Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Thinkific Labs Inc (THNC) shares plummeted 37.47% on May 6, 2025, following the release of its Q1 F2025 earnings presentation, which revealed mixed results and signs of slowing growth. The learning commerce platform, which enables businesses to create and sell online courses, reported modest overall revenue growth but showed concerning declines in gross merchandise volume (GMV) amid what the company described as "macroeconomic uncertainty."

Despite CEO Greg Smith framing 2025 as a "transformational year" with upcoming product launches and marketing campaigns, investors appeared unconvinced by the company’s performance and outlook, sending shares tumbling to $2.72 from the previous close of $4.35.

Quarterly Performance Highlights

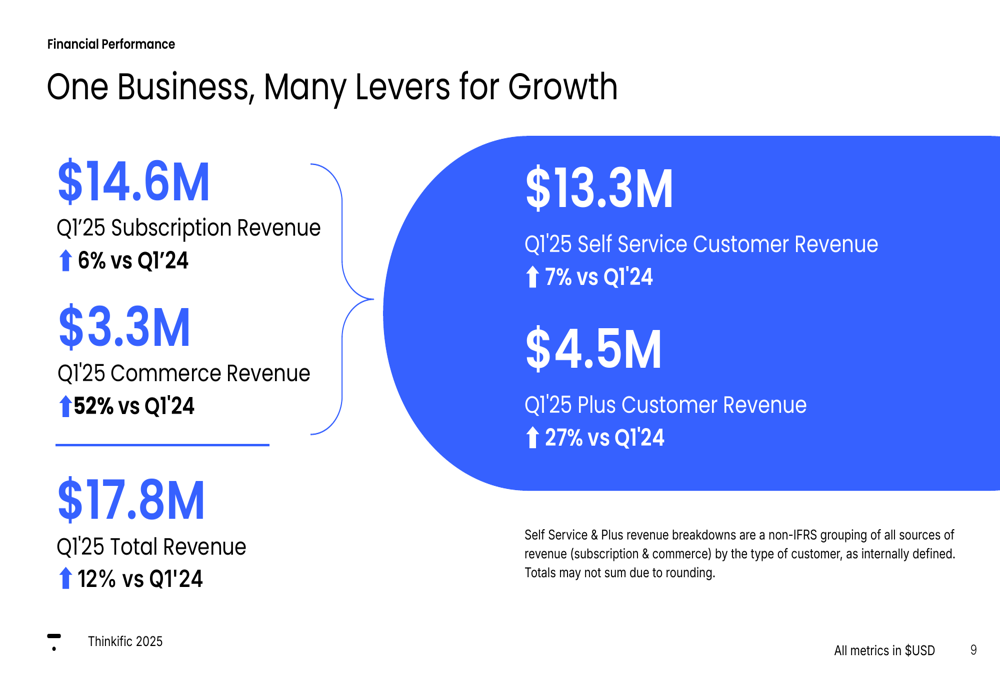

Thinkific reported total revenue of $17.8 million for Q1 2025, representing a 12% year-over-year increase. The company’s performance was driven primarily by its Commerce segment, which grew 52% year-over-year to $3.3 million, while Subscription revenue increased by a more modest 6% to $14.6 million.

As shown in the following breakdown of revenue sources:

The company’s enterprise-focused Thinkific Plus offering continued to show strong momentum, growing 27% year-over-year to $4.5 million, significantly outpacing the 7% growth in Self-Service revenue, which reached $13.3 million.

