US stock futures edge lower after S&P 500 hits record high; PCE data in focus

Introduction & Market Context

TRI Pointe Homes Inc (NYSE:TPH) presented its second quarter 2025 results on July 24, 2025, revealing significant year-over-year declines across key operational and financial metrics. The homebuilder’s stock fell 2.15% to close at $35.19 following the release, reflecting investor concerns about the company’s performance amid challenging market conditions.

The presentation, led by CEO Douglas Bauer, COO Thomas Mitchell, and CFO Glenn Keeler, highlighted the company’s efforts to navigate a housing market characterized by reduced buyer activity, while maintaining a strong balance sheet and positioning for future growth.

Quarterly Performance Highlights

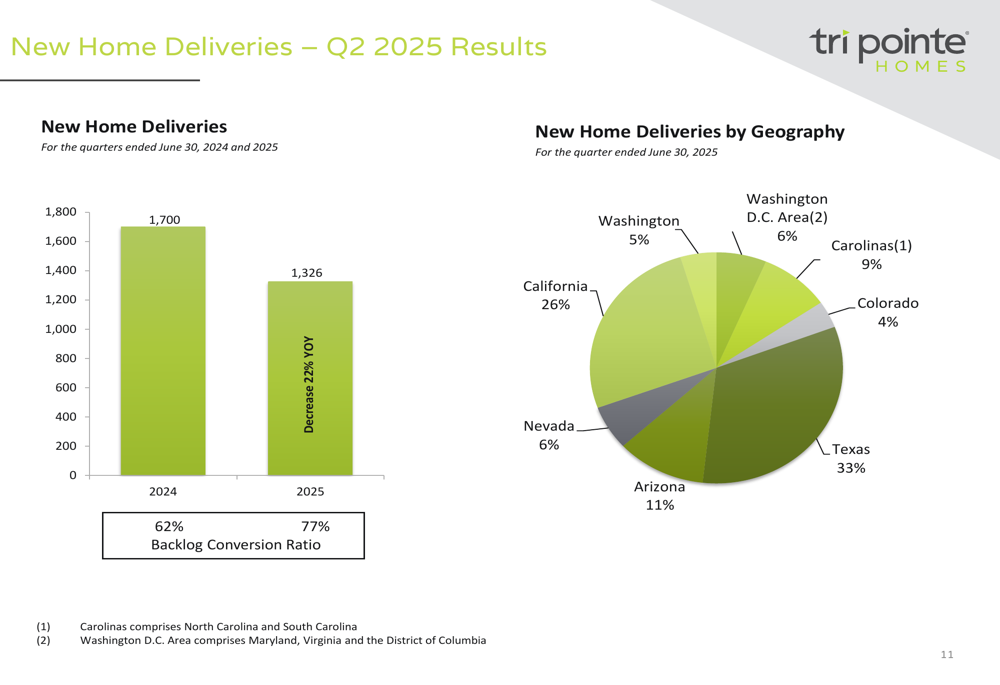

TRI Pointe Homes reported substantial year-over-year declines in its key performance metrics for Q2 2025. Net new home orders decreased 32% to 1,131 homes compared to 1,651 in Q2 2024, while home deliveries fell 22% to 1,326 units from 1,700 in the prior year period.

As shown in the following chart of quarterly deliveries by geography, the company experienced declines across most regions, with California and Texas representing the largest portions of deliveries:

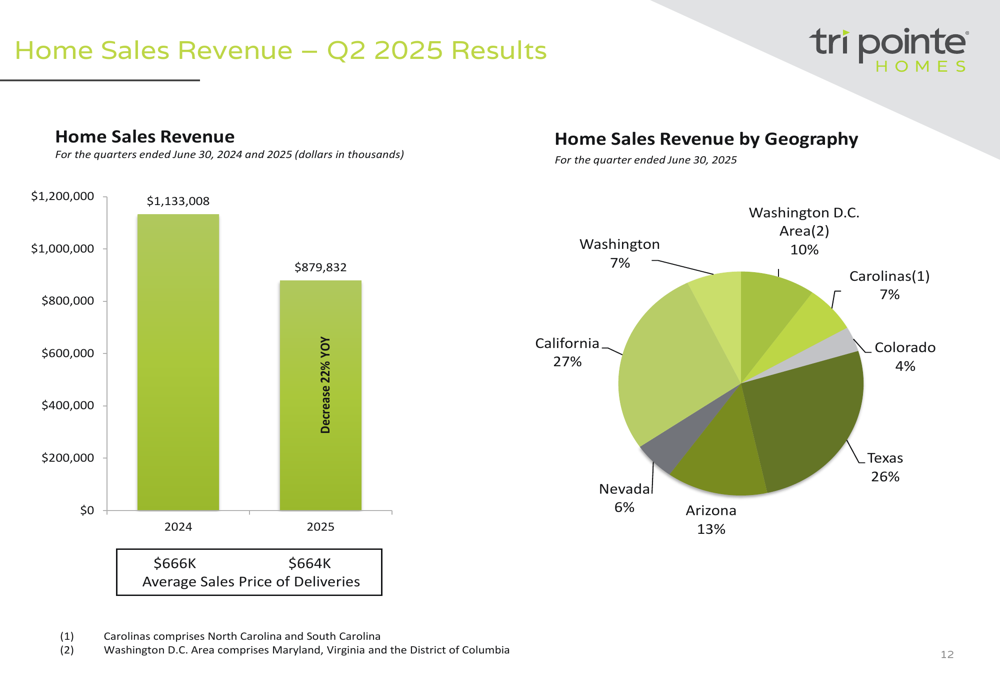

Home sales revenue declined 22% year-over-year to $879.8 million from $1.13 billion, while maintaining a relatively stable average sales price of $664,000 compared to $666,000 in Q2 2024. The geographic distribution of revenue shows California and Texas as the largest contributors:

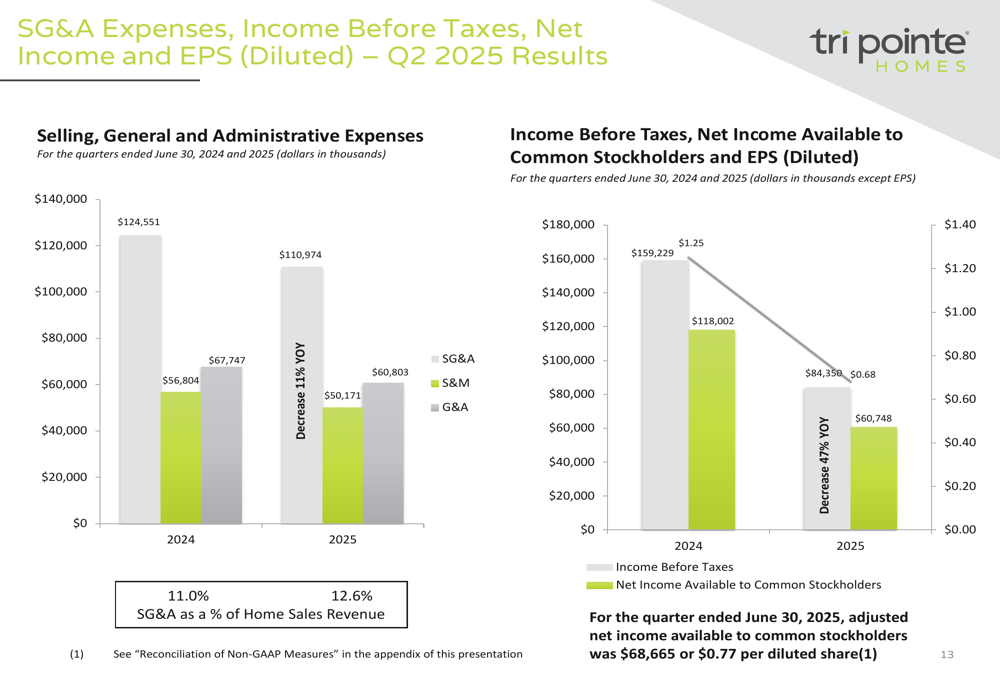

Profitability metrics showed significant pressure, with net income available to common stockholders falling 46% to $60.7 million ($0.68 per diluted share) from $118.0 million ($1.25 per diluted share) in Q2 2024. The company reported adjusted earnings per share of $0.77 for the quarter.

