European stocks mixed on Friday after volatile week; U.K. economic woes

Introduction & Market Context

TOMRA Systems ASA (OB:TOM) presented its second quarter 2025 results on July 17, showcasing a period of mixed performance across its business segments. The company reported a slight revenue decline of 2% year-over-year to €325 million, as strong growth in its Food segment was offset by weakness in Collection. TOMRA's stock has been under pressure recently, trading near its 52-week low at 141.5 NOK, down 1.2% following the earnings release.

The company operates in a complex market environment characterized by regional variations and regulatory developments. TOMRA continues to position itself for future growth through expansion into new deposit return systems (DRS) markets while navigating macroeconomic uncertainties and tariff challenges.

Quarterly Performance Highlights

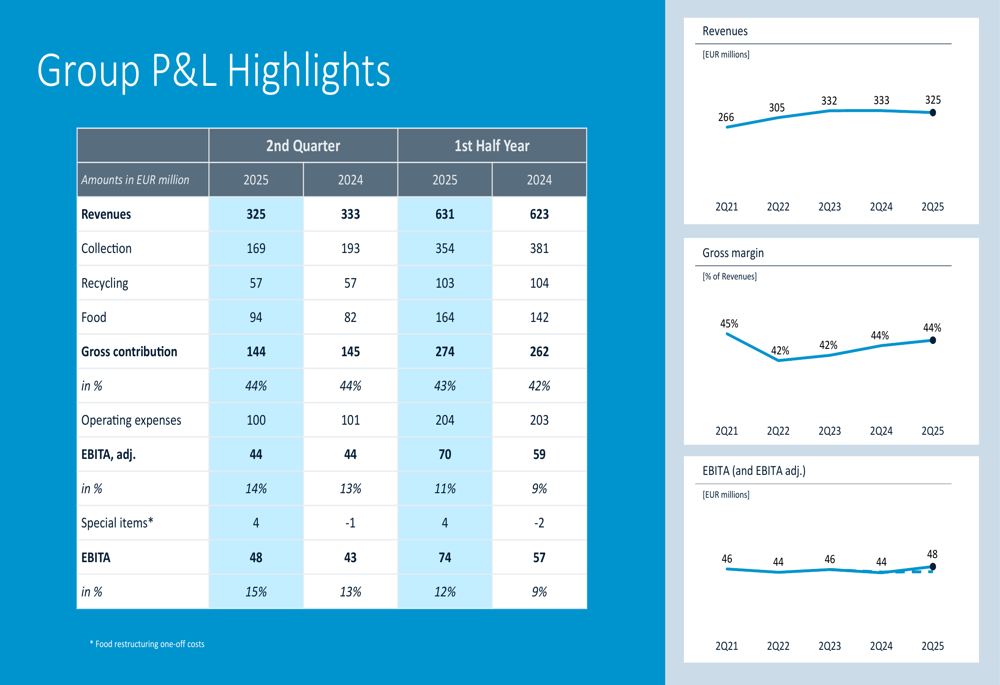

TOMRA's Q2 2025 financial results showed resilience despite challenging market conditions. Total revenues reached €325 million, down 2% compared to Q2 2024. The company maintained a gross margin of 44% and delivered adjusted EBITA of €44 million, unchanged from the previous year. Cash flow from operations was €17 million, down from €34 million in the same period last year.

As shown in the following financial highlights:

The company's performance varied significantly across segments, with Collection experiencing a 12% revenue decline while Food delivered record results. Special items included a €3.7 million positive effect from the Food cost savings program, contributing to an overall EBITA of €48 million when including these items.

The detailed profit and loss statement further illustrates the company's performance:

Segment Analysis

Collection

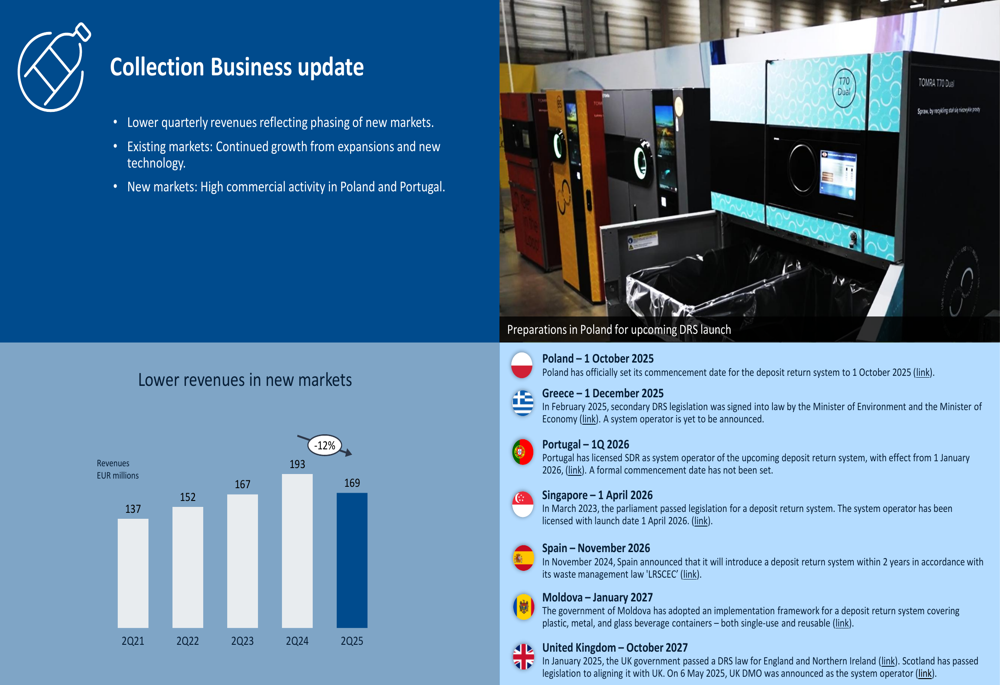

TOMRA's Collection segment faced headwinds in Q2 2025, with revenues declining 12% year-over-year to €169 million. This decrease primarily reflects the phasing of new markets, though the company continues to see growth from expansions and new technology in existing markets.

The segment breakdown shows high commercial activity in Poland and Portugal as these countries prepare for upcoming DRS launches:

Despite the revenue decline, TOMRA remains optimistic about the Collection segment's prospects, highlighting ongoing preparations for DRS implementations in Greece, Portugal, Singapore, Spain, Moldova, and the United Kingdom over the coming years.

Recycling

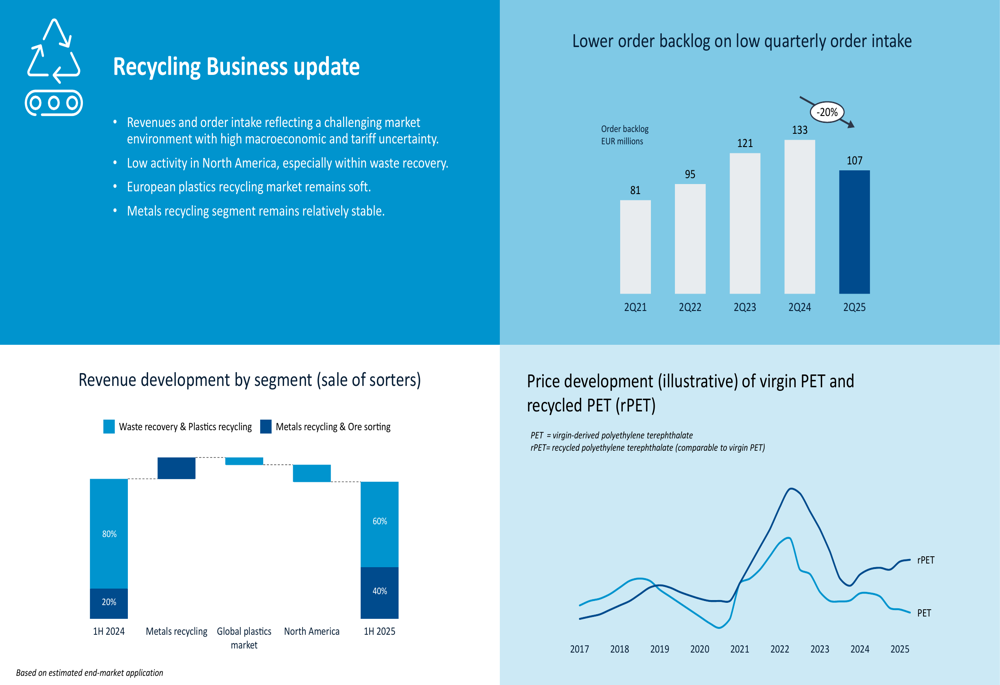

The Recycling segment reported flat revenues of €57 million compared to Q2 2024, reflecting a challenging market environment with high macroeconomic and tariff uncertainty. Order intake and backlog metrics indicate continued pressure, with the backlog declining 20% year-over-year to €107 million.

The segment faces particular challenges in North America, especially within waste recovery, and is dealing with a soft European plastics recycling market:

While metals recycling remains relatively stable, the overall recycling market continues to face headwinds from price pressures and market uncertainty.

