Trump announces 100% chip tariff as Apple ups U.S. investment

Udemy Inc (NASDAQ:UDMY) reported its first profitable quarter since going public, according to the company’s Q2 2025 earnings presentation released on July 30, 2025. The online learning platform exceeded revenue expectations and significantly improved profitability metrics while continuing to expand its AI-powered offerings.

Executive Summary

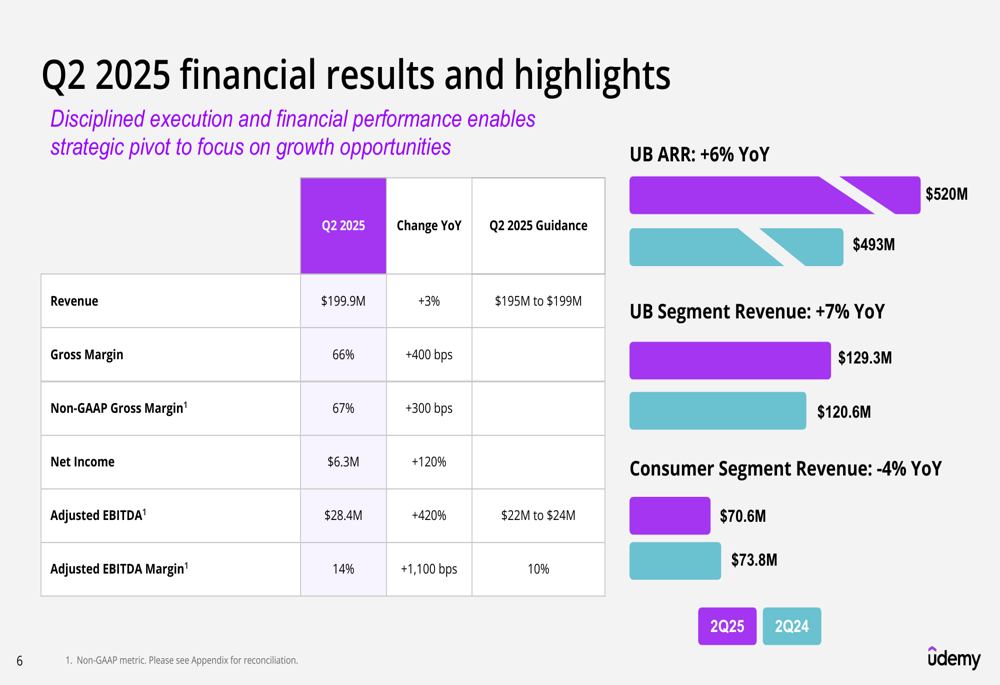

Udemy delivered revenue of $199.9 million in the second quarter, representing a 3% year-over-year increase and exceeding the company’s guidance range of $195-199 million. More notably, the company achieved GAAP net income of $6.3 million, marking its first profitable quarter since its IPO and a 120% improvement from the year-ago period.

"We are positioning Udemy to thrive in any environment, including the next wave of workplace transformation," CEO Hugo Sarazan had noted during the previous quarter’s earnings call, a strategy that appears to be bearing fruit as the company continues its focus on recurring revenue and AI-powered learning solutions.

The company’s stock edged up 1.05% in aftermarket trading to $7.20, building on recent momentum.

Quarterly Performance Highlights

Udemy’s Q2 2025 financial results showed significant improvement across key metrics, particularly in profitability. Adjusted EBITDA reached $28.4 million, a dramatic 420% increase year-over-year, exceeding the high end of guidance ($22-24 million). The adjusted EBITDA margin expanded to 14%, representing an 1,100 basis point improvement.

As shown in the following comprehensive financial results chart:

Gross margin improved to 66%, up 400 basis points from the previous year, while non-GAAP gross margin reached 67%, a 300 basis point increase. The company also reported strong free cash flow of $39.0 million for Q2, bringing the year-to-date total to $46.1 million.

