EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

Travelers Companies (NYSE:TRV) released its second quarter 2025 results on July 17, showcasing exceptional performance across all business segments. The insurance giant reported a dramatic improvement in profitability, with net income soaring 183% compared to the same period last year. This performance builds upon the momentum seen in Q1 2025, when the company significantly outperformed analyst expectations.

The current stock price of $252.19 sits well within its 52-week range of $202.95 to $277.83, with premarket trading showing a slight decline of 0.08% following the presentation. This minimal movement suggests investors may have already priced in strong results following the company’s impressive Q1 performance.

Quarterly Performance Highlights

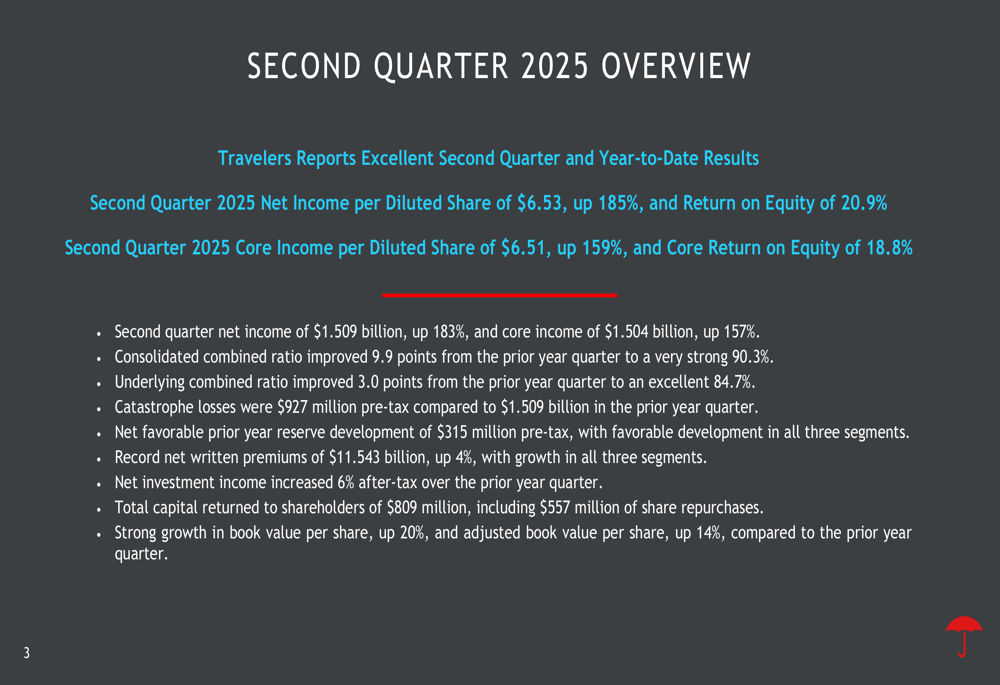

Travelers reported substantial improvements across key financial metrics for the second quarter of 2025, with particularly strong growth in earnings per share and significantly lower catastrophe losses compared to the prior year period.

As shown in the following comprehensive overview of Q2 2025 results:

Net income per diluted share reached $6.53, representing a 185% increase from Q2 2024, while core income per diluted share grew 159% to $6.51. The company achieved a return on equity of 20.9% and core return on equity of 18.8%, reflecting exceptional profitability.

The consolidated combined ratio improved dramatically by 9.9 points to 90.3%, indicating significantly better underwriting results. This improvement was driven by both lower catastrophe losses ($927 million pre-tax compared to $1.509 billion in the prior year quarter) and a 3.0 point improvement in the underlying combined ratio to 84.7%.

