S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

TripAdvisor Inc. (NASDAQ:TRIP) presented its Q1 FY 2025 results on May 7, 2025, revealing a company in transition with divergent performance across its three main business segments. The travel platform’s stock surged 11.76% following the earnings announcement, with shares trading at $14.26, reflecting investor confidence in the company’s strategic direction despite mixed results.

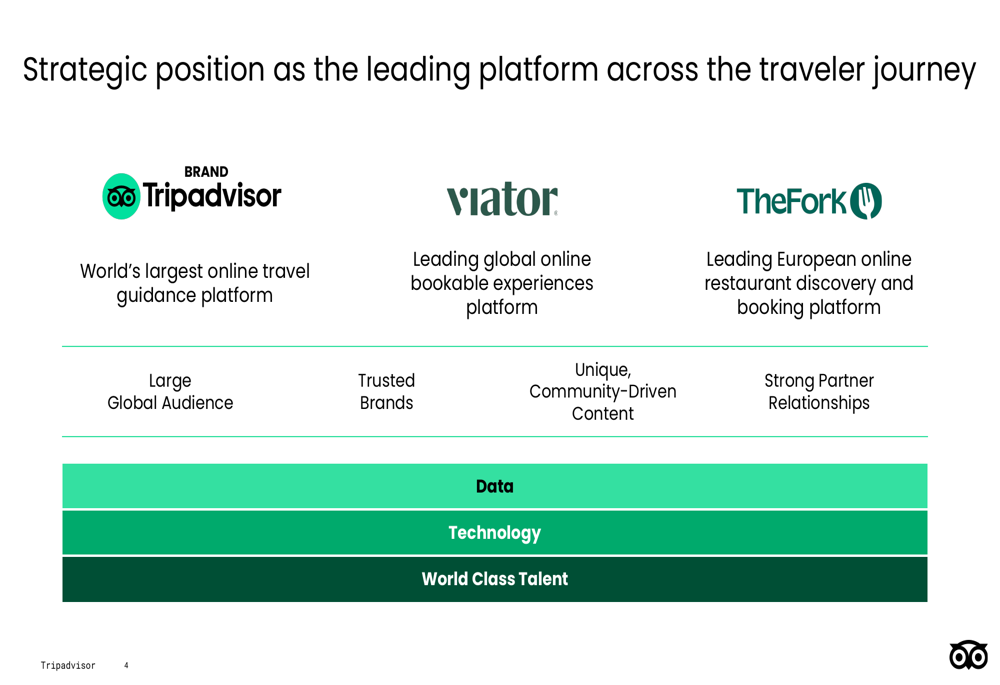

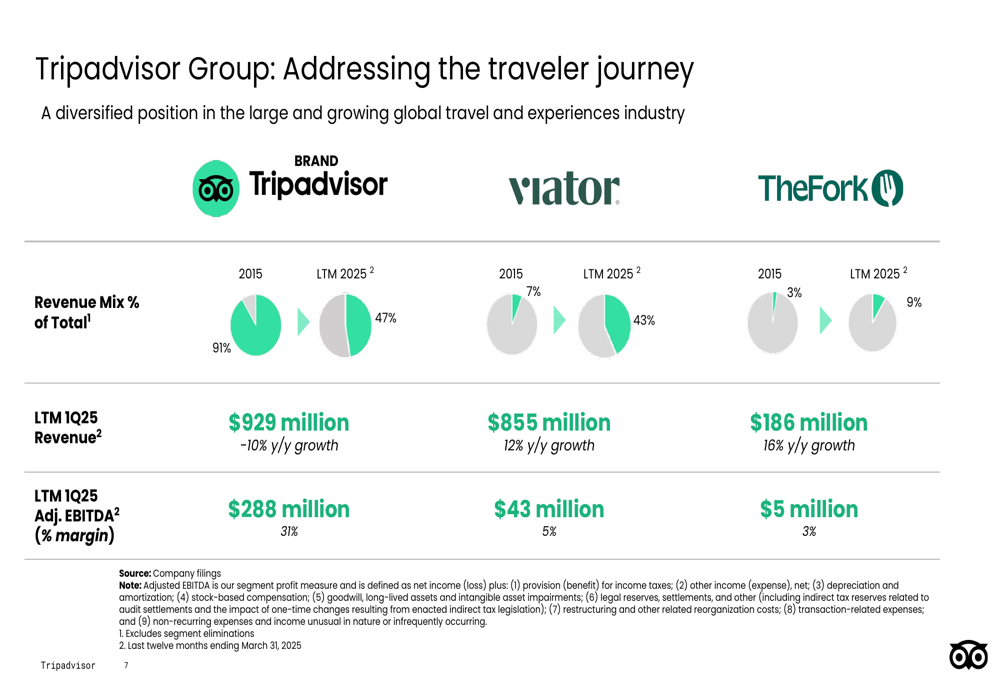

The company continues to position itself as "the world’s most trusted source for travel and experiences," operating through three distinct brands that address different aspects of the traveler journey. TripAdvisor’s presentation