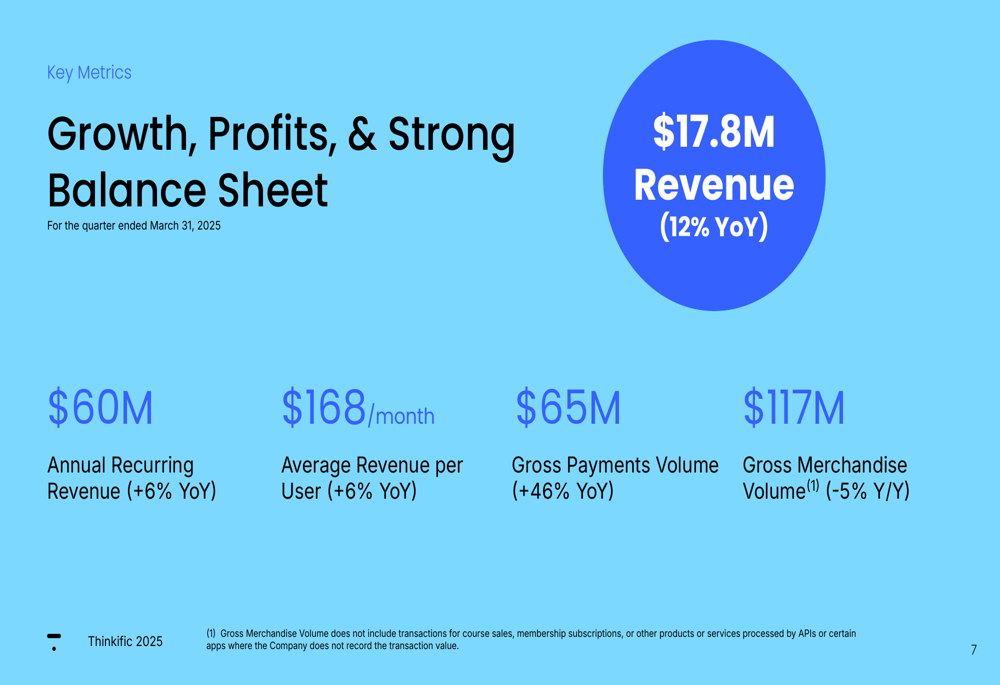

Other key metrics for the quarter included:

While Annual Recurring Revenue (ARR) grew 6% year-over-year to $60 million and Average Revenue Per User (ARPU) increased 6% to $168 per month, the 5% decline in Gross Merchandise Volume (GMV) to $117 million raised concerns about the platform’s overall transaction activity.

Detailed Financial Analysis

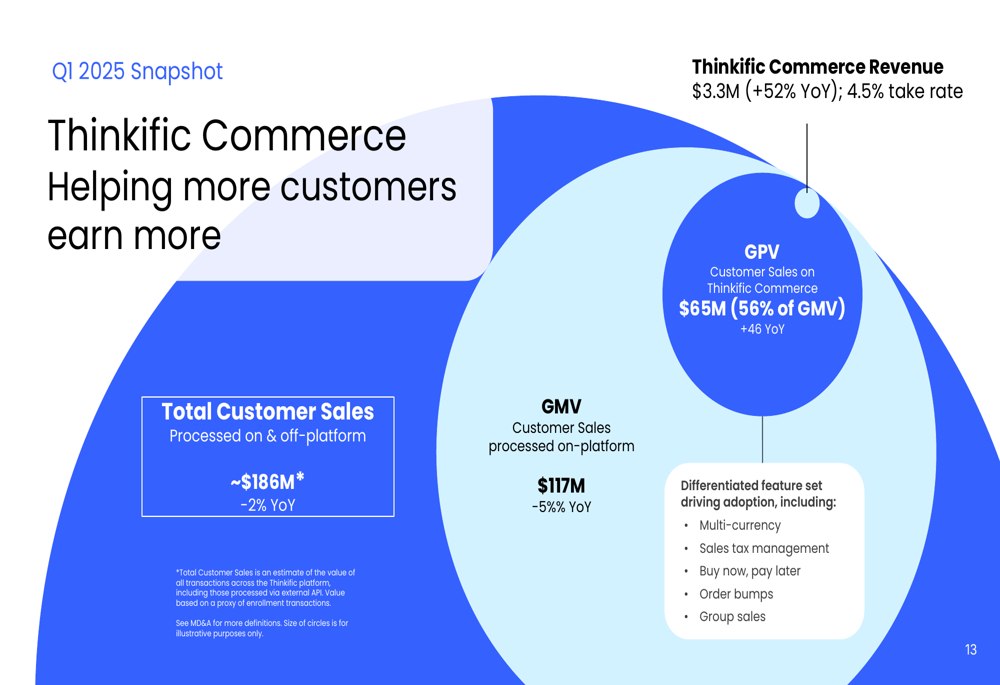

A bright spot in Thinkific’s Q1 results was the performance of its Commerce Engine, which showed significant growth in payment processing. Gross Payments Volume (GPV) increased 46% year-over-year to $65 million, with the company’s payment solution now processing 56% of all platform transactions, up from 52% in Q4 2024.

