Conservative commentator Charlie Kirk shot and killed at Utah event

Introduction & Market Context

TeraWulf Inc (NASDAQ:WULF) presented its first quarter 2025 results on May 9, highlighting a strategic pivot toward high-performance computing (HPC) hosting while navigating challenges in its Bitcoin mining operations. The company’s stock closed at $3.30 on May 8, up 8.2% for the day, but remains down significantly year-to-date, reflecting ongoing market skepticism about its business transformation.

The presentation revealed a company at a strategic inflection point, with declining Bitcoin mining profitability despite increased hash rate capacity, while simultaneously securing its first major HPC hosting client. This dual-track approach comes as TeraWulf attempts to leverage its existing infrastructure advantages in a competitive market.

Quarterly Performance Highlights

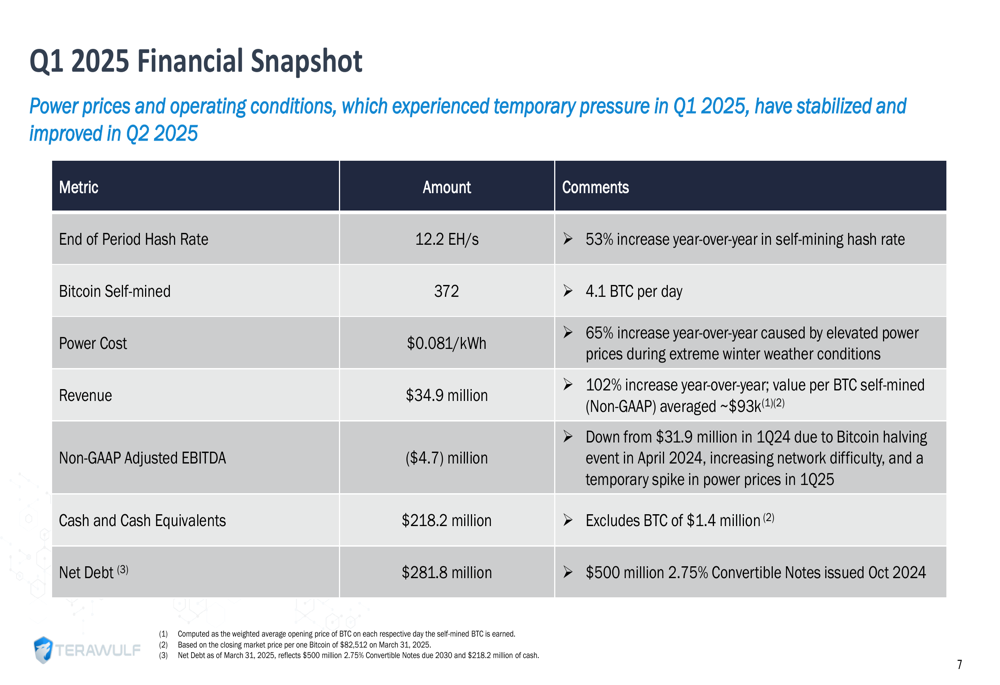

TeraWulf reported mixed results for Q1 2025, with strong year-over-year revenue growth but declining sequential profitability. The company achieved a hash rate of 12.2 EH/s, representing a 53% increase year-over-year, while mining 372 Bitcoin during the quarter (approximately 4.1 BTC per day).

Revenue reached $34.9 million, a 102% increase compared to Q1 2024. However, profitability metrics showed concerning trends, with Non-GAAP Adjusted EBITDA falling to -$4.7 million, down significantly from $31.9 million in Q1 2024. This decline was largely attributed to a 65% year-over-year increase in power costs, which rose to $0.081/kWh.

