These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Textron Inc . (NYSE:TXT) released its first quarter 2025 earnings presentation on April 24, 2025, revealing a 6.5% year-over-year revenue increase to $3.3 billion, driven primarily by exceptional performance in its Bell helicopter division. The presentation comes after a challenging third quarter in 2024 when the company missed earnings estimates and lowered guidance due to labor strikes and production challenges.

Shares of Textron closed at $66.23 on April 23 and were trading up 1.16% to $67 in premarket activity following the earnings release, suggesting cautious optimism from investors despite mixed results across business segments.

Quarterly Performance Highlights

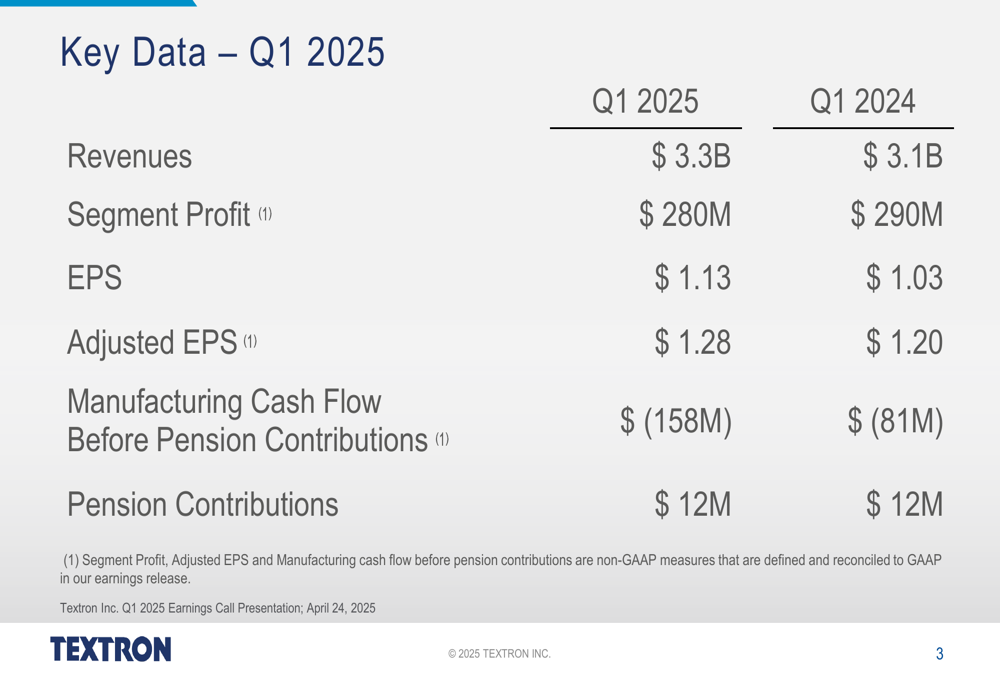

Textron reported earnings per share of $1.13 for Q1 2025, representing a 9.7% increase from $1.03 in the same period last year. On an adjusted basis, EPS reached $1.28, up 6.7% from $1.20 in Q1 2024. This improvement in bottom-line performance came despite a slight decline in segment profit, which decreased 3.4% to $280 million from $290 million a year earlier.

As shown in the following key financial metrics comparison:

The company’s manufacturing cash flow before pension contributions deteriorated to negative $158 million compared to negative $81 million in the first quarter of 2024, indicating ongoing challenges in working capital management. Pension contributions remained stable at $12 million for both periods.