highlighted how its business mix has evolved significantly over the past decade, with the core TripAdvisor brand now representing less than half of total revenue.

As shown in the following strategic positioning overview, the company operates through three complementary platforms:

Quarterly Performance Highlights

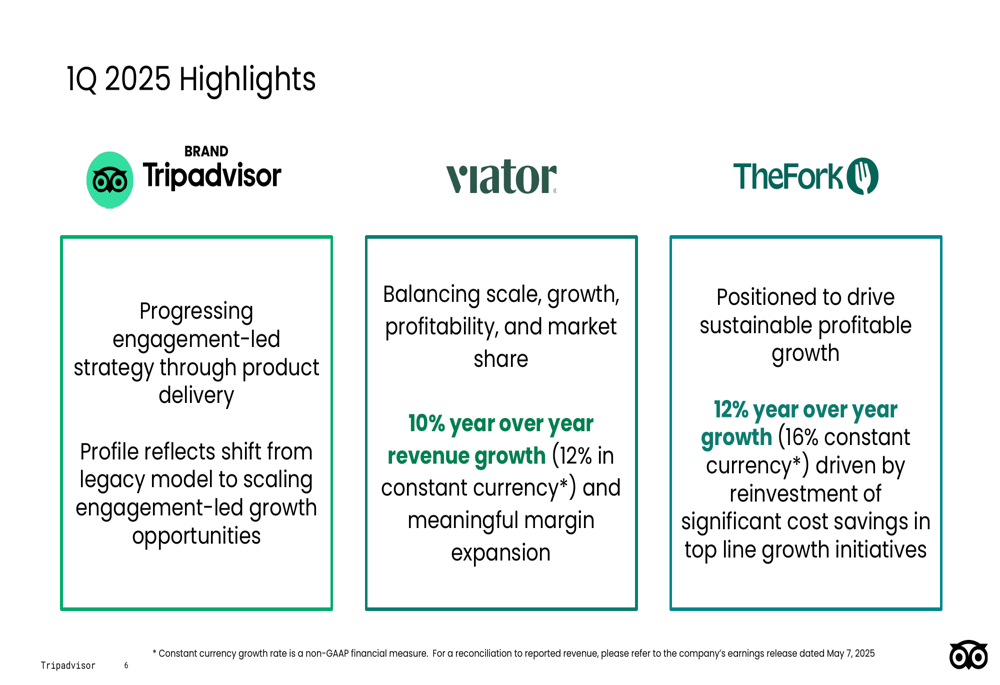

TripAdvisor reported Q1 2025 consolidated revenue of $398 million, representing a modest 1% year-over-year increase (3% in constant currency). Consolidated adjusted EBITDA reached $44 million, or 11% of revenue, slightly below the $47 million (12% margin) reported in Q1 2024. The company significantly outperformed earnings expectations with EPS of $0.14, well above the forecasted $0.04.

