Intel surges more than 8% after chipmaker’s profits top expectations

Introduction & Market Context

T-Mobile US Inc. (NASDAQ:TMUS) released its third-quarter 2025 results on October 23, showcasing record customer growth that prompted the company to raise its guidance across multiple metrics. Despite these achievements, the stock fell 2.2% in regular trading following the announcement, after declining 0.89% in premarket activity, suggesting investors may have expected even stronger results or were concerned about the slight year-over-year decline in net income.

The telecommunications giant reported earnings per share of $2.41, marginally above analysts’ expectations of $2.40, while revenue reached $21.96 billion, exceeding forecasts of $21.88 billion. These results highlight T-Mobile’s continued momentum in the competitive wireless market, even as the company navigates leadership changes with incoming CEO Srini Gopalan set to replace outgoing CEO Mike Sievert.

Quarterly Performance Highlights

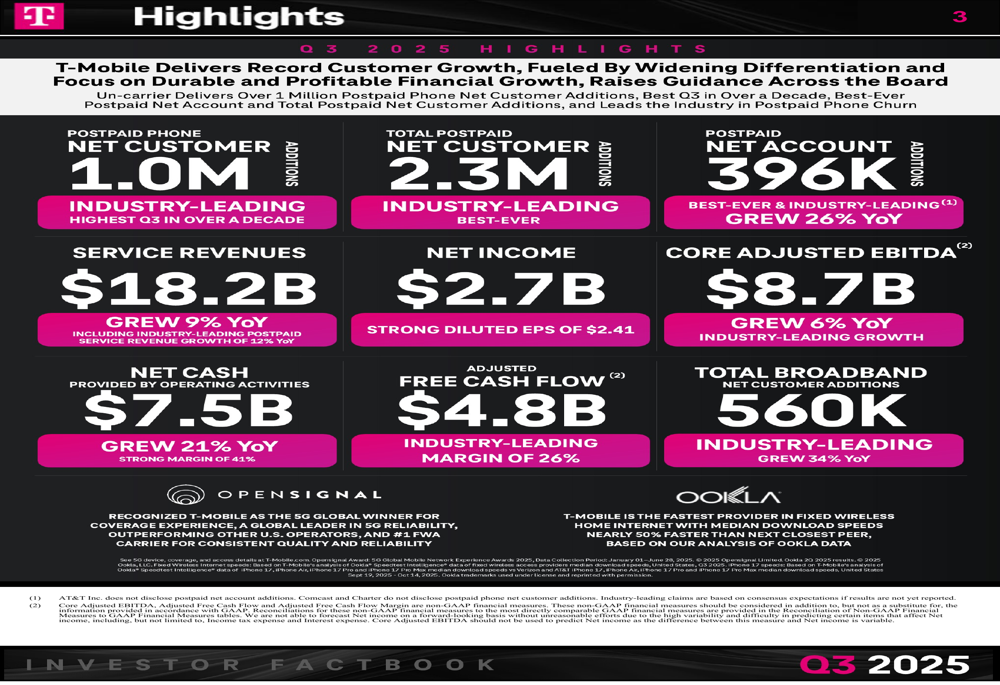

T-Mobile’s Q3 2025 performance was marked by exceptional customer growth across multiple segments. The company achieved 1.0 million postpaid phone net customer additions, its highest Q3 result in over a decade, while total postpaid net customer additions reached a record 2.3 million.

As shown in the following comprehensive overview of key Q3 metrics:

