Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

UL Solutions Inc. (NYSE:ULS) released its Q3 2025 earnings presentation on November 4, 2025, showcasing record quarterly revenue and profitability. The company's shares responded positively, rising 3.73% in pre-market trading to $81.54, reflecting investor confidence in the strong financial performance.

The safety certification and advisory services provider reported significant growth across all business segments, with consolidated revenue increasing by 7.1% year-over-year to $783 million. This performance exceeded analyst expectations, with adjusted earnings per share of $0.56 surpassing the forecast of $0.40.

Quarterly Performance Highlights

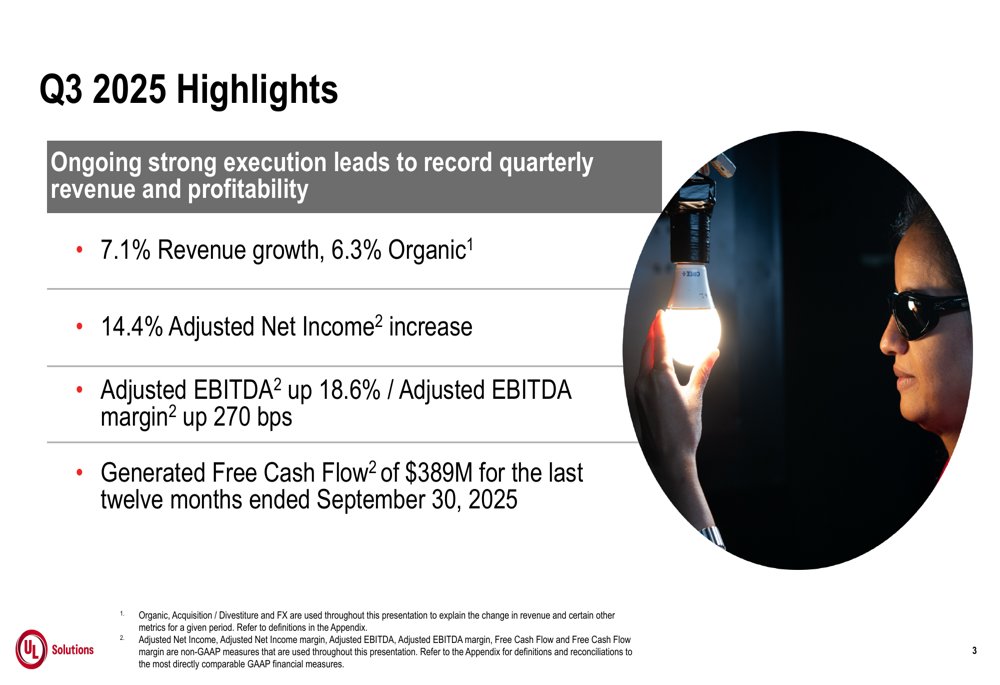

UL Solutions delivered robust financial results for the third quarter, with organic revenue growth of 6.3% and total revenue growth of 7.1% compared to Q3 2024. The company's adjusted EBITDA increased by 18.6% to $217 million, with margin expansion of 270 basis points to 27.7%.

As shown in the following chart highlighting key quarterly metrics:

Adjusted net income rose by 14.4% to $119 million, with adjusted net income margin increasing to 15.2% from 14.2% in the prior year period. The company's revenue growth was driven by strong performance across all segments, with particular strength in the Industrial segment.

