European stocks drop sharply on continued tech valuation concerns

Introduction & Market Context

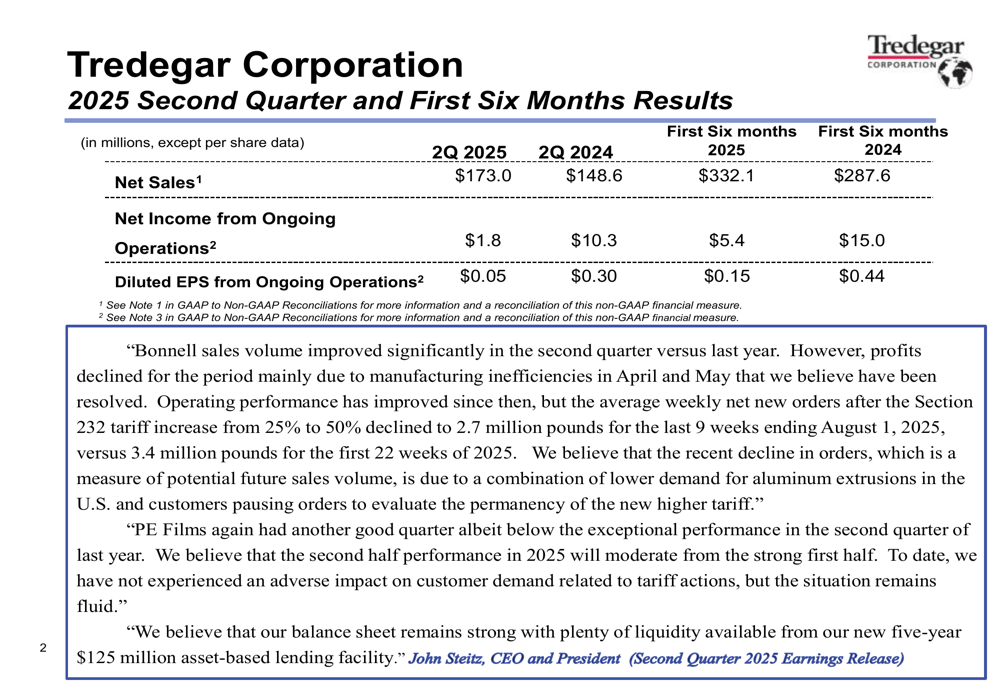

Tredegar Corporation (NYSE:TG) released its second quarter 2025 financial results on August 8, 2025, revealing a significant increase in sales that was overshadowed by substantial profit declines. The company, which specializes in aluminum extrusions and polyethylene films, reported mixed performance across its business segments amid challenging market conditions and rising costs.

The company’s stock closed at $7.78 on October 8, 2025, trading near the middle of its 52-week range of $6.45 to $9.43, reflecting investor uncertainty about Tredegar’s near-term prospects despite some positive volume trends.

Quarterly Performance Highlights

Tredegar reported second quarter 2025 net sales of $173.0 million, a 16.4% increase compared to $148.6 million in the same period of 2024. However, net income from ongoing operations plummeted to $1.8 million, down 82.5% from $10.3 million in Q2 2024. This resulted in diluted earnings per share from ongoing operations of just $0.05, compared to $0.30 in the prior-year period.

For the first six months of 2025, the company reported net sales of $332.1 million, up 15.5% from $287.6 million in the first half of 2024. Net income from ongoing operations for the six-month period was $5.4 million, down 64% from $15.0 million in the comparable period. Diluted EPS from ongoing operations for the first half was $0.15, compared to $0.44 in the first half of 2024.