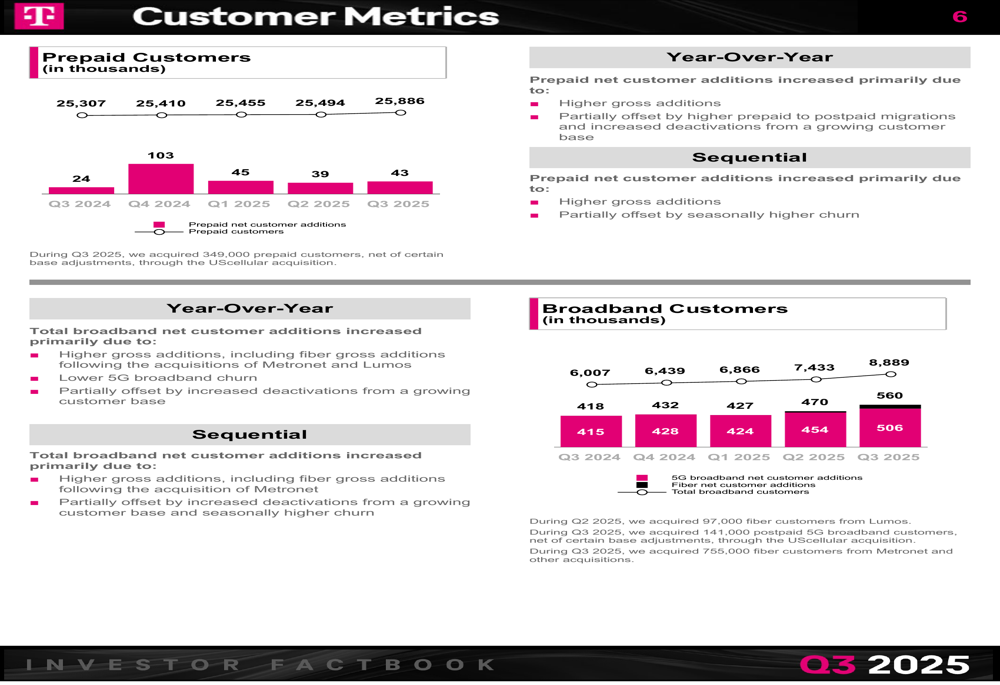

Particularly notable was the 26% year-over-year growth in postpaid net account additions, which reached 396,000 – another record for the company. T-Mobile also continued its strong performance in the broadband segment, with 560,000 net customer additions representing 34% growth compared to the same period last year.

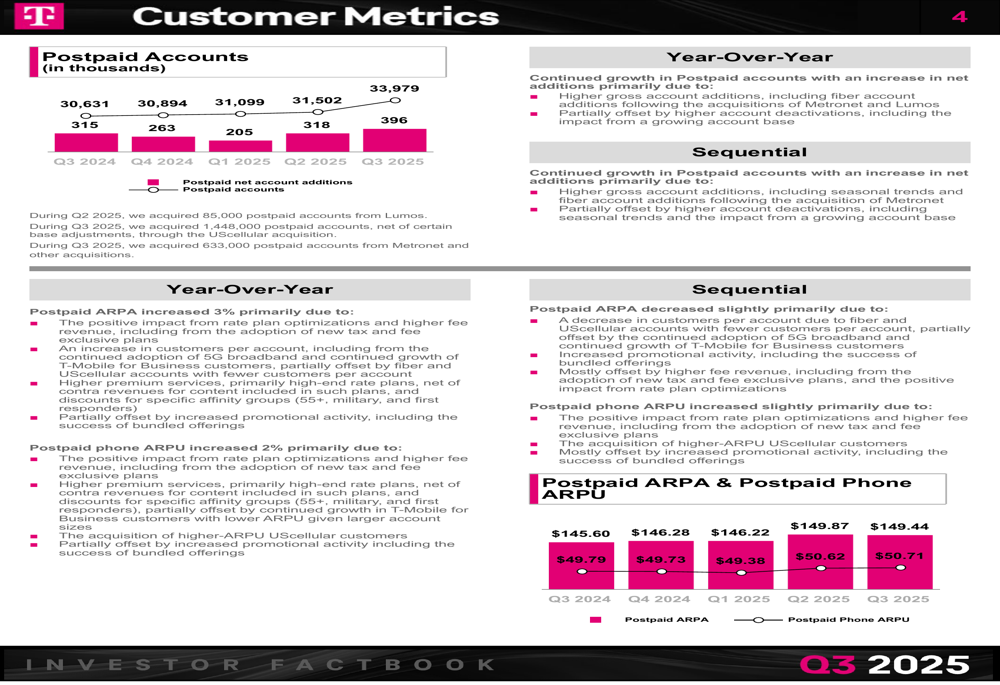

The company’s postpaid accounts have shown consistent growth over the past five quarters, increasing from 30.6 million in Q3 2024 to nearly 34 million in Q3 2025, while maintaining stable ARPU metrics:

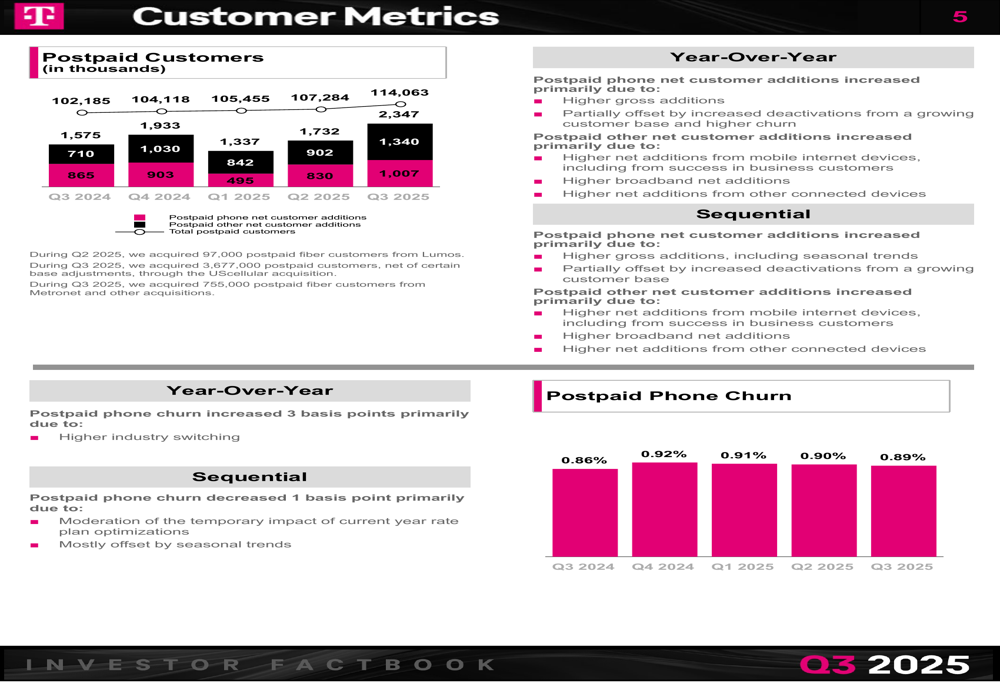

Customer retention remained strong, with postpaid phone churn improving slightly to 0.89% from 0.90% in the previous quarter, though slightly higher than the 0.86% reported in Q3 2024. This stable churn rate, combined with strong customer additions, underscores T-Mobile’s competitive positioning in the market.