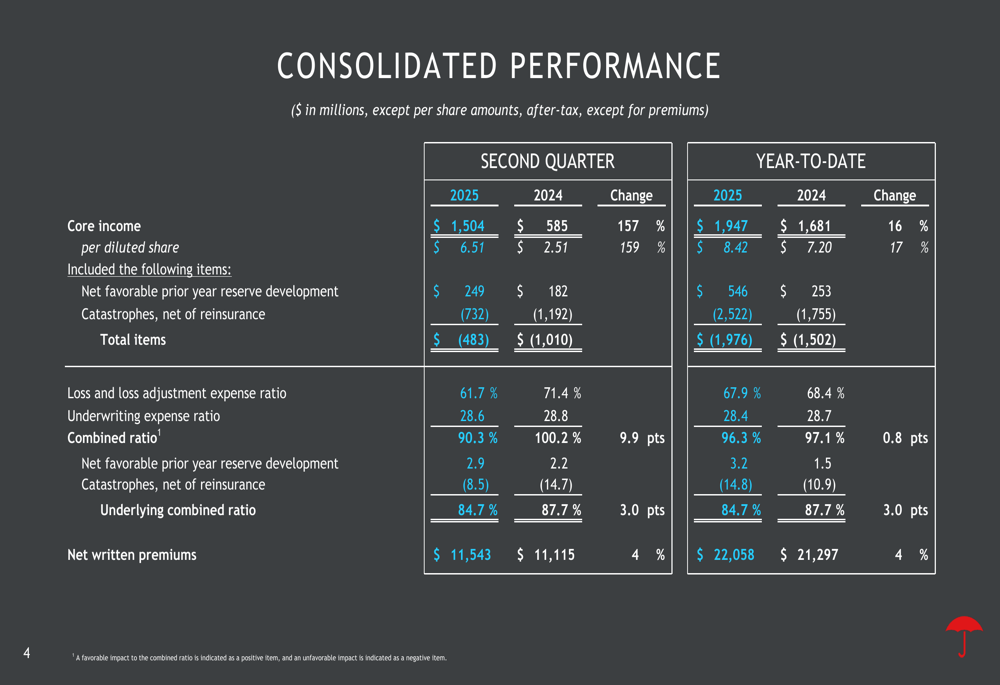

The detailed consolidated performance metrics further illustrate the company’s strong results:

Net written premiums reached a record $11.543 billion, up 4% from the prior year quarter, with growth across all three business segments. The company also reported $315 million in favorable prior year reserve development, with positive contributions from all segments.

Segment Performance Analysis

All three of Travelers’ business segments delivered strong results in Q2 2025, with particularly notable improvements in the Personal Insurance segment.

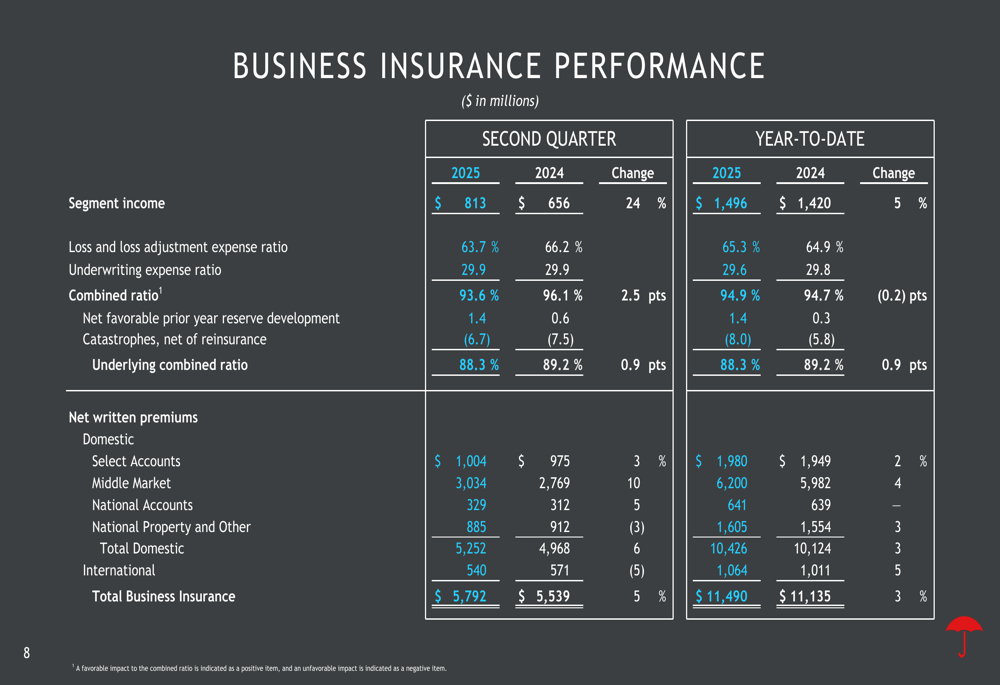

The Business Insurance segment, which represents the largest portion of Travelers’ operations, posted impressive growth:

Segment income for Business Insurance reached $813 million in Q2 2025, a 24% increase from the $656 million reported in Q2 2024. The combined ratio improved by 2.5 points to 93.6%, reflecting better underwriting results. Net written premiums grew by 5%, with domestic Business Insurance showing particularly strong performance in the Middle Market and National Property segments.

