Trading Nvidia earnings report? These are the entry and exit levels to watch for

Introduction & Market Context

Topaz Energy Corp . (TSX:TPZ) recently presented its Q2 2025 corporate overview, highlighting the company’s unique position as a hybrid royalty and infrastructure business in the Western Canadian Sedimentary Basin (WCSB). With a market capitalization of $3.9 billion and an enterprise value of $4.4 billion, Topaz has established itself as a significant player in the Canadian energy sector.

The company’s stock has shown strong performance, with a 34.91% return over the past year according to recent earnings data. Currently trading at $26.08 (as of July 28, 2025), the stock sits comfortably above its 52-week low of $21.00, though still below its 52-week high of $29.51.

Business Model & Revenue Diversification

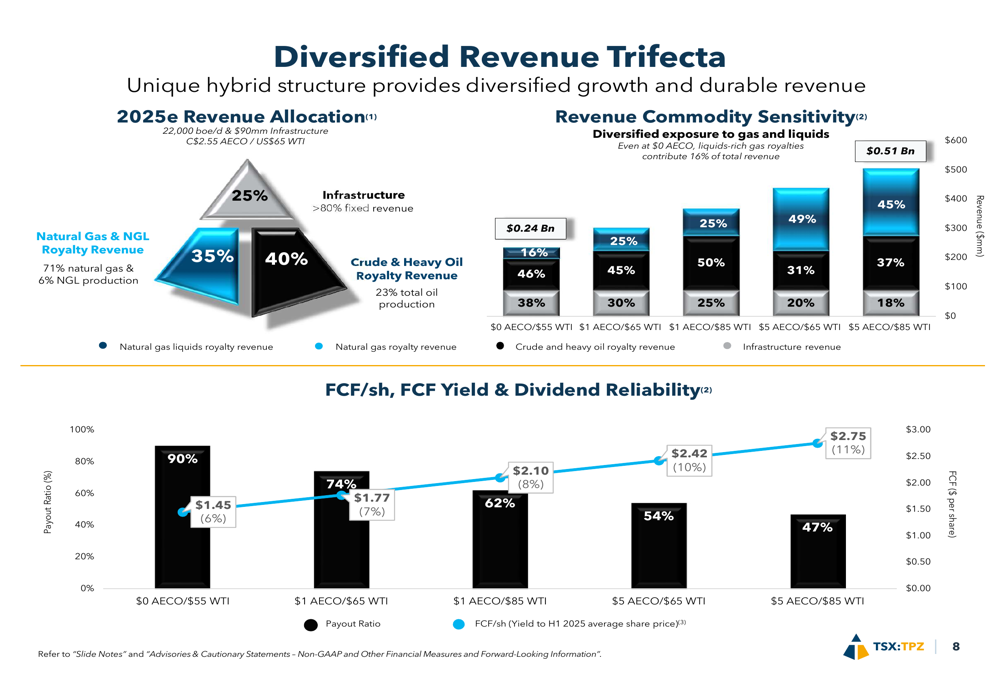

Topaz’s business model is built on a diversified revenue stream that provides resilience against commodity price fluctuations. The company’s 2025 estimated revenue mix consists of 40% liquids-rich natural gas royalty, 25% crude and heavy oil royalty, and 35% high-margin infrastructure.

This "revenue trifecta" approach has enabled Topaz to maintain strong cash flows even during periods of commodity price volatility. The company’s presentation emphasizes its ability to maintain dividend coverage even at $0 AECO/$55 WTI price scenarios, demonstrating the defensive nature of its business model.

As shown in the following revenue diversification chart:

The company’s infrastructure assets provide particularly stable cash flows, with an 81% cash flow margin compared to the 25% industry average for midstream operators. Similarly, Topaz’s royalty assets generate a 92% free cash flow margin versus just 20% for the four largest E&P operators in its portfolio.

Strategic Asset Positioning

Topaz has strategically positioned its assets in the most economic plays within the WCSB. According to the presentation, 68% of the company’s royalty acreage is focused in the Montney, Deep Basin, and Clearwater regions, which feature payout periods of less than 1.3 years, indicating strong economics even in lower commodity price environments.

