Conservative commentator Charlie Kirk shot and killed at Utah event

Introduction & Market Context

TransDigm Group Inc. (NYSE:TDG), a leading manufacturer of highly engineered aerospace components, presented its second quarter fiscal 2025 results on May 6, 2025, highlighting continued strong performance across its commercial aftermarket and defense segments. The company reported double-digit growth in both revenue and EBITDA, maintaining its full-year guidance despite some softness in the commercial OEM market.

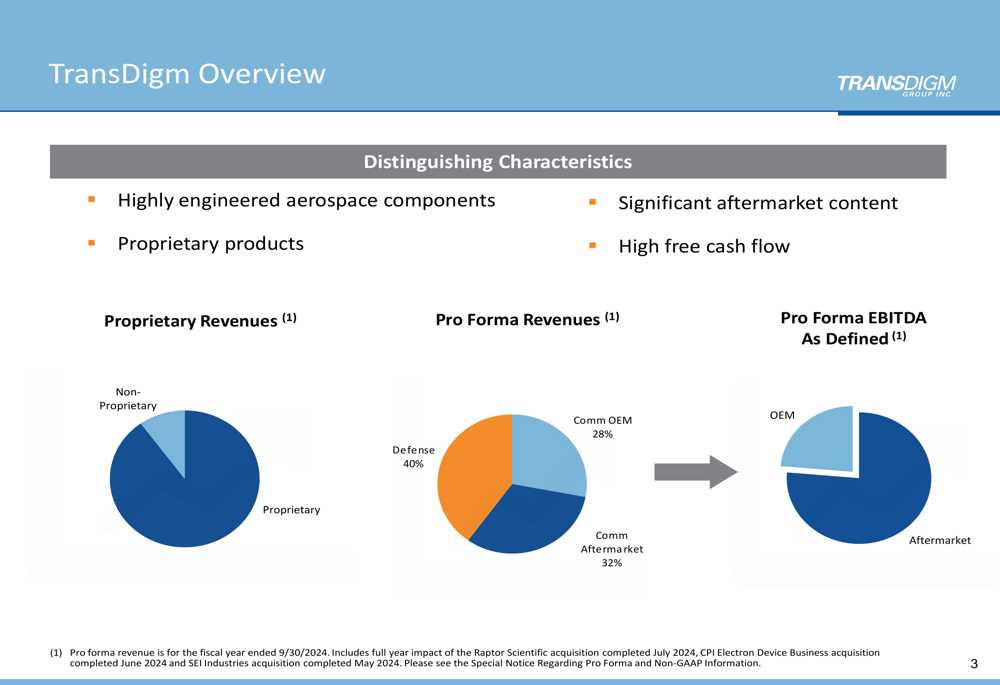

The aerospace supplier continues to benefit from its diversified business model with significant aftermarket content, proprietary products, and high free cash flow generation. TransDigm’s revenue mix remains well-balanced across defense (40%), commercial OEM (28%), and commercial aftermarket (32%) segments, providing resilience against fluctuations in individual aerospace markets.

As shown in the following company overview chart:

Quarterly Performance Highlights

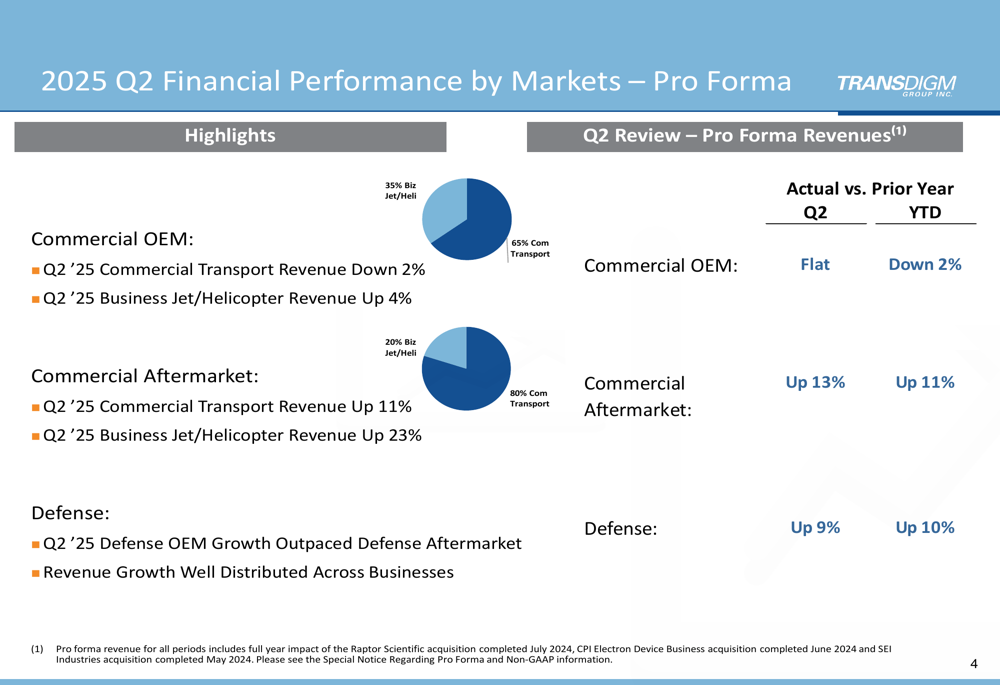

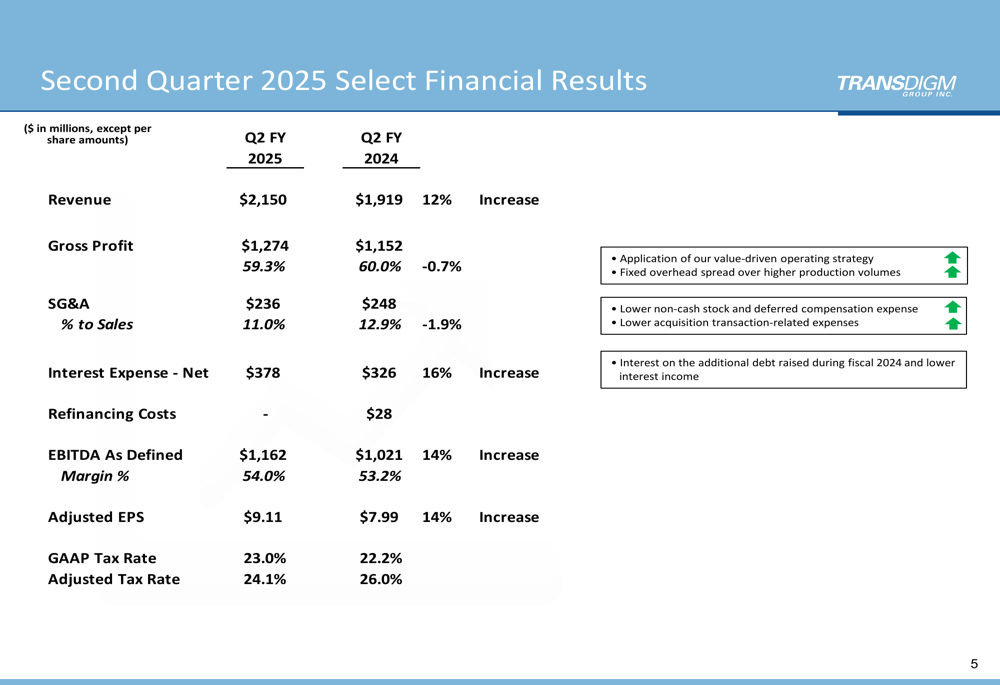

TransDigm reported Q2 FY2025 revenue of $2,150 million, a 12% increase from $1,919 million in the same period last year. This growth was primarily driven by the commercial aftermarket segment, which saw a 13% year-over-year increase, with business jet and helicopter aftermarket revenue surging 23%. Defense revenue also performed well, growing 9% compared to Q2 FY2024.

The company’s commercial OEM segment showed mixed results, with overall performance flat compared to the prior year. Within this segment, commercial transport revenue declined 2%, while business jet and helicopter OEM revenue increased 4%.

The following chart illustrates TransDigm’s Q2 2025 performance across its key market segments:

EBITDA As Defined (TransDigm’s preferred profitability metric) reached $1,162 million, representing a 14% increase from $1,021 million in Q2 FY2024. The EBITDA margin improved to 54.0% from 53.2% in the prior year period, demonstrating the company’s continued focus on operational efficiency despite inflationary pressures.