Detailed Financial Analysis

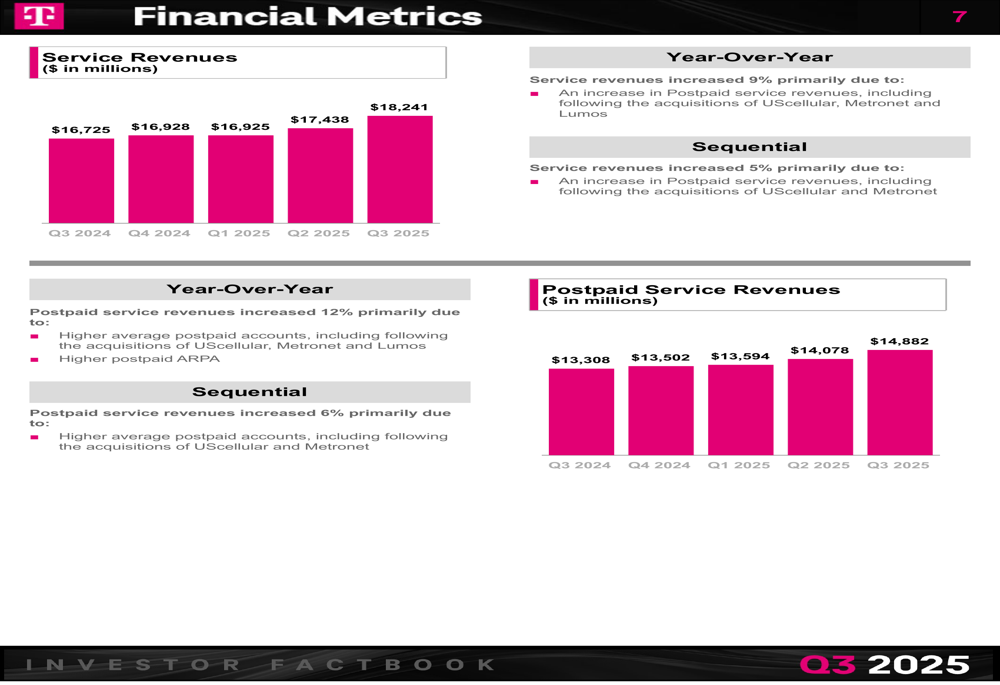

T-Mobile’s financial performance in Q3 2025 was highlighted by robust service revenue growth of 9% year-over-year, reaching $18.2 billion. Particularly impressive was the 12% year-over-year growth in postpaid service revenue, which the company claimed was industry-leading.

The following chart illustrates this consistent upward trajectory in service revenues:

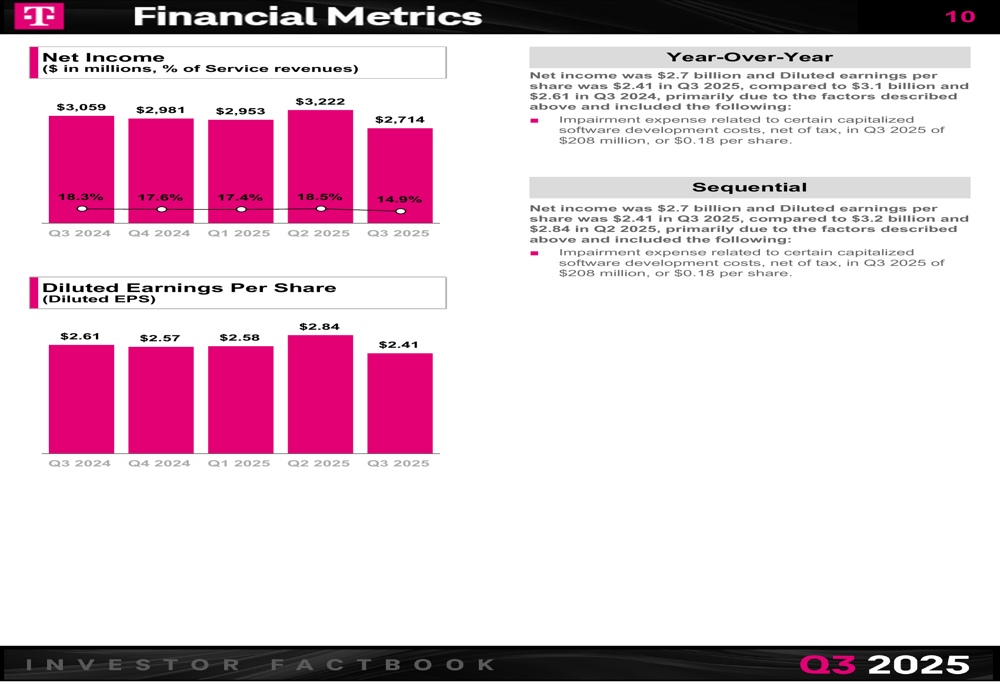

Despite strong revenue performance, T-Mobile’s net income decreased year-over-year from $3.06 billion to $2.71 billion, with diluted earnings per share declining from $2.61 to $2.41. This 11% decrease in net income occurred despite the 9% increase in service revenues, suggesting some pressure on margins.