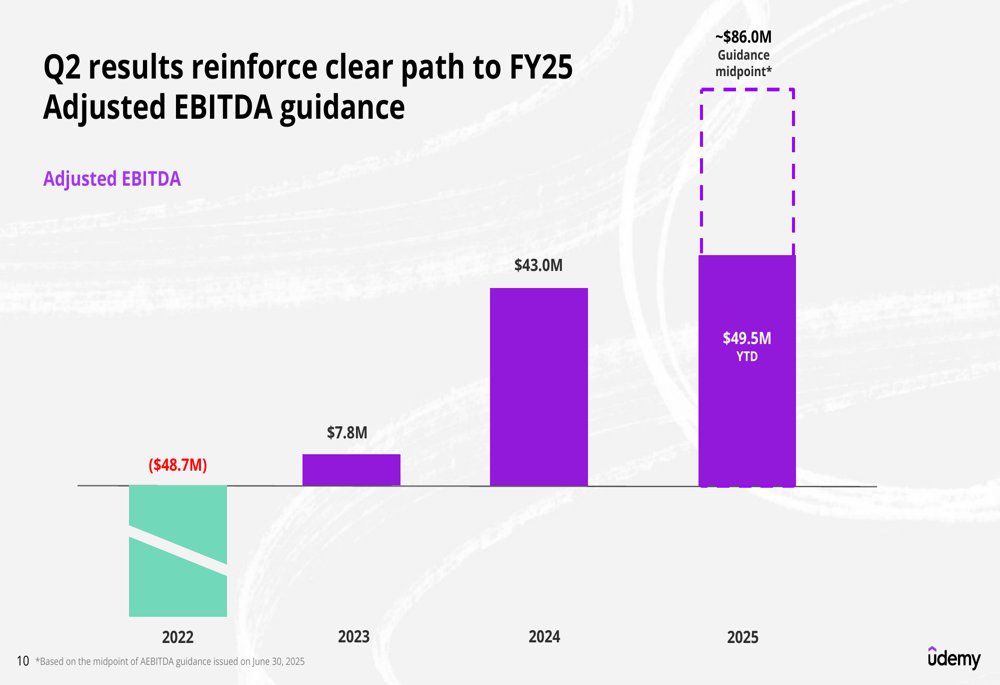

The company’s path to profitability has been consistent over recent years, as illustrated in this adjusted EBITDA progression:

Strategic Initiatives

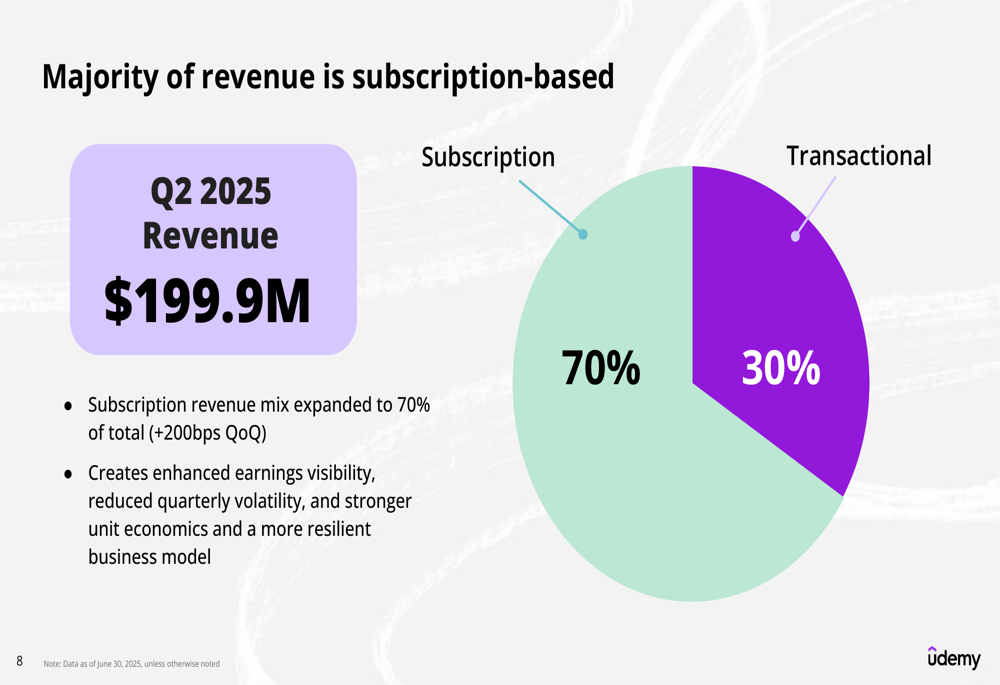

Udemy’s strategic pivot toward a subscription-based revenue model continues to gain traction. Subscription revenue now accounts for 70% of total revenue, an increase of 200 basis points quarter-over-quarter. This shift enhances earnings visibility, reduces quarterly volatility, and strengthens unit economics, creating a more resilient business model.

