Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

Tidewater Inc. (NYSE:TDW), the world’s largest offshore support vessel (OSV) operator, presented its August 2025 investor update following a strong Q1 performance that saw the company beat earnings expectations with an EPS of $0.83 against a forecast of $0.66. The presentation highlights Tidewater’s strategic positioning in a market characterized by robust offshore spending, limited newbuild activity, and an aging global fleet.

With a market capitalization of $2.4 billion and a stock price that has recently surged 10.55% following its Q1 earnings release, Tidewater continues to capitalize on favorable market dynamics while maintaining a strong balance sheet with approximately $600 million in liquidity and a low leverage ratio of 0.5x Net Debt/2025E EBITDA.

Fleet Strategy & Competitive Position

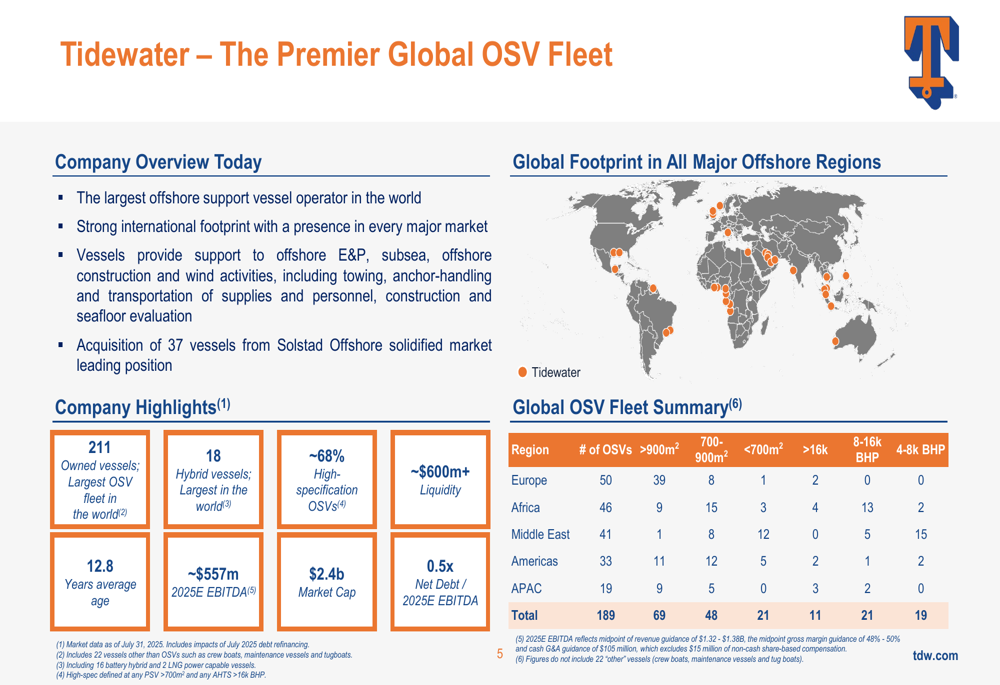

Tidewater has strategically evolved its fleet through targeted acquisitions, adding 83 premier, high-quality vessels via M&A activities. The company now operates 211 owned vessels, including 189 OSVs with an average age of 12.8 years, positioning it as the dominant player in the global OSV market.

As shown in the following comprehensive overview of Tidewater’s current position and fleet composition:

The company’s fleet is heavily weighted toward high-specification vessels, with approximately 68% of its OSVs falling into this category. This strategic focus on modern, capable vessels has been instrumental in driving improved day rates and margins compared to historical peaks.