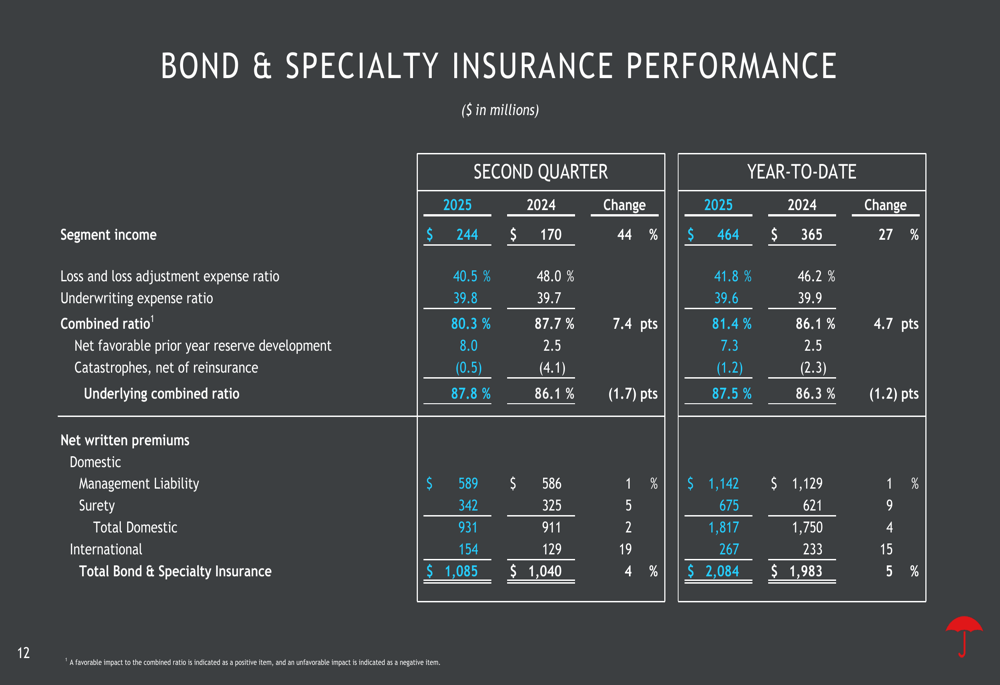

The Bond & Specialty Insurance segment also delivered exceptional results:

Segment income for Bond & Specialty Insurance was $244 million, representing a 44% increase from Q2 2024. Net written premiums grew by 4%, with strong performance in both domestic and international markets. The segment’s combined ratio improved significantly, reflecting disciplined underwriting and favorable prior year reserve development.