The following chart illustrates the current revenue breakdown:

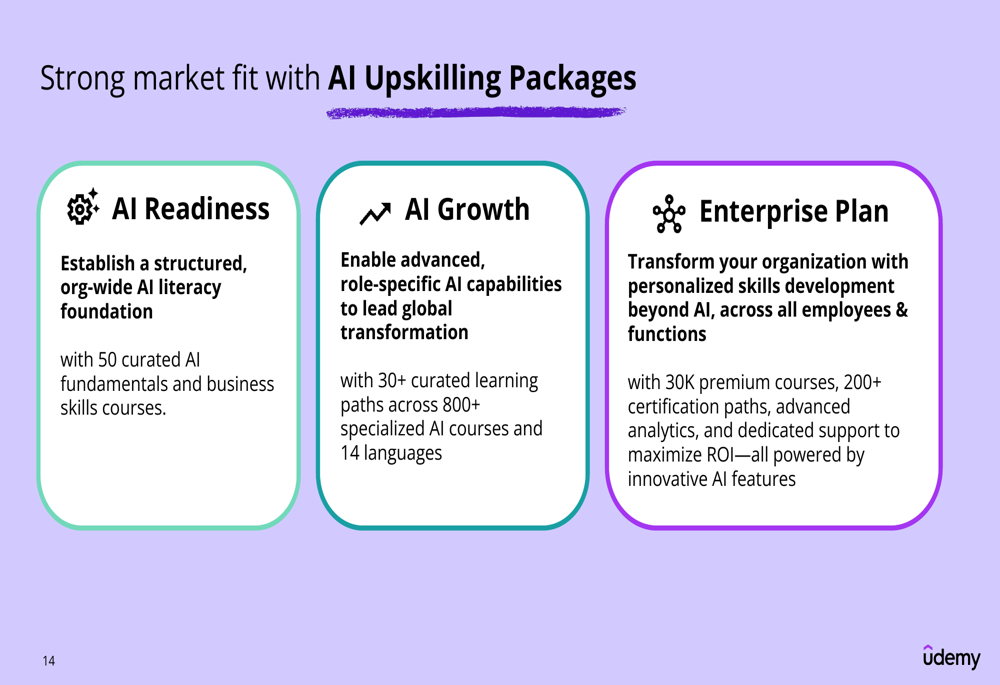

The company has also made significant progress on its AI initiatives, positioning itself as "THE AI-POWERED SKILLS ACCELERATION PLATFORM for the future workplace." Udemy now offers 4,500 AI-focused courses with over 11 million AI course enrollments and 350 million minutes of AI training consumed in the last twelve months.

During Q2, Udemy launched two new AI upskilling packages for enterprise customers:

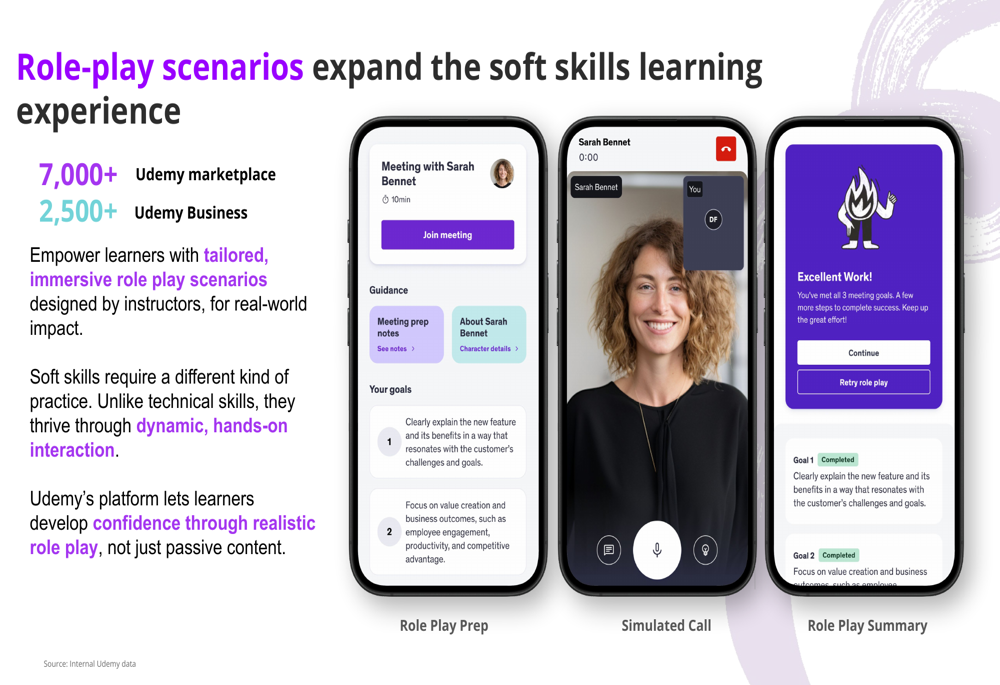

Another notable AI innovation is the Role-Play feature, which offers over 7,000 scenarios in the Udemy marketplace and 2,500+ in Udemy Business. These AI-powered simulations help learners develop soft skills through immersive, instructor-designed conversation scenarios.