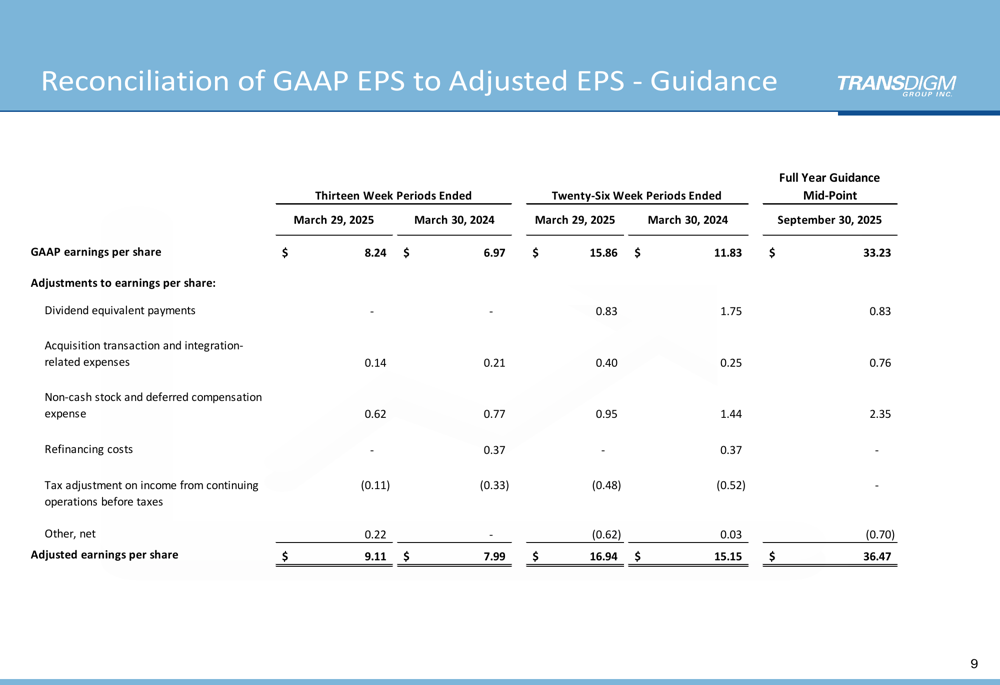

Adjusted earnings per share grew to $9.11, a 14% increase from $7.99 in the same quarter last year, driven by higher sales volumes and improved operational performance.

The detailed financial results for the second quarter are presented in the following table:

Detailed Financial Analysis

While TransDigm’s top-line growth remained robust, gross profit margin experienced a slight contraction of 0.7 percentage points to 59.3% compared to 60.0% in Q2 FY2024. However, the company offset this with improved SG&A efficiency, reducing these expenses as a percentage of sales by 1.9 percentage points to 11.0% from 12.9% in the prior year period.

Interest expense increased 16% to $378 million, reflecting additional debt raised during fiscal 2024 and lower interest income. The company’s adjusted tax rate improved to 24.1% from 26.0% in the same period last year.

TransDigm’s strong performance across its defense and commercial aftermarket segments continues to drive overall growth. Defense revenue growth was well-distributed across businesses, while commercial aftermarket strength was particularly notable in the business jet and helicopter segment, which grew 23% year-over-year.

Forward-Looking Statements

TransDigm maintained its fiscal 2025 guidance, projecting full-year revenue of $8,850 million and EBITDA As Defined between $4,615 million and $4,755 million. The company expects net income between $1,925 million and $2,037 million, with adjusted EPS ranging from $35.51 to $37.43.

For fiscal 2025, TransDigm anticipates continued strength across its key market segments:

- Commercial OEM: Low to mid-single-digit percentage growth

- Commercial Aftermarket: High single-digit to low double-digit percentage growth

- Defense: High single-digit to low double-digit percentage growth

The following slide details the company’s fiscal 2025 outlook:

TransDigm’s financial assumptions for fiscal 2025 remain unchanged from its previous guidance issued in February 2025. The company continues to project capital expenditures between $255 million and $285 million, with a full-year effective tax rate of approximately 22% to 24% for both GAAP and adjusted EPS.

