These are top 10 stocks traded on the Robinhood UK platform in July

Titan International Inc. (NYSE:TWI) shared its investor presentation on July 31, 2025, highlighting the company’s strategic transformation, improved financial resilience during industry downturns, and its path toward mid-cycle earnings targets. The presentation comes as Titan’s stock has faced pressure, dropping 6.73% to $8.46 during the trading session, following a 16.87% decline after its Q1 2025 earnings release that showed an EPS miss despite revenue growth.

Executive Summary

Titan International positions itself as a global leader in off-highway tires, wheels, and undercarriage equipment with an enterprise value of $985 million. The company reported trailing twelve-month (TTM) revenues of $1.78 billion as of June 2025, with adjusted EBITDA of $91 million. However, the company faces challenges with negative free cash flow of $12 million and a leverage ratio of 4.4x, with net debt standing at $401 million.

As shown in the following overview of Titan’s business segments and financial metrics:

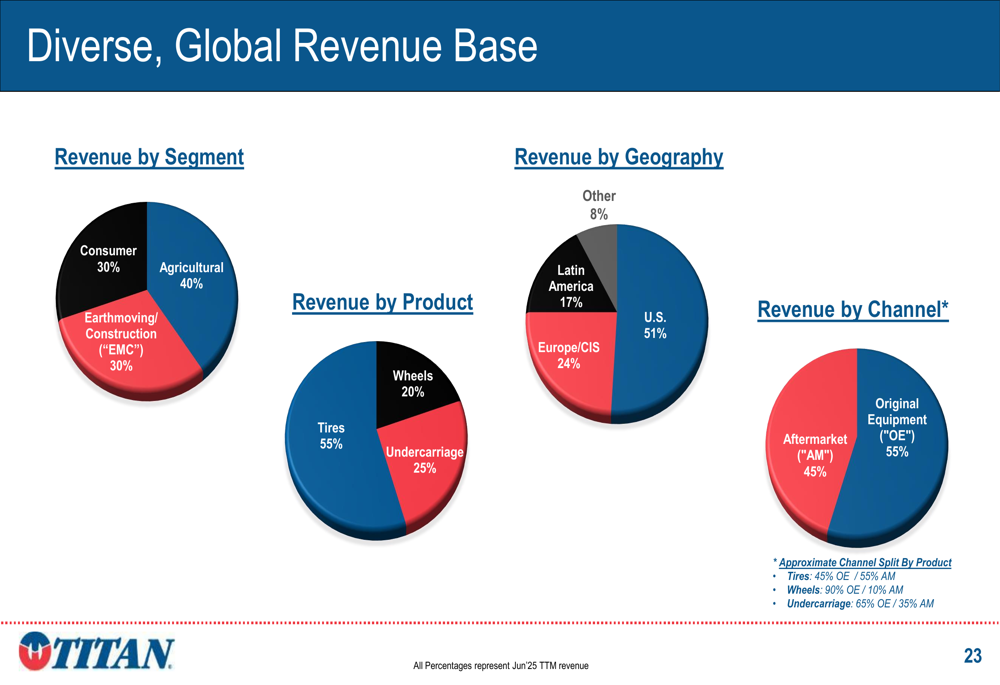

The company’s revenue is diversified across three segments: Agriculture (40%), Earthmoving/Construction (30%), and Consumer (30%). Geographically, Titan generates 51% of revenue from the US, 24% from Europe/CIS, 17% from Latin America, and 8% from other regions.

