Bitcoin price today: tumbles below $90k as Fed cut doubts spark risk-off mood

Introduction & Market Context

Tetra Tech Inc (NASDAQ:TTEK) presented its third quarter fiscal year 2025 earnings on July 31, 2025, revealing substantial growth in revenue and profitability. The water and environmental services provider reported significant margin expansion and earnings per share growth that outpaced revenue increases, continuing the momentum seen in the previous quarter.

The company’s stock closed at $37.54 before the earnings announcement, and showed positive movement in after-hours trading, with the price rising 0.72% to $37.81. This follows a 13.41% surge after the previous quarter’s results, indicating continued investor confidence in the company’s performance and outlook.

Quarterly Performance Highlights

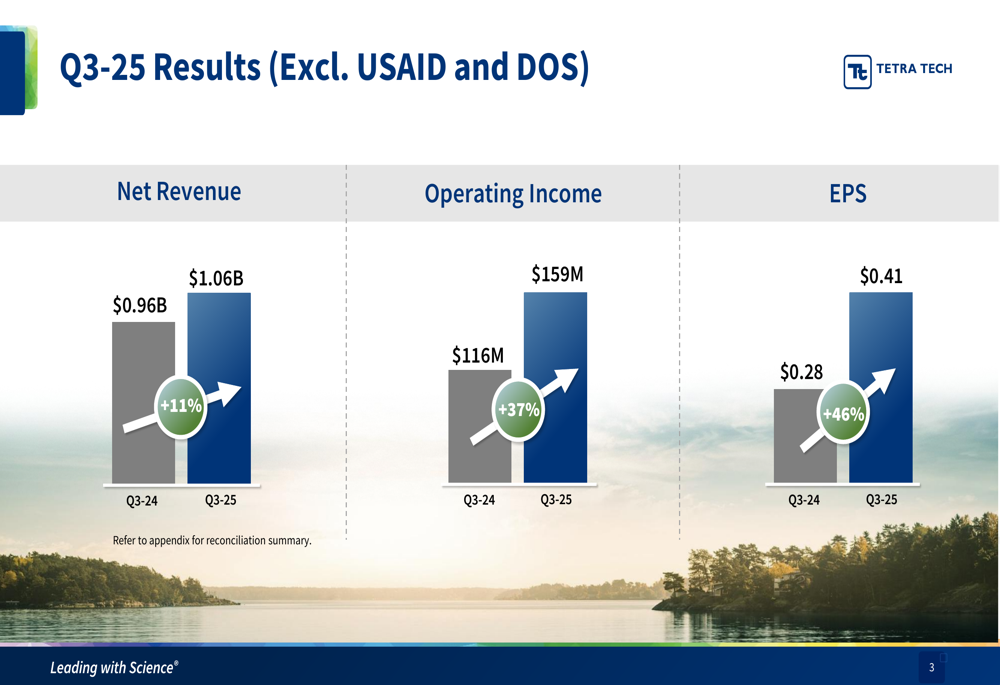

Tetra Tech reported impressive financial results for Q3 2025, with substantial year-over-year improvements across key metrics. Net revenue reached $1.06 billion, representing an 11% increase compared to $0.96 billion in the same period last year. More notably, operating income surged 37% to $159 million, while earnings per share jumped 46% to $0.41.

As shown in the following chart of quarterly financial performance:

These results demonstrate Tetra Tech’s ability to grow profitability at a faster rate than revenue, reflecting improved operational efficiency and successful execution of high-margin projects. The company’s earnings growth continues to exceed its revenue growth, a trend highlighted in its year-to-date performance as well.

