Street Calls of the Week

Two Harbors Investment Corp (NYSE:TWO), an MSR-focused mortgage REIT, presented its first quarter 2025 earnings results on April 29, showing improved performance across key metrics compared to the previous quarter. The company reported a book value increase and a significant turnaround in comprehensive income amid a quarter characterized by modest declines in interest rates and market uncertainty.

Quarterly Performance Highlights

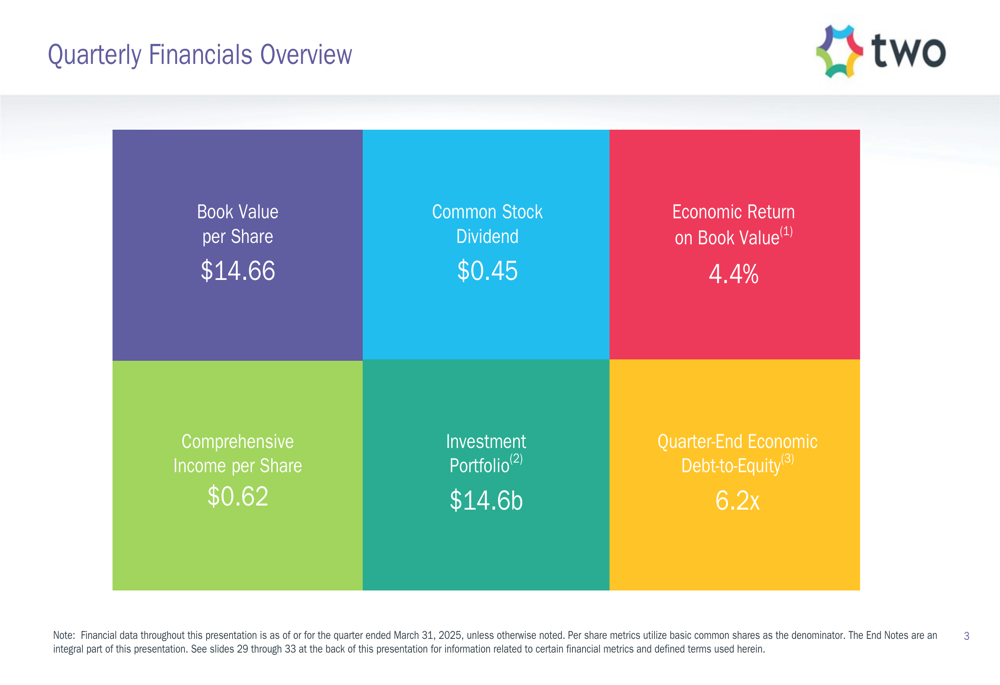

Two Harbors reported a book value per share of $14.66 as of March 31, 2025, representing an increase from $14.47 at the end of December 2024. The company declared a common stock dividend of $0.45 per share and achieved an economic return on book value of 4.4% for the quarter. Comprehensive income rebounded significantly to $64.9 million ($0.62 per share) from a loss of $1.6 million in the fourth quarter of 2024.

As shown in the following quarterly financials overview:

The company’s investment portfolio totaled $14.6 billion with a quarter-end economic debt-to-equity ratio of 6.2x. The improvement in comprehensive income was driven by increased net interest and servicing income, which rose to $133.3 million from $128.1 million in the previous quarter, as well as reduced mark-to-market losses, which decreased to $9.1 million from $47.5 million.