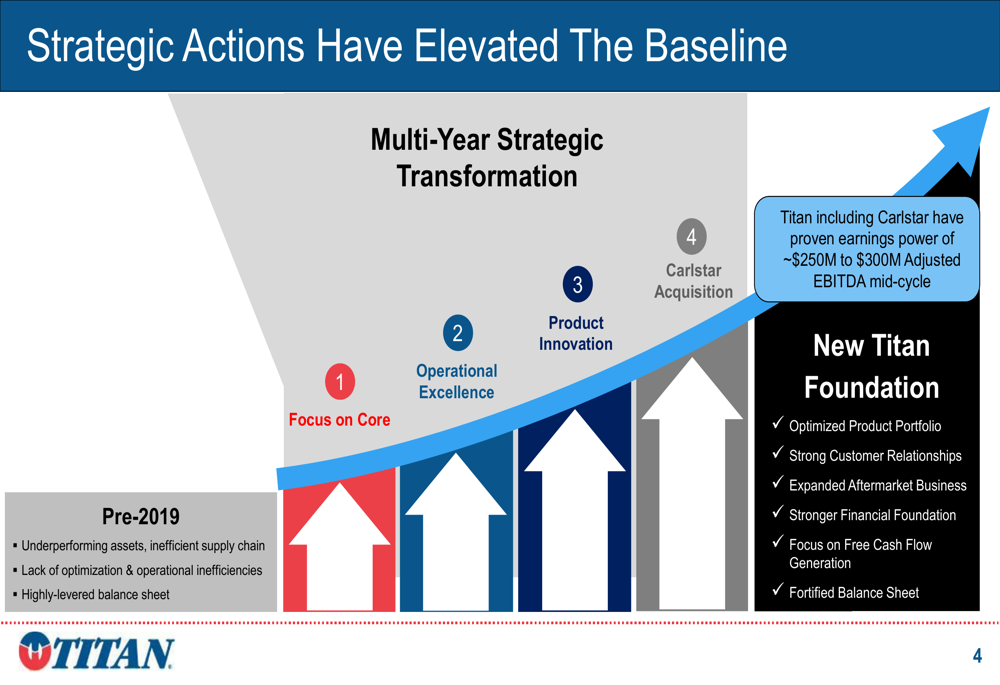

Strategic Transformation

A key focus of the presentation was Titan’s multi-year strategic transformation, which has created what management calls a "New Titan Foundation." The company has shifted from underperforming assets and high leverage to an optimized product portfolio, expanded aftermarket business, and strengthened customer relationships.

The following image illustrates Titan’s strategic transformation journey:

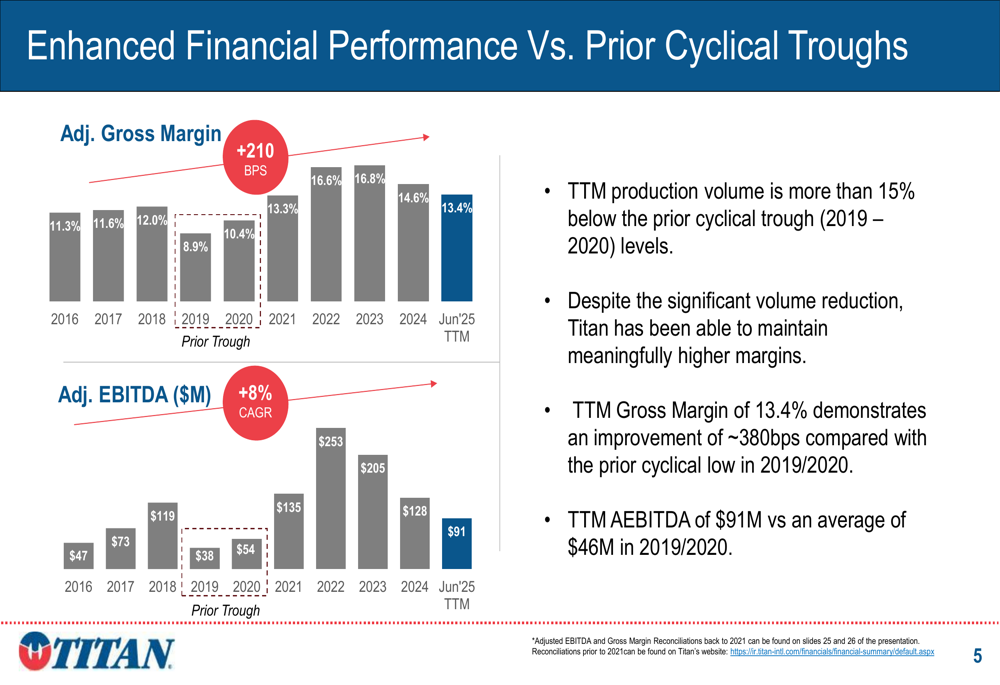

Despite operating in a cyclical trough with production volumes more than 15% below previous cyclical lows (2019-2020), Titan has maintained significantly higher margins. The company’s TTM gross margin of 13.4% represents an improvement of approximately 380 basis points compared to the prior cyclical low, while adjusted EBITDA stands at $91 million versus an average of $46 million in 2019-2020.