Segment Performance Analysis

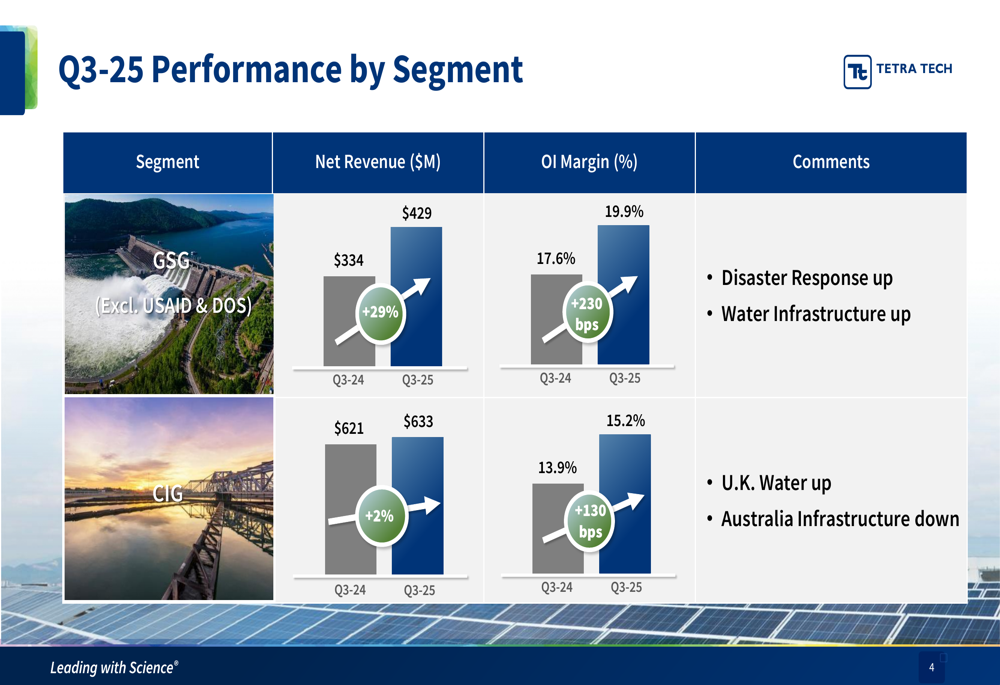

Tetra Tech’s performance was driven by strong results in its Government Services Group (GSG), which saw a 29% increase in net revenue to $429 million, accompanied by a 230 basis point improvement in operating income margin to 19.9%. This segment benefited particularly from increased disaster response activities and water infrastructure projects.

The Commercial International Group (CIG) delivered more modest growth, with net revenue increasing 2% to $633 million and operating income margin improving by 130 basis points to 15.2%. Within this segment, U.K. water planning and design services performed well, while Australia infrastructure projects declined.

The company’s segment performance breakdown is illustrated in the following slide:

Looking at revenue by customer type, U.S. Federal business showed the strongest growth at 46% year-over-year, accounting for 25% of total net revenue. U.S. State & Local government work also performed well with 30% growth, representing 14% of revenue. Meanwhile, U.S. Commercial and International segments, accounting for 19% and 42% of revenue respectively, experienced slight declines of 4% and 1%.