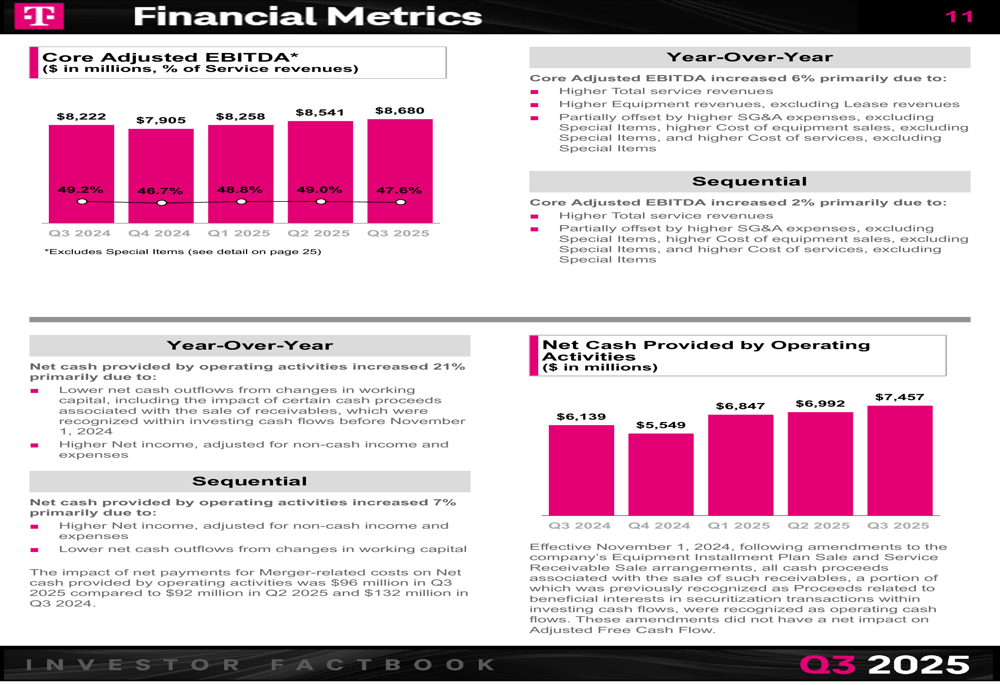

However, Core Adjusted EBITDA showed continued strength, growing 6% year-over-year to $8.68 billion. The company also reported significant improvement in cash flow metrics, with net cash provided by operating activities increasing 21% year-over-year to $7.46 billion.