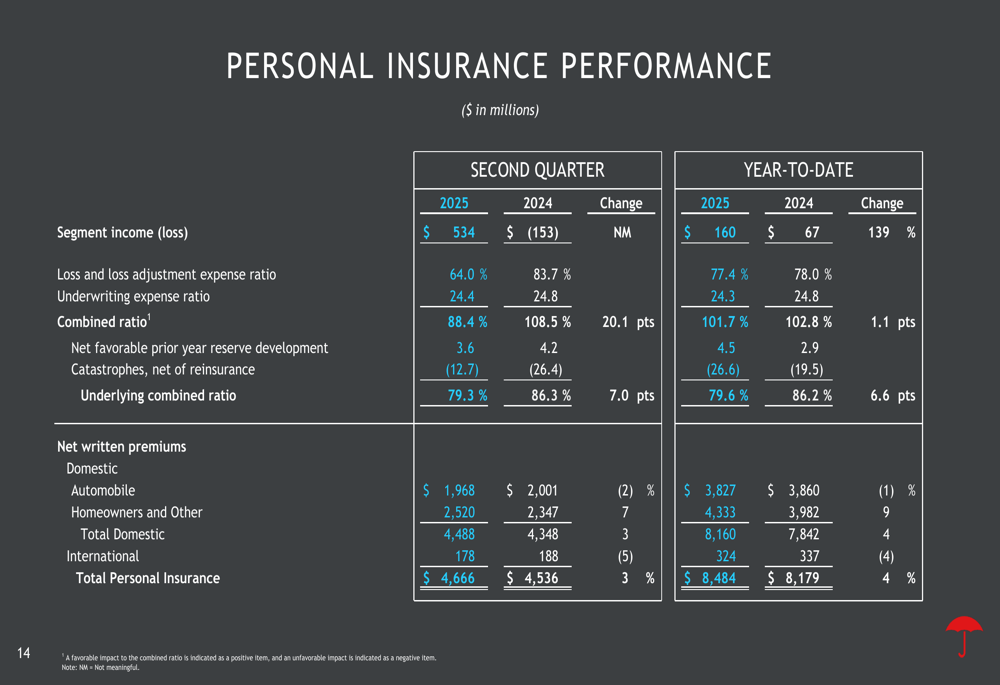

Perhaps most impressive was the dramatic turnaround in the Personal Insurance segment:

The Personal Insurance segment reported income of $534 million in Q2 2025, compared to a loss of $153 million in Q2 2024. This remarkable improvement was driven by significantly lower catastrophe losses and better underlying performance in both auto and homeowners insurance. Net written premiums increased by 3%, with growth in both domestic and international markets.

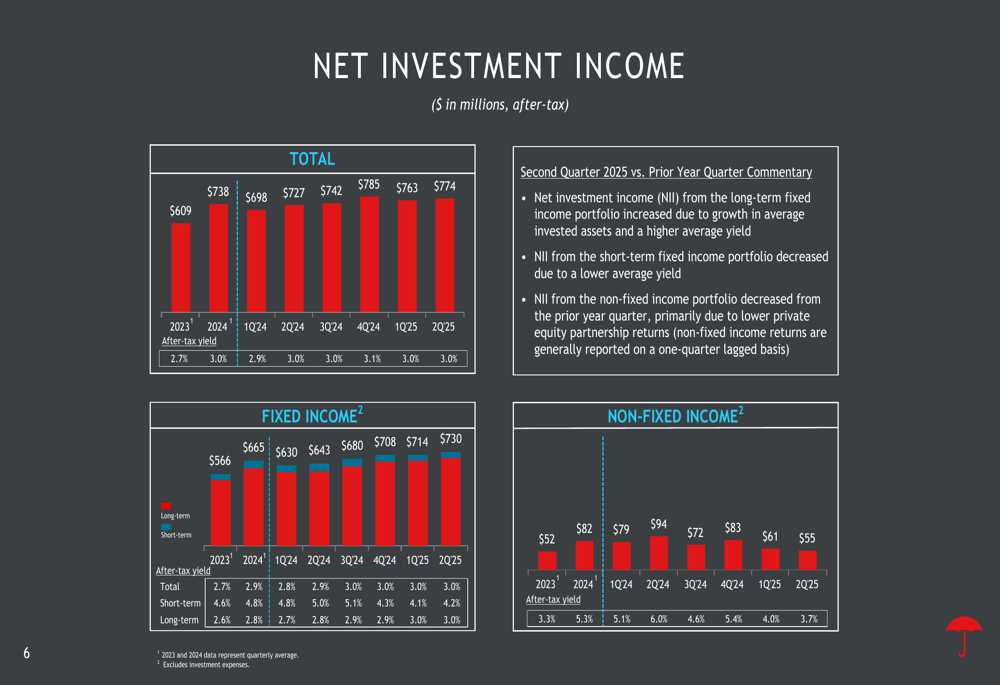

Investment Income and Portfolio Quality

Travelers’ investment portfolio continued to deliver solid results, with net investment income increasing 6% after-tax compared to the prior year quarter. The company maintains a conservative investment approach, with 94% of its $98.1 billion portfolio allocated to fixed income securities.

The following chart illustrates the company’s net investment income trends:

Net investment income from long-term fixed income increased due to growth in average invested assets and a higher average yield, while income from short-term fixed income decreased due to a lower average yield. Non-fixed income returns decreased primarily due to lower private equity partnership returns.