The following slide summarizes the key highlights across TripAdvisor’s three segments for Q1 2025:

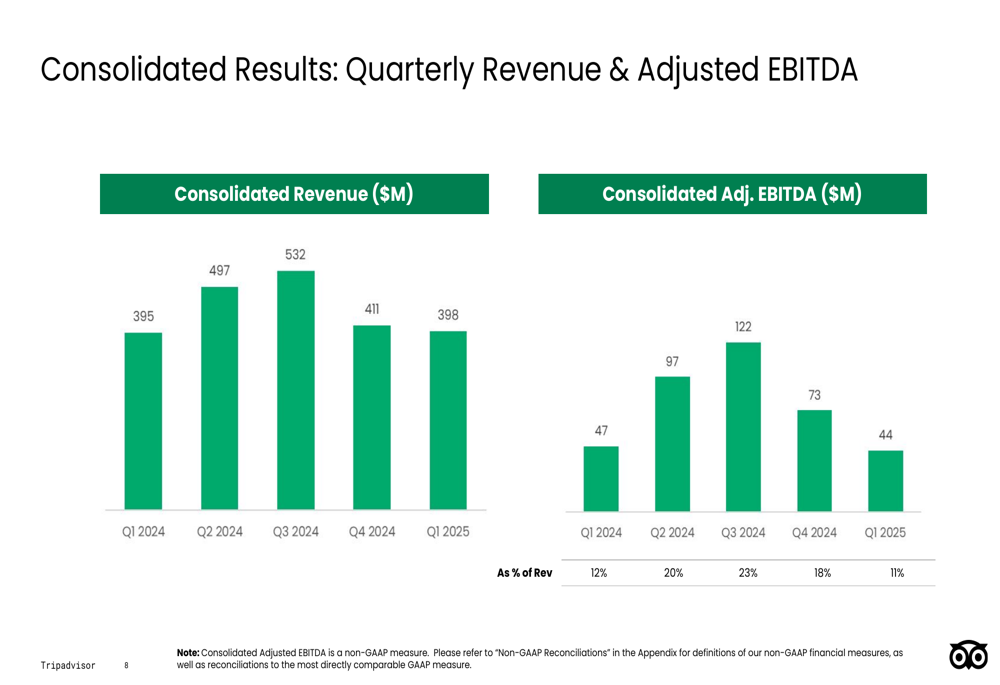

The quarterly performance data reveals clear seasonality in TripAdvisor’s business, with Q2 and Q3 typically representing peak travel seasons and delivering stronger financial results. This pattern is visible in the consolidated quarterly revenue and adjusted EBITDA trends:

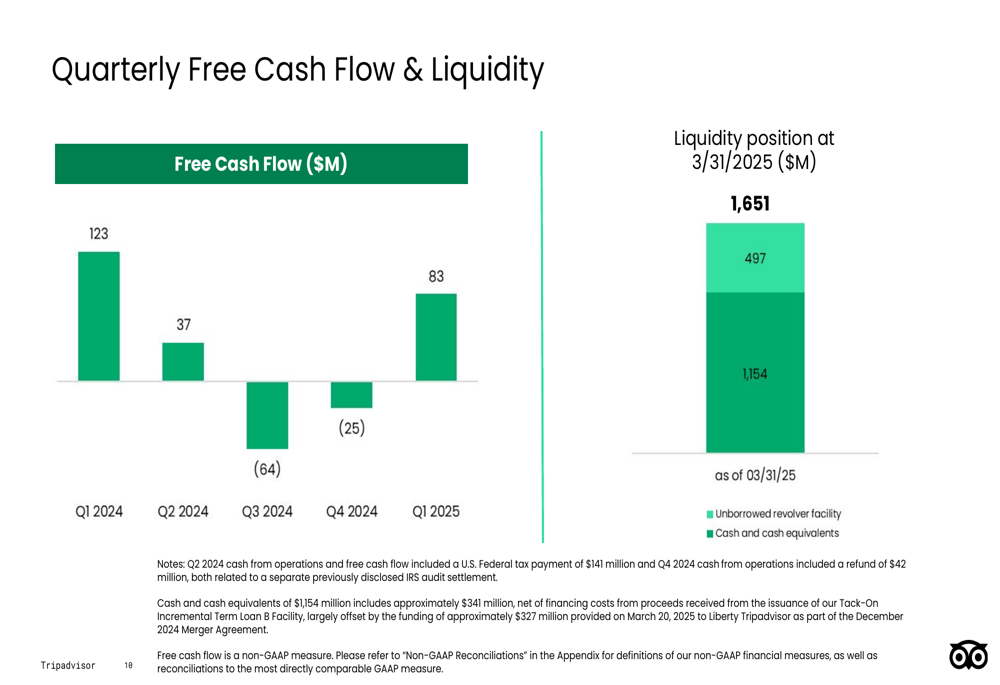

Free cash flow for Q1 2025 was $83 million, down from $123 million in the same period last year but representing a significant improvement from the negative free cash flow reported in the previous two quarters. The company maintains a strong liquidity position of $1.65 billion, including $1.15 billion in cash and cash equivalents.

Segment Analysis

Brand TripAdvisor

The core TripAdvisor brand, which focuses on travel guidance and planning, experienced an 8% year-over-year revenue decline to $219 million in Q1 2025, down from $240 million in Q1 2024. Adjusted EBITDA also decreased to $53 million from $78 million in the prior year period. Despite these challenges, the segment maintains strong profitability with a 24% adjusted EBITDA margin.

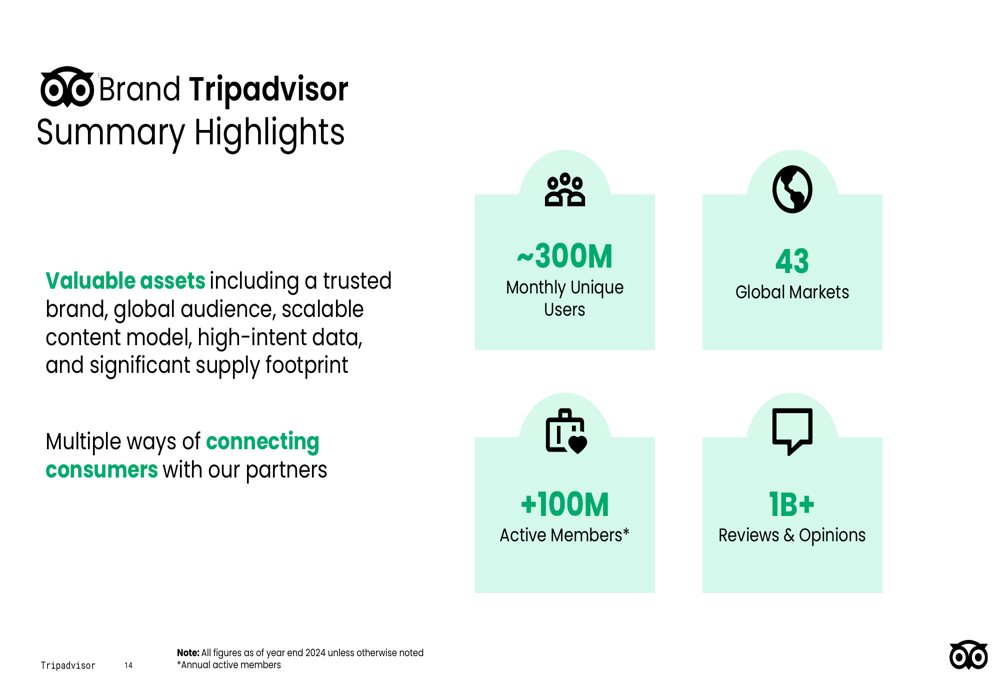

The company’s strategy for Brand TripAdvisor centers on enhancing user engagement through improved trip planning tools and personalized guidance. With approximately 300 million monthly unique users and over 1 billion reviews and opinions, TripAdvisor continues to leverage its position as a trusted source for travel information.

