Street Calls of the Week

TOMRA Systems ASA (OB:TOM) reported stable overall performance in its Q2 2025 results presentation on July 17, despite facing challenges in some business segments. While the company maintained its adjusted EBITA at 44 million euros, matching the year-ago period, total revenues dipped slightly to 325 million euros from 333 million euros in Q2 2024. The company’s stock had already declined 1.77% to 160.8 Norwegian kroner on the day before the presentation.

Quarterly Performance Highlights

TOMRA’s Q2 2025 results revealed a stable gross margin of 44%, unchanged from the same period last year, while operating expenses decreased slightly to 100 million euros from 101 million euros. The company reported a positive special items effect of 3.7 million euros from its Food cost savings program, compared to a negative 0.5 million euros in Q2 2024.

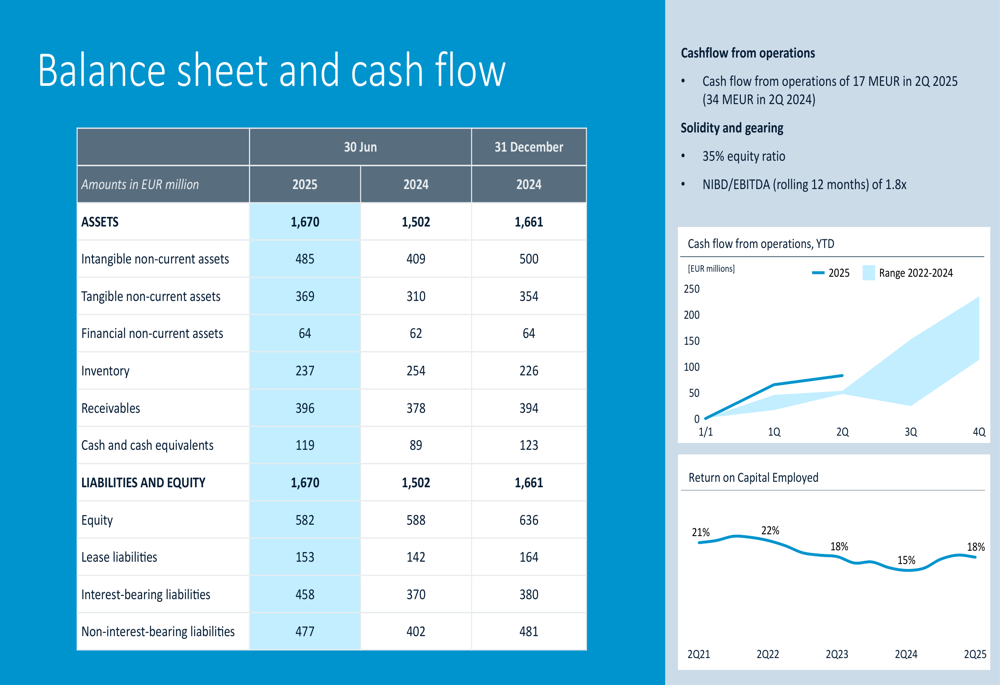

However, cash flow from operations declined significantly to 17 million euros, compared to 34 million euros in the second quarter of 2024.

As shown in the following financial highlights:

Divisional Analysis

The company’s performance varied significantly across its three main business divisions, with the Food segment emerging as the clear standout performer.