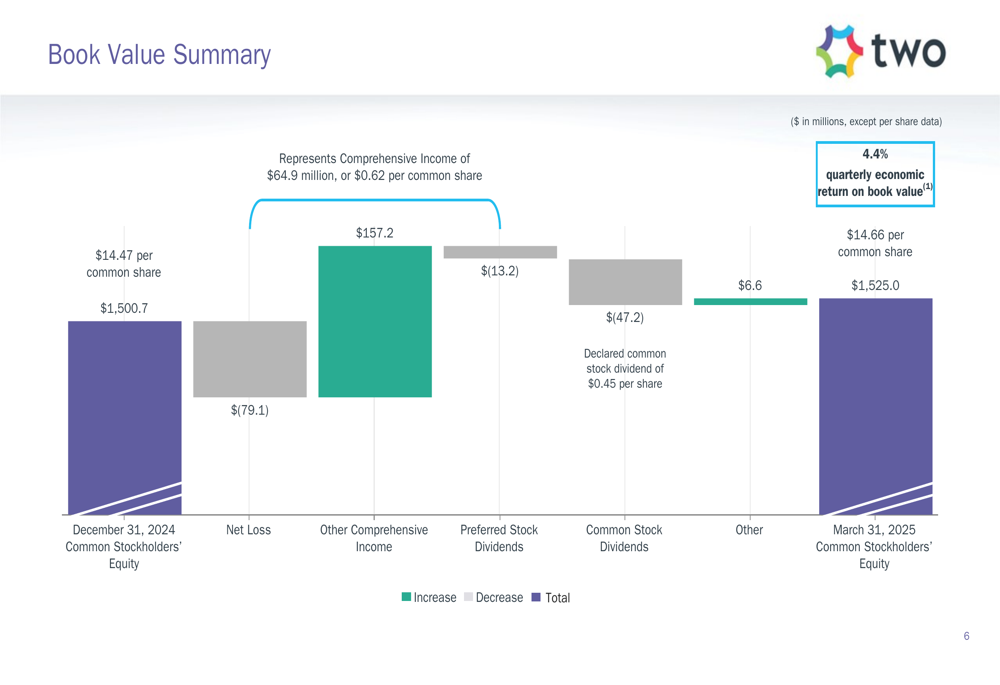

The following waterfall chart illustrates the components contributing to the change in book value:

Market Context and Portfolio Positioning

Two Harbors operated in a market environment where interest rates across the yield curve modestly declined during the quarter. According to the presentation, rates initially rose in January but were tempered by growing economic uncertainty. The yield curve remained positively sloped and at its steepest level since Q1 2022, while the Federal Reserve held rates unchanged and continued to forecast 50 basis points of cuts in 2025.

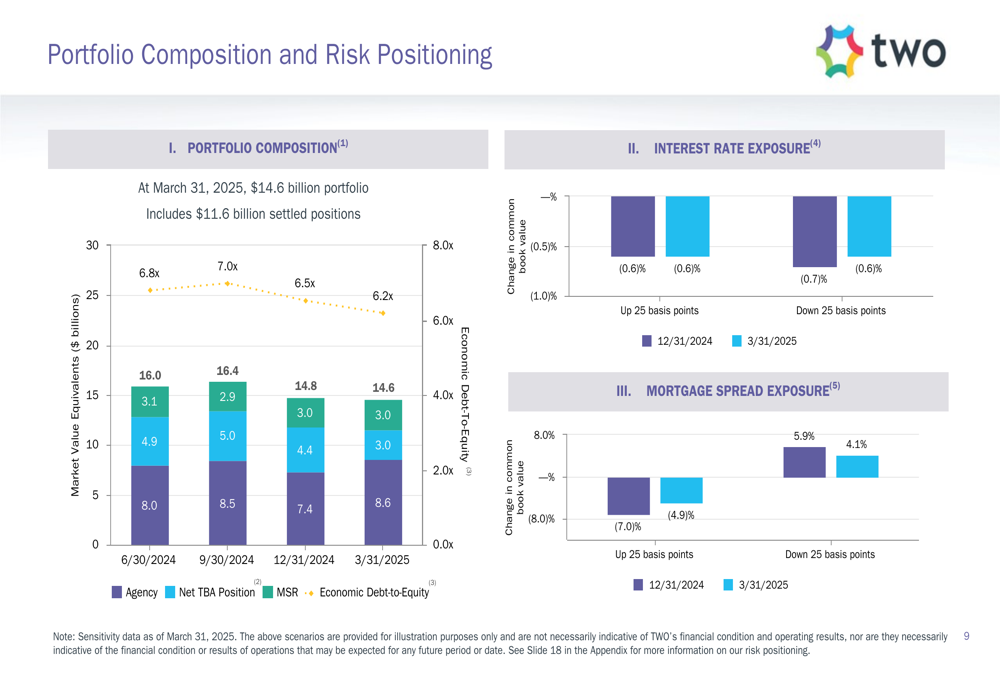

The company maintained its focus on a balanced portfolio approach, with $11.6 billion in settled positions as part of its $14.6 billion total portfolio. The portfolio composition and risk positioning are illustrated in the following chart:

In the Agency RMBS market, Two Harbors noted uneven performance across the coupon stack, with higher coupon TBA and specified pools outperforming longer duration lower coupons. The current coupon performance was aided by the steepening of the swap curve and record amounts of CMO issuance.

Strategic Initiatives and Operational Updates

A key strategic focus for Two Harbors continues to be the integration and optimization of RoundPoint, its mortgage servicing platform. The presentation highlighted several benefits of this acquisition, including cost efficiencies, additional income streams from subservicing and direct-to-consumer originations, and portfolio hedging capabilities.