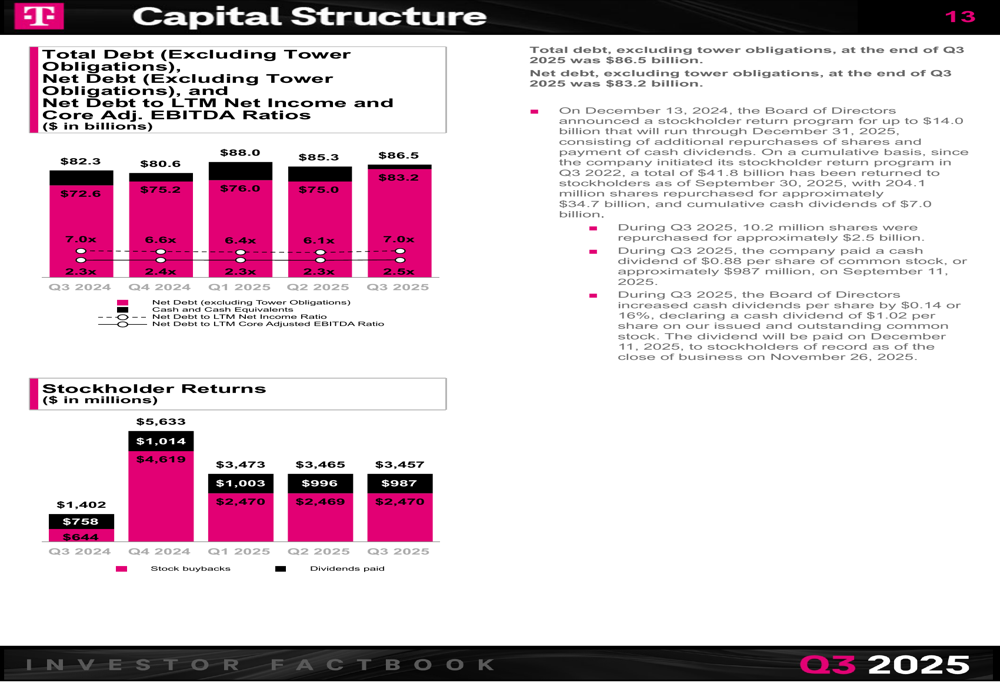

T-Mobile maintained its commitment to shareholder returns, with $987 million in dividends paid and $3.46 billion in stock buybacks during Q3 2025. The company’s capital structure remained relatively stable, though net debt to LTM Core Adjusted EBITDA ratio increased slightly to 2.5x from 2.3x a year earlier.

Strategic Initiatives

T-Mobile continues to emphasize its network leadership as a key competitive advantage. The company highlighted recognition from OpenSignal as the "5G Global Winner for Coverage Experience" and a "Global Leader in 5G Reliability." Additionally, Ookla recognized T-Mobile as the fastest provider in fixed wireless home internet, with median download speeds nearly 50% faster than its closest competitor.

The broadband segment represents an increasingly important growth vector for T-Mobile, with total broadband customers reaching 8.9 million in Q3 2025, up from 6.0 million a year earlier. This nearly 50% year-over-year increase demonstrates the company’s successful expansion beyond its traditional wireless business.

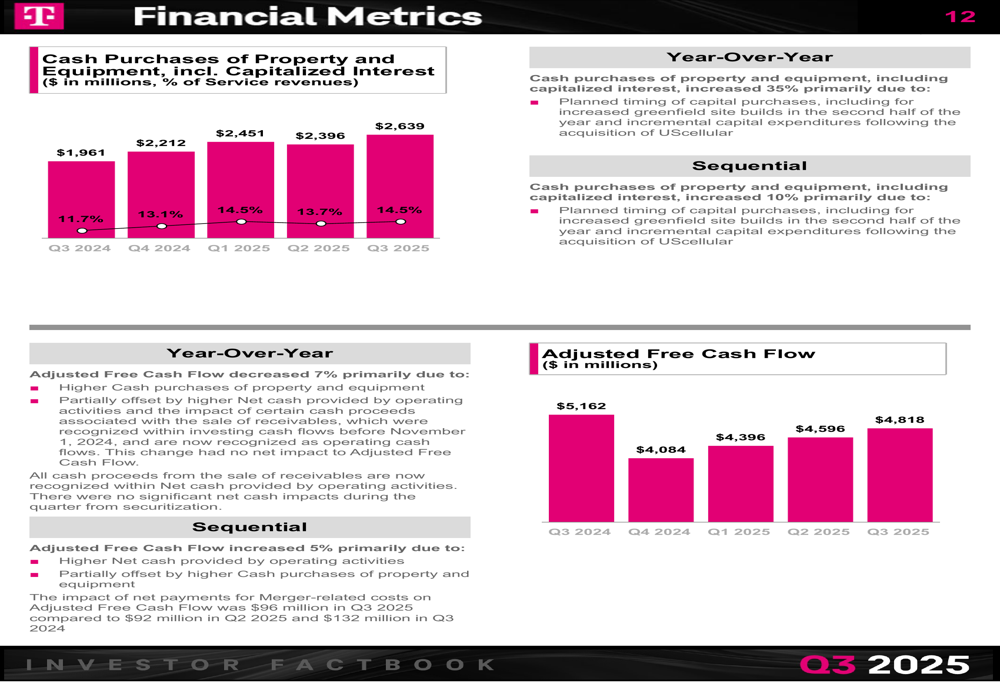

To support this growth, T-Mobile is increasing its capital expenditures, with cash purchases of property and equipment rising to $2.64 billion in Q3 2025, representing 14.5% of service revenues. This investment reflects the company’s commitment to maintaining its network leadership position while expanding into new service areas.