Cash Flow and Balance Sheet Strength

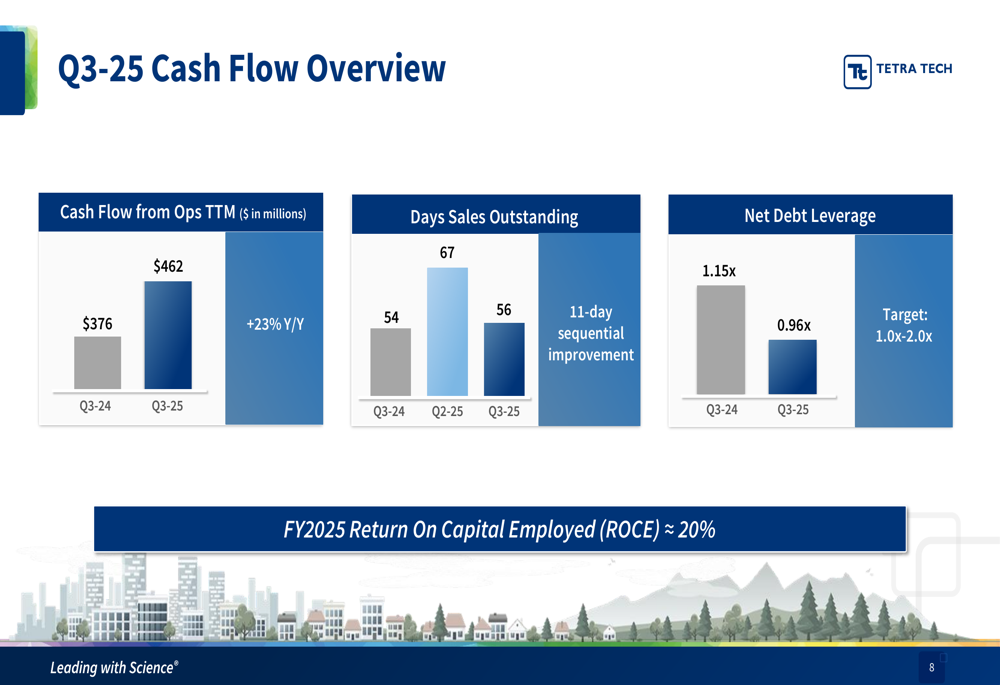

Tetra Tech demonstrated robust cash generation and balance sheet management in Q3 2025. Cash flow from operations for the trailing twelve months reached $462 million, a 23% increase from the prior year. The company also improved its working capital efficiency, reducing days sales outstanding to 56 days, an 11-day sequential improvement.

The company’s financial position is further strengthened by a net debt leverage ratio of 0.96x, down from 1.15x in the previous year and well within the target range of 1.0x-2.0x. This provides Tetra Tech with significant financial flexibility for future investments and shareholder returns.

The following chart illustrates the company’s cash flow performance:

Tetra Tech’s capital allocation strategy includes both growth initiatives and shareholder returns. The company has returned $248 million to shareholders through dividends and share repurchases year-to-date, with $648 million remaining in its authorized buyback program. The quarterly dividend was increased by 12% year-over-year, reflecting confidence in sustained cash generation.

Strategic Initiatives and Market Opportunities

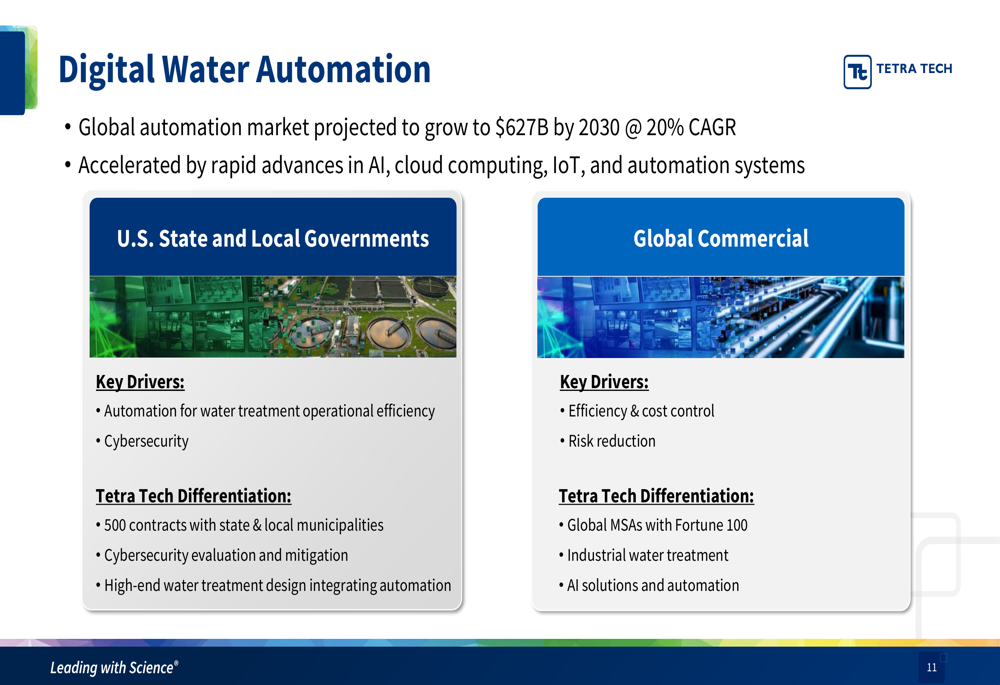

Tetra Tech continues to focus on high-growth areas within the water and environmental sectors. The company highlighted digital water automation as a significant opportunity, noting that the global automation market is projected to grow to $627 billion by 2030 at a 20% compound annual growth rate. This growth is being accelerated by advances in artificial intelligence, cloud computing, Internet of Things, and automation systems.