Business Segments Performance

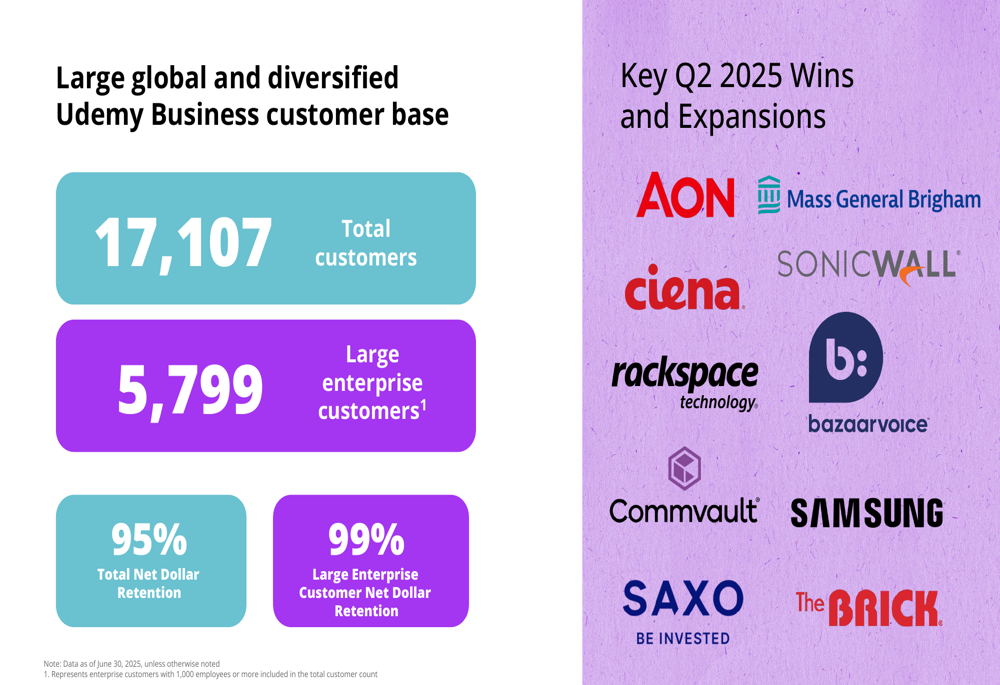

Udemy’s business is divided into two main segments: Enterprise (Udemy Business) and Consumer. The Enterprise segment continues to drive growth with revenue of $129.3 million, up 7% year-over-year. Udemy Business Annual Recurring Revenue (UB ARR) reached $520 million, a 6% increase from the previous year.

The company now serves 17,107 total customers, including 5,799 large enterprise customers. While the total Net Dollar Retention rate stands at 95%, large enterprise customers show stronger retention at 99%.

In contrast, the Consumer segment revenue declined by 4% year-over-year to $70.6 million. However, the company highlighted progress in its consumer subscription strategy, surpassing 200,000 paid subscribers as subscription revenue increased to 15% of the segment’s total mix, up 2 percentage points in just one quarter.

Forward-Looking Statements

For Q3 2025, Udemy projects revenue between $190-195 million and adjusted EBITDA of $18-20 million, representing a margin of approximately 10% at the midpoint.

For the full year 2025, the company expects:

- Revenue of $784-794 million

- Adjusted EBITDA of $84-89 million (11% margin at midpoint)

These projections suggest a slight sequential decline in Q3 before a stronger Q4, following seasonal patterns typical in the education technology sector.

Competitive Industry Position

Udemy continues to strengthen its position as a leader in the online learning market, particularly in AI skills development. The company’s investment highlights underscore its scale and growth trajectory, with a five-year revenue CAGR of 23% and a strong global presence with over 60% of revenue coming from outside North America.

The company’s vibrant marketplace now includes 85,000+ instructors, 250,000+ courses, and 1.1 billion enrollments, serving 81 million learners across 75 local languages. This extensive content library and global reach provide Udemy with significant competitive advantages in the rapidly evolving online education space.

With $393 million in cash and no outstanding debt, Udemy maintains a strong financial position to continue investing in growth initiatives while delivering improving profitability metrics. The company’s strategic focus on AI-powered learning solutions and subscription-based revenue appears well-aligned with current market trends, positioning it favorably against competitors in the educational technology sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.