Aluminum Extrusions Segment Analysis

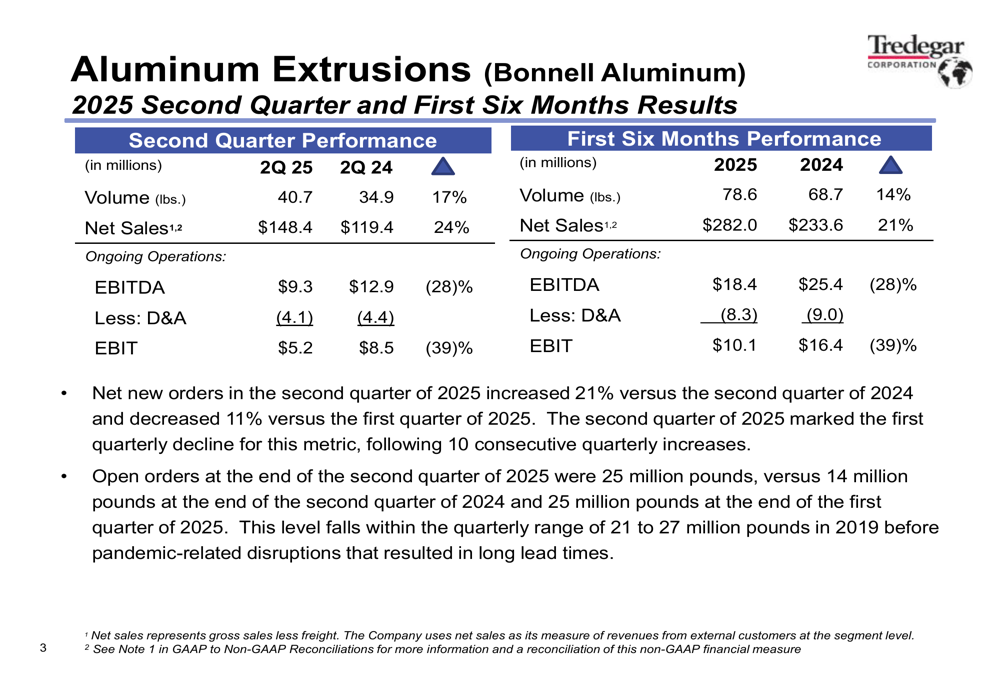

The Aluminum Extrusions segment, operating under the Bonnell Aluminum name, showed strong volume growth but declining profitability. Second quarter 2025 volume increased 17% to 40.7 million pounds, compared to 34.9 million pounds in Q2 2024. Net sales rose 24% to $148.4 million. However, EBITDA decreased 28% to $9.3 million, and EBIT fell 39% to $5.2 million.

The significant EBITDA decline of $3.6 million versus Q2 2024 was attributed to several factors, including timing of raw material costs under the FIFO method (a $0.7 million charge in Q2 2025 versus a $1.2 million benefit in Q2 2024), higher fixed costs associated with wage increases ($0.8 million), higher SG&A expenses ($0.7 million), and increased employee-related medical costs ($1.2 million). Manufacturing inefficiencies in April and May 2025 also resulted in approximately $3 million in unfavorable costs.

