Legrand hits record high after agreeing $1.1bn deal to acquire Avtron Power

Introduction & Market Context

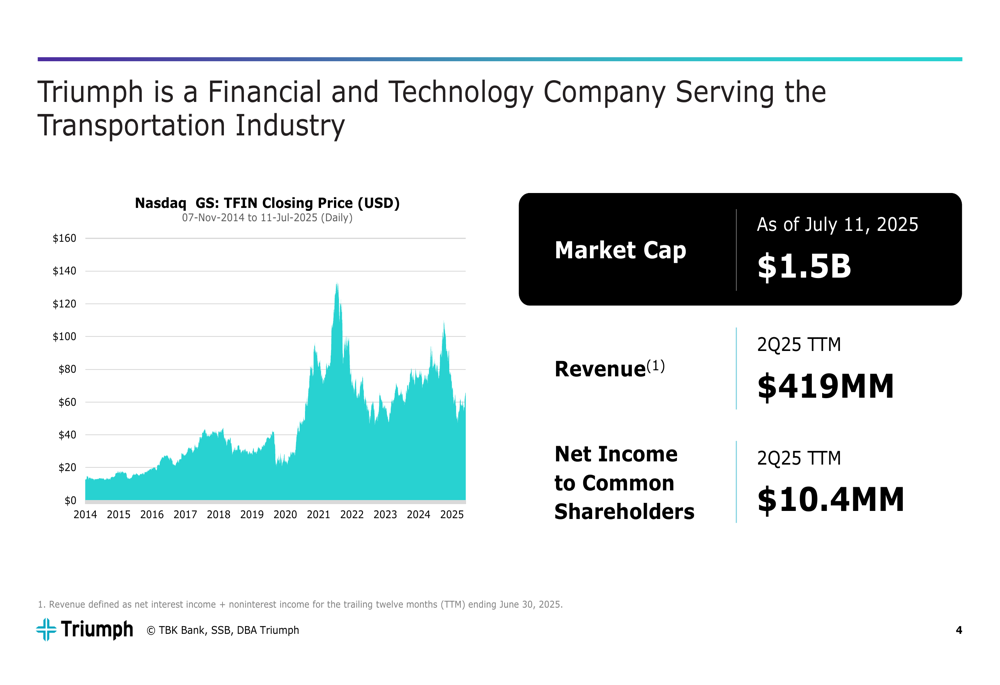

Triumph Financial (NASDAQ:TFIN) presented its July 2025 investor deck showcasing its recovery from a challenging first quarter and outlining its strategic positioning in the freight and logistics industry. The company, which serves a $990 billion U.S. trucking market that represents 3.7% of U.S. GDP, has seen its market capitalization grow to $1.5 billion as of July 11, 2025, up from $1.04 billion reported after Q1 results.

The stock has shown significant recovery since its post-Q1 earnings drop, currently trading at $62.15, well above the $44.68 level seen after the company missed revenue forecasts in Q1. This rebound suggests renewed investor confidence in Triumph’s multi-segment strategy spanning factoring, payments, and intelligence services.

Executive Summary

Triumph Financial reported trailing twelve-month revenue of $419 million and net income to common shareholders of $10.4 million as of Q2 2025. The company positions itself as a technology-enabled financial services provider focused on the transportation industry, with three core business segments.

As shown in the following overview of Triumph’s financial metrics and stock performance:

The company’s strategy centers on creating an interconnected ecosystem of services for the freight and logistics industry, where it has established itself as the second-largest transportation factor in North America. Triumph’s network now encompasses 533 brokers, 57 factors, 74 shippers, and over 174,000 carriers, creating what the company describes as "the only true Network in brokered freight."