This financial resilience through industry cycles is demonstrated in the following chart:

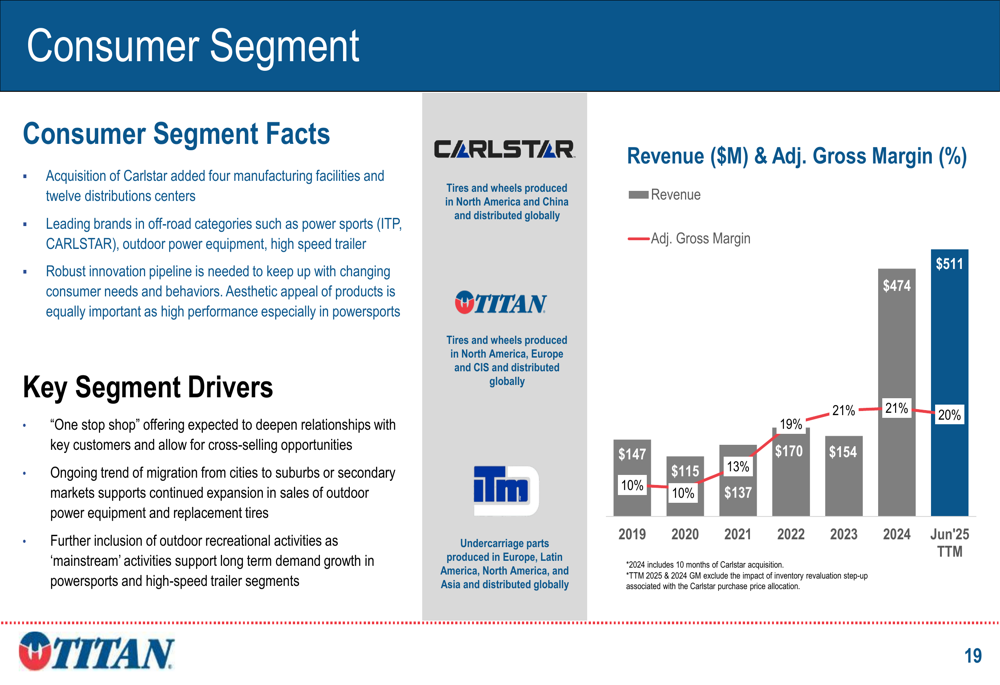

Carlstar Acquisition Impact

A significant development in Titan’s strategy has been the acquisition of Carlstar, which has substantially expanded the company’s consumer segment. The acquisition has diversified Titan’s revenue streams and created synergy opportunities across commercial, procurement, manufacturing, and distribution operations.

The impact of this acquisition is particularly evident in the consumer segment’s financial performance, where revenue jumped to $511 million (TTM Jun’25) while maintaining strong gross margins of 20%:

Titan expects to realize synergies from the Carlstar acquisition of $6 million in FY2024, an incremental $7-9 million in FY2025, and a long-term target of $25-30 million. These synergies are expected to contribute to the company’s path toward higher mid-cycle earnings.

