Fed independence crucial for U.S. and global economy, says Williams

Introduction & Market Context

The Joint Corp (NASDAQ:JYNT), a provider of affordable chiropractic care, presented its second quarter 2025 financial results on August 7, 2025, revealing significant progress in its strategic shift toward a franchise-heavy business model. The company reported a 52% increase in consolidated Adjusted EBITDA despite modest revenue growth, while continuing to execute on its refranchising initiative. The stock closed at $10.70, down 3.86% on the day of the presentation.

The company’s mission to "improve quality of life through routine and affordable chiropractic care" remains central to its operations as it works toward its vision of becoming "America’s most accessible health and wellness services company." With 80% of new patients citing aches and pains as their primary reason for seeking treatment, The Joint continues to position itself as an accessible solution in the healthcare market.

Quarterly Performance Highlights

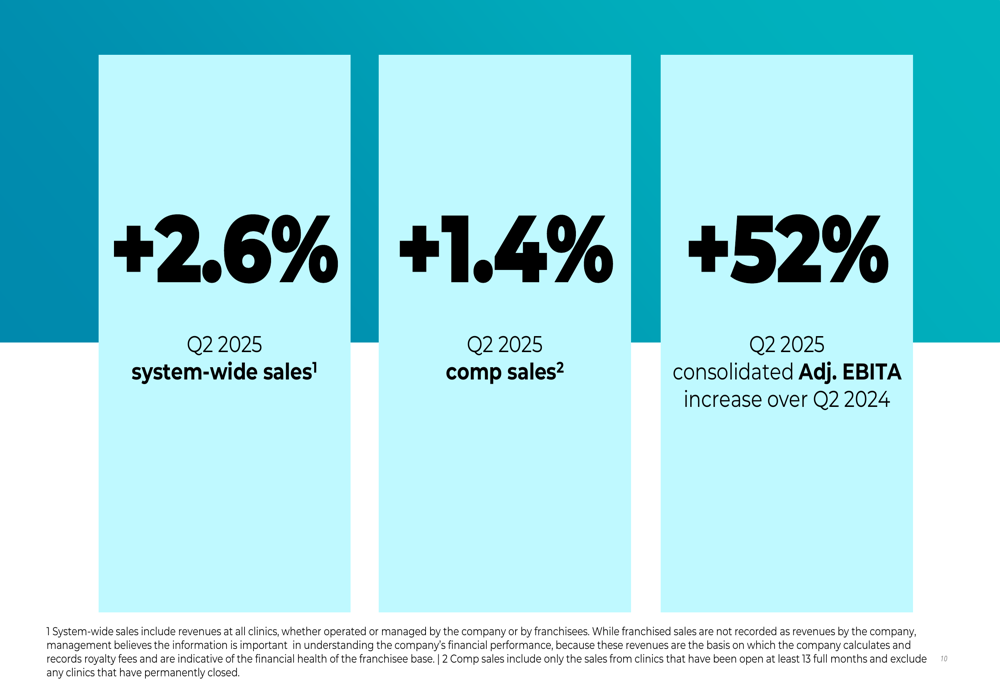

The Joint Corp reported several positive financial metrics for Q2 2025, most notably a substantial improvement in profitability. System-wide sales increased by 2.6% compared to Q2 2024, while comparable sales grew by 1.4%. Revenue reached $13.3 million, representing a 5% increase year-over-year.

As shown in the following financial highlights from the presentation:

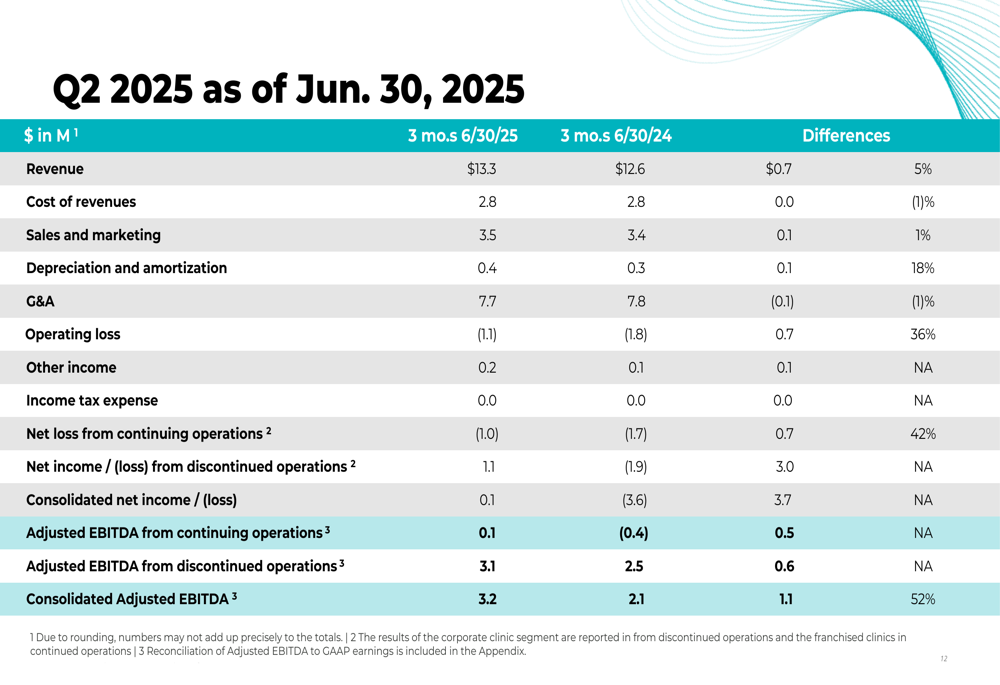

The most impressive metric was the 52% increase in consolidated Adjusted EBITDA compared to the same period last year. However, the company still reported an operating loss of $1.1 million (a 36% increase from Q2 2024) and a net loss from continuing operations of $1.0 million (a 42% increase).

The detailed financial results provide further context for the quarter’s performance:

The company’s liquidity position remains strong, with unrestricted cash increasing to $29.8 million as of June 30, 2025, up from $25.1 million at the end of 2024. Additionally, The Joint has $20 million available through its JP Morgan Chase (NYSE:JPM) line of credit and has authorized a stock repurchase plan of up to $5 million through June 2027.

Strategic Initiatives

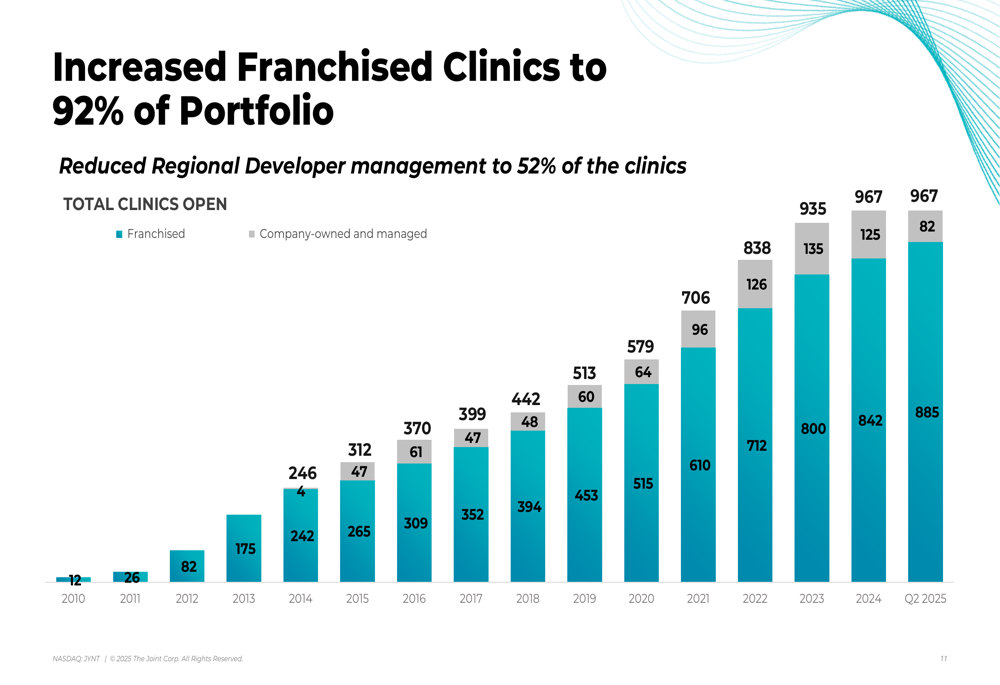

The Joint Corp continues to execute its strategy of becoming a pure play franchisor. During Q2 2025, the company refranchised 37 clinics: 31 in Arizona and New Mexico, 5 in Kansas City, and 1 in California. This strategic shift is evident in the company’s clinic portfolio, where franchised clinics now represent 92% of the total, up from a much smaller percentage in previous years.