Strategic Initiatives

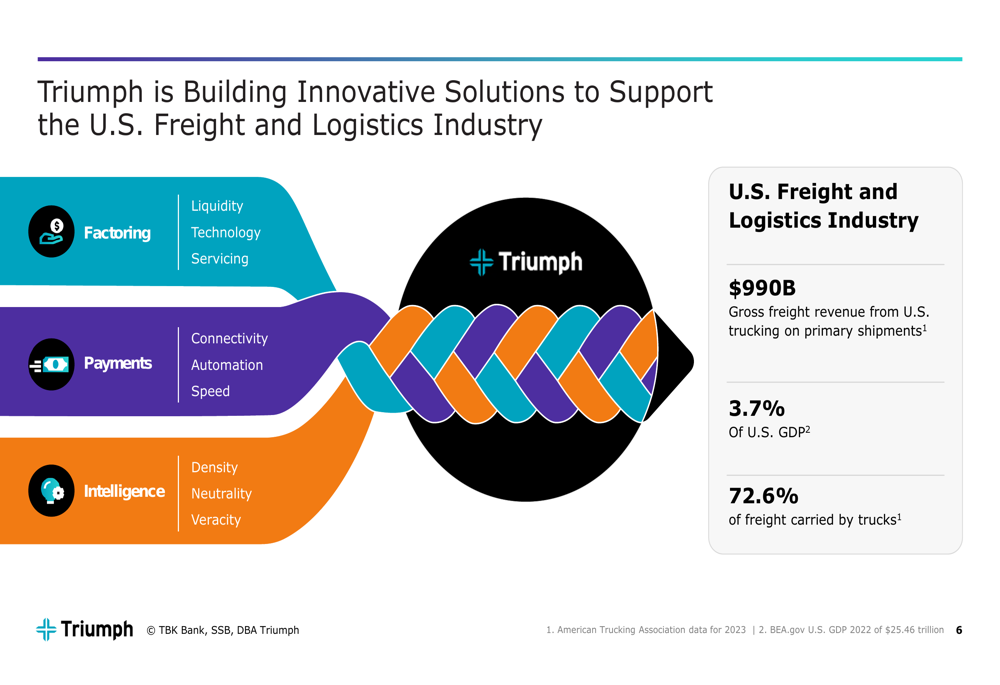

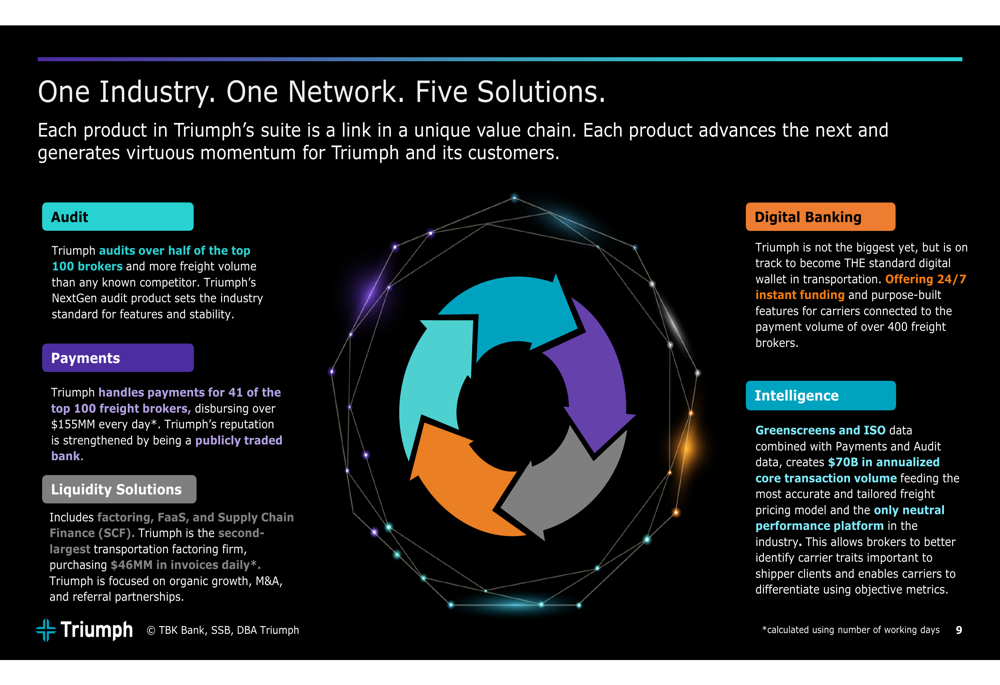

Triumph’s business model is built around three core segments: Factoring, Payments, and Intelligence. Each segment targets specific needs within the transportation industry while creating synergies across the company’s ecosystem.