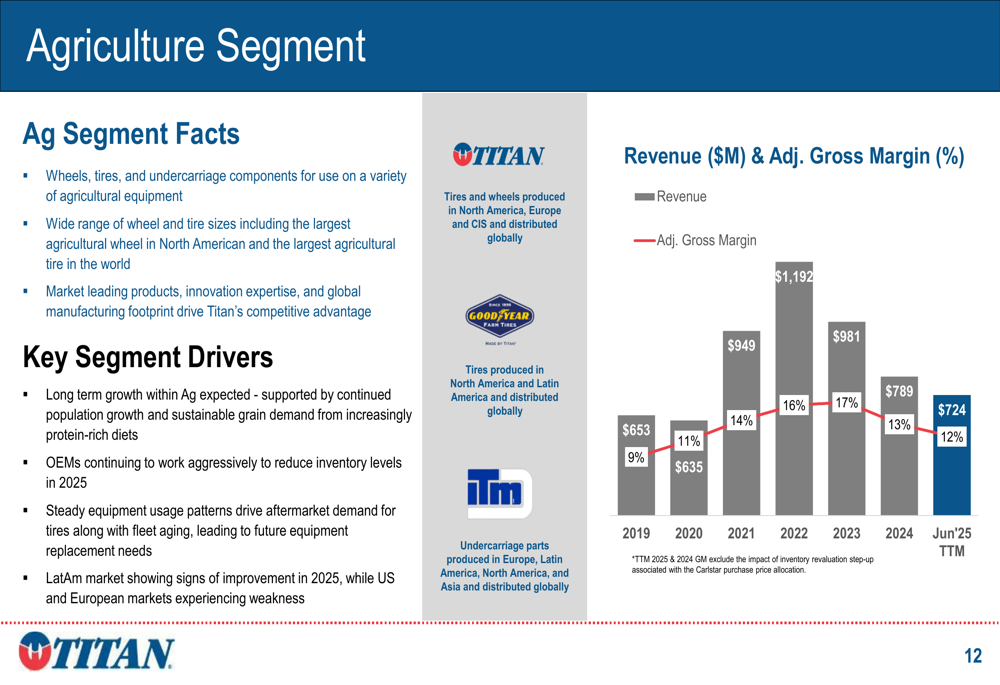

Segment Performance Analysis

Titan’s agricultural segment, which represents 40% of total revenue, has seen declining performance from its peak. Revenue has fallen from $1,192 million to $724 million (TTM Jun’25), with adjusted gross margins dropping from 17% to 12%:

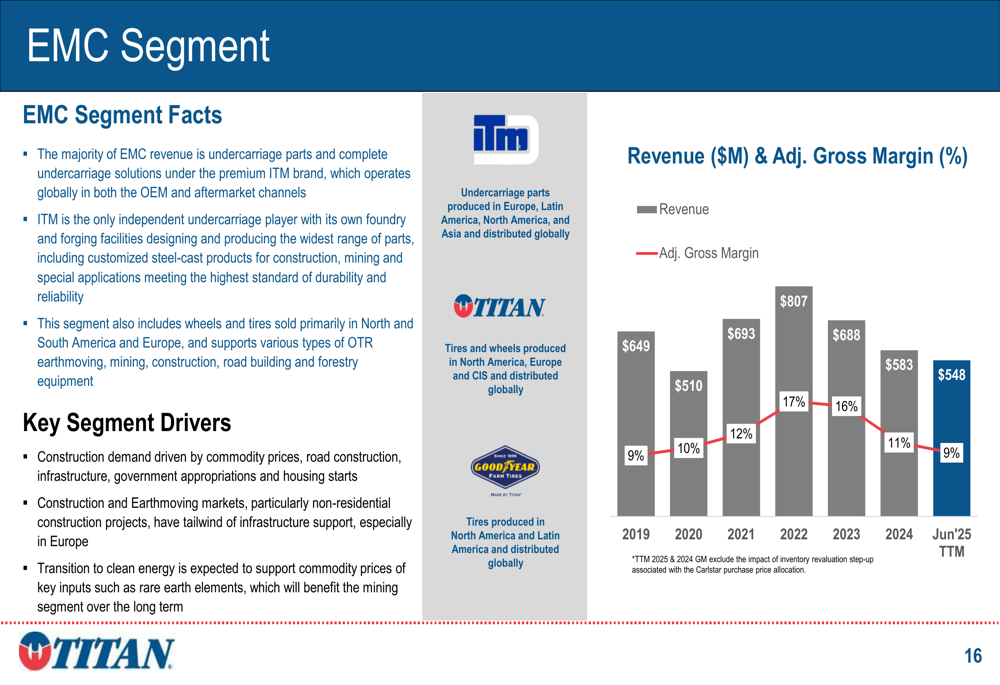

Similarly, the Earthmoving/Construction segment has experienced declining revenue and margins, with revenue falling from a peak of $807 million to $548 million (TTM Jun’25) and adjusted gross margins declining from 17% to 9%:

These segment trends reflect the cyclical challenges facing Titan’s core markets, though management emphasizes that the company’s improved operational efficiency has allowed it to maintain better margins than in previous downturns.