The following chart illustrates this dramatic transformation in the company’s business model:

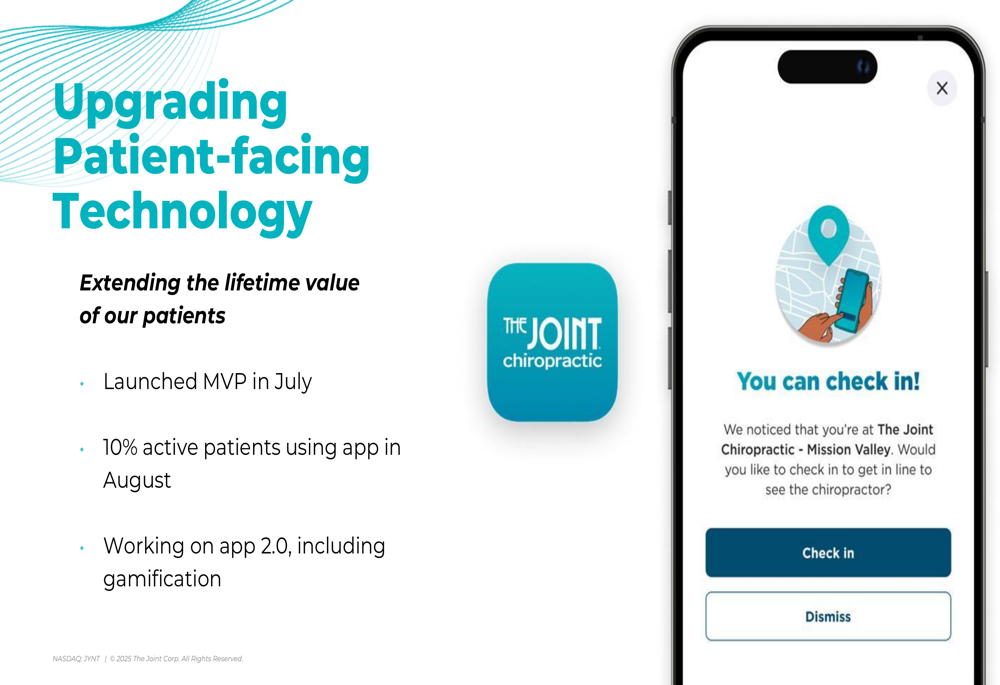

Beyond refranchising, The Joint is implementing several initiatives to drive growth and enhance patient value. In July 2025, the company launched a new mobile app, with 10% of active patients already using it by August. The company is working on version 2.0 of the app, which will include gamification features to increase engagement.

As shown in this mockup of the patient-facing technology:

The company is also implementing a dynamic revenue management strategy, which includes more frequent but smaller price increases than in the past. Walk-in pricing adjustments were made in December 2024, and "Kickstart" plans were introduced in July 2025, with additional pricing opportunities being explored for the remainder of the year.

The Joint’s strategic priorities remain centered around patients, as illustrated in this comprehensive framework:

Detailed Financial Analysis

The Joint Corp’s financial performance in Q2 2025 shows a company in transition. While revenue growth remains modest at 5%, the significant improvement in Adjusted EBITDA suggests that operational efficiencies are beginning to materialize as the company shifts toward a franchise-heavy model.

This improvement is particularly notable when compared to Q1 2025 results, where the company reported Adjusted EBITDA of just $46,000, down from $425,000 in Q1 2024. The substantial year-over-year improvement in Q2 suggests that the company’s strategic initiatives are gaining traction.