The following illustration shows how Triumph’s solutions address different aspects of the freight and logistics industry:

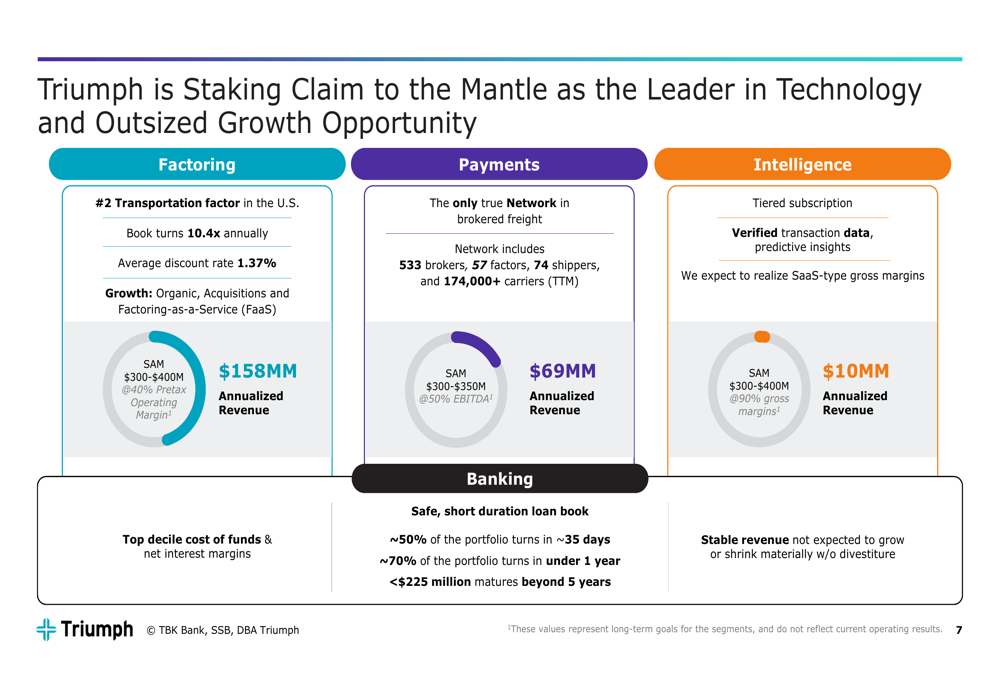

The company has identified substantial addressable markets for each segment, with long-term margin targets that reflect the different economics of each business line. Factoring, the most established segment, generates $158 million in annualized revenue with a serviceable addressable market of $300-400 million and targeted 40% pretax operating margins. The Payments segment produces $69 million in annualized revenue against a $300-350 million addressable market with 50% EBITDA margin goals. The emerging Intelligence segment, with $10 million in annualized revenue, targets a $300-400 million market with SaaS-type gross margins of 90%.

This multi-segment approach is illustrated in the company’s growth opportunity slide:

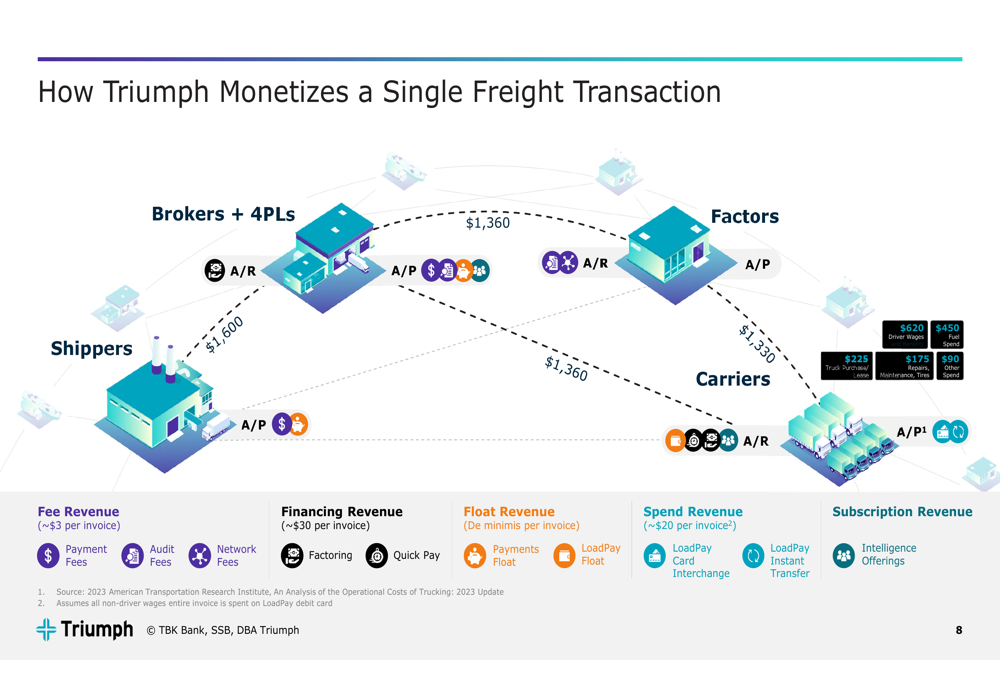

A key strength of Triumph’s business model is its ability to monetize multiple aspects of a single freight transaction. The company generates approximately $3 per invoice in fee revenue, $30 per invoice in financing revenue, and $20 per invoice in spend revenue, along with additional float revenue and subscription fees.

The following diagram illustrates how Triumph extracts value across the freight transaction ecosystem:

Detailed Financial Analysis

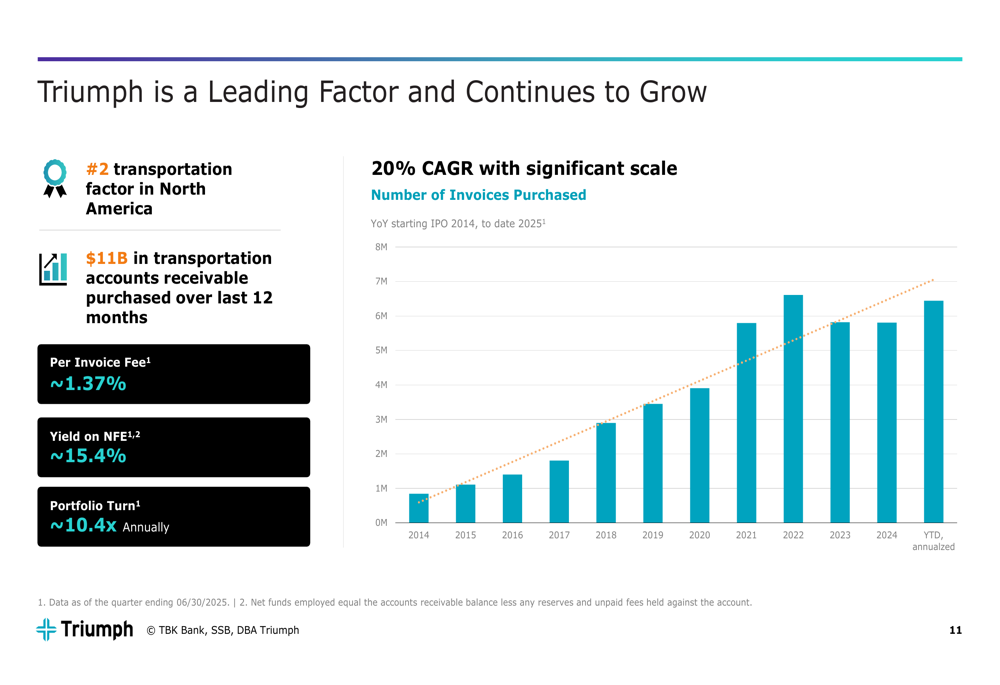

Triumph’s factoring business has shown consistent growth, with a 20% CAGR in invoices purchased from 2014 to 2025. As the second-largest transportation factor in North America, the company purchased $11 billion in transportation accounts receivable over the last 12 months.

The factoring segment maintains an average discount rate of 1.37% with portfolio turns of approximately 10.4x annually, yielding approximately 15.4% on net funds employed. This performance represents a significant improvement from the challenges noted in Q1 2025, when the company faced headwinds in the freight sector.