Collection Division

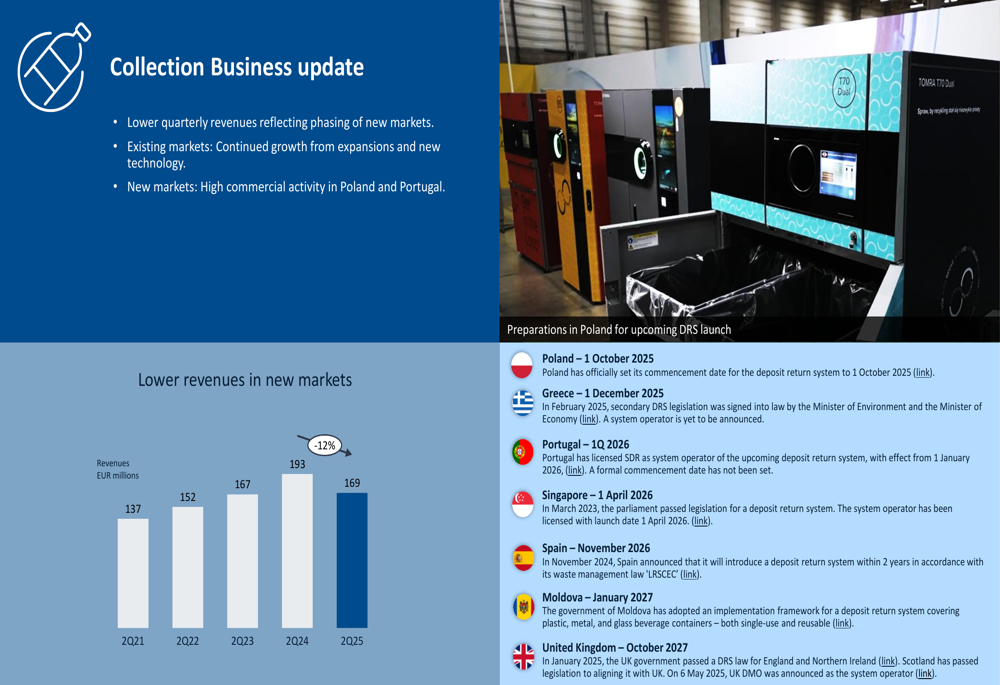

TOMRA’s Collection division, which handles reverse vending machines for container deposit systems, reported lower quarterly revenues of 169 million euros, down 12% from 193 million euros in Q2 2024. This decline primarily reflects the phasing of new markets, while existing markets continued to show growth from expansions and new technology.

The division maintained its EBITA margin at 16% despite the revenue decline, with absolute EBITA falling to 27 million euros from 32 million euros in Q2 2024.

As shown in the following Collection business update:

The company highlighted high commercial activity in preparation for upcoming Deposit Return System (DRS) launches in several countries, including Poland (October 2025), Greece (December 2025), Portugal (Q1 2026), and others extending through 2027.

Recycling Division

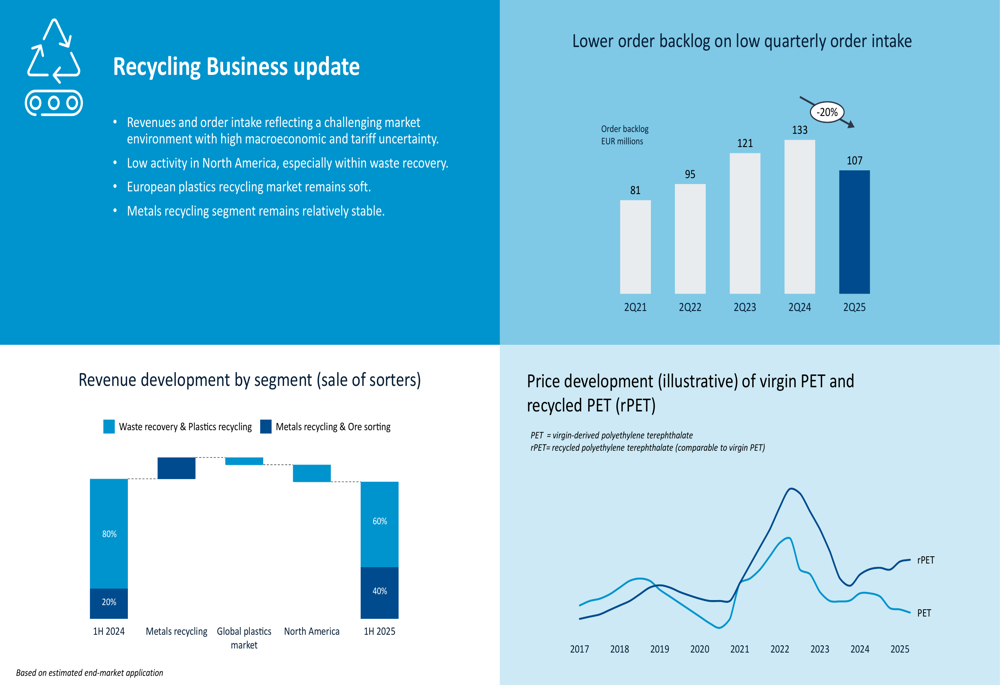

The Recycling division faced the most significant challenges, with revenues flat at 57 million euros but EBITA declining to 6 million euros from 10 million euros in Q2 2024. The division’s EBITA margin contracted to 11% from 17% a year earlier.

Order intake fell sharply to 41 million euros from 65 million euros in Q2 2024, while the order backlog declined 20% to 107 million euros.

As illustrated in the Recycling business update:

TOMRA cited continued uncertainty due to macroeconomic factors and tariffs, along with a soft European plastics recycling market. The division experienced low activity in North America, especially within waste recovery, while the metals recycling segment remained relatively stable.

Food Division

The Food division delivered exceptional results, with revenues increasing to 94 million euros from 82 million euros in Q2 2024. Adjusted EBITA more than doubled to 17 million euros from 8 million euros, resulting in an improved margin of 18% compared to 10% a year earlier.