Food

The Food segment emerged as TOMRA's standout performer in Q2 2025, delivering record high quarterly EBITA, order intake, and backlog. Revenues increased by 15% to €94 million, while EBITA more than doubled from €8 million in Q2 2024 to €20 million.

Market sentiment is improving with strong order intake across all regions:

The segment's success is attributed to large orders in categories including Citrus, Avocados, and Potatoes, though management acknowledges that macroeconomic and tariff uncertainty may impact customer investment sentiment going forward.

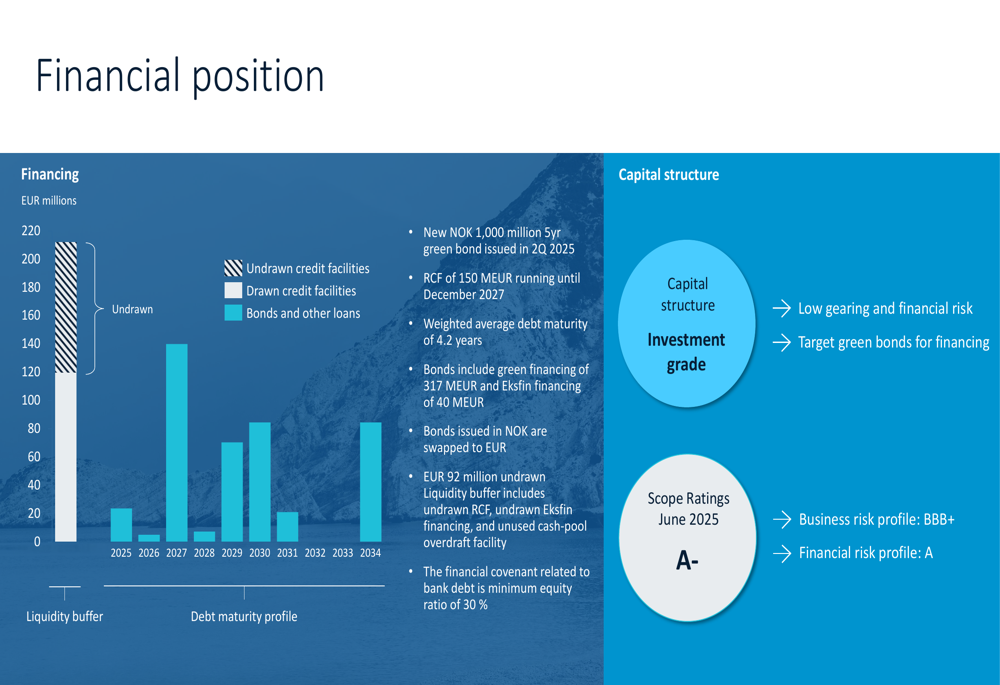

Financial Position and Outlook

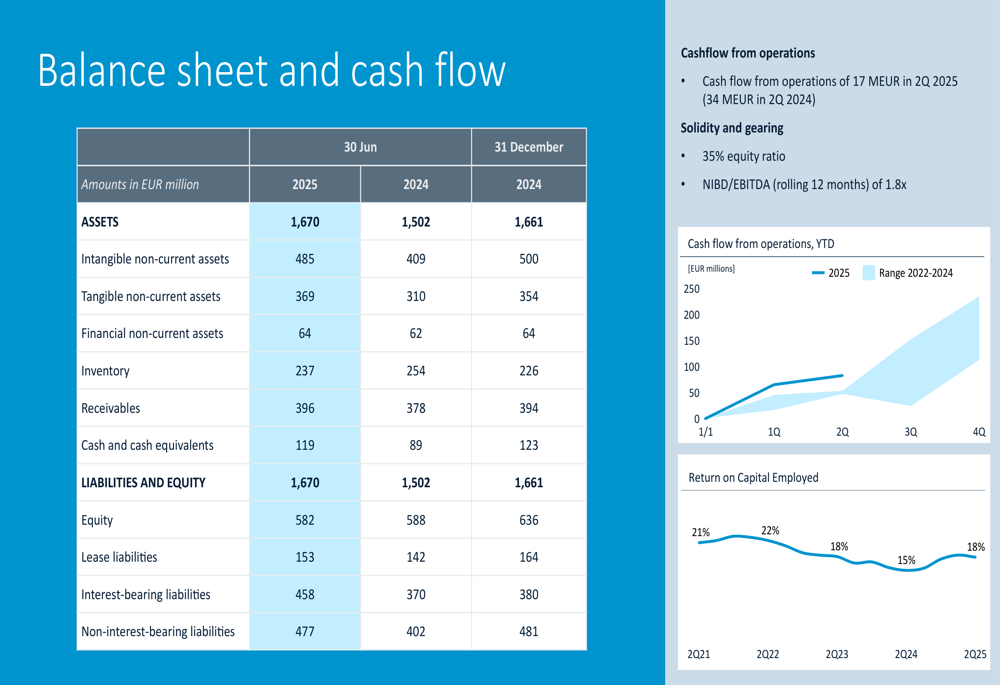

TOMRA maintains a solid financial position with an equity ratio of 35% and a NIBD/EBITDA ratio of 1.8x. The company issued a new NOK 1,000 million 5-year green bond in Q2 2025 and has a weighted average debt maturity of 4.2 years.

The balance sheet and cash flow highlights demonstrate the company's financial stability:

TOMRA's debt profile shows a balanced maturity structure with significant undrawn credit facilities providing additional financial flexibility:

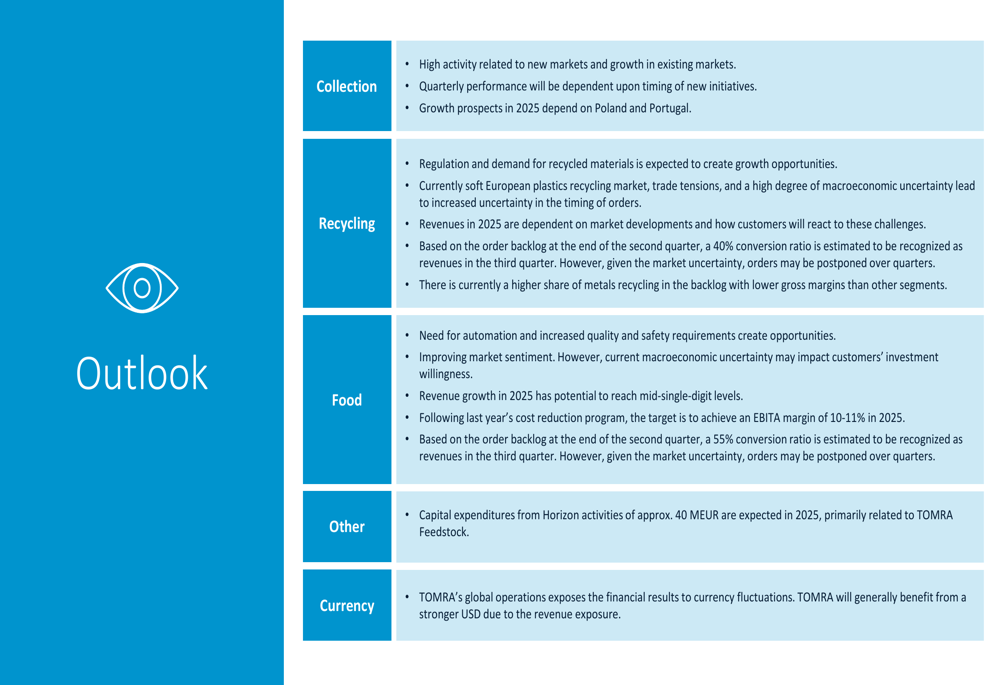

Looking ahead, TOMRA provided segment-specific outlooks, noting high activity related to new markets in Collection, while acknowledging market uncertainties in Recycling. The Food segment is expected to achieve mid-single-digit revenue growth in 2025:

Capital expenditures from Horizon activities are expected to reach approximately €40 million in 2025, primarily related to TOMRA Feedstock.

Strategic Initiatives

TOMRA continues to advance strategic initiatives across its business segments. In the Collection segment, the company is preparing for new market entries, particularly in Poland and Portugal. The Horizon business is making progress with TOMRA Feedstock's commissioning phase yielding good throughput and high purities.

TOMRA Reuse preparations are underway in Lisbon, with 17 return points planned across the downtown area by October. The company has also launched a Reuse Collection Point accepting reusable food packaging, with live testing ongoing in Aarhus.

A significant milestone is the upcoming official opening of Områ, Norway's National Sorting Facility for Plastics, scheduled for November 5, 2025. This facility represents TOMRA's commitment to advancing recycling infrastructure and capabilities.

Despite current challenges in some segments, TOMRA's management remains focused on long-term growth opportunities driven by global sustainability trends and increasing adoption of deposit return systems worldwide. The company's strategic positioning across Collection, Recycling, and Food segments provides diversification and multiple growth avenues as markets evolve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.