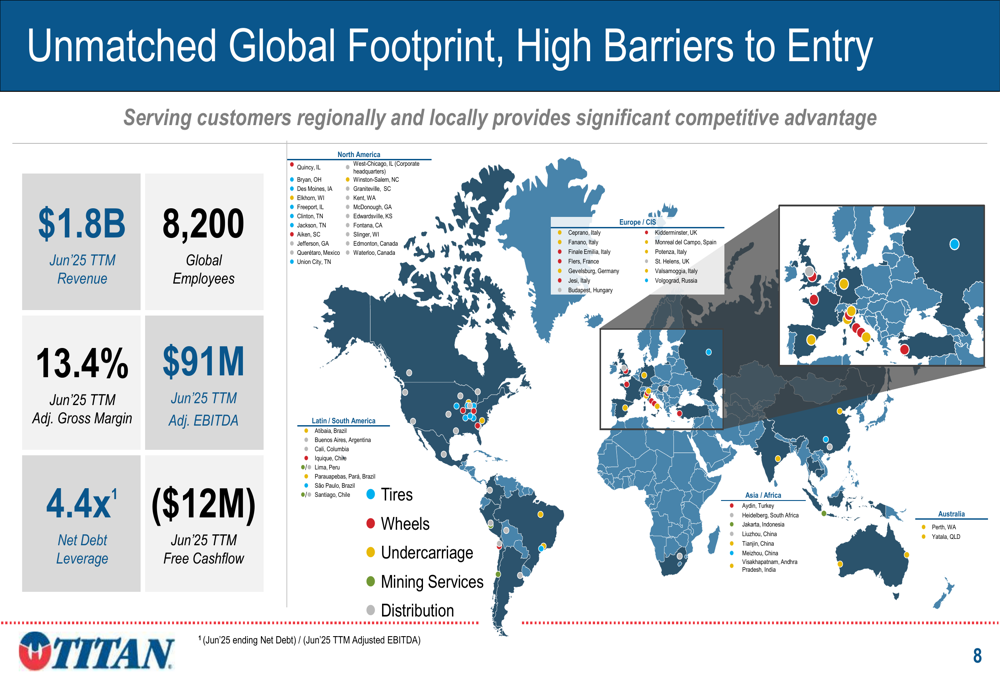

Global Footprint and Competitive Position

Titan highlighted its extensive global footprint as a competitive advantage, with manufacturing facilities, distribution centers, and sales offices across multiple continents. The company employs approximately 8,200 people globally.

The following world map illustrates Titan’s global presence:

This global reach allows Titan to serve diverse markets and customers, with revenue well-balanced between original equipment (55%) and aftermarket (45%) channels. The company maintains long-standing relationships with blue-chip OEM customers and has globally recognized brands in its portfolio.

Path to Mid-Cycle EBITDA Target (NYSE:TGT)

Despite current challenges, Titan outlined a path to achieving $250 million in mid-cycle adjusted EBITDA. This target is based on two components: a return to mid-cycle volumes (contributing approximately $125 million in EBITDA) and synergies plus growth initiatives (contributing approximately $25 million in EBITDA).

The company is focusing on several organic growth strategies, including strategic supplier sourcing, M&A revenue synergies, product development, and increased penetration of its Low Sidewall Technology (LSW). Titan also continues to invest in product innovation across all segments, as illustrated in the following slide:

Market Context and Outlook

Titan’s presentation comes amid challenging market conditions. The company’s Q1 2025 earnings revealed mixed results, with revenue of $491 million exceeding forecasts but earnings per share of $0.01 falling short of the expected $0.04. For Q2 2025, Titan projects revenue between $450 million and $500 million, with adjusted EBITDA guidance of $25 million to $35 million.

The company’s stock has been under pressure, trading near its 52-week low of $5.93, reflecting investor concerns about the high leverage ratio and negative free cash flow. However, management expressed confidence in improved cash flow in the latter half of the year and emphasized the company’s strategic positioning across all three segments.

Titan’s revenue diversification across segments, geographies, and channels provides some resilience against market fluctuations:

While Titan faces near-term challenges with high debt levels and cyclical market pressures, the company’s presentation emphasizes its improved operational efficiency, strategic transformation, and potential for stronger performance as markets recover. Investors will be watching closely to see if Titan can execute on its synergy targets from the Carlstar acquisition and navigate the current industry trough while maintaining its improved margin profile.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.