The following chart illustrates the scale and growth of Thinkific’s Commerce Engine:

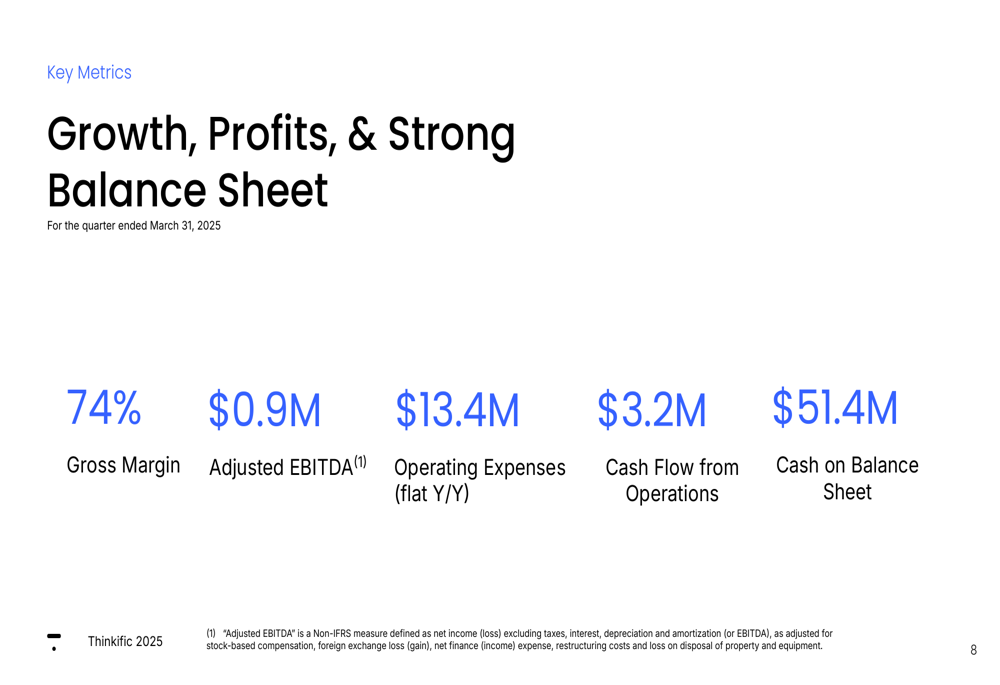

Profitability metrics remained stable, with overall gross margin holding steady at 74% compared to the same period last year. Notably, Commerce gross margin improved to 37% from 33% in Q1 2024, while Subscription gross margin edged up slightly to 82% from 81%.

The company maintained disciplined cost control, with operating expenses flat year-over-year at $13.4 million. This contributed to positive Adjusted EBITDA of $0.9 million and operating cash flow of $3.2 million for the quarter. Thinkific ended the period with a strong cash position of $51.4 million on its balance sheet.

Strategic Initiatives

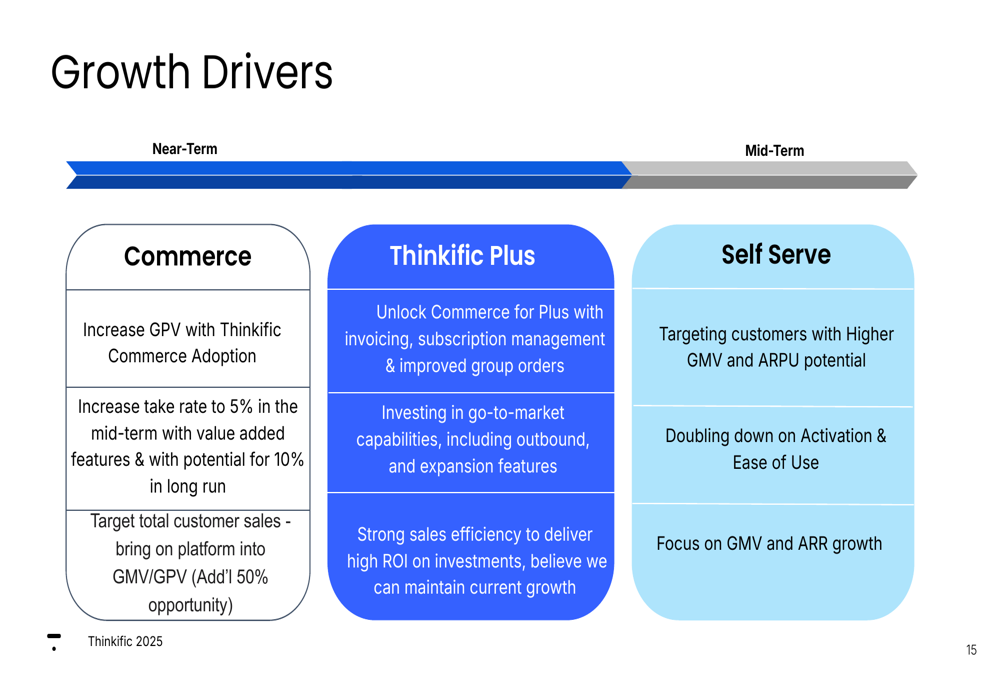

Thinkific outlined three key growth drivers in its presentation, focusing on expanding its Commerce offerings, accelerating Thinkific Plus adoption, and enhancing its Self-Serve platform.