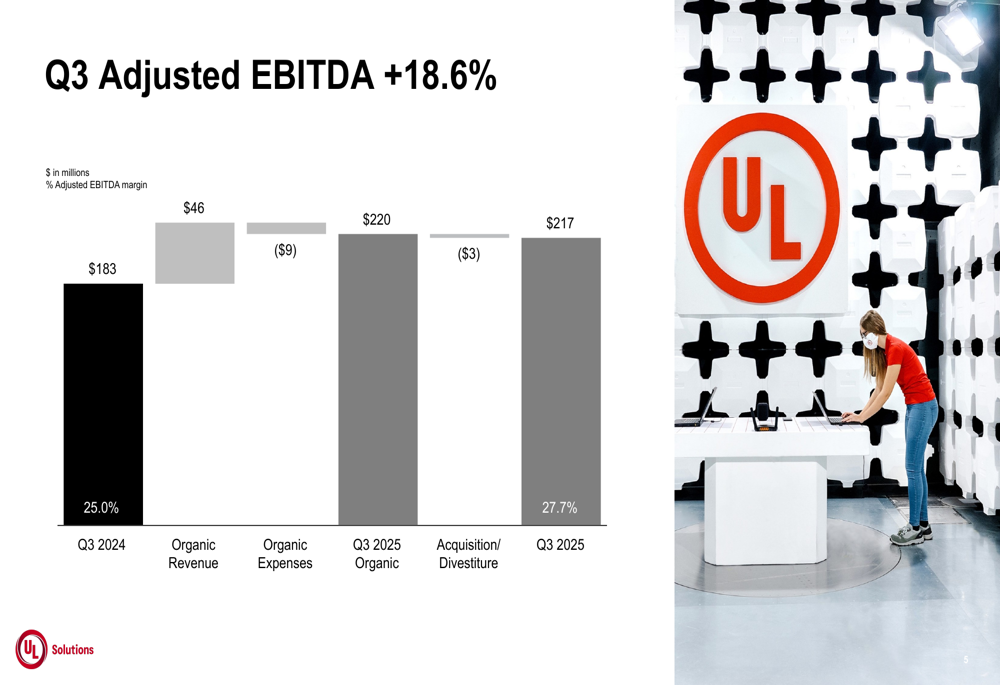

The following waterfall chart illustrates the components of revenue growth:

Profitability improvements were equally impressive, with adjusted EBITDA growth of 18.6% driven by operating leverage from revenue growth, partially offset by increased employee compensation expenses:

Segment-by-Segment Analysis

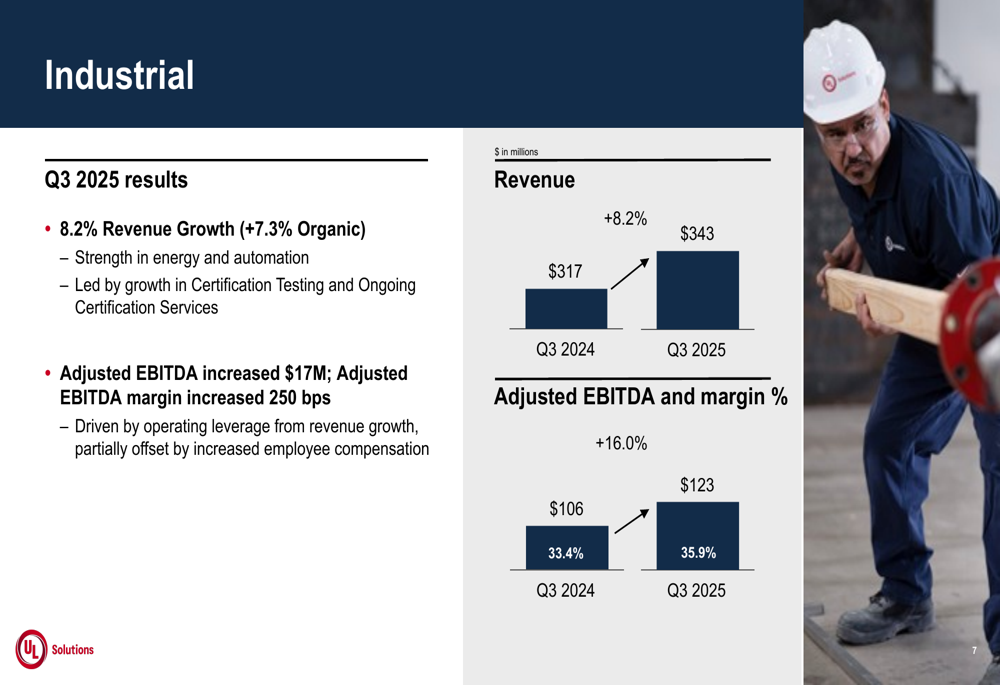

The Industrial segment led the company's growth, with revenue increasing by 8.2% (7.3% organic) to $343 million. This performance was driven by strength in energy and automation sectors, particularly in Certification Testing and Ongoing Certification Services. The segment's adjusted EBITDA increased by 16.0% to $123 million, with margin expansion of 250 basis points to 35.9%.

