-18% year-over-year) but acknowledges ongoing revenue challenges as the company transitions its business model. Management expects total ARR to return to growth (flat to 2% year-over-year) by the end of 2025, suggesting the transformation is progressing but still requires time to fully materialize in top-line results.

Competitive Industry Position

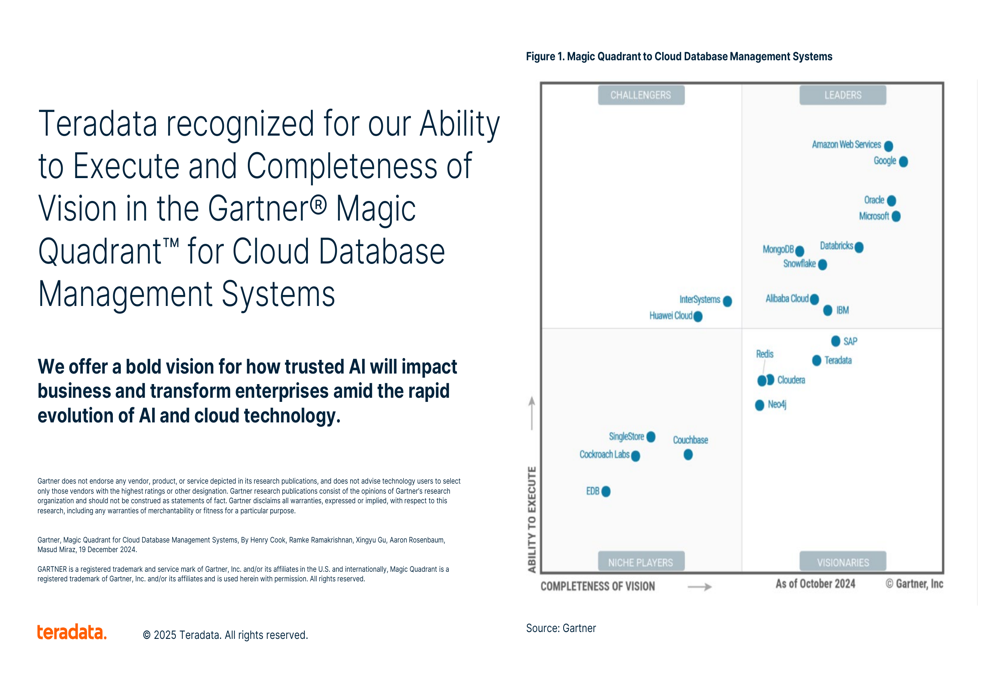

Teradata continues to strengthen its position in the competitive cloud database and AI landscape, receiving recognition from multiple industry analysts. The company was named a Leader in Gartner (NYSE:IT)’s Magic Quadrant for Cloud Database Management Systems, highlighting its strong ability to execute and completeness of vision.