The company’s strategic focus on digital water automation is illustrated in the following slide:

Additionally, Tetra Tech is well-positioned to benefit from the recently signed One Big Beautiful Bill Act (OBBBA), which provides supplemental funding for various U.S. federal agencies. The legislation includes $150 billion for Defense to improve water infrastructure and defense facilities, $25 billion for the Coast Guard, and $12.5 billion for the FAA, all areas where Tetra Tech has established contract capacity and expertise.

The company’s backlog remains strong at $4.15 billion, slightly up from $4.14 billion in the same period last year, providing visibility into future revenue. Recent key contract wins include a $990 million multiple-award contract for engineering design for NAVFAC Pacific and a $249 million multiple-award contract for energy resilience for USACE Huntsville District.

Guidance and Outlook

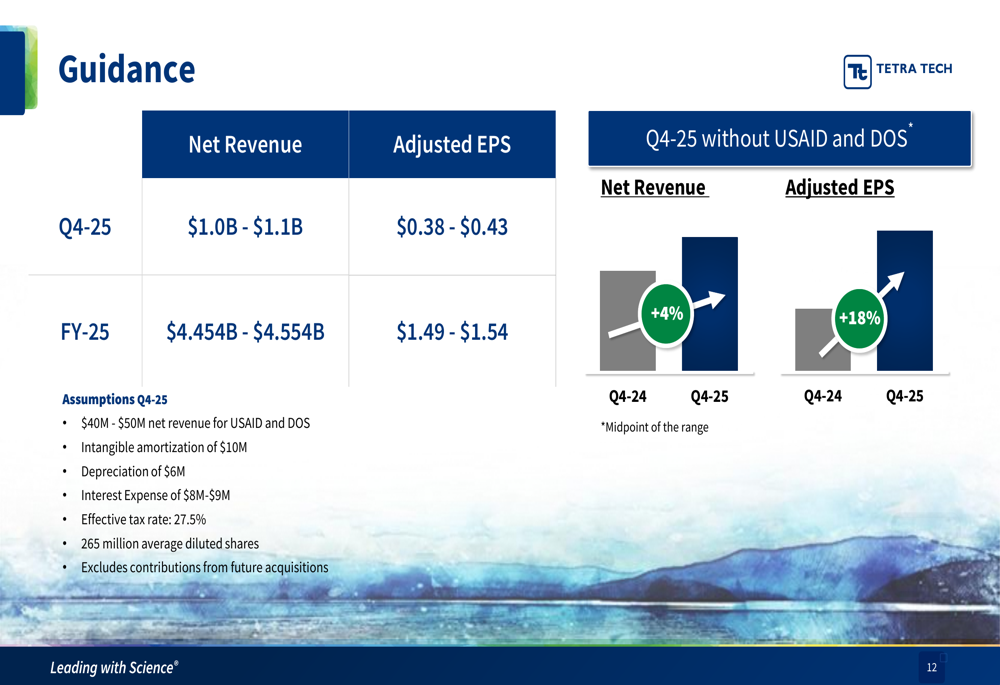

Looking ahead, Tetra Tech provided guidance for both the fourth quarter and full fiscal year 2025. For Q4, the company expects net revenue between $1.0 billion and $1.1 billion, with adjusted earnings per share of $0.38 to $0.43. For the full year, net revenue is projected to reach $4.454 billion to $4.554 billion, with adjusted EPS of $1.49 to $1.54.

The company’s financial guidance is summarized in the following slide:

This guidance represents approximately 4% growth in net revenue and 18% growth in adjusted EPS for the fourth quarter compared to the same period last year (excluding USAID and DOS). The company remains confident in its ability to deliver solid performance, citing continued demand for its differentiated water services, significant margin expansion, and a strong balance sheet for future capital deployment.

Tetra Tech’s performance in Q3 2025 builds on the momentum seen in the previous quarter, where the company exceeded analyst expectations with EPS of $0.33 against a forecast of $0.30. The continued strength in the Government Services Group, improved margins, and robust cash flow position the company well for sustained growth in its core water, environmental, and infrastructure markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.