Gold prices steady ahead of Fed decision; weekly weakness noted

Introduction & Market Context

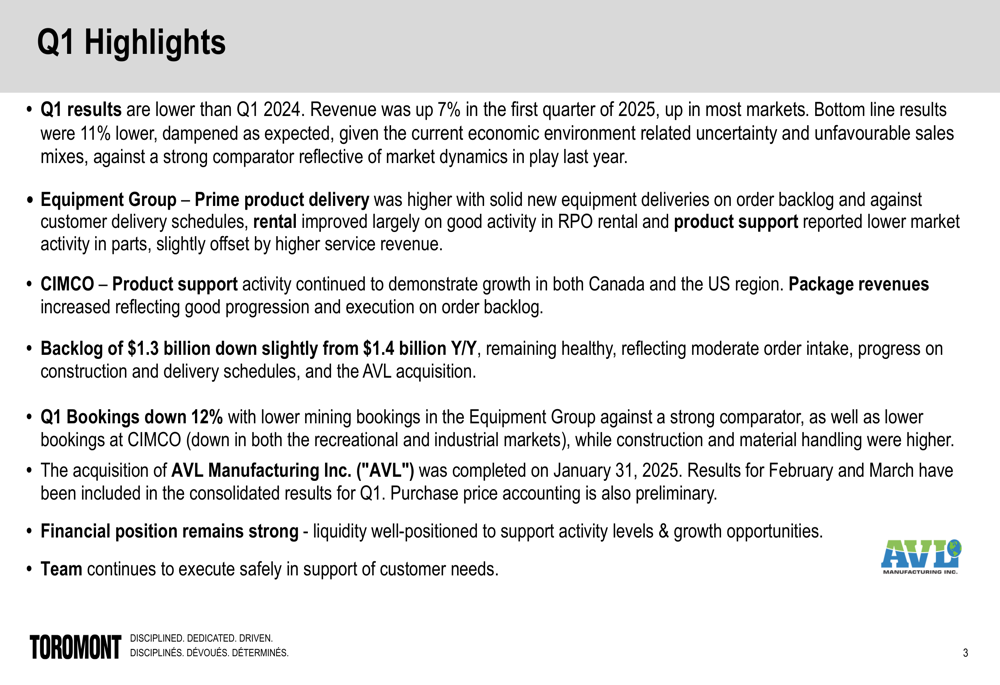

Toromont Industries Ltd . (TSX:TIH) presented its first quarter 2025 results on May 1, revealing a mixed performance characterized by revenue growth but declining profitability. The heavy equipment dealer and refrigeration systems provider faced economic headwinds including inflation, interest rate pressures, and volatile foreign exchange rates.

The company’s stock closed at C$116.64 on April 30, 2025, and has traded between C$107.32 and C$134.88 over the past 52 weeks, reflecting the challenging operating environment that has persisted from previous quarters.