Segment Performance Analysis

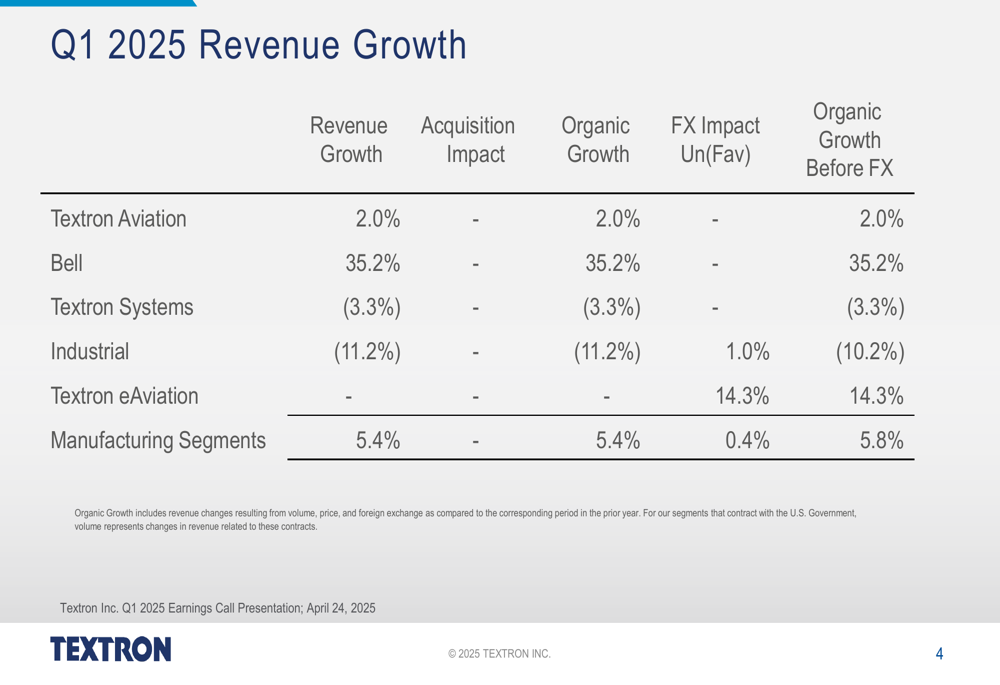

The most striking aspect of Textron’s Q1 results was the dramatic variance in performance across its business segments. Bell emerged as the standout performer with 35.2% organic revenue growth, while the Industrial segment experienced a concerning 11.2% decline.

The following breakdown illustrates the divergent segment performance:

Textron Aviation, which includes the Cessna and Beechcraft brands, delivered modest 2.0% growth despite lingering effects from labor disruptions experienced in late 2024. The Bell segment’s exceptional performance likely reflects increased defense contract fulfillment and recovery from previous supply chain constraints.

Textron Systems, which provides military, government, and commercial customers with unmanned aircraft systems and other defense products, saw a 3.3% revenue decline. The Industrial segment’s 11.2% drop (10.2% before foreign exchange impacts) represents a continuation of challenges in specialized vehicles and automotive components markets.

The relatively new Textron eAviation division, which includes the Pipistrel electric aircraft business, showed encouraging 14.3% growth, albeit from a smaller base.

Financial Position and Outlook

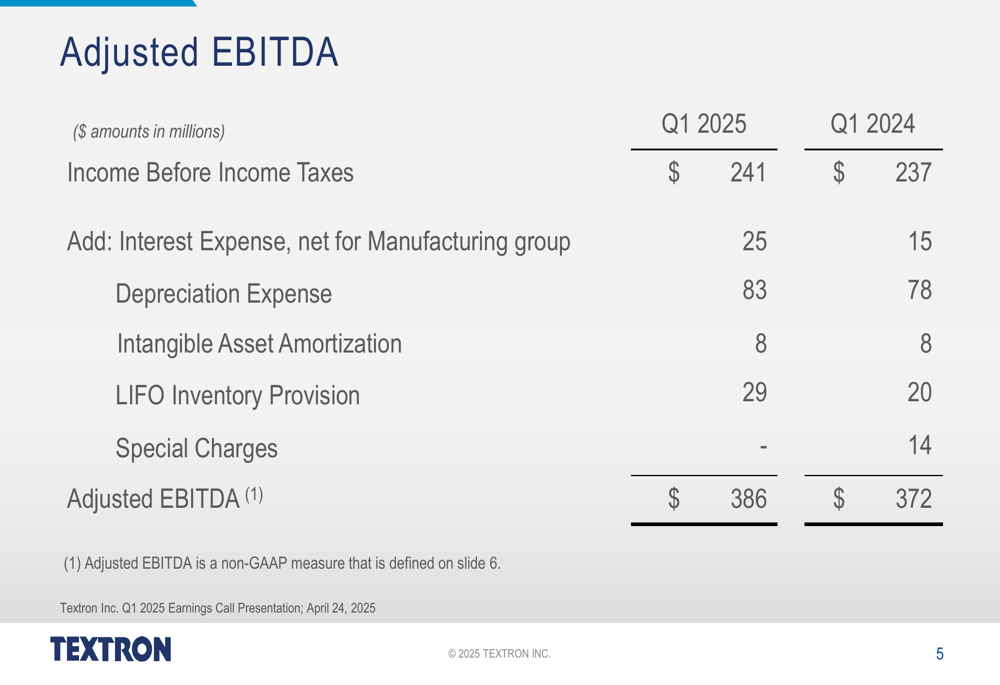

Textron’s adjusted EBITDA increased to $386 million in Q1 2025 from $372 million in Q1 2024, representing a 3.8% improvement. This metric provides insight into the company’s operational performance before accounting for certain non-cash and non-recurring items.