The following chart demonstrates Triumph’s growth in factoring volume:

The payments segment has also shown strong performance, with fees increasing 12-13% according to the Q1 2025 earnings report. The investor deck highlights that Triumph now handles payments for over 400 freight brokers, with its Digital Wallet LoadPay generating $350 per account that is 90 days or older.

Competitive Industry Position

Triumph has positioned itself at the center of the freight and logistics ecosystem through its integrated network of solutions. The company’s "One Industry. One Network. Five Solutions" approach combines Audit, Digital Banking, Intelligence, Liquidity Solutions, and Payments into a cohesive offering.

This integration is illustrated in the following network diagram:

The company’s Intelligence segment represents a significant competitive advantage, covering $70 billion in annual verified freight transactions, which accounts for 63% of brokered freight transaction volume. This data density provides Triumph with unique insights that it monetizes through tiered subscription services.

The value of Triumph’s network is further enhanced by strategic acquisitions, including greenscreens.ai and ISO, which have strengthened the company’s intelligence offerings. These acquisitions have helped Triumph build a more comprehensive solution set while expanding its market reach.

Forward-Looking Statements

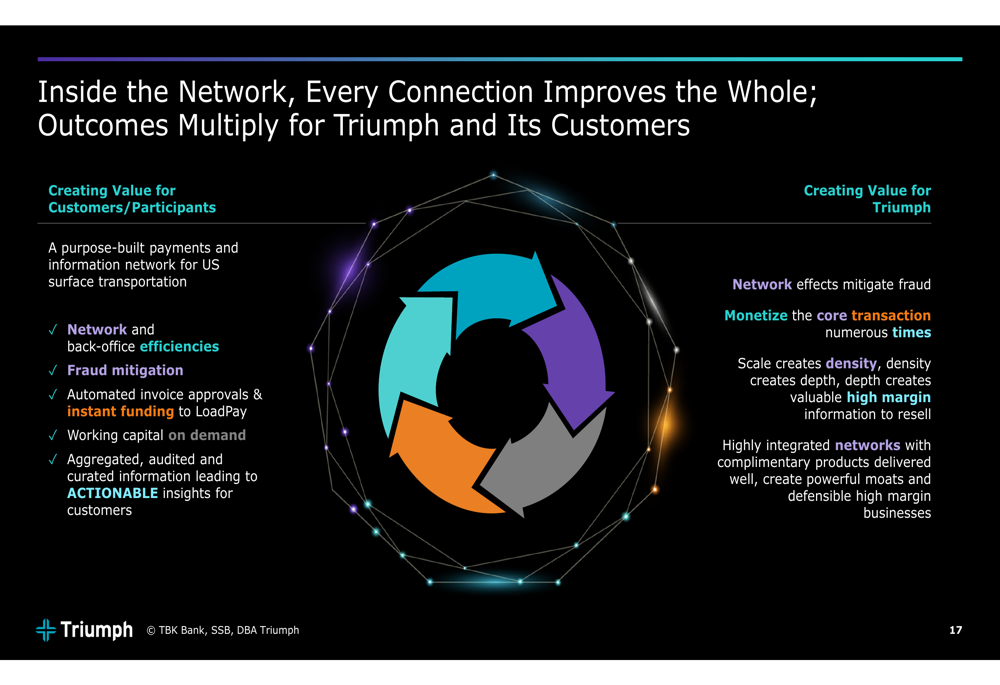

Looking ahead, Triumph is focused on scaling its Intelligence segment, which the company believes offers the highest margin potential. The presentation emphasizes the scalability of this business line and its ability to provide verified transaction data and predictive insights to network participants.

As shown in the following slide about the value of Triumph’s network:

The company is also expanding its Factoring-as-a-Service (FaaS) offering, which leverages Triumph’s technology infrastructure to create a scalable, monetizable asset. This initiative represents a shift from traditional factoring to a more technology-driven approach that can potentially accelerate growth.

While the presentation paints an optimistic picture of Triumph’s prospects, investors should note the challenges identified in the Q1 2025 earnings report, including persistent freight market headwinds and tariff uncertainties. The company’s ability to execute on its multi-segment strategy while navigating these industry challenges will be critical to sustaining its recent stock price recovery and delivering on the growth opportunities outlined in the investor deck.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.