Bitcoin price today: dips to $92k as Fed cut doubts spark risk-off mood

Introduction & Market Context

TGS NOPEC Geophysical Company ASA (OB:TGS) presented its first quarter 2025 results on May 9, 2025, highlighting solid performance despite ongoing industry challenges. The company, which completed its merger with PGS in July 2024, reported growth in both revenue and EBITDA compared to the same period last year, primarily driven by strong multi-client performance and improved asset utilization.

The presentation comes amid a challenging backdrop for the energy sector, with declining reserve life and replacement ratios for major international oil companies creating both challenges and opportunities for seismic data providers. TGS management emphasized their disciplined approach to capital allocation while maintaining their dividend commitment to shareholders.

Quarterly Performance Highlights

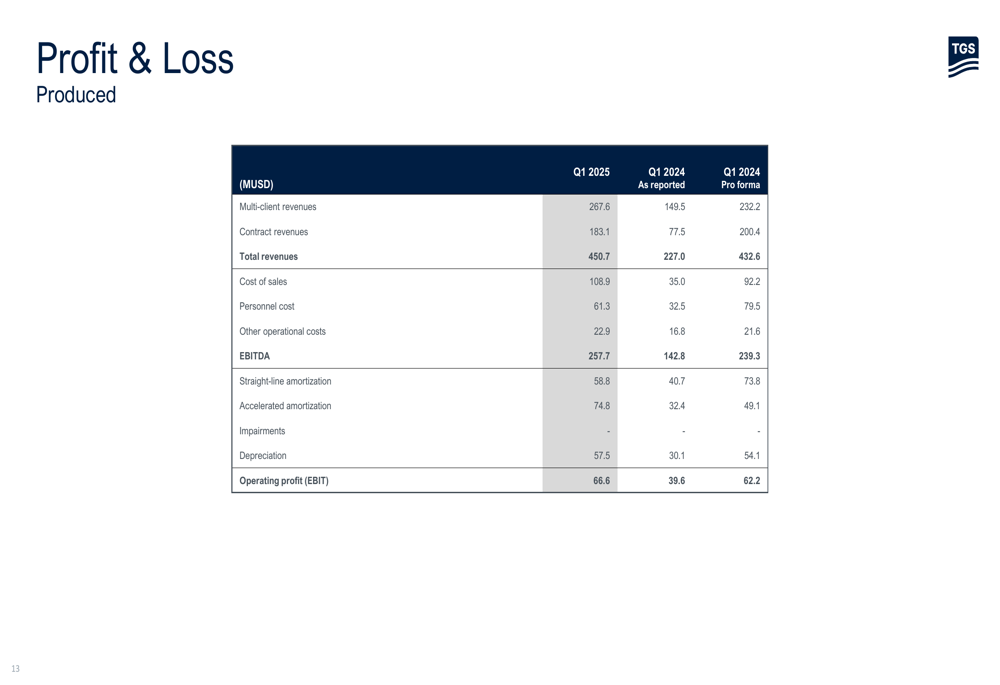

TGS reported total revenues of $451 million for Q1 2025, representing a 4.2% increase from $433 million in Q1 2024. EBITDA rose more significantly to $258 million, up 7.9% from $239 million in the same period last year, reflecting improved operational efficiency. The company generated a net cash flow of $78 million and maintained its quarterly dividend at $0.155 per share.

As shown in the following comprehensive profit and loss statement, TGS saw particularly strong performance in its multi-client segment, with revenues reaching $267.6 million compared to $232.2 million in Q1 2024:

The company’s operating profit (EBIT) reached $66.6 million, compared to $62.2 million in Q1 2024 on a pro forma basis. This performance was achieved despite ongoing market uncertainties and competitive pressures in certain segments.