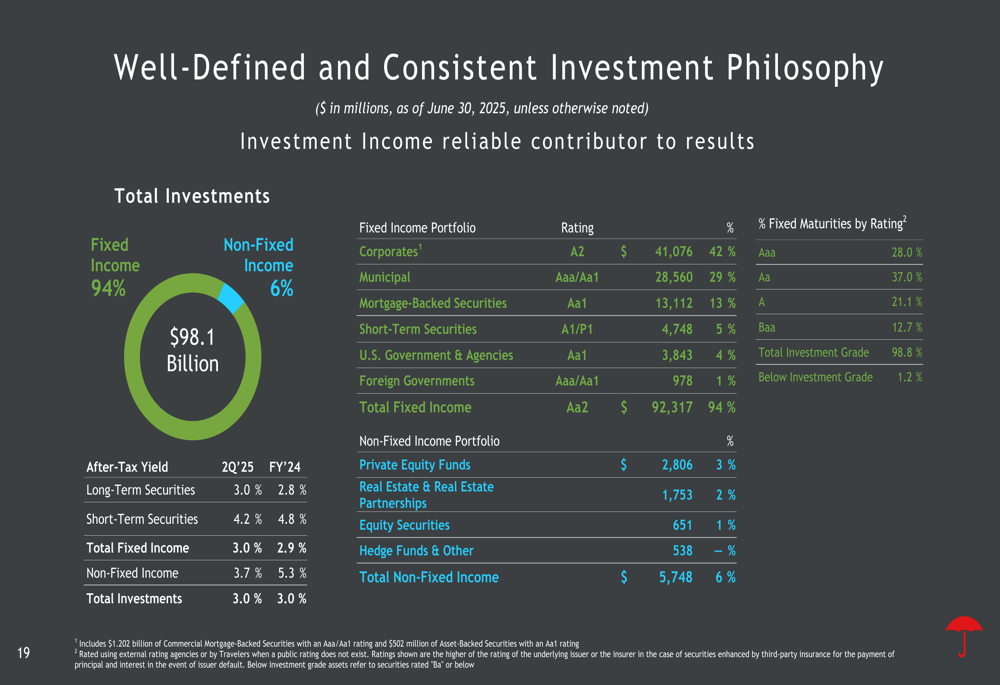

The company’s well-defined investment philosophy emphasizes quality and stability:

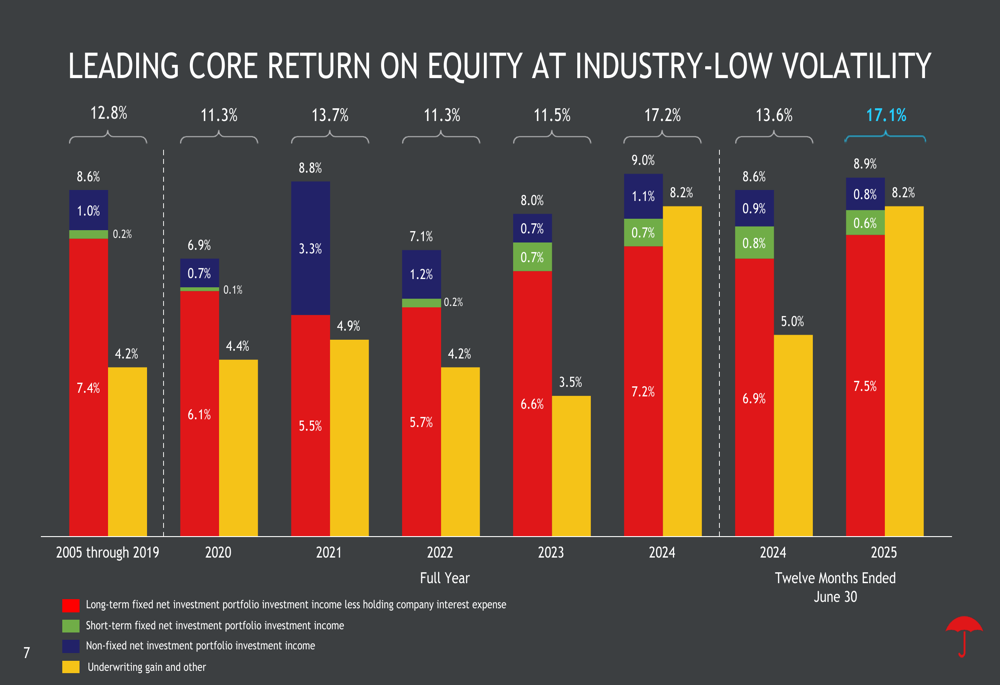

The fixed income portfolio maintains an excellent credit quality profile, with 65% of fixed maturities rated Aaa or Aa. This conservative approach has contributed to Travelers’ industry-leading core return on equity with low volatility, as illustrated in the following chart:

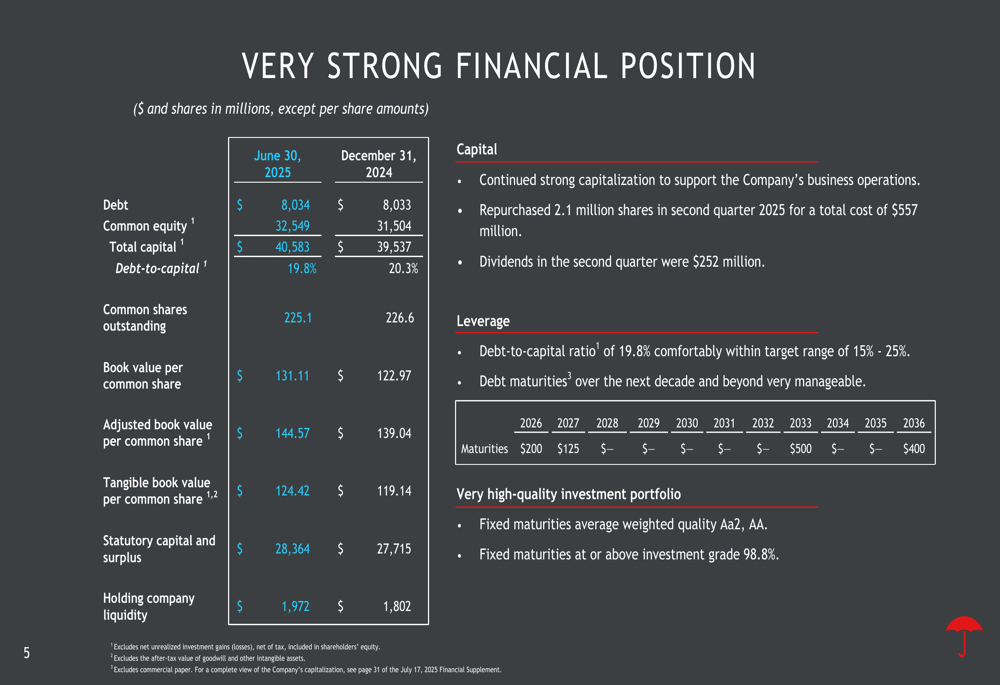

Capital Management and Financial Position

Travelers maintains a very strong financial position, with increasing capital levels and a conservative debt-to-capital ratio. The company continued to return significant capital to shareholders through share repurchases and dividends.

The following slide details the company’s financial strength:

Total (EPA:TTEF) capital increased to $40.583 billion as of June 30, 2025, up from $39.537 billion at the end of 2024. The debt-to-capital ratio improved to 19.8%, down from 20.3% at year-end 2024, remaining comfortably within the company’s target range.

Book value per common share grew to $131.11, a 20% increase compared to the prior year quarter, while adjusted book value per share increased 14% to $144.57. During the second quarter, Travelers repurchased 2.1 million shares for $557 million and paid dividends of $252 million, bringing total capital returned to shareholders to $809 million.

Forward-Looking Statements

While Travelers did not provide specific forward guidance in the presentation, the company’s strong performance across all segments suggests continued momentum for the remainder of 2025. The significant improvement in the Personal Insurance segment is particularly noteworthy, as it represents a turnaround from recent challenges in that business.

The company’s comprehensive catastrophe reinsurance program, as detailed in the appendix, positions Travelers well to manage potential storm losses during the hurricane season. With $575 million in catastrophe bonds and substantial excess-of-loss coverage, the company has taken prudent steps to mitigate catastrophe risk.

Travelers’ consistent strategy of maintaining pricing discipline while growing premiums appears to be yielding results, with renewal premium changes remaining positive across all segments while retention rates stay strong. This balanced approach, combined with the company’s strong capital position and investment portfolio, provides a solid foundation for continued performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.