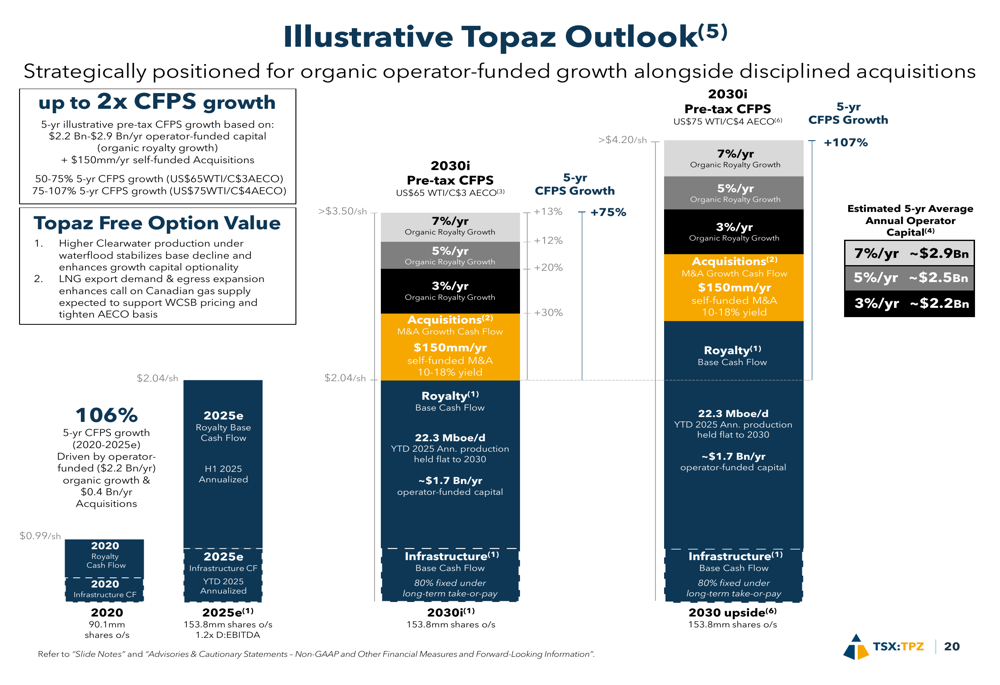

The company’s outlook for future growth is supported by several catalysts, including the commissioning of LNG Canada Phase 1 in July 2025, which provides a 10% expansion in natural gas egress capacity. Additionally, potential data center projects in Alberta could significantly increase electricity demand, further supporting natural gas prices.

Topaz’s long-term strategy is clearly illustrated in the following outlook chart, which projects continued growth through both organic development and acquisitions:

Financial Performance & Dividend Strategy

Topaz has demonstrated strong financial performance, with a projected 2025 free cash flow yield of 8%. The company’s Q1 2025 results, released prior to this presentation, showed an EPS of $0.14, exceeding analyst expectations of $0.1013, and quarterly revenue of $92.2 million.

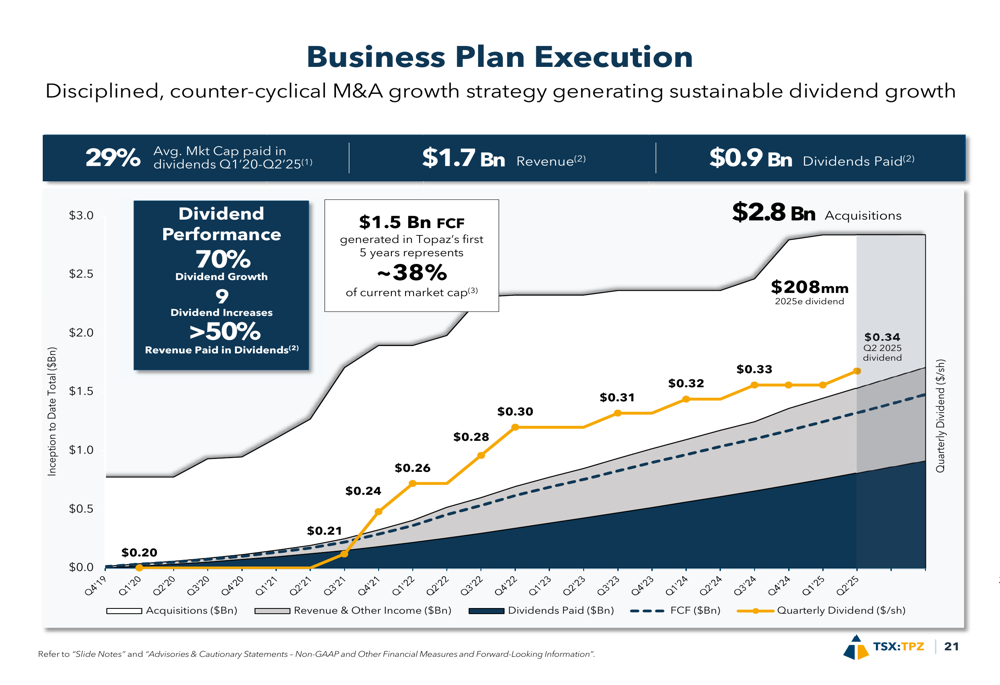

The company’s dividend strategy has been a cornerstone of its shareholder return policy. Since inception, Topaz has increased its dividend nine times, with a total growth of 70% from $0.80 per share in 2020 to a projected $1.35 per share in 2025. The current dividend yield stands at 5.3% according to the presentation, with a projected 2025 payout ratio of 66%.