Quarterly Performance Highlights

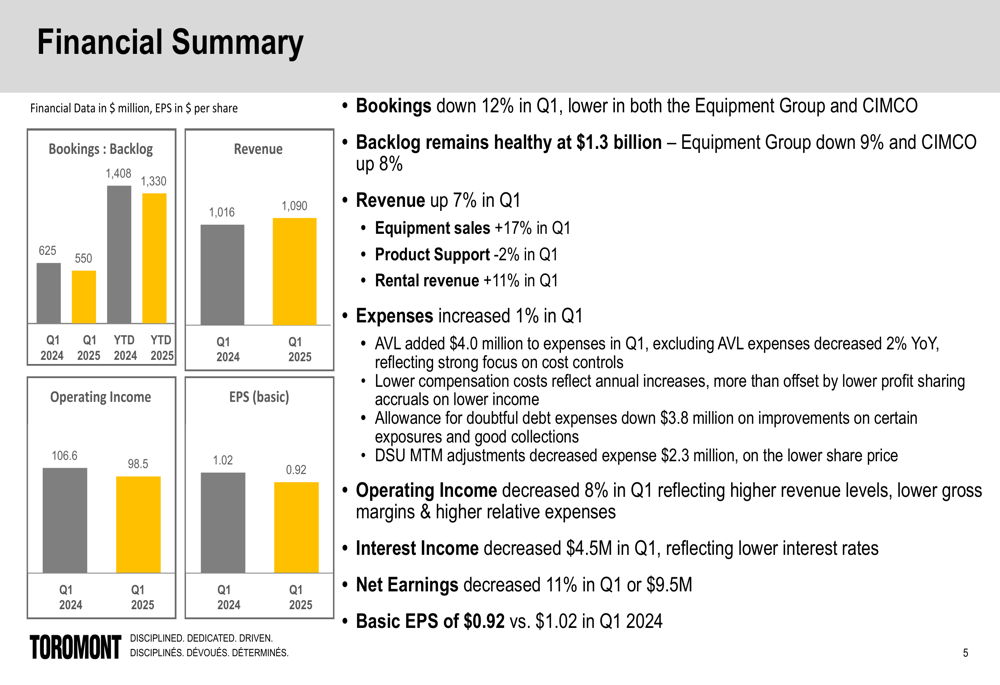

Toromont reported a 7% increase in revenue for Q1 2025 compared to the same period last year, but this top-line growth was overshadowed by an 11% decline in net earnings. Basic earnings per share fell to $0.92 from $1.02 in Q1 2024, representing a 9.8% decrease.

As shown in the following financial summary:

The company’s order bookings decreased by 12% in Q1, while the backlog remained relatively healthy at $1.3 billion, though slightly down from $1.4 billion year-over-year. Equipment sales showed strong growth of 17%, but this was partially offset by a 2% decline in product support revenue. Rental revenue increased by 11% compared to Q1 2024.

Operating income decreased by 8% to $98.5 million, impacted by margin pressures and changing product mix. The company also noted a $4.5 million decrease in interest income during the quarter, further affecting bottom-line results.

Segment Analysis

Toromont’s business is divided into two main segments: the Equipment Group and CIMCO, which showed divergent performance in the quarter.

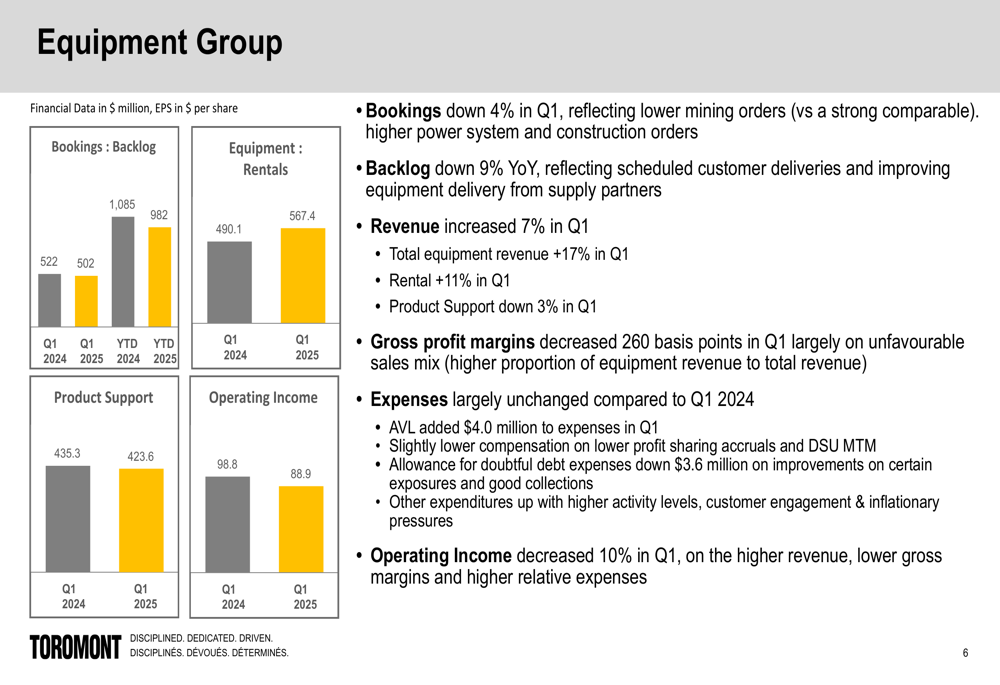

The Equipment Group, which represents the bulk of Toromont’s business, experienced challenges despite revenue growth:

The Equipment Group saw a 7% increase in revenue, driven by a 17% rise in equipment sales and 11% growth in rentals. However, product support revenue declined by 3%, and gross profit margins decreased by 260 basis points. Operating income for this segment fell by 10% to $88.9 million, reflecting the margin pressure despite higher sales volumes.