The following slide highlights key metrics for the Brand TripAdvisor segment:

Viator

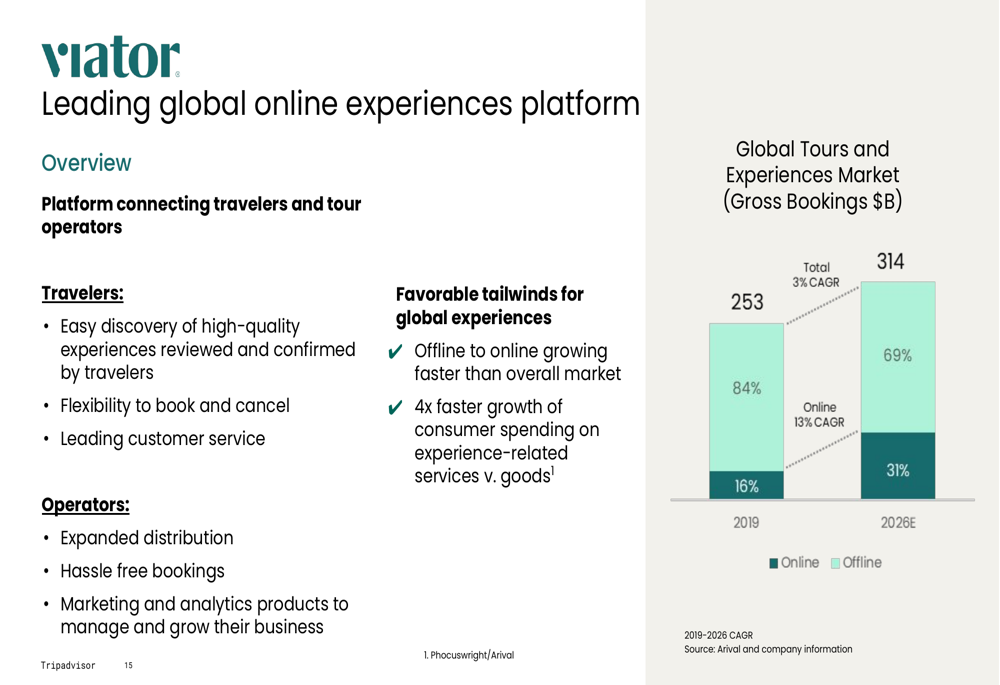

Viator, TripAdvisor’s experiences booking platform, delivered the strongest performance among the company’s segments with Q1 2025 revenue of $156 million, representing 10% year-over-year growth (12% in constant currency). While the segment reported an adjusted EBITDA loss of $18 million, this marked an improvement from the $27 million loss in Q1 2024.

The company’s presentation emphasized Viator’s market leadership position, claiming approximately four times more bookable experiences than its closest competitor. The experiences market is projected to grow at a 13% CAGR through 2026, significantly outpacing the broader travel market.