The reconciliation from income before taxes to adjusted EBITDA is detailed below:

Notable in this reconciliation is the increased LIFO inventory provision of $29 million compared to $20 million in the prior year, suggesting potential inventory valuation challenges. The absence of special charges in Q1 2025 (compared to $14 million in Q1 2024) contributed positively to the results.

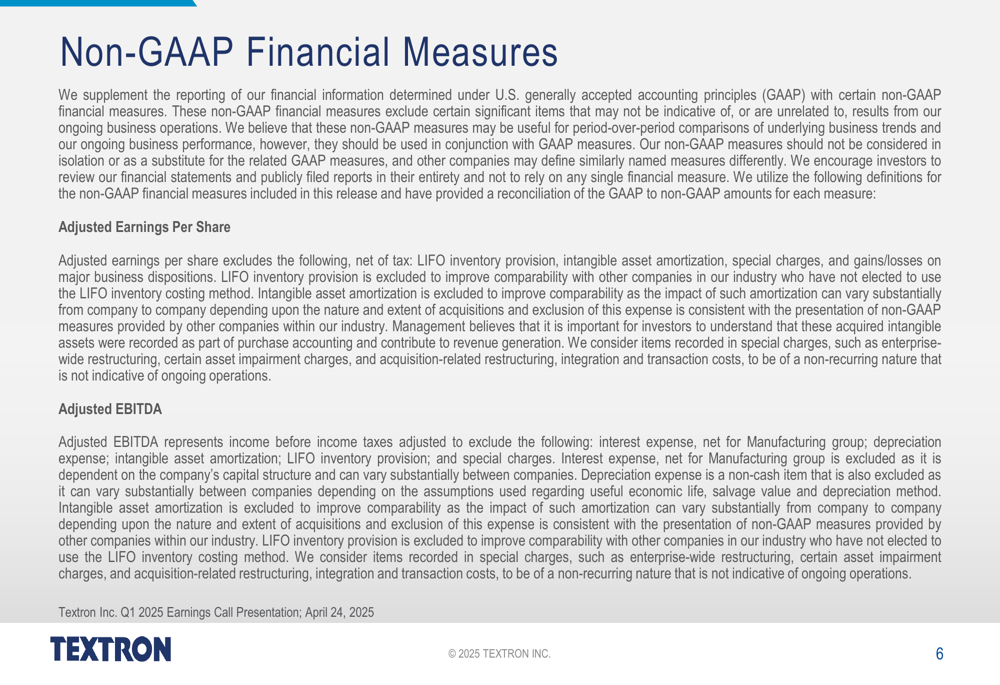

For context on the non-GAAP measures used in the presentation:

Market Reaction and Outlook

The modest premarket stock price increase of 1.16% suggests investors are cautiously positive about Textron’s Q1 results, particularly appreciating the EPS growth and Bell segment’s strong performance while remaining concerned about cash flow deterioration and weakness in the Industrial segment.

These results come after a challenging period for Textron. In Q3 2024, the company missed earnings estimates and lowered its full-year guidance due to a labor strike and production challenges. The current quarter shows signs of recovery in some areas but continued difficulties in others.

Textron’s diverse brand portfolio positions it across multiple aerospace, defense, and industrial markets:

The company’s ability to leverage this diversification has helped offset weaknesses in certain segments, particularly as Bell’s strong performance compensated for declines elsewhere. However, the continued cash flow challenges and mixed segment performance suggest Textron still faces headwinds as it progresses through 2025.

While the presentation did not include specific forward guidance, investors will be watching closely to see if the Bell segment’s momentum can be maintained and whether the Industrial and Systems segments can reverse their negative trends in subsequent quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.