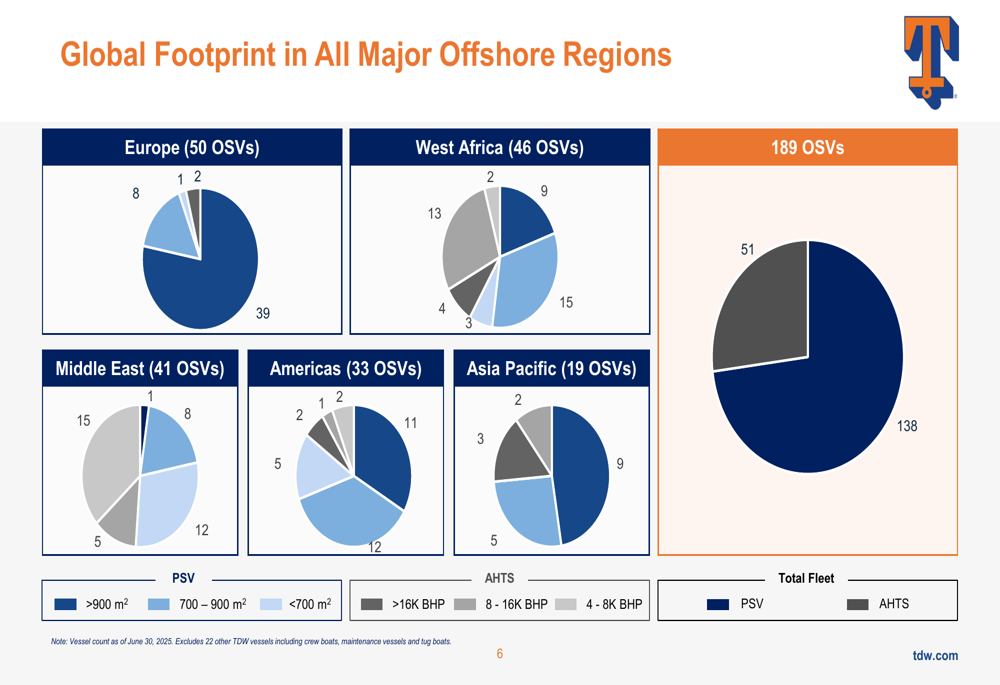

Tidewater’s global footprint spans all major offshore regions, with a balanced distribution of vessels that allows it to serve diverse markets and mitigate regional volatility. The company’s regional presence is visualized in this breakdown:

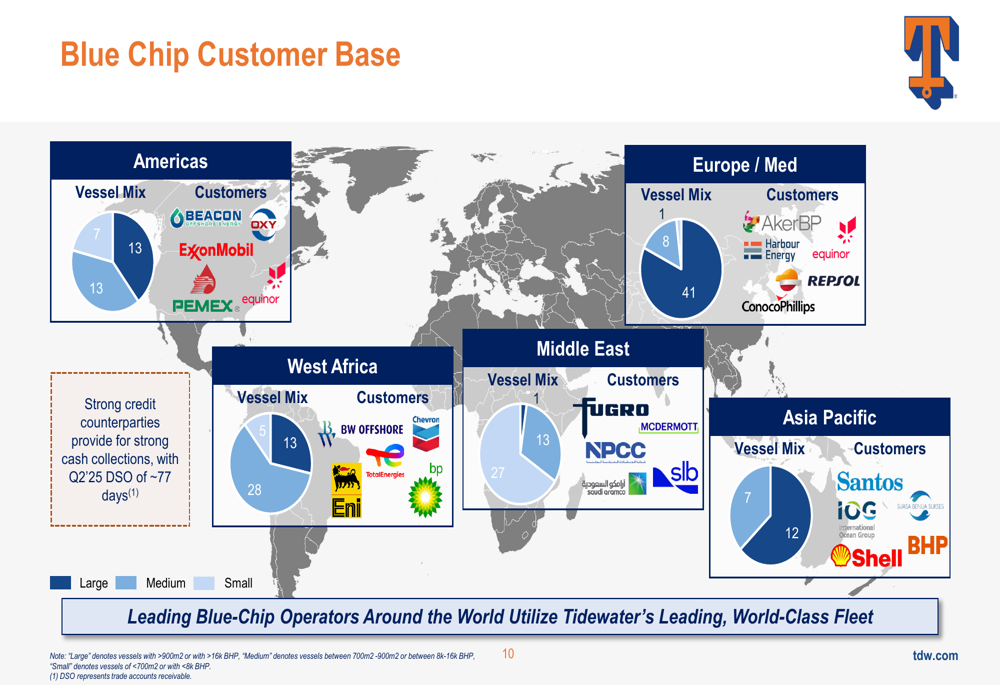

This extensive global reach enables Tidewater to maintain relationships with blue-chip customers across the energy sector, including major operators like ExxonMobil (NYSE:XOM), Equinor, Shell, and Saudi Aramco (TADAWUL:2222). The company’s diverse customer base by region is illustrated here:

Financial Performance & Outlook

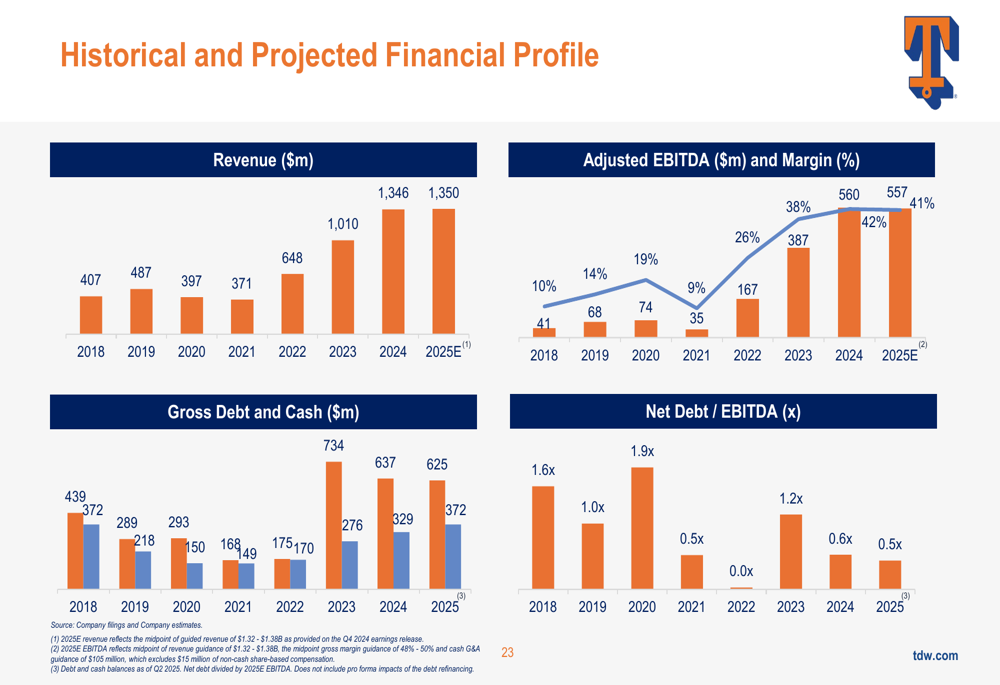

Tidewater’s financial trajectory shows steady improvement, with the company projecting 2025E EBITDA of approximately $557 million. This outlook is supported by the company’s strong Q1 2025 performance, where it reported revenue of $333.4 million and maintained a gross margin above 50% for the second consecutive quarter.

The company’s historical and projected financial profile demonstrates this positive trend:

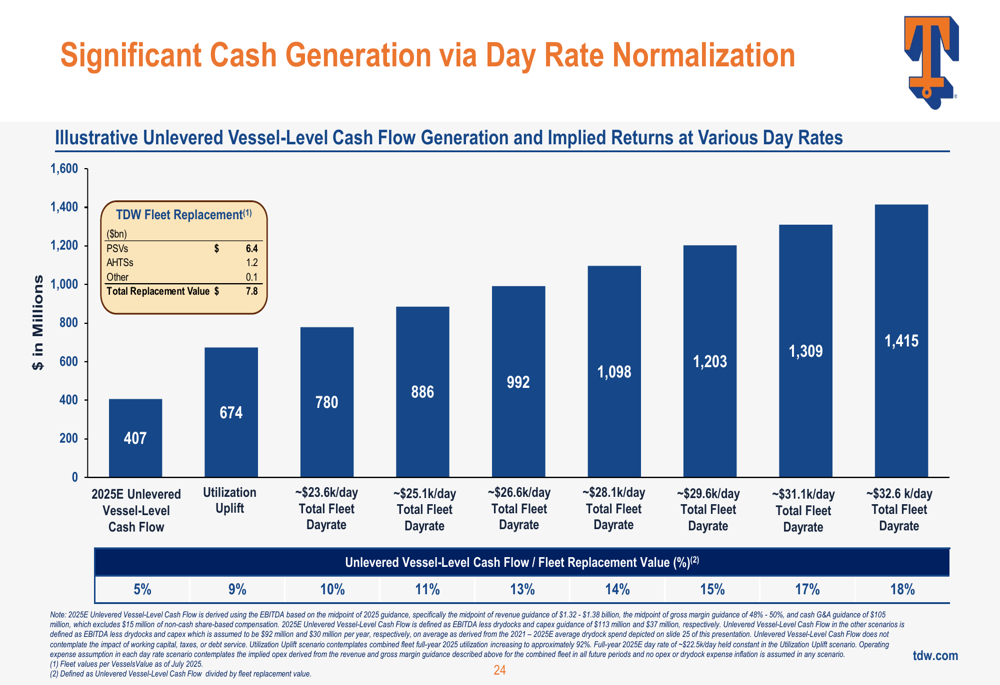

Day rate normalization has been a key driver of Tidewater’s improved financial performance. The company’s presentation illustrates the significant cash generation potential at various day rate levels:

In its Q1 earnings call, Tidewater provided guidance for full-year 2025 revenue between $1.32 billion and $1.38 billion with a gross margin of 48-50%, aligning with the projections shown in the investor presentation. The company noted that 88% of its revenue is supported by firm backlog and options, providing strong visibility for the remainder of the year despite projecting a 5% sequential decline in Q2 revenue.

Market Dynamics Supporting Growth

Several market factors are creating favorable conditions for Tidewater’s continued growth. The offshore market demonstrated robust growth across most major basins in 2024, and the long-term outlook for international and offshore markets remains strong, with global offshore capital commitments expected to rebound meaningfully in 2026.

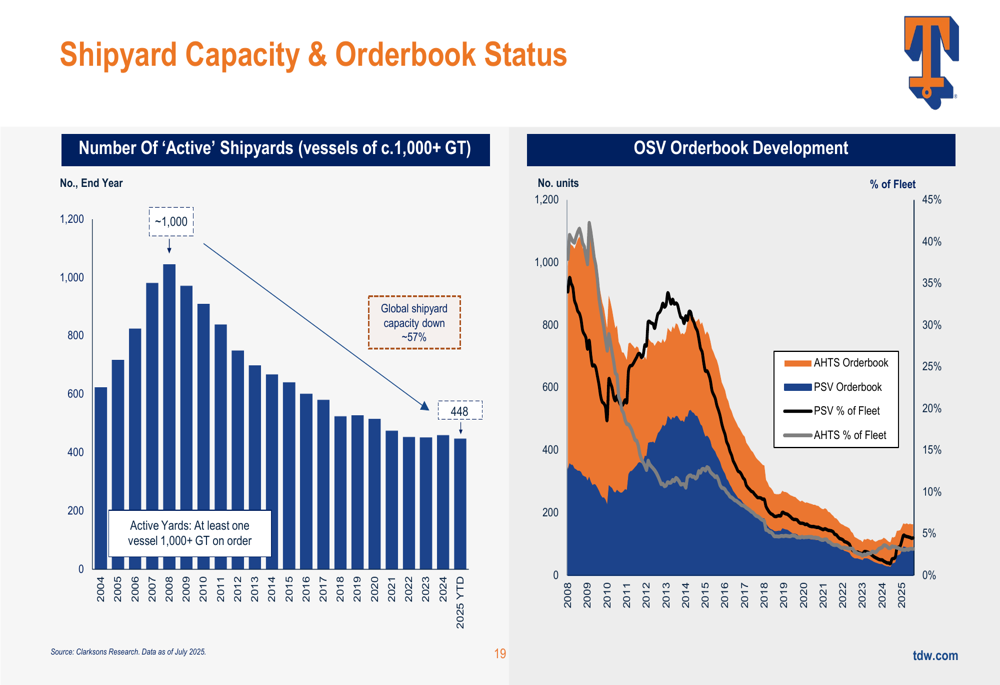

Critically, the supply of OSVs remains constrained due to limited newbuild activity. The economics of newbuilds require an average through-cycle day rate of approximately $44,000 per day to achieve an "NPV Zero" based on a 20-year useful life, significantly above current rates. This economic reality, combined with reduced shipyard capacity and limited debt availability for new construction, has restricted the addition of new vessels to the global fleet.

