Legrand hits record high after agreeing $1.1bn deal to acquire Avtron Power

Introduction & Market Context

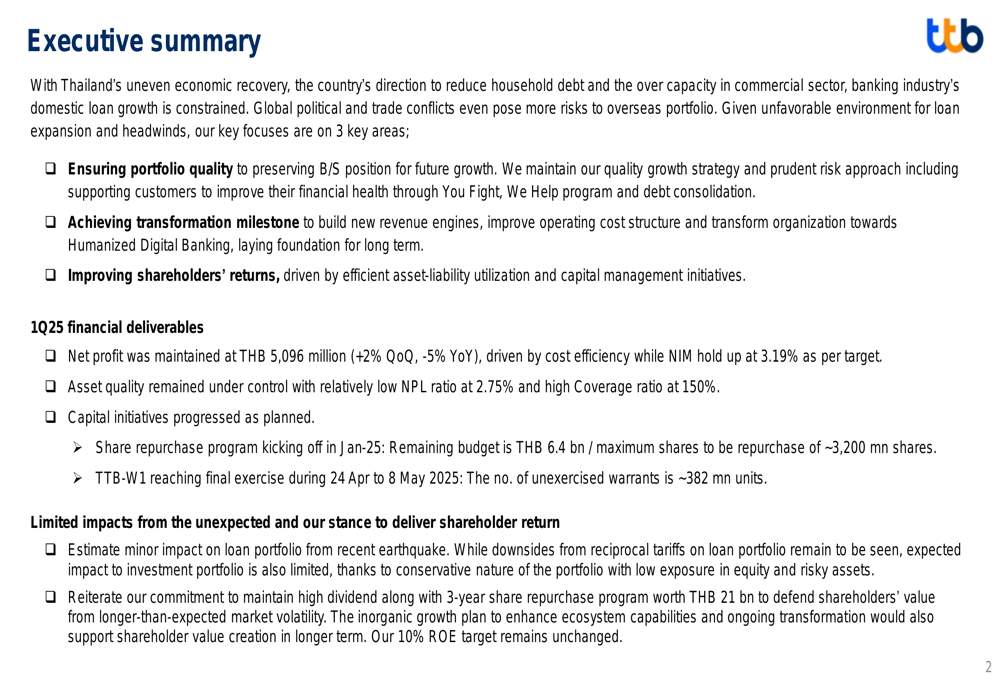

TTB Thanachart Bank (TTB) has released its Q1 2025 financial performance presentation, highlighting the bank’s resilience amid Thailand’s uneven economic recovery and global uncertainties. The bank reported a net profit of THB 5,096 million, representing a 2% increase quarter-on-quarter but a 5% decrease year-on-year, as it continues its transformation journey toward becoming "the most recommended bank" in Thailand.

The presentation, delivered on April 18, 2025, emphasized TTB’s strategic focus on ensuring portfolio quality, achieving transformation milestones, and improving shareholder returns in a challenging economic environment. The bank noted limited expected impact from a recent earthquake, while maintaining a cautious outlook regarding potential effects from reciprocal tariffs.

As shown in the following executive summary slide, TTB is maintaining its 10% ROE target while implementing a share repurchase program and managing its capital position:

Quarterly Performance Highlights

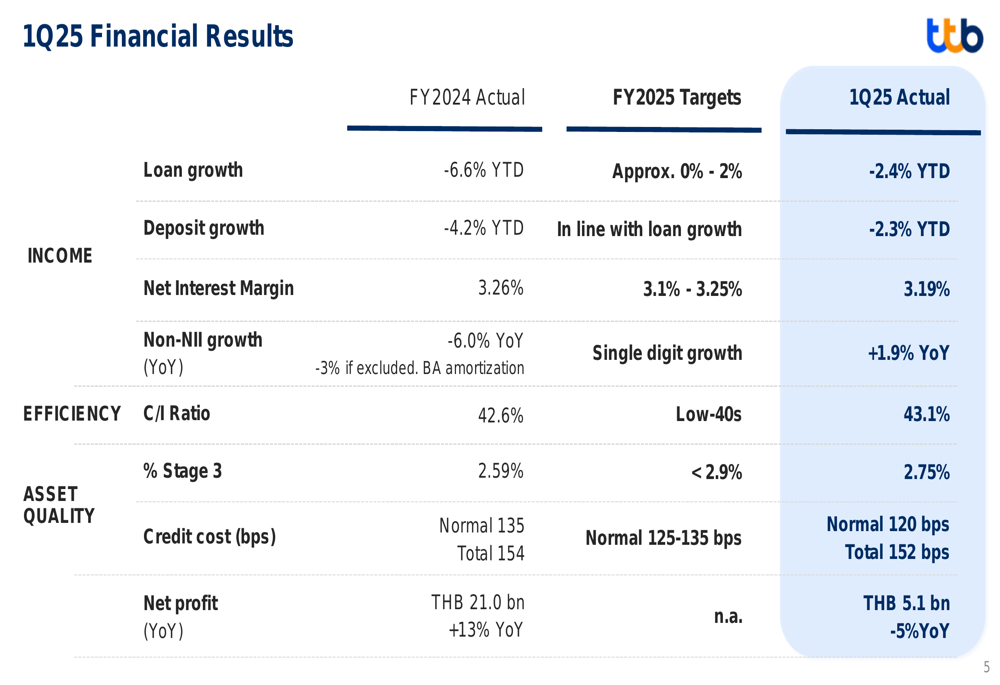

TTB’s Q1 2025 financial results show a mixed performance against the bank’s full-year targets. Total (EPA:TTEF) loans declined by 2.4% year-to-date, while deposits decreased by 2.3%, reflecting the bank’s strategic decision to optimize its balance sheet structure. The net interest margin (NIM) stood at 3.19%, down from 3.26% in FY2024, but still within the bank’s target range of 3.1-3.25%.

The bank maintained strong asset quality with a Stage 3 loan ratio of 2.75%, slightly up from 2.59% at the end of 2024 but still below the target ceiling of 2.9%. The credit cost normalized at 120 basis points, an improvement from the 135 basis points recorded in the previous year.

The comprehensive financial performance metrics are illustrated in the following slide:

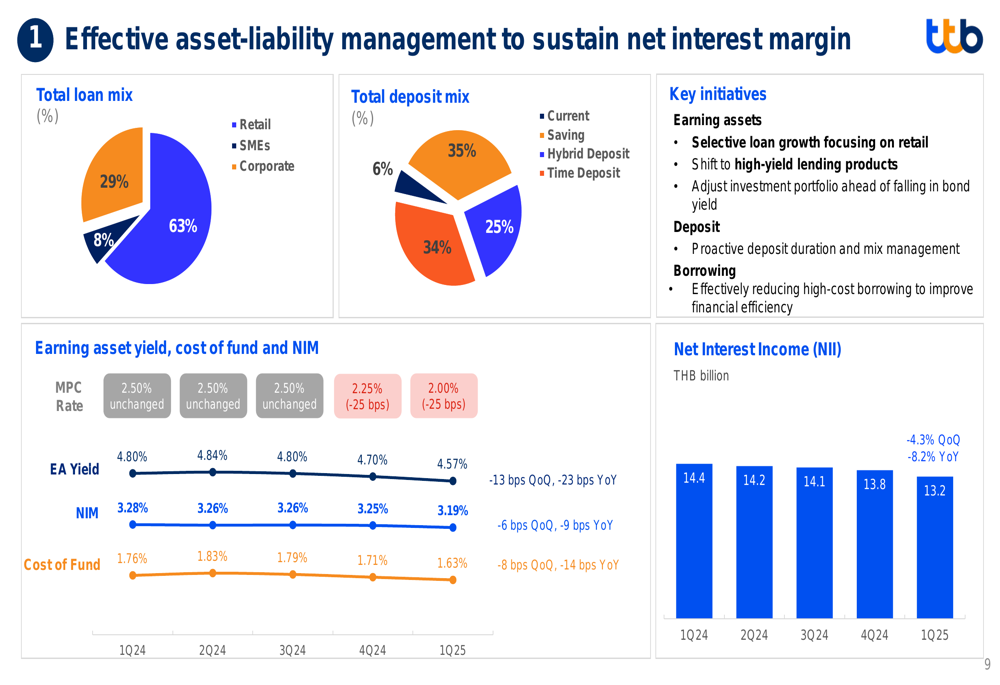

TTB’s net interest income decreased from THB 14.4 billion in Q1 2024 to THB 13.2 billion in Q1 2025, primarily due to margin compression as the cost of funds declined at a slower pace than earning asset yields. This trend is visualized in the asset-liability management slide:

Strategic Initiatives

TTB continues to execute its transformation strategy, which has evolved from the 2019 merger integration to the current phase of business model transformation. The bank has shifted its loan portfolio significantly toward retail lending, which now comprises 61% of total loans compared to 31% in 2018, while reducing its exposure to SME lending from 29% to 8% during the same period.