The company’s homebuilding gross margin decreased to 20.8% from 23.6% in the prior year period, while SG&A expenses as a percentage of home sales revenue increased to 12.6% from 11.0%, reflecting reduced operating leverage amid lower revenue.

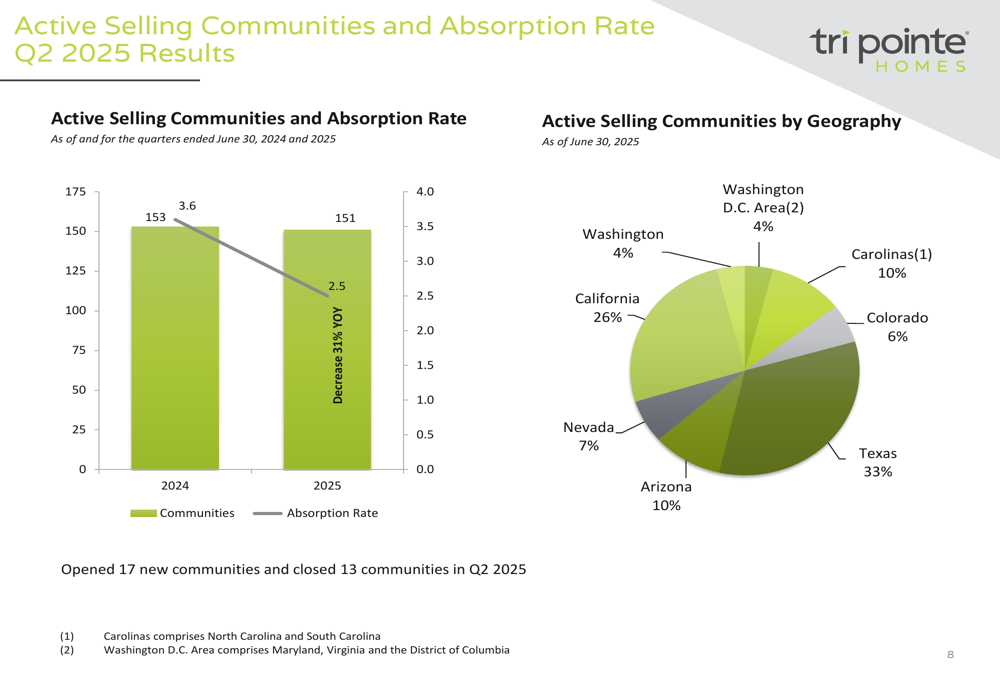

The absorption rate, which measures orders per community per month, declined to 2.5 from 3.6 in Q2 2024, reflecting slower sales velocity. The company ended the quarter with 151 active selling communities, slightly down from 153 a year earlier.