The segment's performance is illustrated in the following chart:

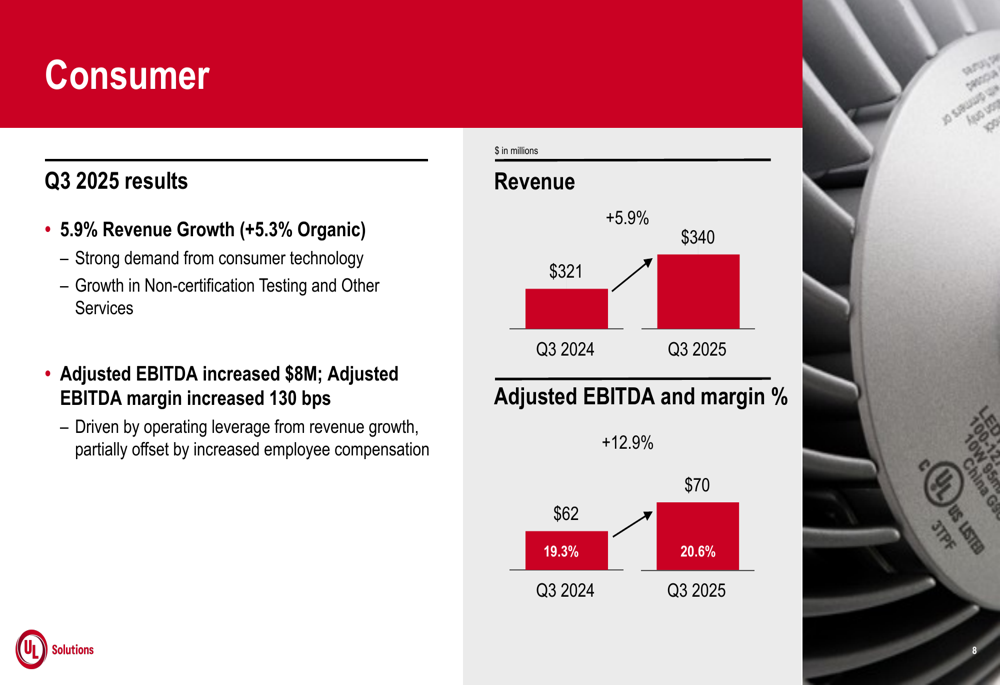

The Consumer segment also delivered solid results, with revenue growth of 5.9% (5.3% organic) to $340 million. This growth was driven by strong demand from consumer technology and growth in Non-certification Testing and Other Services. Adjusted EBITDA for the segment increased by 12.9% to $70 million, with margin expansion of 130 basis points to 20.6%.

The Consumer segment's performance is detailed in the following chart:

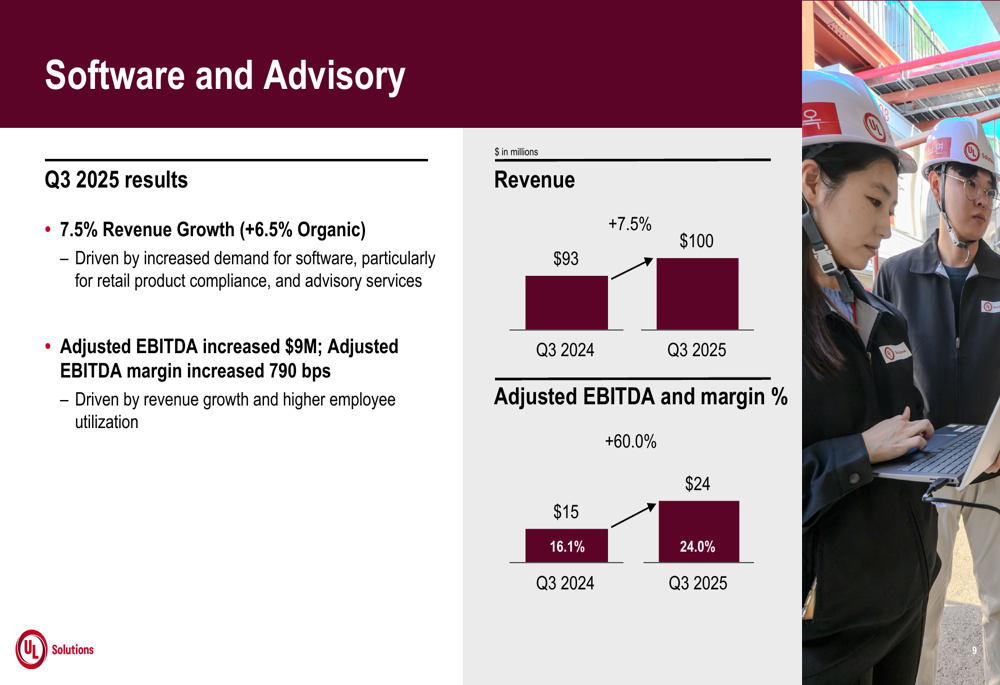

The Software and Advisory segment showed the most significant margin improvement, with revenue increasing by 7.5% (6.5% organic) to $100 million. The segment's adjusted EBITDA surged by 60.0% to $24 million, with margin expansion of 790 basis points to 24.0%, driven by revenue growth and higher employee utilization.