The bank’s strategic framework spans short-term (1 year), medium-term (2-3 years), and long-term (3-5 years) horizons, focusing on effective asset-liability management, digital-first revenue generation, customer-centric lending, and ecosystem development. TTB aims to achieve a top-quartile ROE of over 10%, maintain a high-yield loan mix of 30-35% in retail, and reduce its cost-to-income ratio to below 40%.

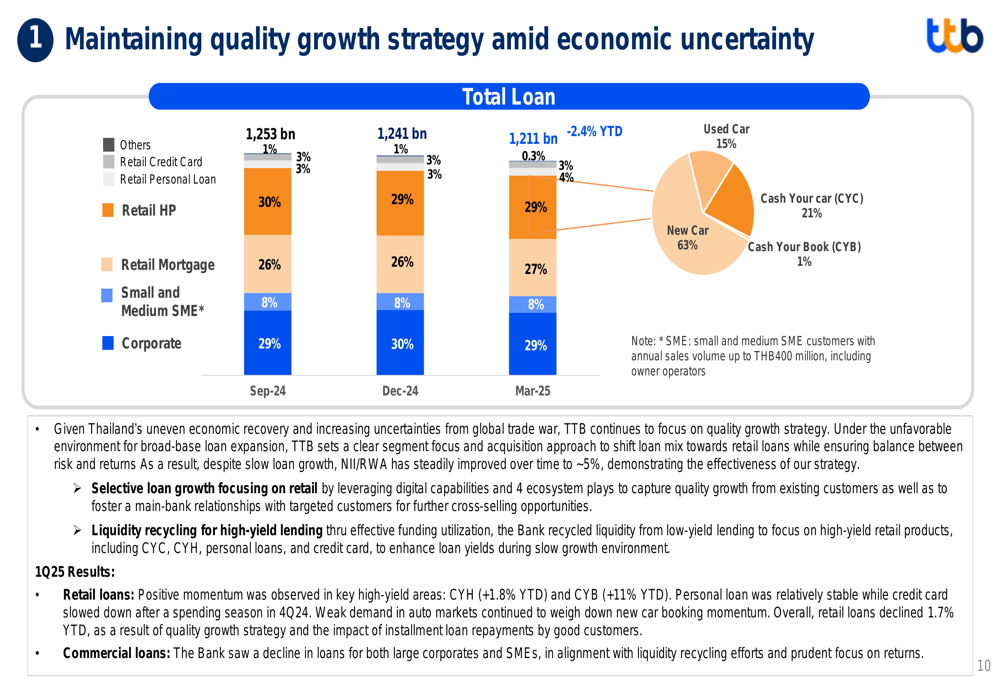

The bank’s loan portfolio strategy focuses on selective growth in retail segments while maintaining quality:

Digital Transformation Progress

A cornerstone of TTB’s strategy is its digital transformation, which has yielded impressive results. The bank has grown its digital user base from 1.8 million to 6.1 million, representing a 227% increase. TTB is leveraging digital platforms to drive customer engagement and cross-selling through personalized offerings and ecosystem development.