Segment Performance Analysis

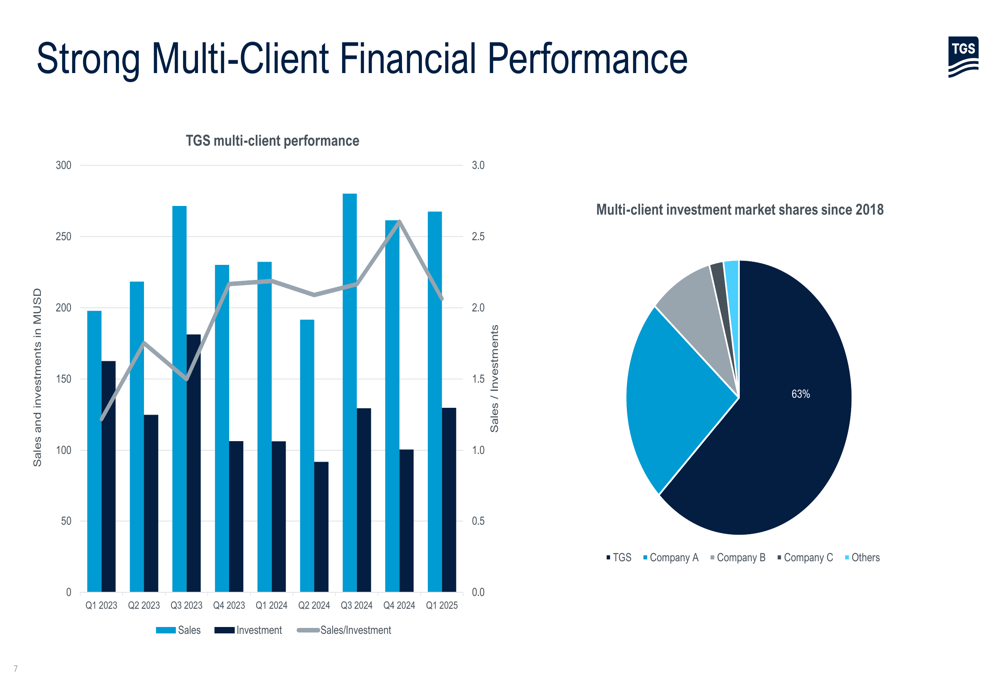

TGS’s multi-client business emerged as the standout performer in Q1 2025, with sales of $267.6 million representing a 15.2% increase year-over-year. This growth was attributed to high client commitment and strong sales of vintage library data in frontier areas. The company invested $129.7 million in multi-client projects during the quarter, including key projects in the equatorial margin of Brazil and offshore Argentina.

The following chart illustrates TGS’s dominant position in the multi-client market, where it holds a 63% market share of investments since 2018:

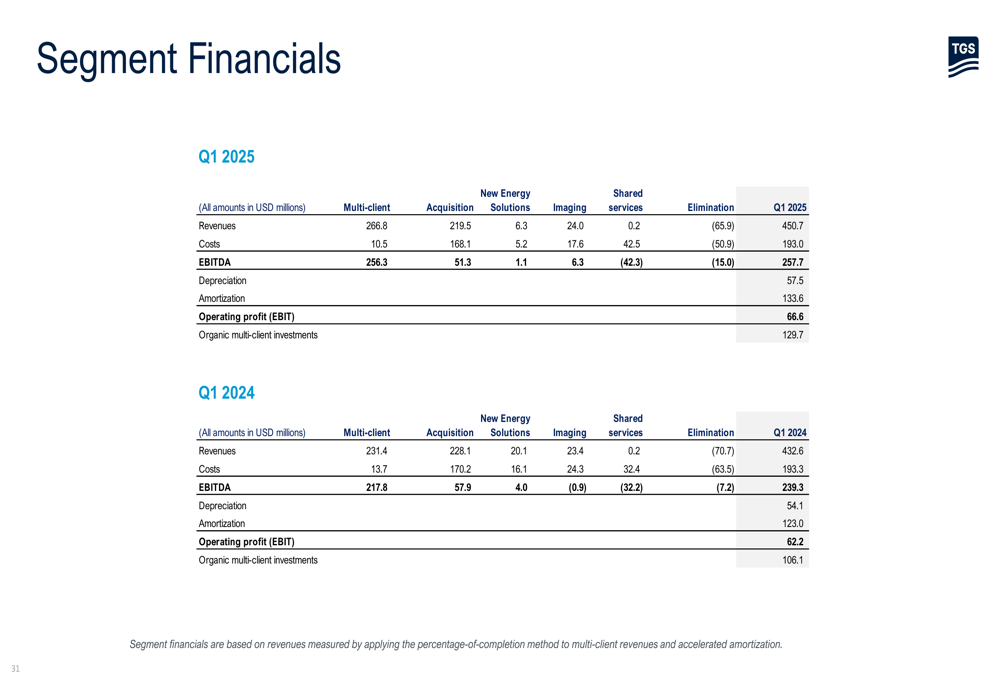

The contract business showed mixed results, with OBN (ocean bottom node) contract revenues increasing 28.6% to $90 million, while streamer contract revenues declined 17.7% to $130 million. Overall, the segment demonstrated significant year-over-year improvement in asset utilization.

The company’s New Energy Solutions segment experienced a significant decline, with revenues falling to just $6 million from $20 million in Q1 2024. TGS attributed this to lower data acquisition activity in the quarter.

The imaging segment delivered stable revenues of $24 million but showed dramatic improvement in profitability, with EBITDA margin increasing to 26% compared to -4% in Q1 2024. The following segment breakdown provides a comprehensive view of performance across all business areas:

Financial Position and Cash Flow

TGS maintained a solid balance sheet in Q1 2025, with total equity of $2,055.4 million as of March 31, 2025. The company’s cash flow from operating activities was strong at $260.8 million, while investing activities consumed $144.5 million and financing activities used $77.0 million.

The company’s multi-client library, a key asset, was valued at $1,139.4 million, slightly down from $1,196.8 million at the end of 2024. This reflects the company’s continued investment in this core business segment while managing amortization.

TGS has maintained its quarterly dividend of $0.155 per share, with an ex-date of May 16, 2025, and payment date of June 2, 2025. The current dividend yield stands at approximately 7.4%, significantly higher than in previous years, as shown in the presentation. The company highlighted that it has returned more than $1.5 billion to shareholders through dividends and buybacks since 2010.

Outlook and Guidance

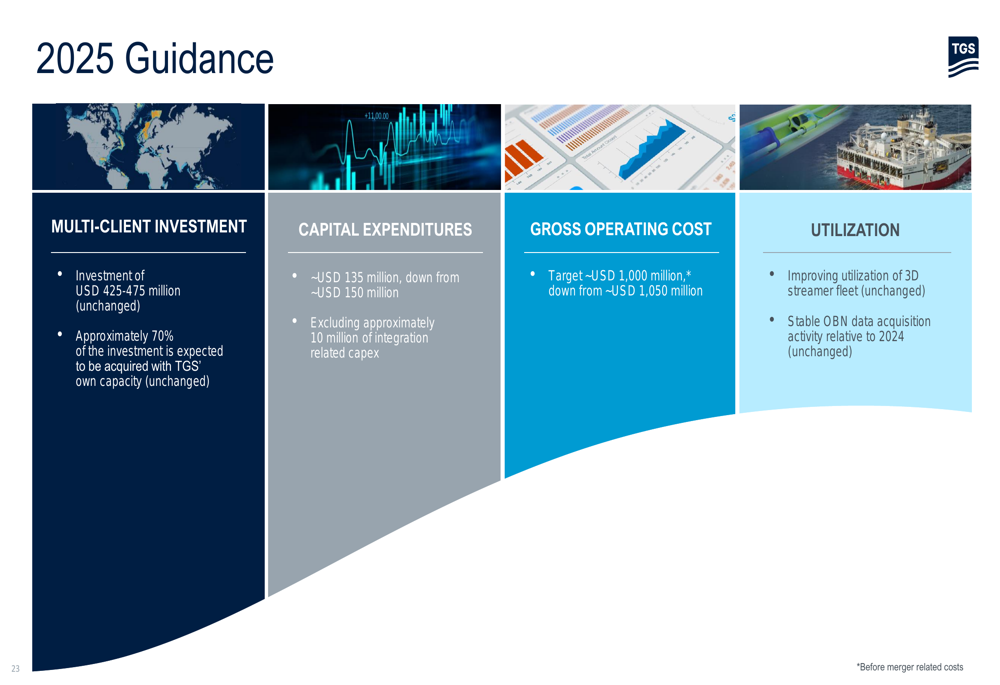

Looking ahead, TGS provided updated guidance for 2025, maintaining its multi-client investment target while reducing projections for capital expenditures and operating costs:

The company expects to invest $425-475 million in multi-client projects, with approximately 70% of this investment to be acquired with TGS’s own capacity. Capital expenditures are now projected at approximately $135 million, down from the previous guidance of $150 million, excluding integration-related expenses.

TGS also reduced its target for gross operating costs to approximately $1,000 million, down from $1,050 million, before merger-related costs. The company expects improving utilization of its 3D streamer fleet and stable OBN data acquisition activity relative to 2024.

For Q2 2025 specifically, TGS anticipates normalized OBN crew count of approximately 2.5-3.0, streamer 3D fleet utilization in line with Q1 2025, and multi-client investments of approximately $100 million.

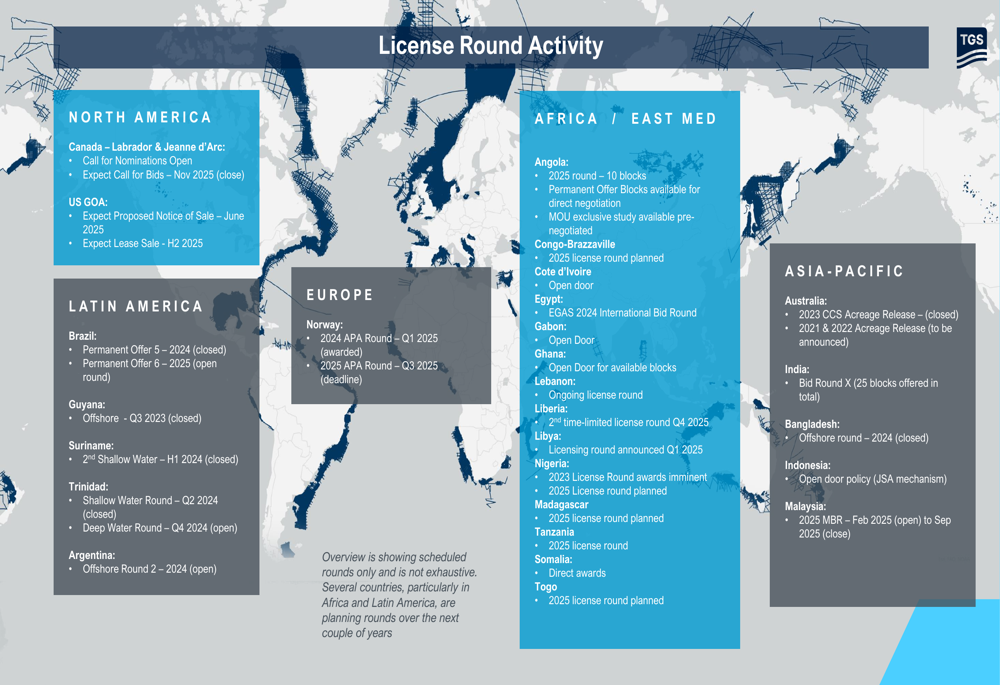

The global market opportunity remains substantial, as illustrated by the company’s license round activity map showing numerous upcoming bidding opportunities across multiple regions:

In response to macro uncertainties, including oil price volatility, TGS outlined several strategic initiatives including strengthening its sales force and business development efforts, enhancing customer relationships, implementing high scrutiny for all capital expenditures, and deferring non-critical investments.

Despite challenges in certain segments and broader market uncertainties, TGS’s strong Q1 2025 performance, particularly in its core multi-client business, positions the company to maintain its market leadership while delivering value to shareholders through consistent dividends and disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.