The following chart illustrates the Software and Advisory segment's performance:

Cash Flow and Financial Position

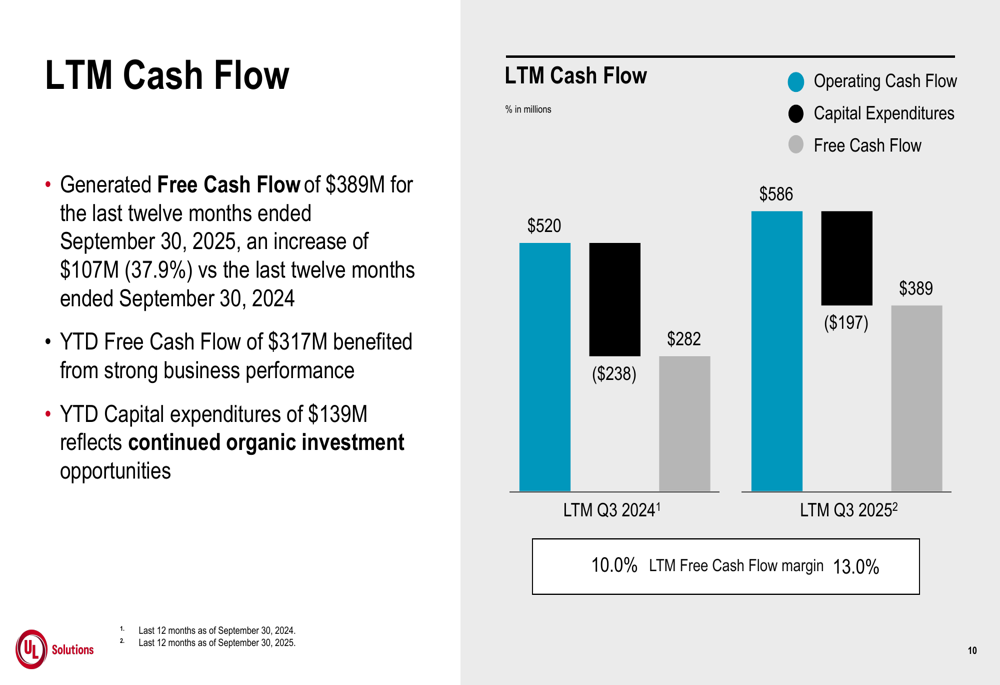

UL Solutions generated robust free cash flow of $389 million for the last twelve months ended September 30, 2025, representing a significant increase of 37.9% compared to the same period in 2024. The free cash flow margin improved from 10.0% to 13.0%, reflecting the company's strong operational execution and disciplined capital management.

Year-to-date free cash flow of $317 million benefited from strong business performance, while capital expenditures of $139 million reflected continued organic investment opportunities. The following chart illustrates the company's cash flow performance:

Forward-Looking Statements

Based on the strong performance in the first nine months of 2025, UL Solutions has strengthened its outlook for the full year. The company now expects organic revenue growth between 5.5% and 6.0% at constant currency, with adjusted EBITDA margin organic improvement to approximately 25%.

Capital expenditures are projected to be between 6.5% and 7.0% of revenue, while the effective tax rate is expected to be between 25% and 26%. The company also indicated its intention to continue pursuing acquisitions and portfolio refinements to enhance its market position.

As shown in the following slide detailing the company's outlook:

During the earnings call, CEO Jenny Scalen emphasized the critical nature of UL Solutions' services: "Our services have remained in strong demand. This validates both the mission-critical nature of our services and our customers' commitment to bringing new products to market." CFO Ryan Robinson highlighted the company's adaptability: "We are continuing to tailor our business to today's rapidly changing landscape."

With a strong balance sheet, expanding margins across all segments, and continued organic growth, UL Solutions appears well-positioned to maintain its momentum through the remainder of 2025 and beyond. The company's focus on high-growth areas such as AI safety certifications and data center services, as mentioned in the earnings call, provides additional avenues for future expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.