Backlog and Order Trends

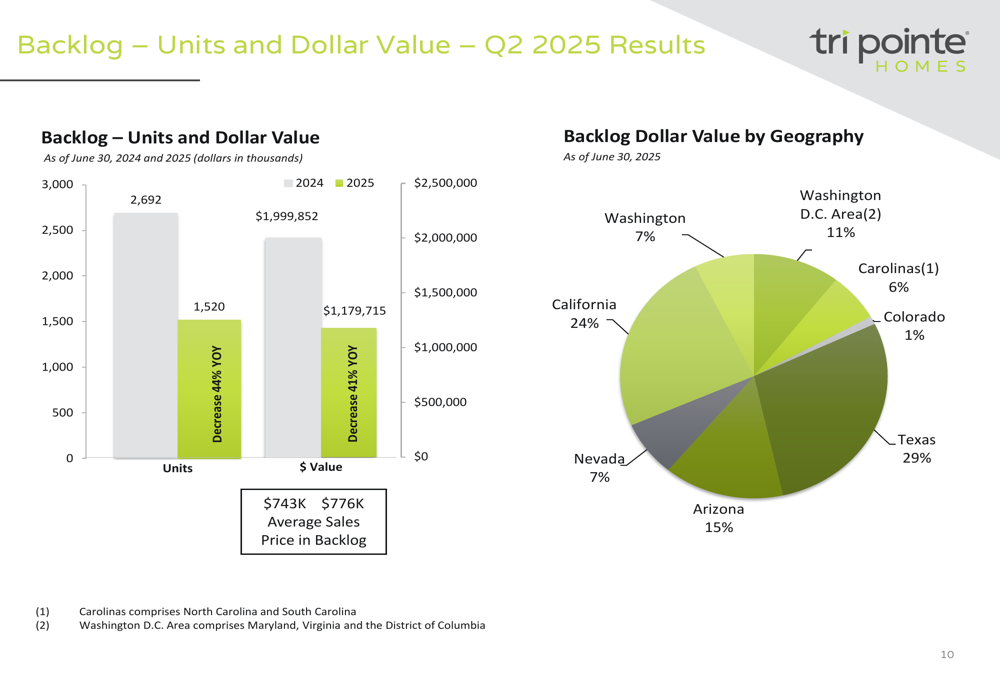

TRI Pointe’s backlog, a key indicator of future revenue, showed significant declines. Backlog units decreased 44% to 1,520 homes from 2,692 a year earlier, while backlog dollar value fell 41% to $1.18 billion from $2.00 billion. The average sales price in backlog increased to $776,000 from $743,000, partially offsetting the impact of lower unit volume.

The following chart illustrates the backlog trends and geographic distribution:

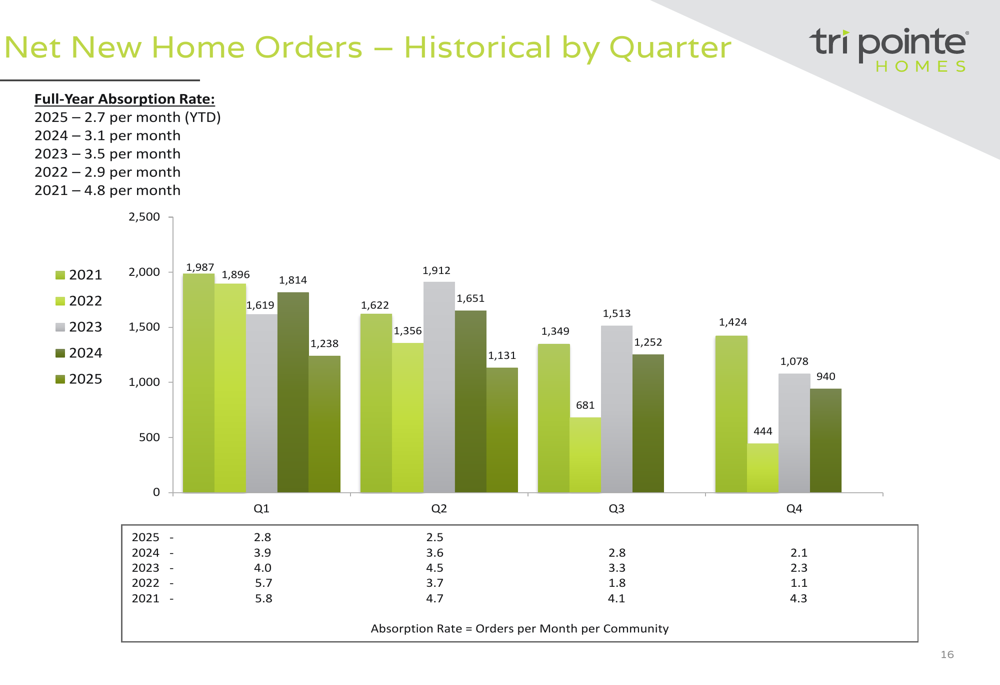

Looking at the historical order trends, TRI Pointe has experienced a general downward trajectory in net new home orders since 2021, with absorption rates also declining:

Geographic Diversification and Land Position

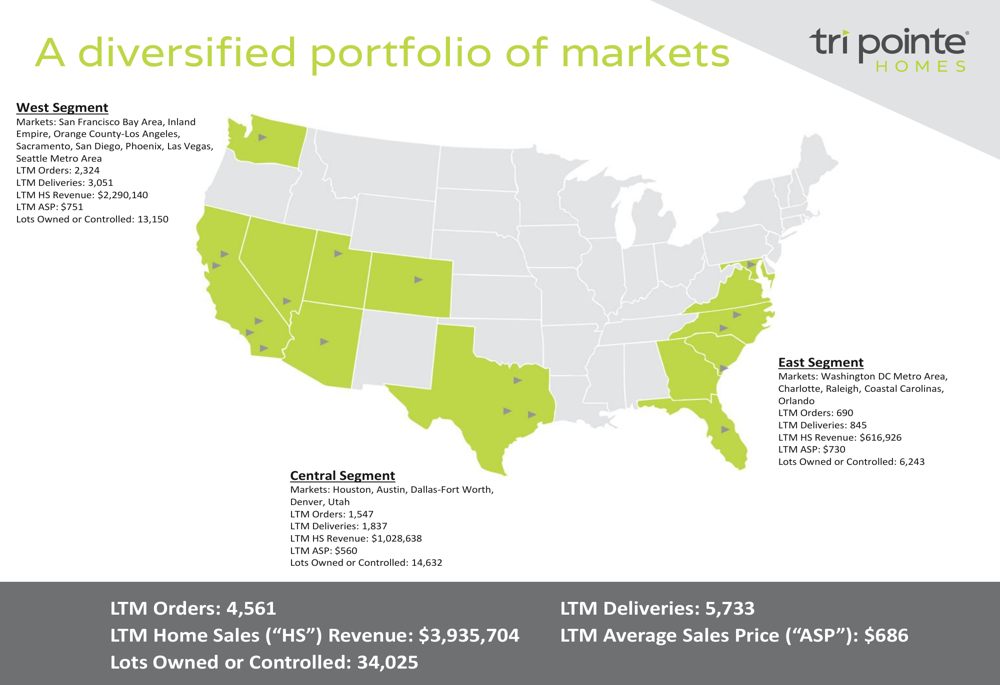

Despite the challenging quarter, TRI Pointe maintains a diversified portfolio across 18 markets in the United States, organized into three segments: West, Central, and East. The company’s market presence spans from California to the Carolinas, providing geographic diversification.

As shown in the following map and data table, the company has a significant presence in high-growth markets:

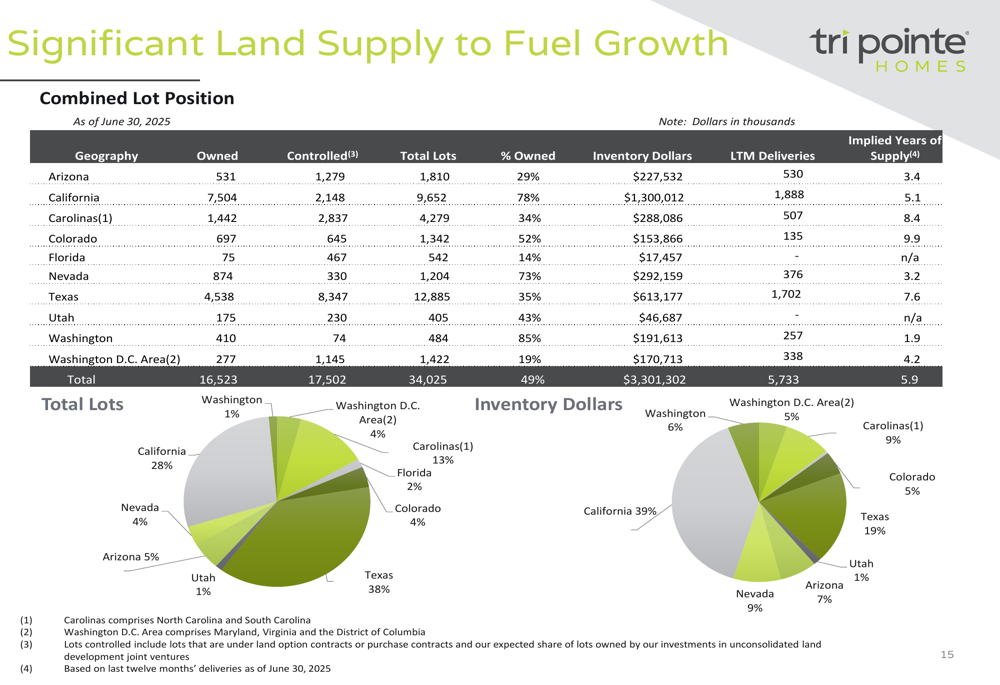

A key strength highlighted in the presentation is TRI Pointe’s substantial land position, with 34,025 lots owned or controlled as of June 30, 2025, representing approximately 5.9 years of supply based on trailing twelve-month deliveries. The company owns 49% of these lots, with the remainder under option contracts, providing flexibility.

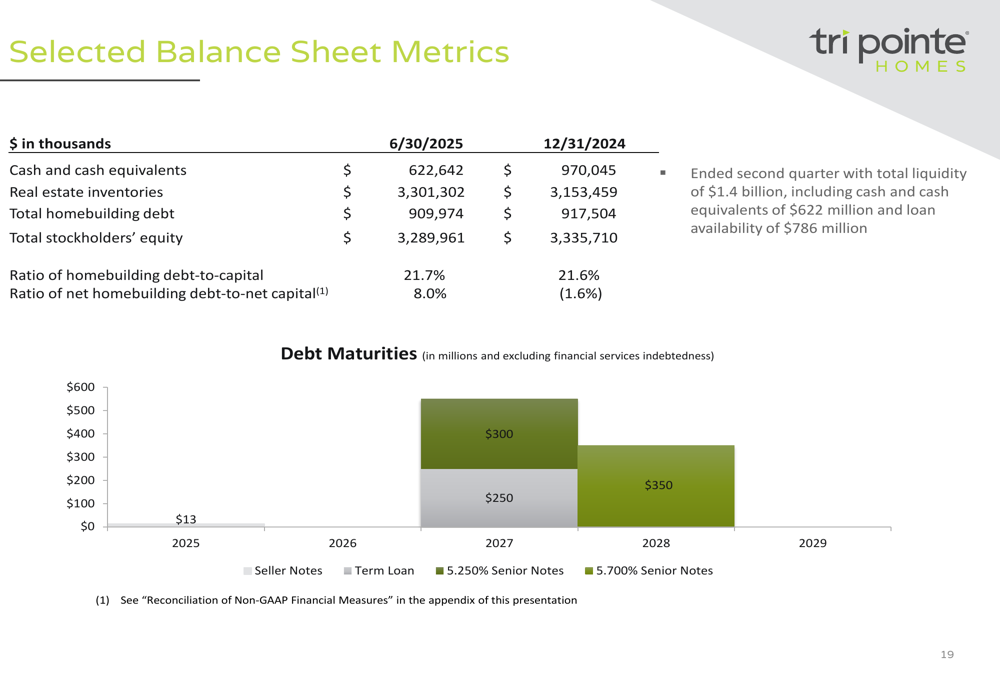

Balance Sheet and Capital Management

TRI Pointe continues to maintain a strong balance sheet with $622.6 million in cash and cash equivalents as of June 30, 2025, down from $970.0 million at the end of 2024. The company reported total liquidity of $1.4 billion, including $786 million in loan availability.

The company’s homebuilding debt-to-capital ratio stood at 21.7%, slightly up from 21.6% at the end of 2024, while the net homebuilding debt-to-net capital ratio was 8.0%, compared to -1.6% at year-end 2024.