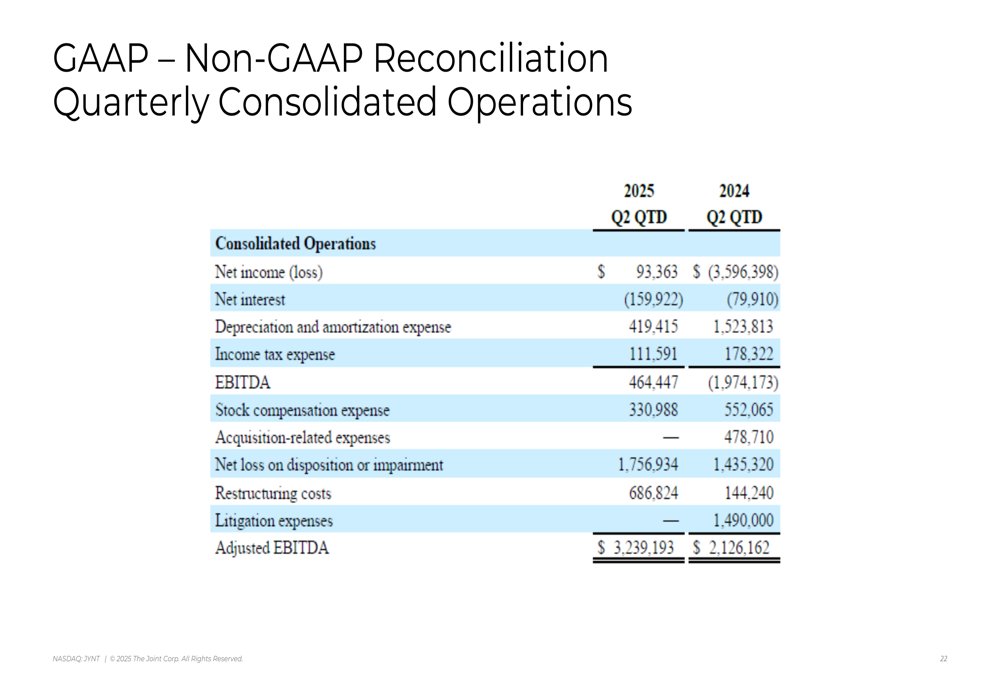

The GAAP reconciliation provides further insight into the components driving the improved EBITDA performance:

Despite the positive EBITDA trend, investors should note that the company continues to report operating losses and net losses from continuing operations, which increased by 36% and 42% respectively compared to Q2 2024. This suggests that while operational improvements are underway, the company still faces challenges in achieving bottom-line profitability.

Forward-Looking Statements

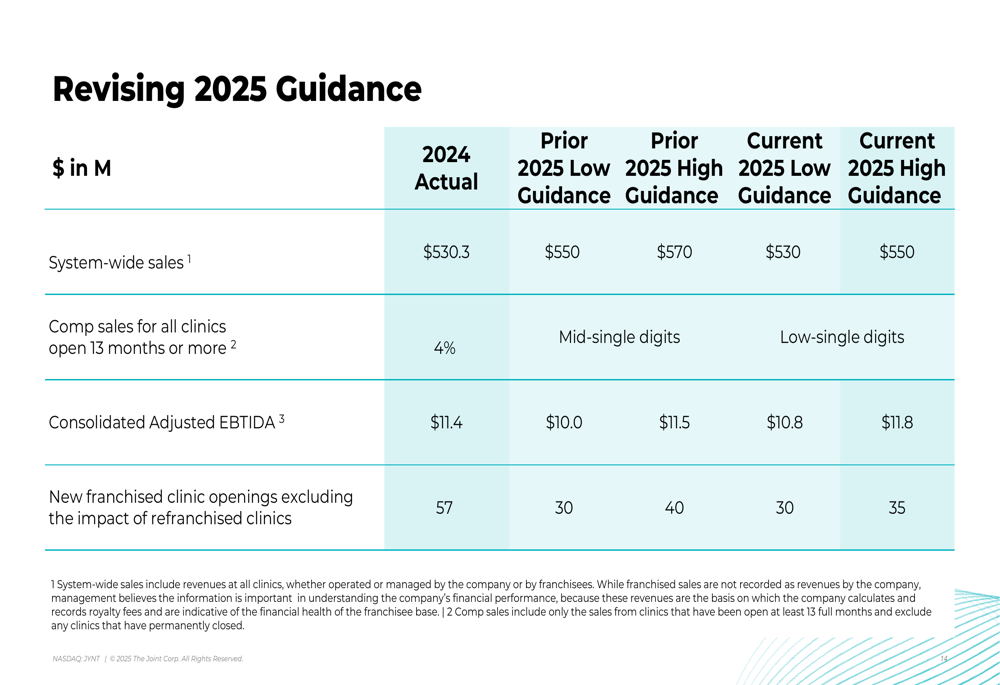

The Joint Corp has revised its 2025 guidance, adjusting expectations for system-wide sales downward while raising projections for consolidated Adjusted EBITDA. The company now expects system-wide sales of $530-550 million, down from the previous guidance of $550-570 million provided in Q1 2025.

As detailed in the revised guidance slide:

Despite lowering sales expectations, the company has increased its Adjusted EBITDA guidance to $10.8-11.8 million, up from the previous range of $10.0-11.5 million. This suggests management’s confidence in operational efficiencies and cost control measures.

The company also narrowed its projection for new franchised clinic openings to 30-35 for the year, compared to the previous range of 30-40. This slight adjustment, combined with the continued refranchising efforts, underscores The Joint’s commitment to its franchise-centric strategy.

CEO Sanjiv Razdan emphasized the company’s focus on patient experience and operational excellence as key drivers of long-term success. With a strong liquidity position and strategic initiatives underway in technology, pricing, and marketing, The Joint Corp appears positioned to continue its transformation while working toward sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.