Capital Structure and Debt Management

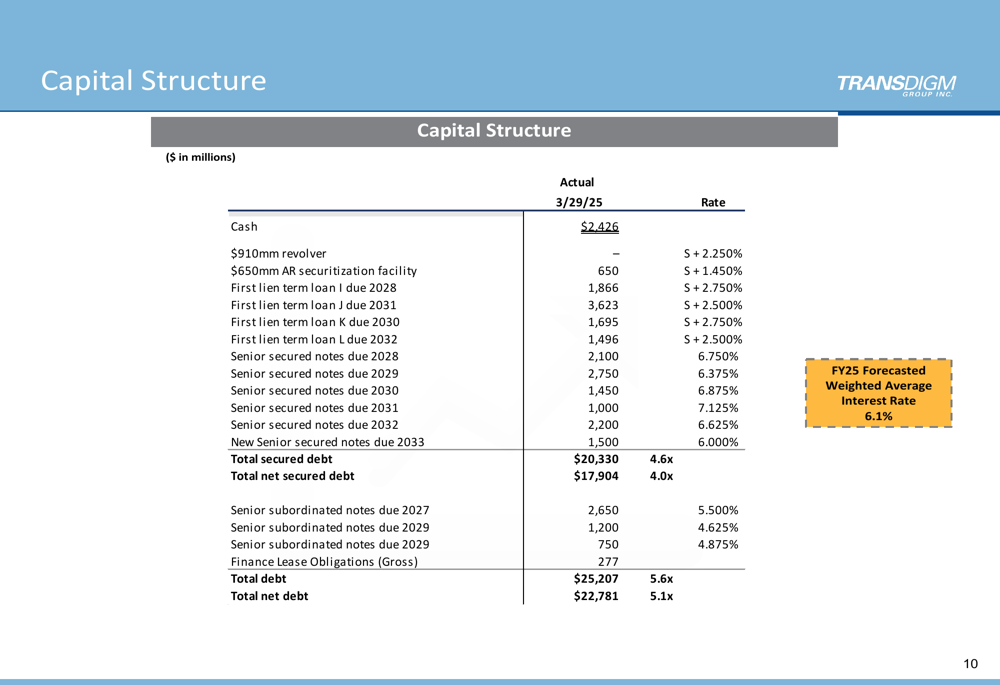

As of March 29, 2025, TransDigm reported a cash balance of $2,426 million and total debt of $25,207 million, representing a leverage ratio of 5.6x. The company’s net debt stood at $22,781 million (5.1x leverage).

The following slide provides a detailed breakdown of TransDigm’s capital structure:

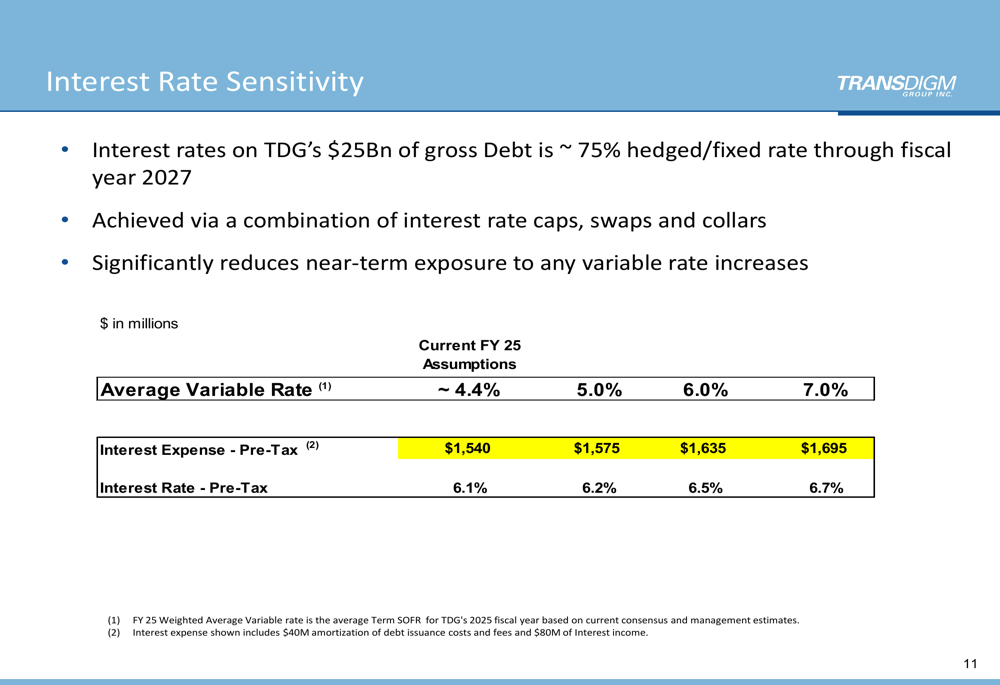

TransDigm has implemented a comprehensive interest rate management strategy, with approximately 75% of its gross debt hedged or fixed through fiscal year 2027. This approach significantly reduces the company’s near-term exposure to variable rate increases. The company has utilized a combination of interest rate caps, swaps, and collars to achieve this protection.

The impact of different interest rate scenarios on TransDigm’s interest expense is illustrated in the following chart:

The company’s debt maturity profile is well-structured, with maturities spread across multiple years to minimize refinancing risk. TransDigm’s $910 million revolving credit facility matures in February 2029, while its $650 million accounts receivable securitization facility renews annually in July.

TransDigm continues to demonstrate strong financial performance driven by its diversified business model and focus on proprietary, highly engineered aerospace components. The robust growth in commercial aftermarket and defense segments has offset challenges in the commercial OEM market, allowing the company to maintain its full-year guidance. With a well-structured capital position and effective interest rate management strategy, TransDigm appears well-positioned to navigate potential market volatility while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.