Order intake surged 28% to a record 106 million euros, while the order backlog grew to 137 million euros from 119 million euros in Q2 2024.

The following Food business update highlights this strong performance:

TOMRA reported improving market sentiment with strong order intake across all regions, including large orders in several categories such as Citrus, Avocados, and Potatoes. This performance builds on the positive trend seen in Q1 2025, when the Food division reported its first positive EBITDA for a first quarter.

Financial Position

TOMRA maintained a solid financial position with an equity ratio of 35% and a net interest-bearing debt to EBITDA ratio of 1.8x on a rolling 12-month basis. The company received an A- credit rating from Scope Ratings in June 2025.

The balance sheet showed total assets of 1,670 million euros as of Q2 2025, up from 1,502 million euros in Q2 2024. Interest-bearing liabilities increased to 458 million euros from 370 million euros a year earlier.

As shown in the following balance sheet and cash flow summary:

Forward-Looking Statements

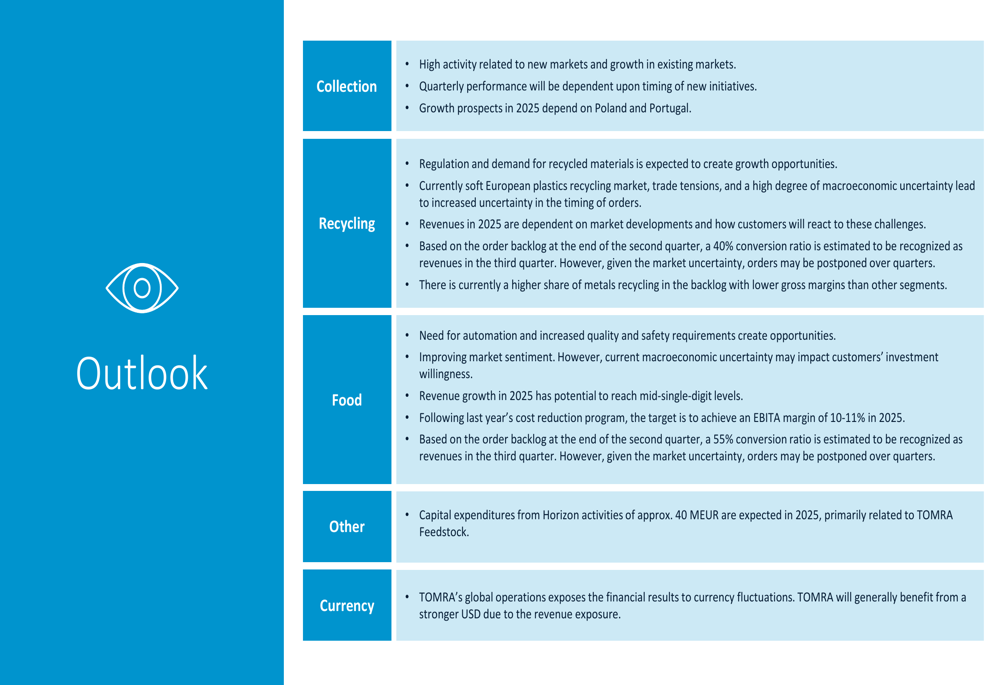

TOMRA provided a detailed outlook for each of its business segments, highlighting both opportunities and challenges ahead.

For the Collection division, the company expects high activity related to new markets and continued growth in existing markets, with quarterly performance dependent on the timing of new initiatives. Growth prospects for 2025 will largely depend on developments in Poland and Portugal.

In the Recycling segment, TOMRA acknowledged the current challenges but maintained that regulation and demand for recycled materials should create growth opportunities over time. Based on the current order backlog, the company estimates a 40% conversion ratio to be recognized as revenues in the third quarter.

The Food division outlook remains positive, with revenue growth potential in the mid-single-digit range for 2025. Following last year’s cost reduction program, TOMRA targets an EBITA margin of 10-11% for this division in 2025, with approximately 55% of the current order backlog expected to convert to revenue in Q3.

As detailed in the company’s outlook:

TOMRA also noted that capital expenditures from Horizon activities of approximately 40 million euros are expected in 2025, primarily related to TOMRA Feedstock. The company’s global operations expose its financial results to currency fluctuations, with TOMRA generally benefiting from a stronger USD due to its revenue exposure.

This Q2 2025 presentation follows TOMRA’s Q1 results, which showed a 5% year-over-year revenue increase and improved gross margins. While the Food division continues its strong trajectory, the challenges in the Recycling division appear to have intensified since the first quarter report.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.