As shown in the following business plan execution chart, Topaz has paid approximately 29% of its average market capitalization in dividends from Q1 2020 through Q2 2025:

The company’s strong free cash flow generation has supported both dividend growth and acquisition activity. Since inception, Topaz has generated $1.5 billion in free cash flow (representing about 38% of its current market cap), paid $0.9 billion in dividends, and completed $2.8 billion in acquisitions.

Competitive Advantages & Market Positioning

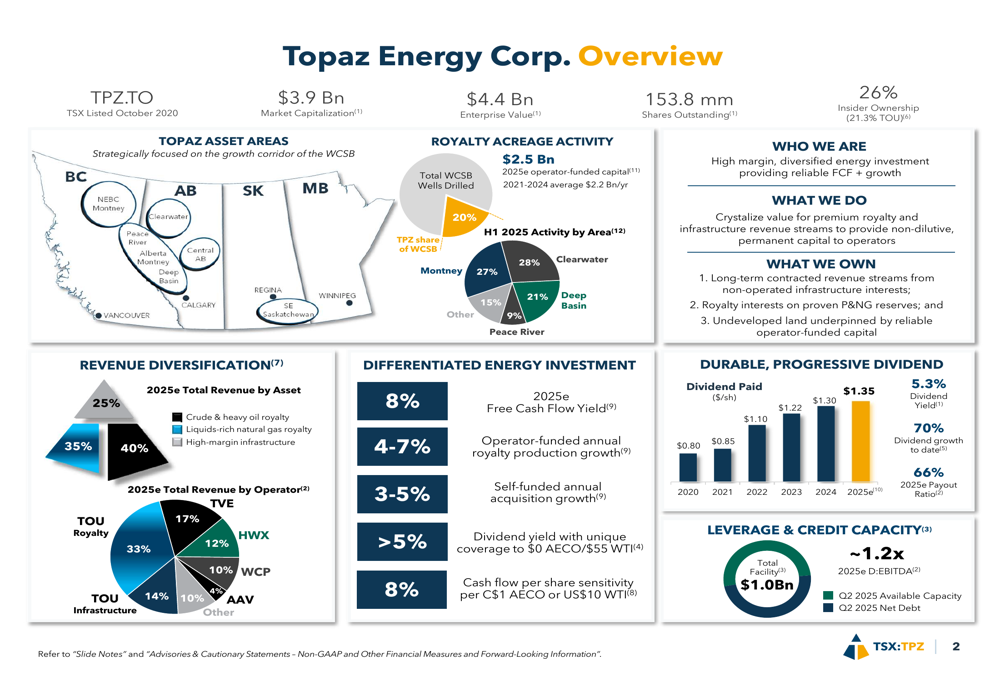

Topaz highlights several competitive advantages that differentiate it from peers in the energy sector. These include its diversified high-quality assets, defensive growth profile, durable revenue streams, and high-margin fixed infrastructure.

The company’s competitive positioning is illustrated in this overview of its advantages:

A key strength is Topaz’s relationship with strategic operating partners who provide dedicated capital for development. Approximately 93% of Topaz’s royalty volume comes from leading Canadian operators with size, scale, and economic resiliency at oil prices below US$55 WTI.

The company has also increased its share of WCSB rig activity from 11% in 2020 to 20% in the first half of 2025, demonstrating its growing influence in the basin.

Forward Outlook & Growth Catalysts

Looking ahead, Topaz has provided guidance for 2025, projecting production between 21,000 and 23,000 BOE per day and processing revenue between $88 million and $92 million. The company expects to maintain a year-end net debt to EBITDA ratio of 1.2x.

Topaz’s growth strategy combines operator-funded royalty production growth (projected at 4-7% annually) with self-funded acquisition growth (3-5% annually). This approach has delivered strong results, with the Q1 2025 earnings report showing a 17% year-over-year increase in royalty production, exceeding the company’s long-term growth projections.

The company’s overview slide provides a comprehensive snapshot of its current position and future outlook:

CEO Marty Staples expressed confidence in the company’s strategic positioning during the recent earnings call, stating, "We remain extremely confident in the price resiliency of the plays." This sentiment is reflected in the presentation’s emphasis on the company’s focus on commodity price-resilient plays.

With its diversified revenue streams, strategic asset positioning, and disciplined capital allocation approach, Topaz appears well-positioned to continue delivering value to shareholders through both dividend growth and capital appreciation in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.