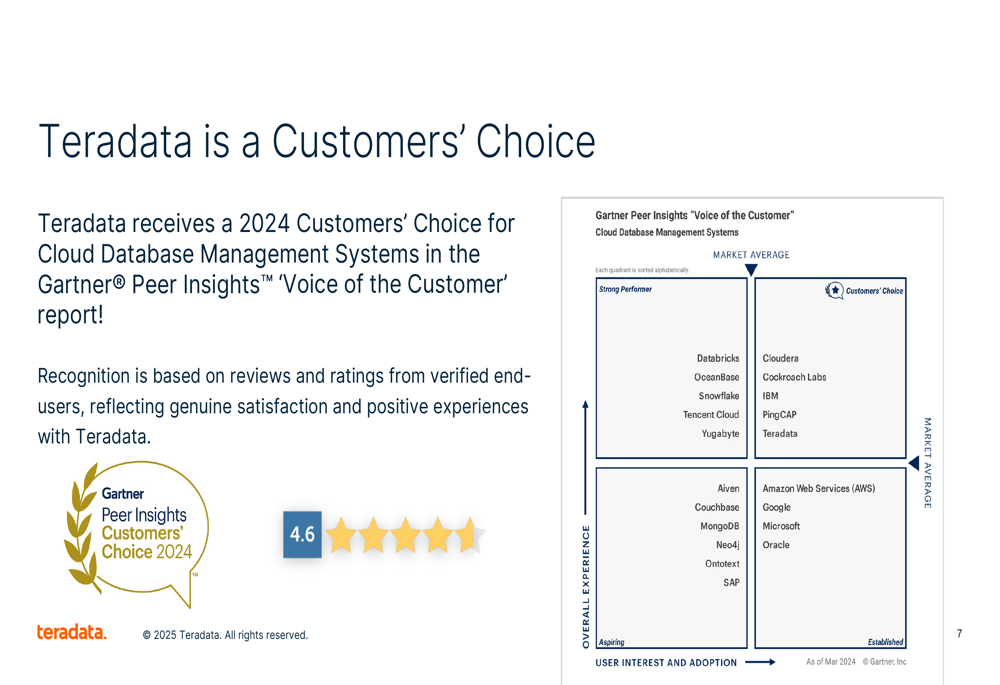

Additionally, Teradata received recognition as a 2024 Customers’ Choice in Gartner Peer Insights’ "Voice of the Customer" report, reflecting positive feedback from actual users of its solutions.

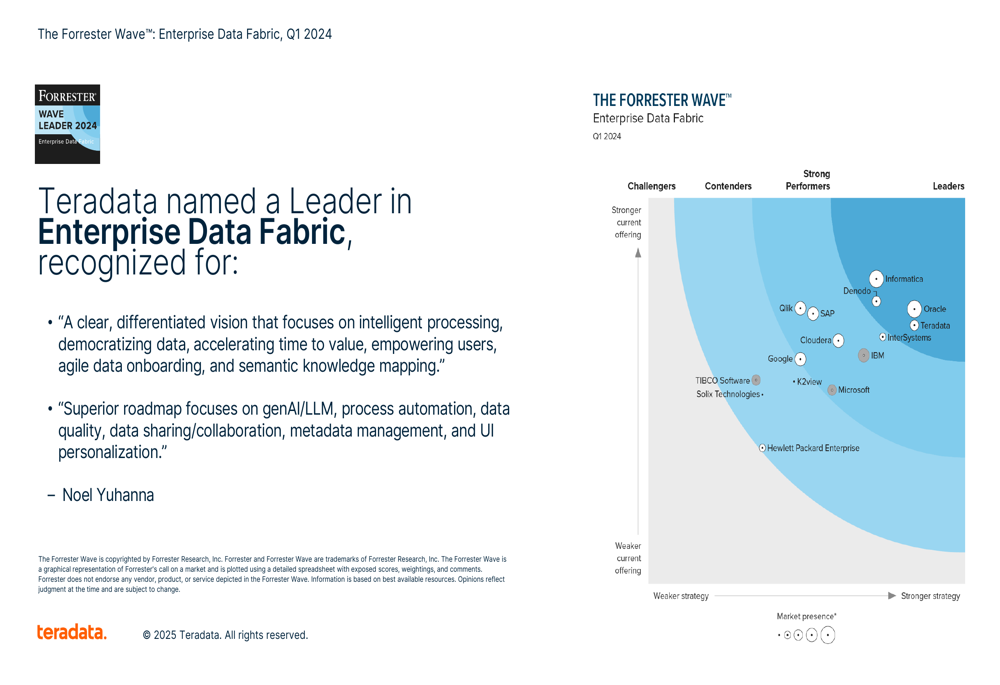

The company was also named a Leader in Enterprise Data Fabric by Forrester, with the analyst firm highlighting Teradata’s "clear, differentiated vision" and "superior roadmap" focused on generative AI, process automation, and data management capabilities.

Beyond product capabilities, Teradata emphasized its commitment to environmental, social, and governance (ESG) initiatives, showcasing various recognitions and affiliations that underscore its focus on sustainable and responsible business practices.

Executive Commentary

During the earnings call, Teradata’s CEO emphasized the critical role of trusted data in AI success, stating, "Trusted data is critical to success with AI." This messaging aligns with the company’s positioning as a provider of trusted data solutions for AI applications, a strategic focus that management believes will drive future growth as organizations increasingly adopt AI technologies.

The company’s Chief Product Officer reinforced this message, noting that "There is no trusted AI without trusted data," highlighting Teradata’s commitment to data integrity as a key differentiator in the competitive landscape.

As Teradata continues its transformation toward a cloud-centric business model, investors will be closely watching whether the company can accelerate its cloud ARR growth while stabilizing overall revenue performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.