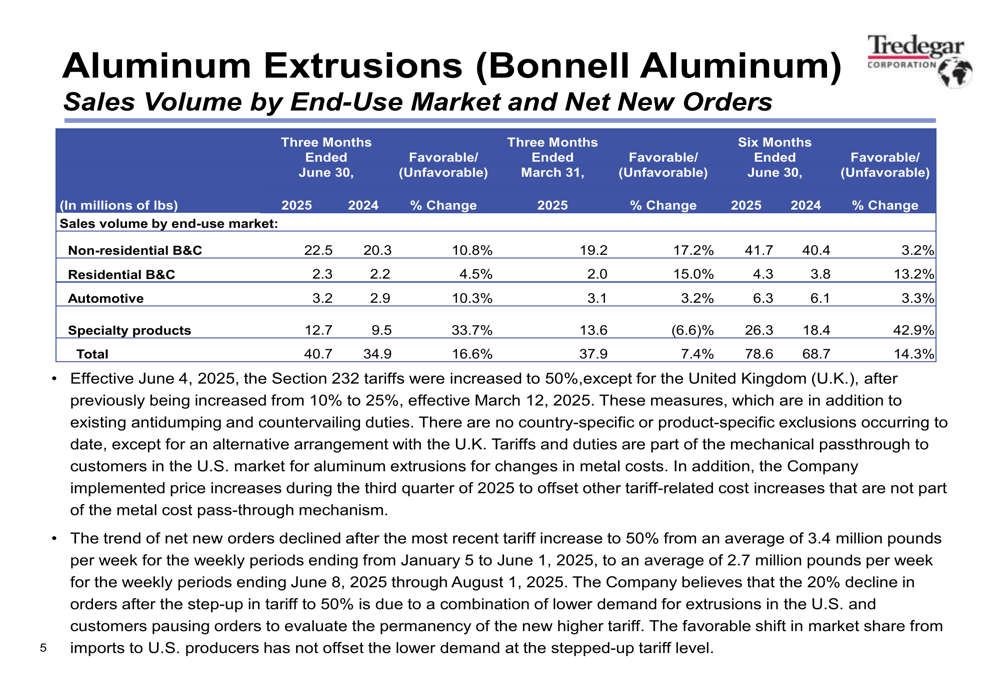

The segment experienced a 21% year-over-year increase in net new orders, though orders declined 11% compared to the previous quarter. Open orders stood at 25 million pounds, up from 14 million pounds a year earlier but level with the prior quarter. The company noted that net new orders declined from an average of 3.4 million pounds per week to 2.7 million pounds per week due to lower demand for extrusions and customers pausing orders to evaluate the impact of tariff increases under Section 232.

The company’s Aluminum Extrusions business serves diverse end markets, with non-residential building and construction representing 53% of net sales, followed by electrical and other (13%), machinery and equipment (11%), automotive (8%), consumer durables (8%), and residential building and construction (7%). This diversification provides some buffer against market-specific downturns.

PE Films Segment Performance

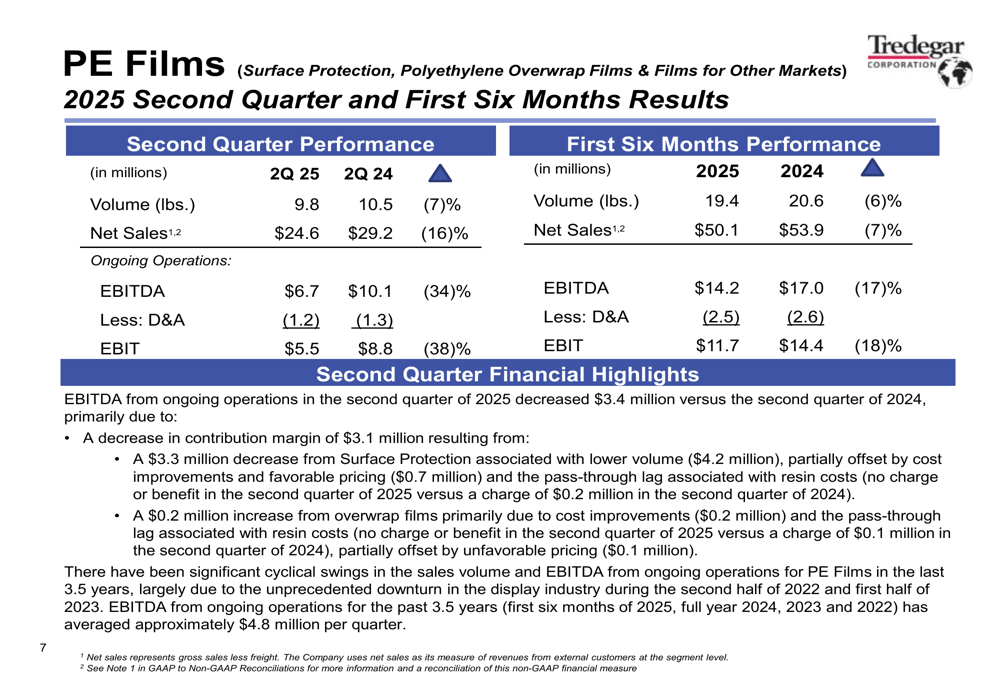

The PE Films segment faced more significant challenges in the quarter. Volume decreased 7% to 9.8 million pounds, compared to 10.5 million pounds in Q2 2024. Net sales declined 16% to $24.6 million, while EBITDA fell 34% to $6.7 million and EBIT decreased 38% to $5.5 million.

The EBITDA decrease of $3.4 million was primarily attributed to a decrease in contribution margin. The company noted that PE Films has experienced significant cyclical swings in sales volume and EBITDA from ongoing operations.

PE Films serves two primary markets: surface protection (72% of sales) and overwrap packaging (28%). Geographically, 57% of sales come from North America and 43% from Asia. The business focuses on high-value applications in display technologies, with major manufacturers as customers and primary end-use markets including LCD, LED, OLED, QLED displays, automotive displays, semiconductors, and digital signage.