As shown in this analysis of shipyard capacity and orderbook status:

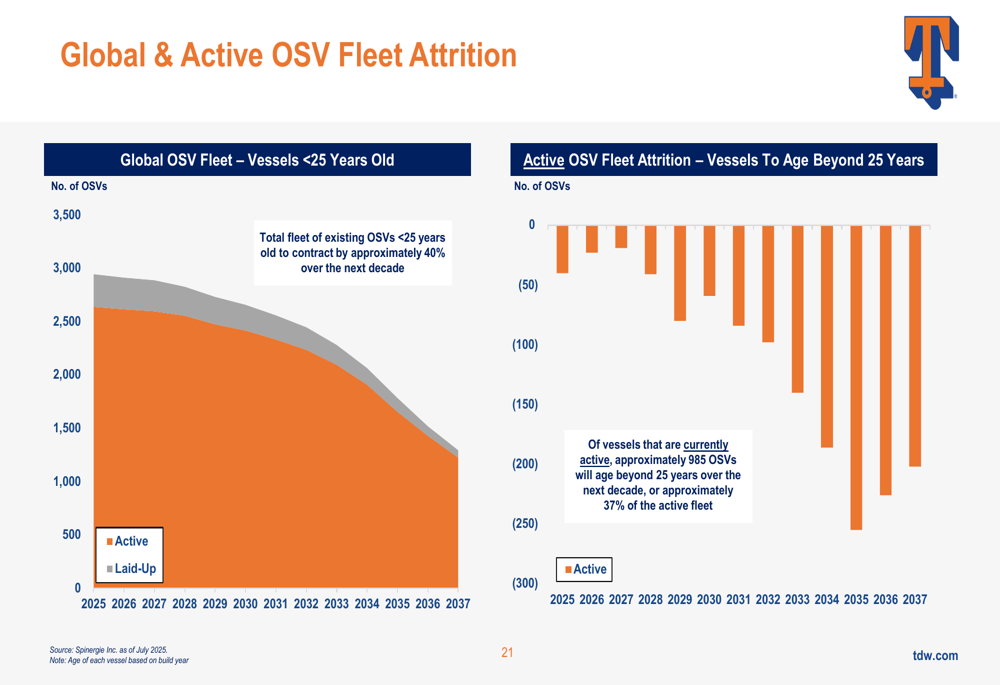

Simultaneously, the global OSV fleet is aging, with 985 vessels expected to exceed 25 years of age over the next decade, potentially leading to increased attrition and further tightening supply:

These market dynamics—robust demand coupled with constrained supply—create a favorable environment for established operators like Tidewater with modern, high-specification fleets.

Sustainability Initiatives

Tidewater has emphasized its commitment to sustainability across environmental, social, and governance dimensions. The company operates the world’s largest fleet of hybrid vessels (18 in total) and has aligned its emissions reduction targets with IMO standards, aiming to reduce well-to-wake CO2-e intensity by 40% by 2030.

The company’s sustainability framework is outlined here:

Safety performance remains a priority, with Tidewater reporting a 10-year average Total (EPA:TTEF) Recordable Case Frequency (TRCF) of 0.59, demonstrating its commitment to maintaining safe operations across its global fleet.

Outlook & Strategic Positioning

Tidewater appears well-positioned to capitalize on favorable market dynamics through 2025 and beyond. The company’s strategic focus on high-specification vessels, global presence, blue-chip customer relationships, and strong balance sheet provide a solid foundation for continued growth.

As summarized in the presentation’s key takeaways:

With day rates continuing to normalize and offshore activity remaining robust, Tidewater’s outlook for the remainder of 2025 appears positive. The company’s CEO, Quentin Neen, expressed during the Q1 earnings call a preference for "value accretive acquisitions," suggesting that further strategic fleet expansion may be on the horizon as the company leverages its strong financial position to consolidate its market leadership.

As offshore energy development continues to expand globally and the supply-demand dynamics for OSVs remain favorable, Tidewater’s position as the world’s largest OSV operator with the highest-specification fleet places it at the forefront of the industry’s growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.