As shown in the following financial snapshot from the company’s presentation:

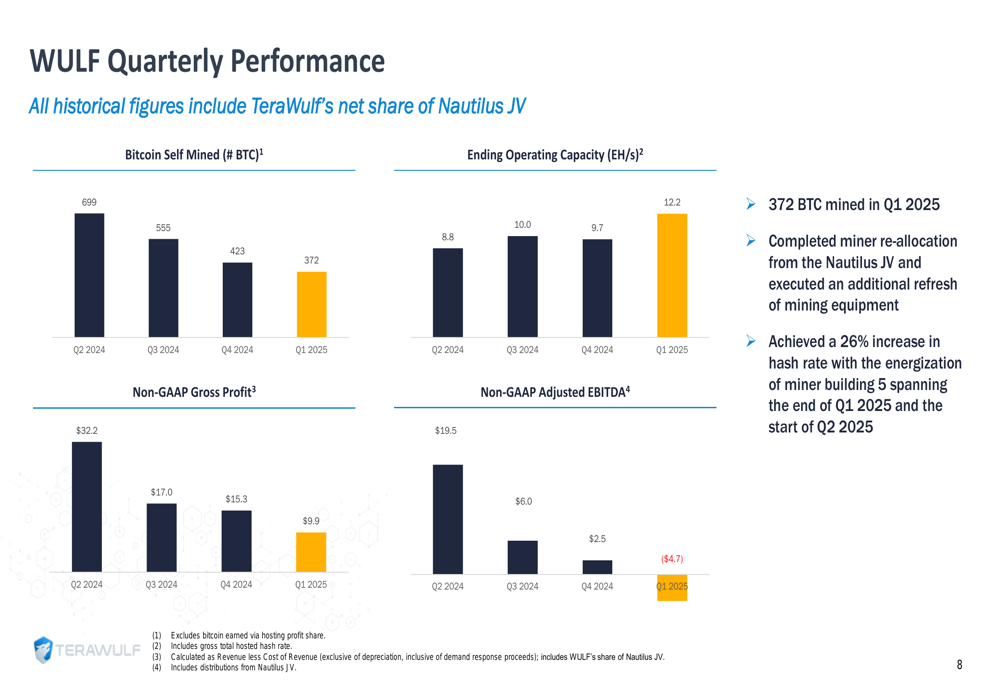

The quarterly performance trends further illustrate the challenges facing TeraWulf’s mining operations, with sequential declines in Bitcoin production despite increasing hash rate capacity. This divergence highlights the impact of network difficulty increases and rising operational costs.

As shown in the following chart of quarterly performance metrics:

Strategic Initiatives

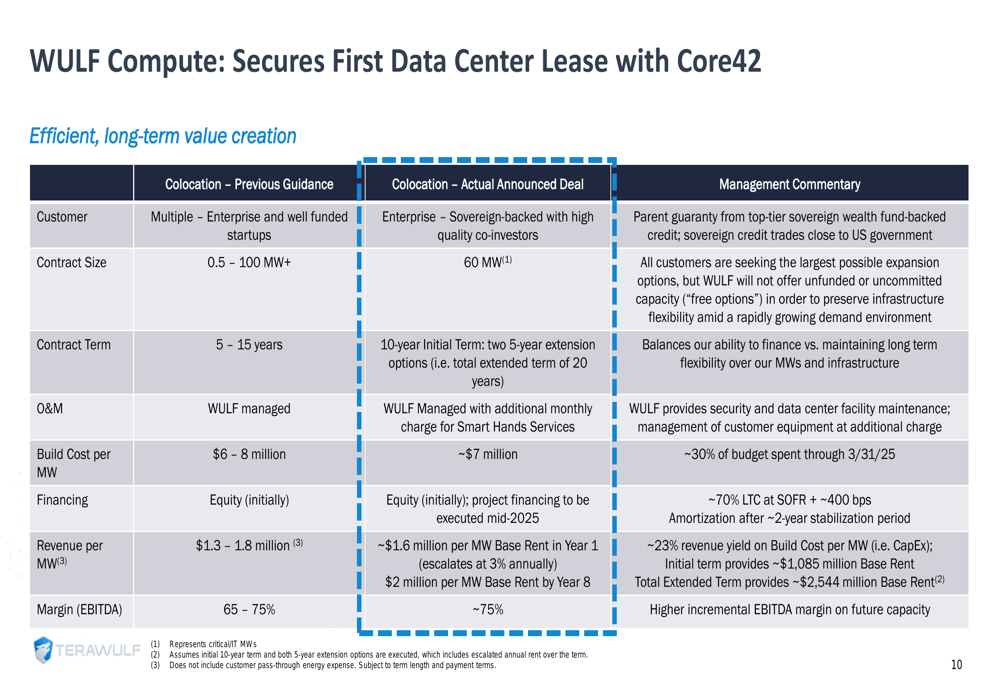

The centerpiece of TeraWulf’s strategic pivot is its recently announced agreement with Core42, a UAE-based AI cloud and managed services provider backed by G42, whose investors include Microsoft (NASDAQ:MSFT), Silver Lake, and Mubadala Investment Company. This deal represents TeraWulf’s first major HPC hosting client and signals the company’s shift toward diversifying beyond Bitcoin mining.

The Core42 agreement includes a 60 MW contract with a 10-year initial term and two 5-year extension options. The deal is expected to generate approximately $1.6 million per MW in base rent during the first year, escalating at 3% annually to reach $2 million per MW by year eight, with EBITDA margins of approximately 75%.

The details of this landmark agreement are illustrated in the following comparison between previous guidance and the actual deal terms:

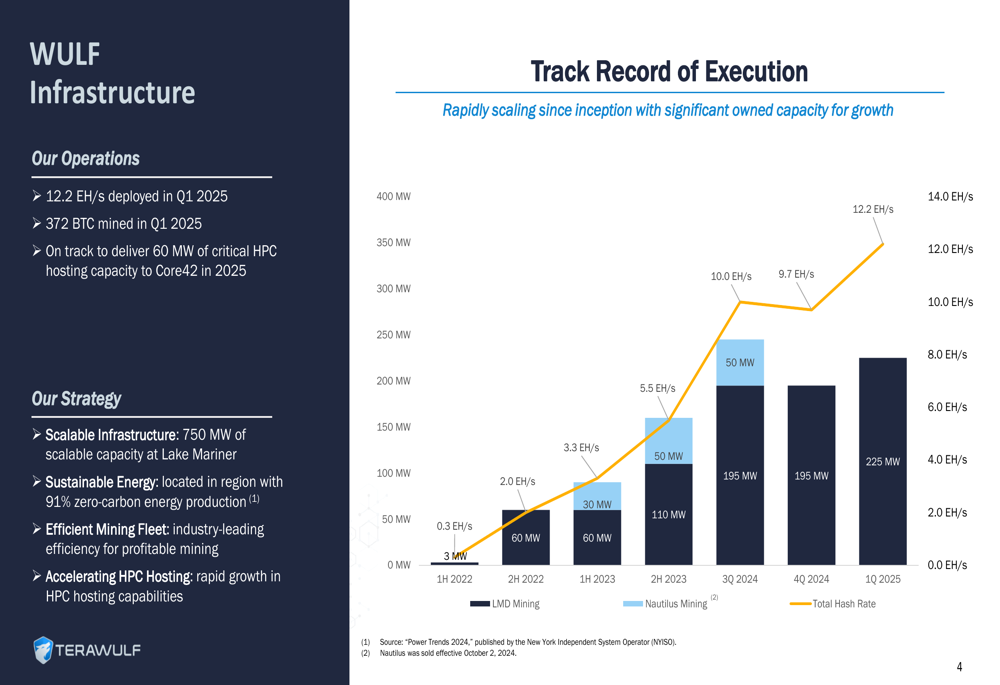

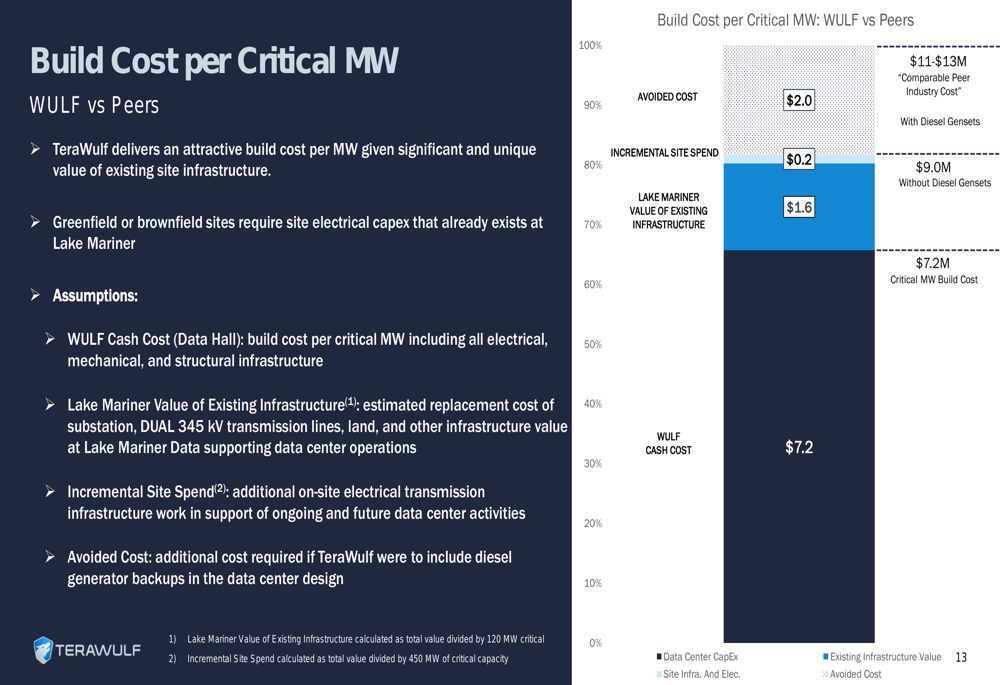

TeraWulf’s infrastructure strategy leverages its existing assets at the Lake Mariner facility, which the company claims provides cost advantages compared to peers. The presentation highlighted that TeraWulf can deliver HPC hosting capacity at approximately $7.2 million per critical MW, which it asserts is competitive due to the value of existing site infrastructure.

The company’s infrastructure development and execution track record was emphasized as a key competitive advantage:

Detailed Financial Analysis

TeraWulf ended Q1 2025 with $218.2 million in cash and cash equivalents, plus $1.4 million in Bitcoin holdings. The company reported net debt of $281.8 million, which includes $500 million in 2.75% Convertible Notes issued in October 2024.

The quarter saw significant capital allocation decisions, including a $90 million pre-payment from Core42, $76 million invested in HPC hosting capacity, $33 million in share repurchases, and $17 million in mining infrastructure investments. These allocations reflect the company’s strategic shift toward HPC hosting while maintaining its Bitcoin mining operations.

The company’s mining fleet efficiency improved to 18 J/TH in Q1 2025, compared to 25.4 J/TH in Q1 2024, demonstrating operational improvements despite profitability challenges. The fleet now consists primarily of newer, more efficient S21 Pro and S21 miners, which account for a significant portion of the company’s 12.2 EH/s total capacity.