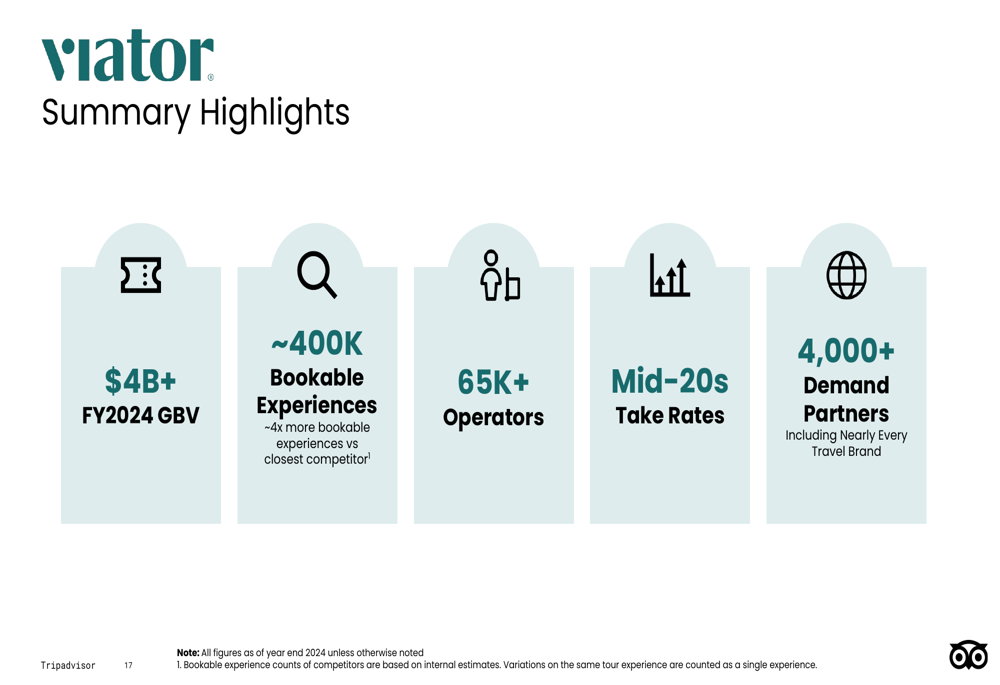

Viator’s key performance metrics demonstrate its scale and market leadership:

TheFork

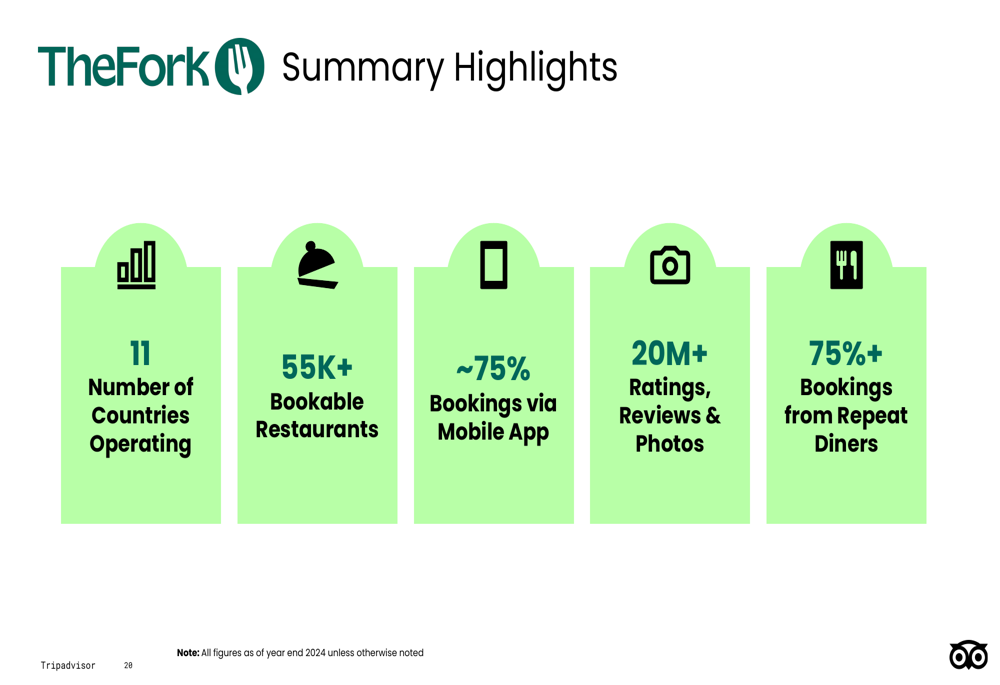

TheFork, TripAdvisor’s restaurant discovery and booking platform focused primarily on European markets, reported Q1 2025 revenue of $46 million, up 12% year-over-year (16% in constant currency). The segment posted an adjusted EBITDA loss of $3 million, slightly improved from the $4 million loss in Q1 2024.

Operating in 11 countries across Europe with over 55,000 bookable restaurants, TheFork benefits from strong user loyalty, with more than 75% of bookings coming from repeat diners. The platform’s mobile-first approach is evident, with approximately 75% of bookings occurring via its mobile app.