Financial Position and Outlook

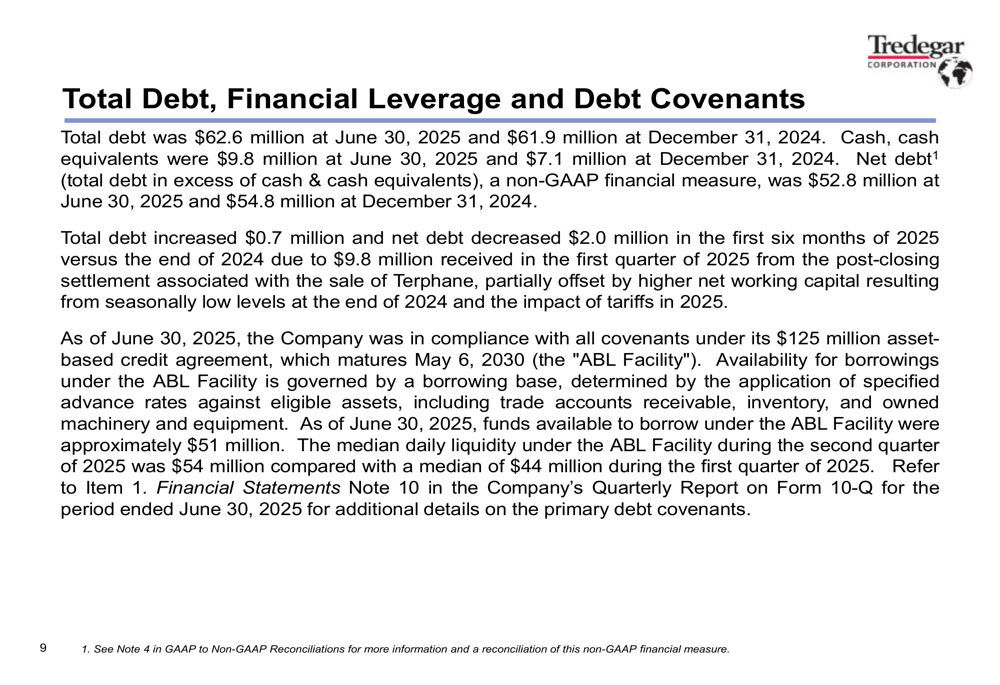

As of June 30, 2025, Tredegar reported total debt of $62.6 million and net debt (total debt minus cash and cash equivalents) of $52.8 million. The company was in compliance with all covenants under its $125 million asset-based credit agreement, with availability for borrowings of approximately $51 million. The median daily liquidity under the facility during Q2 2025 was $54 million.

For the first six months of 2025, cash flows used in operations were $2.9 million, while capital expenditures totaled $5.6 million. The company has suspended its quarterly dividend since August 3, 2023, reflecting a more conservative financial approach amid challenging market conditions.

Management projects capital expenditures of $19 million for 2025, with $17 million allocated to Aluminum Extrusions and $2 million to PE Films. This includes $5 million for Aluminum Extrusions productivity projects, $1 million for PE Films productivity projects, and $13 million to support continuity of operations across both segments.

Detailed Financial Analysis

The company’s financial performance reveals a concerning trend of margin compression despite sales growth. While net sales increased 16.4% in Q2 2025 compared to Q2 2024, the significant 82.5% decline in net income from ongoing operations indicates substantial pressure on profitability.

The Aluminum Extrusions segment, which accounts for approximately 86% of total quarterly sales, showed strong volume growth but faced significant cost pressures. The segment’s EBITDA margin declined from 10.8% in Q2 2024 to 6.3% in Q2 2025, highlighting the challenge of maintaining profitability amid rising costs.

The PE Films segment, representing approximately 14% of quarterly sales, experienced both volume and pricing pressures. The segment’s EBITDA margin decreased from 34.6% in Q2 2024 to 27.2% in Q2 2025, still representing a relatively strong margin but showing significant erosion.

Forward-Looking Statements

Tredegar faces several challenges and opportunities looking forward. In the Aluminum Extrusions segment, the Architecture Billings Index (ABI), a leading indicator for non-residential building and construction activity, suggests potential headwinds in the coming 9-12 months. The impact of increased tariffs under Section 232 also creates uncertainty, as evidenced by the recent slowdown in new orders.

For the PE Films segment, the company sees positive market trends driven by increased demand for displays and semiconductors. However, the cyclical nature of this business and recent margin pressure suggest continued volatility.

The company’s focus on productivity improvements, as evidenced by the planned capital expenditures, indicates management’s recognition of the need to address cost pressures and improve operational efficiency to restore profitability in the face of challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.