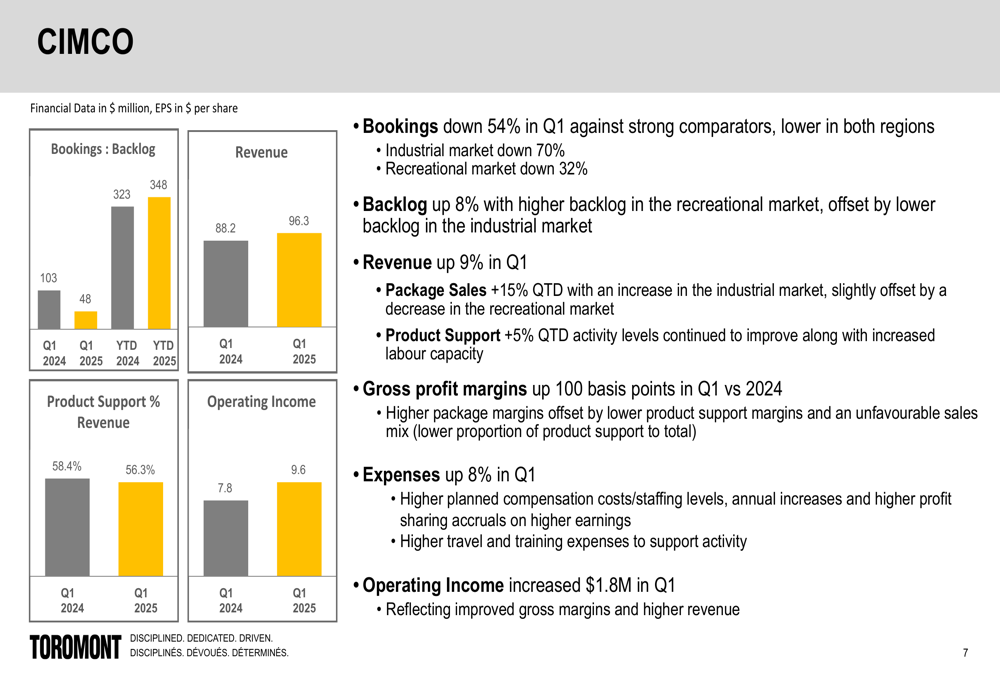

In contrast, CIMCO, the company’s refrigeration systems division, delivered stronger results:

CIMCO’s revenue increased by 9% to $96.3 million, with package sales up 15% and product support growing by 5%. Gross profit margins improved by 100 basis points compared to Q1 2024. Despite an 8% increase in expenses, operating income for CIMCO increased by $1.8 million, demonstrating the segment’s resilience and growth potential.

Financial Position & Capital Allocation

Despite the earnings challenges, Toromont maintained a strong financial position with significant liquidity and continued shareholder returns:

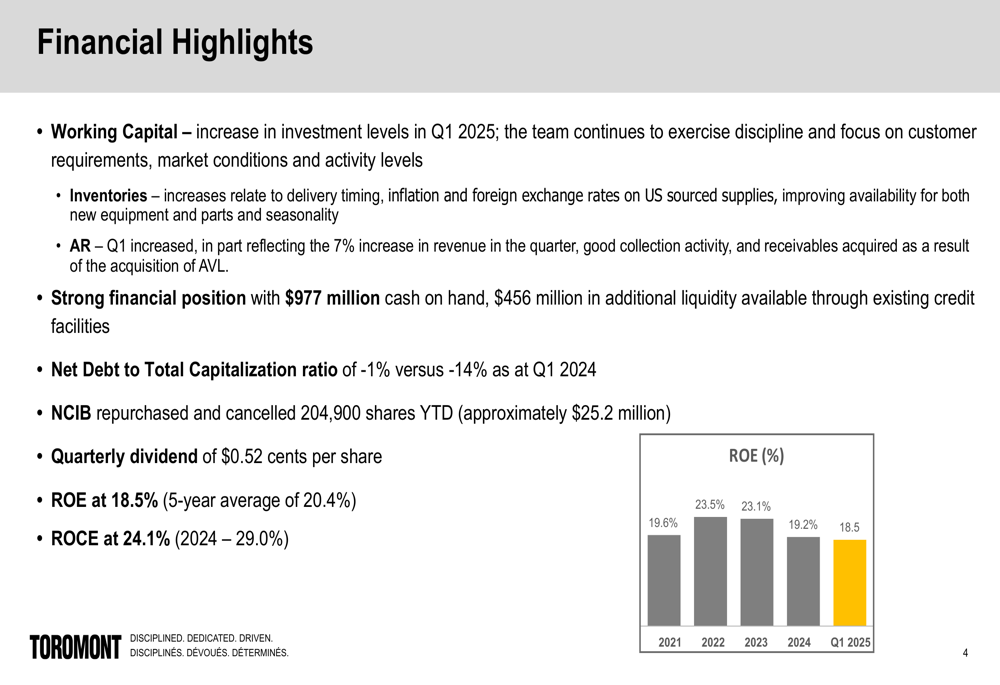

The company reported $977 million in cash on hand and an additional $456 million in available liquidity. The net debt to total capitalization ratio stood at -1%, compared to -14% in Q1 2024, indicating a slight change in capital structure but still reflecting a very strong balance sheet.

Toromont continued its capital allocation strategy with a quarterly dividend of $0.52 per share and the repurchase and cancellation of 204,900 shares year-to-date at a cost of approximately $25.2 million under its Normal Course Issuer Bid (NCIB) program.

Return on equity (ROE) was 18.5%, below the five-year average of 20.4% and continuing a downward trend from the 23.5% peak in 2022. Similarly, return on capital employed (ROCE) decreased to 24.1% from 29.0% in 2024.

Strategic Initiatives & Outlook

During the quarter, Toromont completed the acquisition of AVL Manufacturing Inc. on January 31, 2025, expanding its capabilities and market reach:

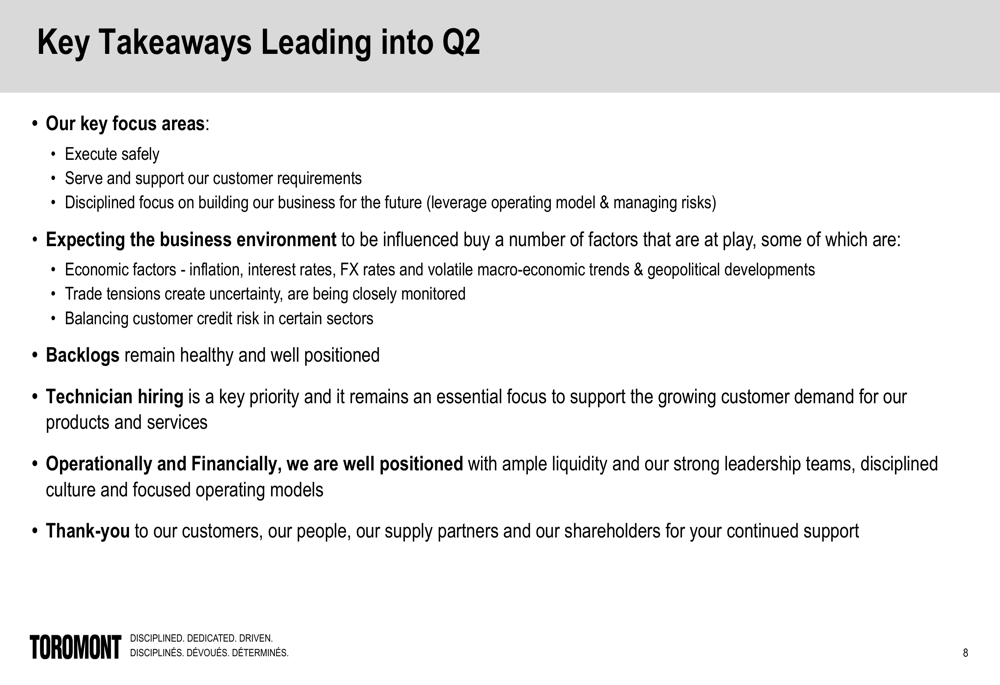

Looking ahead, Toromont identified several focus areas and challenges for the coming quarters:

Management emphasized three key focus areas: executing safely, serving and supporting customer requirements, and maintaining a disciplined focus on building the business for the future. The company acknowledged that the business environment would continue to be influenced by economic factors, trade tensions, and customer credit risks in certain sectors.

Technician hiring was highlighted as a key priority, suggesting that the company is positioning itself for future growth despite current challenges. Management expressed confidence in Toromont’s operational and financial positioning, with ample liquidity to navigate the uncertain economic landscape.

As Toromont moves into Q2 2025, investors will be watching closely to see if the company can maintain revenue growth while addressing the margin pressures that impacted its bottom-line performance in the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.