Forward-Looking Statements

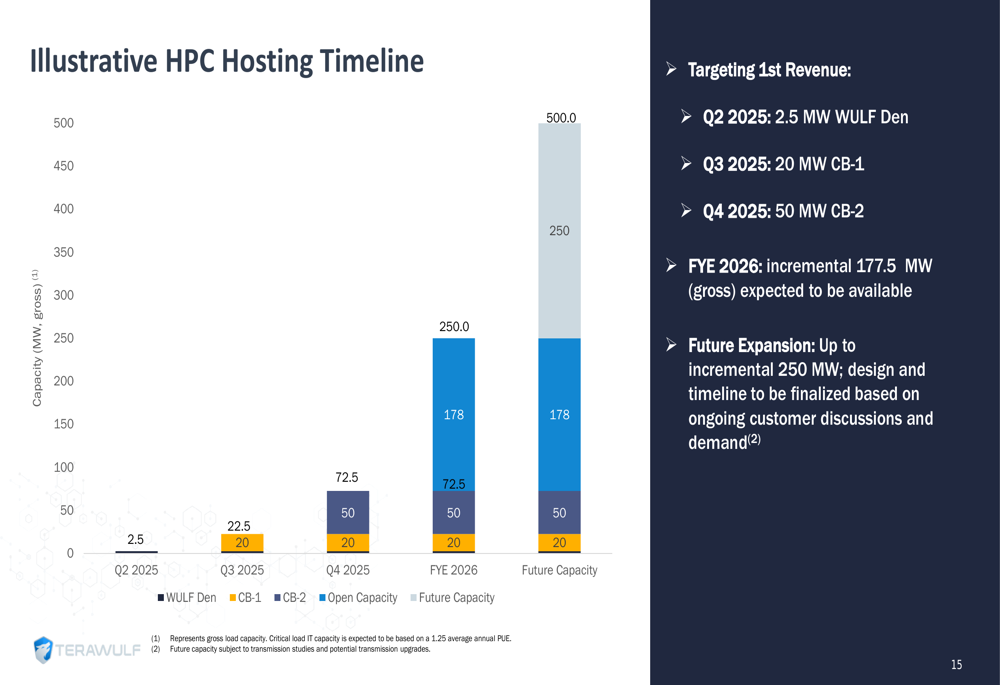

TeraWulf outlined an ambitious growth plan for its HPC hosting business, targeting 200 MW (net) run rate by the end of 2026. The company’s HPC hosting timeline shows a phased approach, beginning with the first revenue expected in Q2 2025 with 2.5 MW, followed by 20 MW in Q3 and 50 MW in Q4.

The company’s HPC hosting timeline is illustrated in the following chart:

For its Bitcoin mining operations, TeraWulf is targeting 225 MW and 12 EH/s for Q2-Q4 2025, maintaining current capacity levels rather than pursuing aggressive expansion. This stabilization reflects the challenging economics of Bitcoin mining amid rising network difficulty and power costs.

TeraWulf’s 2025 capital allocation plan includes approximately $300 million in project financing for HPC hosting capacity, offset by an equivalent investment in that capacity. The company also plans to invest $60 million in site electrical infrastructure, leaving an estimated $158 million in unallocated cash by the end of 2025.

Competitive Industry Position

TeraWulf positions itself as uniquely advantaged in the competitive landscape of both Bitcoin mining and HPC hosting due to its existing infrastructure at Lake Mariner. The company claims its build cost per critical MW is lower than peers due to avoided costs for site electrical infrastructure that already exists at its facility.

As shown in the following comparison of build costs versus peers:

The company’s HPC hosting economics are projected to deliver attractive returns, with updated guidance suggesting approximately $1.6 million in annual recurring rent per MW and EBITDA margins of approximately 75%. The total capital expenditure for the HPC hosting business is estimated at $430 million, with a cost of approximately $7.2 million per critical MW.

Analyst Perspectives

While the presentation did not include analyst commentary, the company’s Q4 2024 earnings call transcript revealed analyst concerns about power price volatility and its impact on costs. According to the previous earnings report, TeraWulf missed both earnings and revenue forecasts for Q4 2024, with an EPS of -$0.09 against an expected -$0.028.

CEO Paul Prager has emphasized the company’s long-term vision, stating, "This is not a sprint. This is about building a business with long-term steady and predictable cash flows." This perspective aligns with the strategic pivot toward HPC hosting, which offers more predictable revenue streams compared to volatile Bitcoin mining.

The market’s reaction to TeraWulf’s strategic shift has been cautious, with the stock experiencing significant volatility. According to the earnings article, the stock has a beta of 4.06 and was down 36.22% year-to-date as of the previous earnings report, suggesting ongoing investor uncertainty about the company’s transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.