Strategic Positioning

TripAdvisor’s presentation revealed how dramatically the company’s revenue mix has evolved over the past decade. In 2015, the core TripAdvisor brand accounted for 91% of total revenue, with Viator at just 7% and TheFork at 3%. By Q1 2025, the TripAdvisor brand’s contribution had declined to 47%, while Viator had grown to 43% and TheFork to 9%.

This transformation reflects the company’s strategic shift toward higher-growth segments of the travel market, particularly experiences, which are growing faster than traditional hotel bookings.

CEO Matt Goldberg emphasized this strategic direction during the earnings call, noting: "Travel sentiment remains positive, with travelers continuing to plan leisure summer travel and putting experiences at the heart of their budgets." He also highlighted the company’s adaptability in serving price-sensitive travelers seeking value and choice.

Financial Outlook

TripAdvisor maintained its full-year guidance of 5-7% revenue growth, with Q2 consolidated revenue growth expected between 5-8%. The Viator segment is projected to achieve mid-teens growth in experiences booked, with the company targeting OTA-like margins for Viator in the long term.

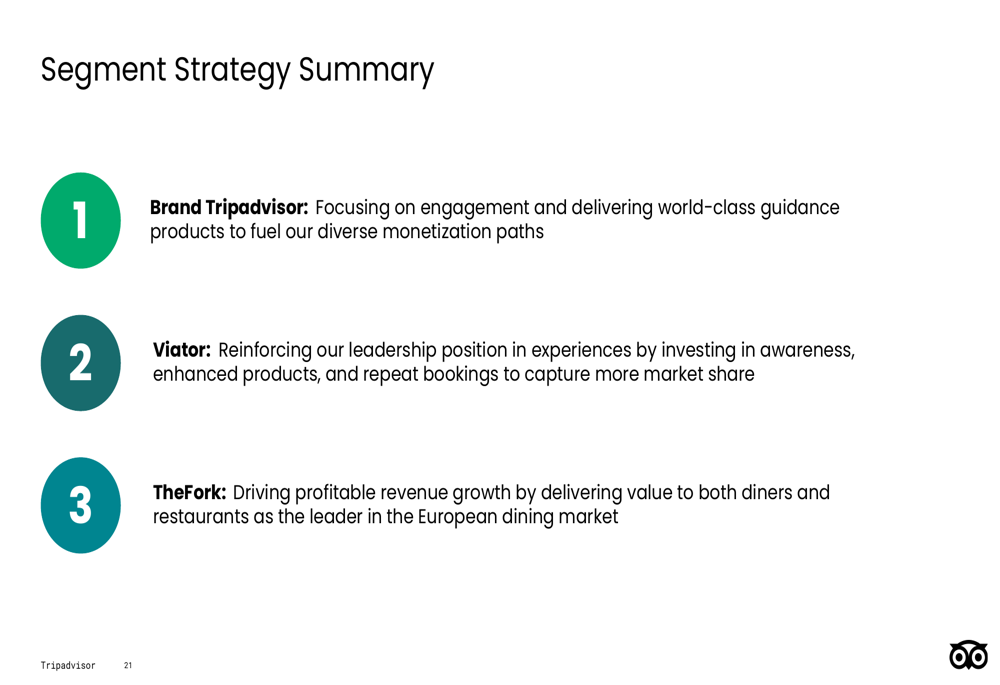

The company’s segment strategy summary outlines distinct approaches for each brand:

While macroeconomic pressures and shifts in international travel patterns remain potential challenges, TripAdvisor’s diversified business model provides some resilience against market fluctuations. The company’s strong liquidity position also offers flexibility to navigate changing market conditions and invest in growth opportunities.

As TripAdvisor continues its strategic evolution, investors will be watching closely to see if Viator’s strong growth trajectory can offset the declining performance of the core TripAdvisor brand, and whether TheFork can achieve sustainable profitability in the competitive restaurant booking market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.