Forward-Looking Statements

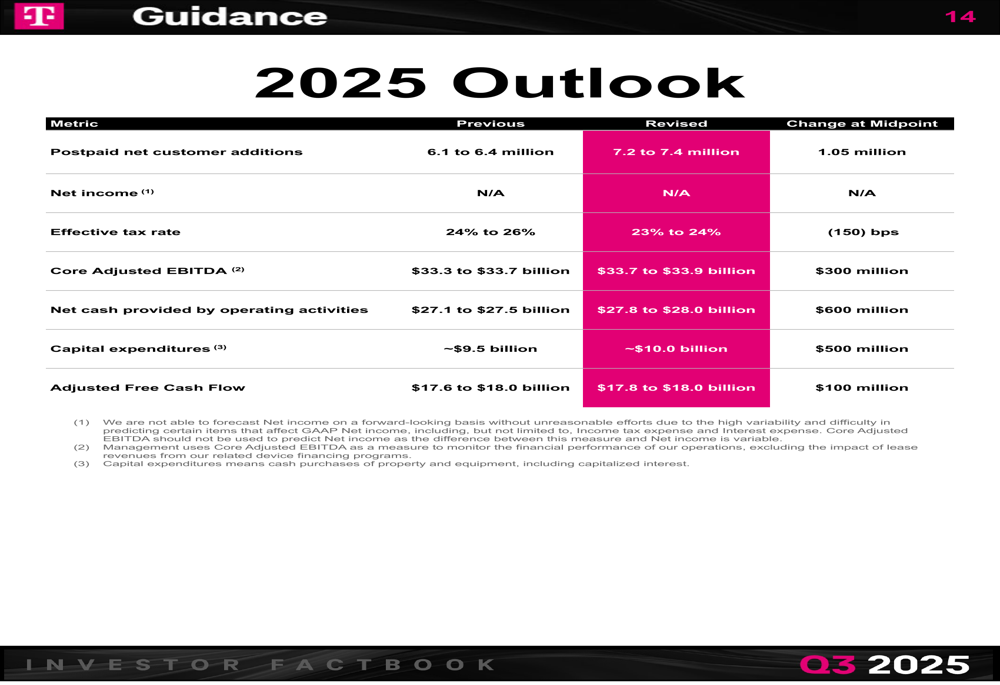

Based on its strong Q3 performance, T-Mobile raised its guidance across multiple metrics for the full year 2025. Most notably, the company increased its forecast for postpaid net customer additions from 6.1-6.4 million to 7.2-7.4 million, representing a substantial increase of 1.05 million at the midpoint.

The following table details T-Mobile’s revised guidance across key metrics:

Core Adjusted EBITDA guidance was raised by $300 million at the midpoint to $33.7-33.9 billion, while net cash provided by operating activities guidance was increased by $600 million at the midpoint to $27.8-28.0 billion. The company also raised its capital expenditure forecast from approximately $9.5 billion to approximately $10.0 billion, reflecting increased investment to support its growing customer base and network expansion.

During the earnings call, executives expressed confidence in T-Mobile’s competitive positioning, with incoming CEO Srini Gopalan stating, "Our differentiation is only widening," and outgoing CEO Mike Sievert adding, "We have never been more successful." However, the company did acknowledge ongoing merger-related costs, estimated at approximately $300 million for Q4 2025, as it continues to integrate UScellular operations.

Despite the slight decline in net income and EPS, T-Mobile’s record customer growth and raised guidance suggest management remains confident in the company’s trajectory for the remainder of 2025 and beyond. The market’s negative reaction may reflect concerns about increased capital expenditures or potential margin pressure, but the fundamental growth story appears intact based on the company’s presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.