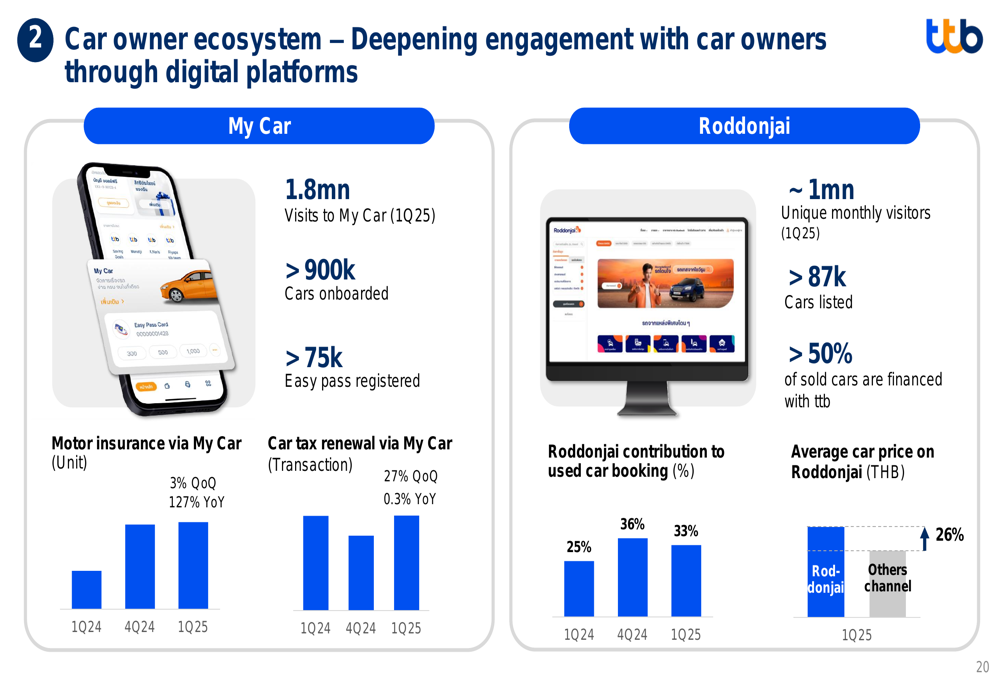

The bank has developed specialized ecosystems for key customer segments, including car owners, homeowners, salaried employees, and wealth clients. The car owner ecosystem, through the My Car app and Roddonjai platform, has generated 1.8 million visits in Q1 2025, with 900,000 cars onboarded and significant contributions to used car financing:

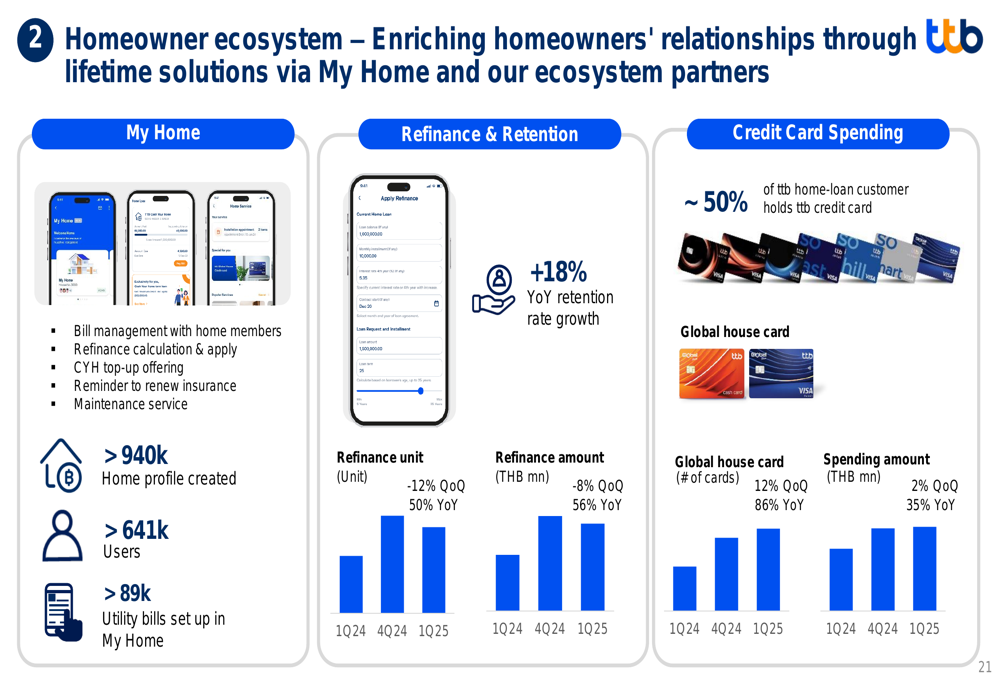

Similarly, the homeowner ecosystem has created over 940,000 home profiles and attracted more than 641,000 users:

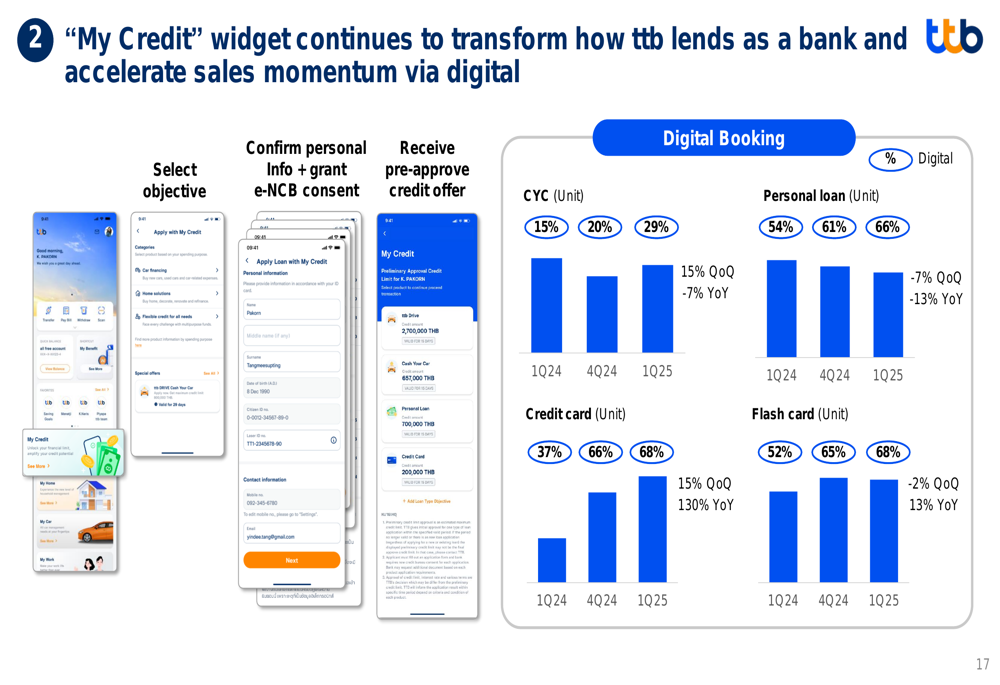

TTB’s digital-first approach has also transformed its lending process through the "My Credit" widget, which provides upfront credit assessment and personalized offers to customers. This has significantly increased digital booking rates across various loan products:

Risk Management Approach

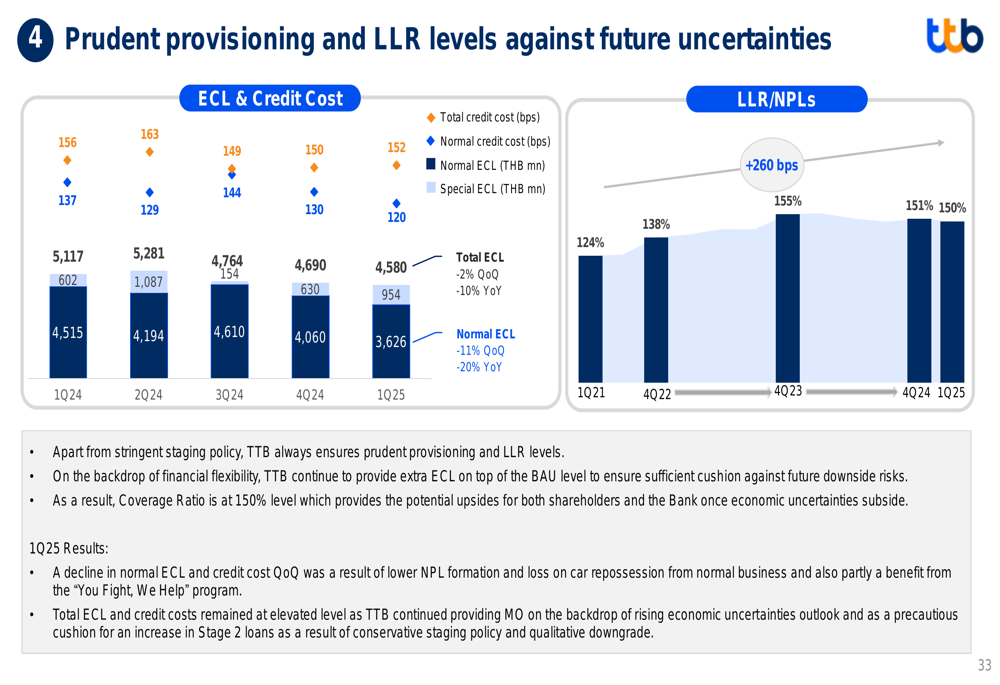

TTB maintains a conservative approach to risk management, with prudent provisioning and loan classification policies. The bank’s coverage ratio stands at 150%, providing a buffer against future uncertainties. The bank has implemented proactive collection strategies and loan restructuring initiatives to mitigate potential defaults.