For its Commerce segment, the company aims to increase GPV by driving higher adoption of Thinkific Commerce, with plans to raise its take rate to 5% in the mid-term through value-added features, and potentially to 10% in the long run. Management also highlighted an opportunity to bring more off-platform transactions (estimated at 50% of total customer sales) onto the platform.

The following strategic roadmap details the company’s growth initiatives across all segments:

For Thinkific Plus, the enterprise segment, the company is investing in go-to-market capabilities and expansion features, including invoicing, subscription management, and improved group orders. The Self-Serve strategy focuses on targeting customers with higher GMV and ARPU potential, while improving activation and ease of use.

Forward-Looking Statements

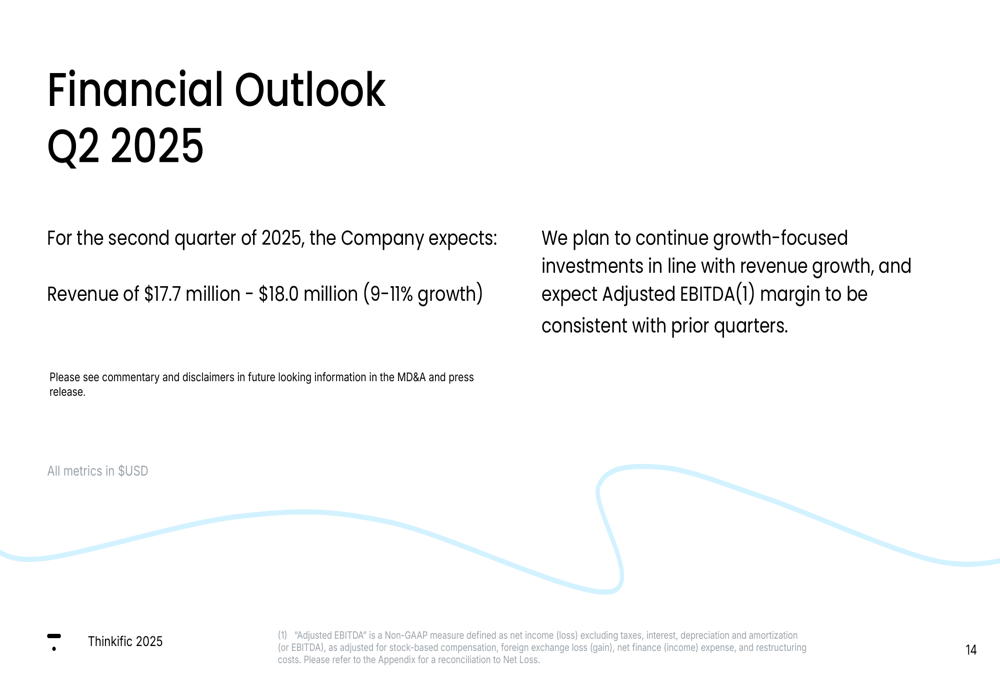

Looking ahead to Q2 2025, Thinkific provided revenue guidance of $17.7-$18.0 million, representing growth of 9-11% year-over-year. This outlook suggests a deceleration from the 12% growth achieved in Q1, which likely contributed to investor concerns.

CEO Greg Smith characterized 2025 as "a year of transformation for Thinkific," noting that the company is "working hard on executing the focused strategy we outlined last call and are gearing up for important product launches and marketing and brand campaigns this summer."

Despite management’s optimism about the company’s strategic direction, the combination of slowing revenue growth, declining GMV, and cautionary language about "headwinds to GMV growth and macroeconomic uncertainty" appears to have overshadowed the positive aspects of the quarter, resulting in the sharp stock price decline.

The market reaction suggests investors may require more concrete evidence that Thinkific’s transformation strategy can successfully address the challenges in its core business before regaining confidence in the company’s growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.