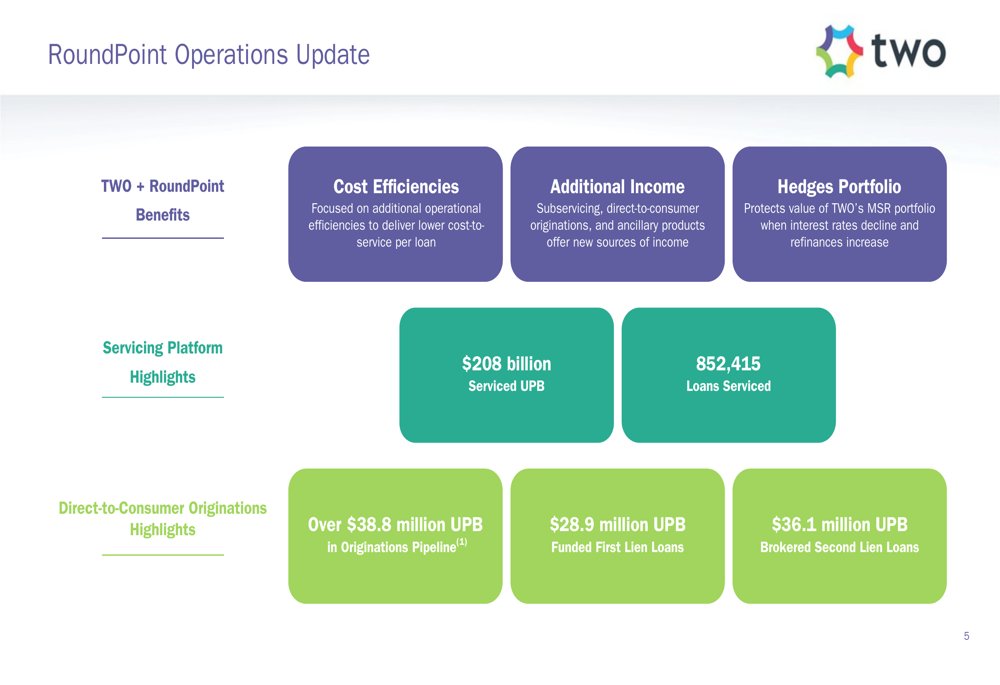

As shown in the RoundPoint operations update:

The servicing platform currently manages $208 billion in unpaid principal balance across 852,415 loans. The direct-to-consumer originations pipeline exceeded $38.8 million UPB, with $28.9 million UPB in funded first lien loans and $36.1 million UPB in brokered second lien loans. These operations provide Two Harbors with additional revenue streams and help protect the value of its MSR portfolio when interest rates decline and refinances increase.

MSR Portfolio Performance

Two Harbors’ MSR portfolio, a cornerstone of its investment strategy, showed stable performance with a fair value of $2.96 billion as of March 31, 2025, a slight decrease from $2.99 billion at the end of the previous quarter. The average 3-month CPR (Constant Prepayment Rate) decreased to 4.2% from 4.9%, reflecting the continued "lock-in" effect of higher mortgage rates.

The company emphasized that the MSR market remains well-supported due to high demand, ample opportunities, and relatively high rates keeping borrowers locked into their existing mortgages. This aligns with executive commentary from the previous quarter’s earnings call, where management highlighted the growing depth of the MSR financing market.

Forward-Looking Statements and Return Potential

Looking ahead, Two Harbors presented an optimistic outlook for returns, projecting static return estimates of 12-14% for servicing and 10-15% for securities. The company estimates a prospective quarterly static return per basic common share of $0.33 to $0.54.

The presentation highlighted the "TWO Advantage," emphasizing the company’s market presence in finding investments in hedged MSR, its focused investment strategy, favorable market environment with MSR "hundreds of basis points out of the money for refinancing," and strong balance sheet with diversified financing.

As illustrated in this strategic overview:

These projections align with the outlook provided in the previous quarter’s earnings call, where the company projected a static return on portfolio ranging from 9.8% to 12.1% and a potential static return on common equity between 10.8% and 14.4%.

Market Reaction

Following the earnings release, Two Harbors’ stock rose 1.08% in after-hours trading to $12.13, building on a 2.08% gain during the regular session. The stock has shown positive momentum, trading above both its previous close of $11.77 and moving closer to its 52-week high of $14.28.

Two Harbors continues to position itself as an MSR-focused REIT with a unique hedged strategy designed to generate attractive returns in various interest rate environments. With the successful integration of RoundPoint and improved financial performance in Q1 2025, the company appears well-positioned to capitalize on its strategic advantages in the mortgage market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.