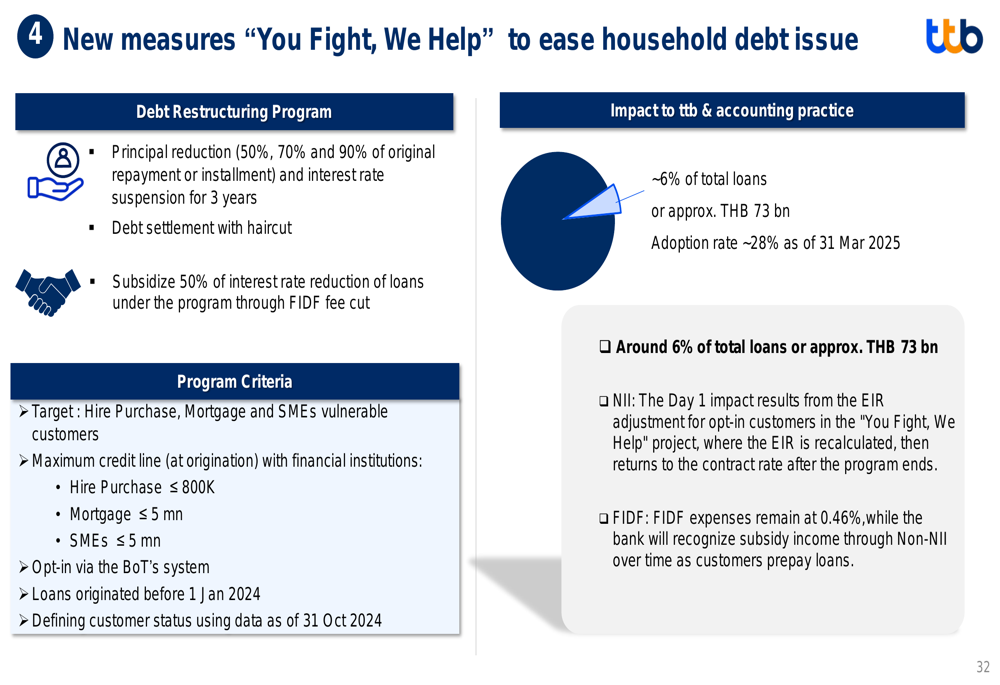

As part of its commitment to addressing household debt issues, TTB has introduced the "You Fight, We Help" program, which includes principal reduction, debt settlement with haircuts, and interest rate subsidies:

The bank’s conservative loan staging policy and proactive provisioning have resulted in a resilient loan loss reserve distribution:

Capital Management & Shareholder Returns

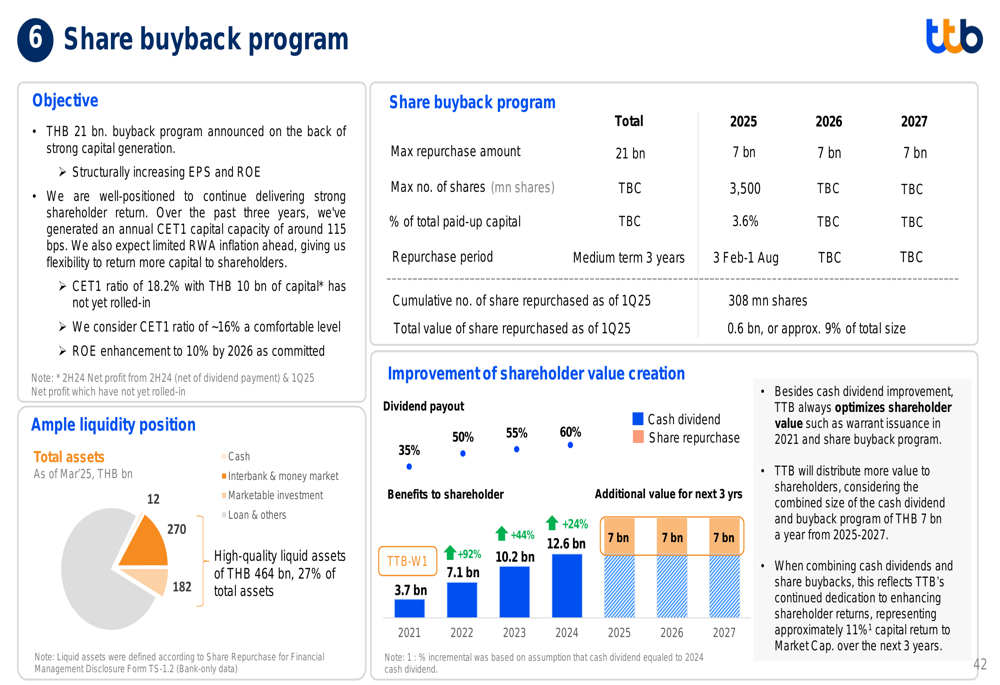

TTB is focused on optimizing shareholder value through a balance of immediate returns and long-term investments. The bank has implemented a THB 21 billion share repurchase program aimed at structurally increasing earnings per share and return on equity. As of Q1 2025, the bank has already repurchased a significant portion of shares while maintaining ample liquidity:

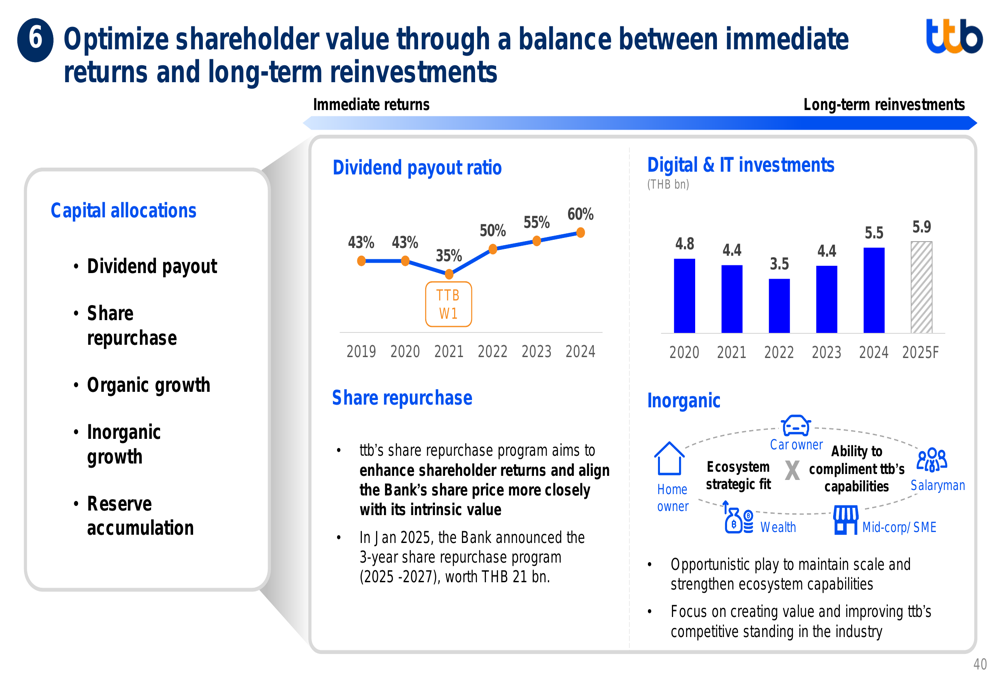

The bank’s approach to shareholder value creation balances immediate returns through dividends and share repurchases with long-term investments in digital capabilities and potential inorganic growth:

Forward-Looking Statements

Looking ahead, TTB remains committed to its transformation journey while navigating economic uncertainties. The bank expects to maintain its net interest margin within the target range of 3.1-3.25%, achieve loan growth of 0-2% for the full year, and keep its Stage 3 loan ratio below 2.9%.

TTB’s long-term aspirations include achieving a top-quartile ROE of over 10%, maintaining a high-yield loan mix, improving non-interest income to assets ratio to over 1.0%, and driving digital adoption to over 90% for both sales and service transactions.

The bank anticipates limited impact from the recent earthquake on its loan portfolio and continues to monitor potential effects from reciprocal tariffs. TTB’s conservative provisioning and strong capital position provide resilience against these uncertainties while supporting its commitment to shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.