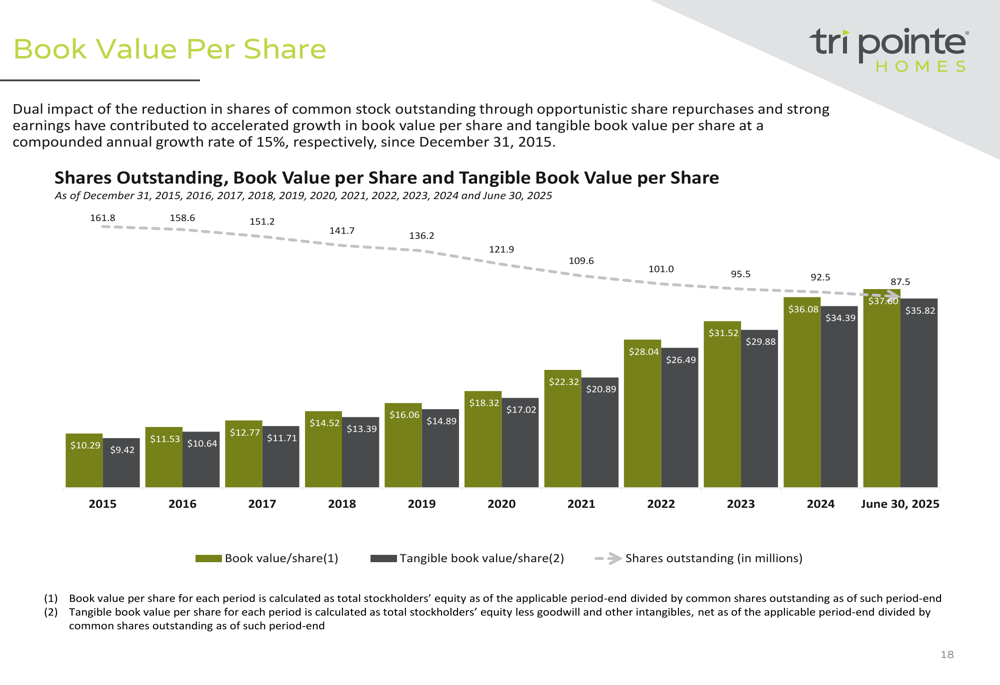

TRI Pointe has consistently increased its book value per share, reaching $36.08 as of June 30, 2025, up from $34.39 at the end of 2024. Tangible book value per share increased to $37.60 from $35.82. This growth has been supported by the company’s share repurchase program, which has reduced shares outstanding from 161.8 million in 2015 to 87.5 million as of June 30, 2025.

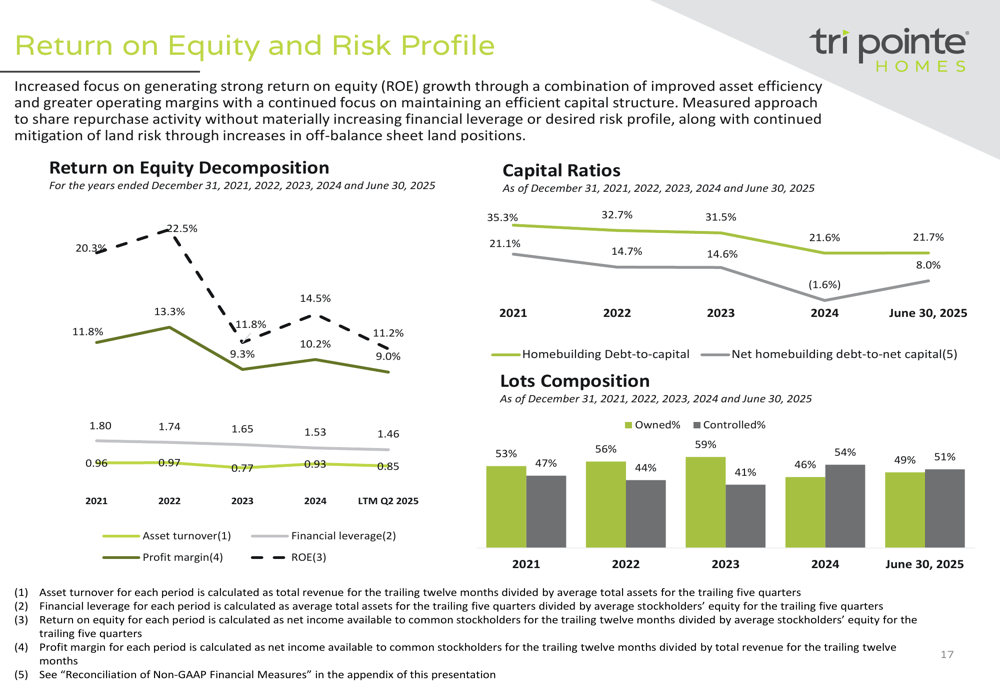

The company’s return on equity has declined from its peak of 22.5% in 2022 to 11.2% for the twelve months ended June 30, 2025, reflecting the challenging operating environment:

Forward Guidance

For the third quarter of 2025, TRI Pointe expects to deliver between 1,000 and 1,100 homes at an average sales price between $675,000 and $685,000. The company anticipates a homebuilding gross margin percentage of 20.0% to 21.0% and an SG&A expense ratio of 13.0% to 14.0% of home sales revenue.

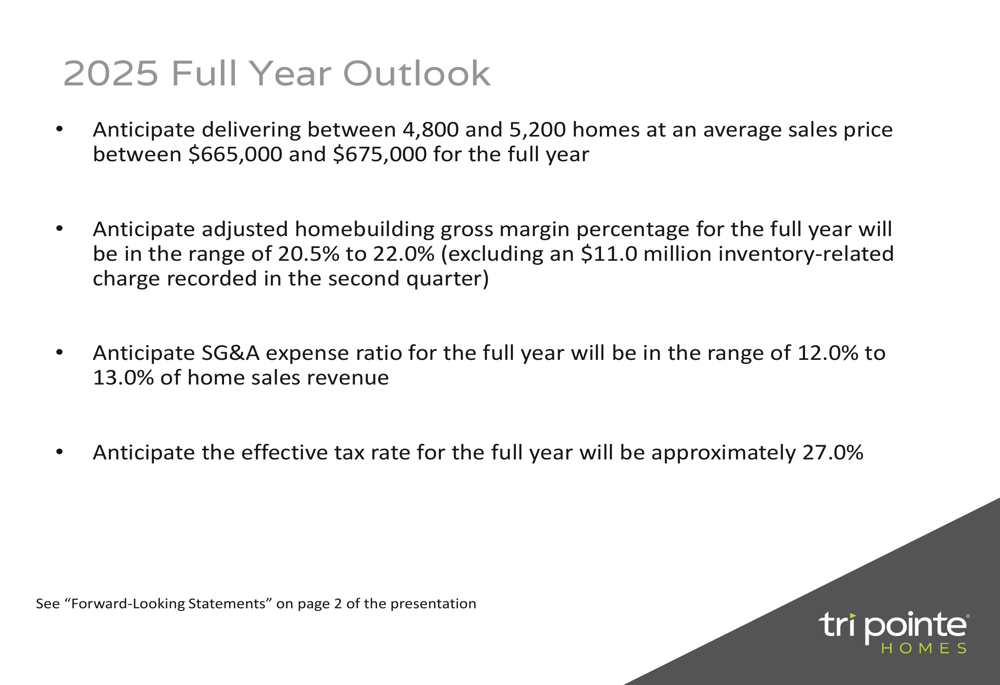

For the full year 2025, the company projects deliveries of 4,800 to 5,200 homes at an average sales price between $665,000 and $675,000. This represents a slight downward revision from the guidance provided in Q1 2025, which projected 5,000 to 5,500 deliveries. The company expects an adjusted homebuilding gross margin percentage of 20.5% to 22.0% (excluding an $11.0 million inventory-related charge recorded in the second quarter) and an SG&A expense ratio of 12.0% to 13.0%.

Conclusion

TRI Pointe Homes’ Q2 2025 results reflect the challenges facing the homebuilding industry, with significant year-over-year declines across key metrics. However, the company maintains a strong balance sheet with moderate debt levels, substantial liquidity, and a significant land position to support future growth when market conditions improve.

The slight downward revision to full-year guidance suggests that management expects the challenging environment to persist through the remainder of 2025. Investors will be watching closely to see if the company can maintain its margins and effectively manage its land position while navigating the current market slowdown.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.