Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

United Community Banks , Inc. (NASDAQ:NYSE:UCB) presented its first quarter 2025 results on April 22, 2025, highlighting solid performance across key metrics. The bank, which is celebrating its 75th anniversary, reported improved margins, deposit growth, and strong capital ratios, positioning it well in the competitive Southeast banking landscape.

With total assets of $27.9 billion and a network of 200 banking offices across the Southeast, United Community Banks continues to build on its reputation for customer service, having been ranked #1 in Customer Satisfaction with Consumer Banking in the Southeast in 2025 by J.D. Power.

The bank’s stock closed at $24.58 on April 21, 2025, with a 52-week range of $22.93 to $35.38, according to recent market data.

Quarterly Performance Highlights

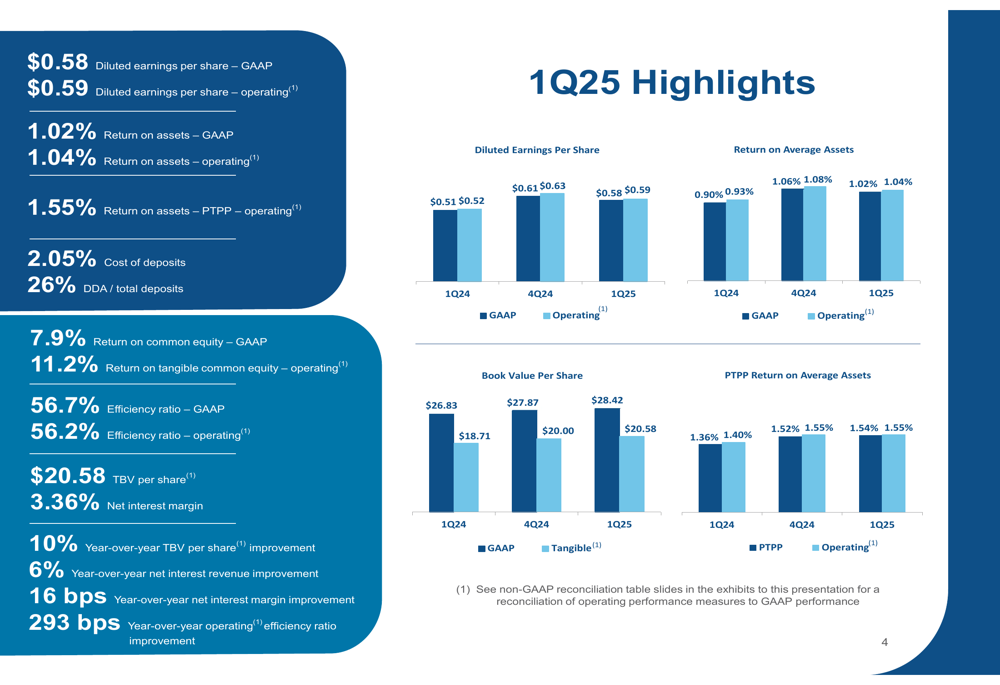

United Community Banks reported operating earnings per share of $0.59 for Q1 2025, a slight improvement from the $0.58 reported in Q2 2024. The bank’s operating return on assets reached 1.04%, crossing above the 1% threshold, while return on common equity on an operating basis was 11.2%.

As shown in the following chart of key financial metrics, the bank demonstrated year-over-year improvements across several important indicators:

Net interest margin expanded to 3.36%, representing a 16 basis point improvement year-over-year. This margin expansion contributed to a 6% increase in net interest revenue compared to the same period last year. The bank’s efficiency ratio improved significantly, with the operating efficiency ratio decreasing by 293 basis points year-over-year to 56.2%.

Tangible book value per share grew to $20.58, representing a 10% improvement year-over-year, continuing the positive trend seen in previous quarters.

Deposit and Loan Growth Analysis

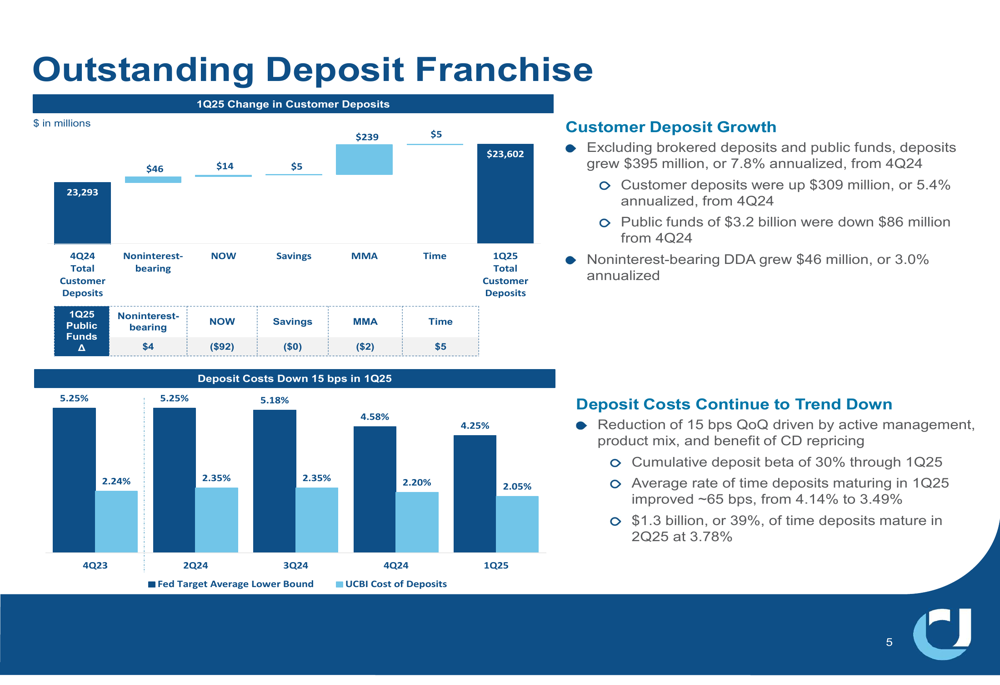

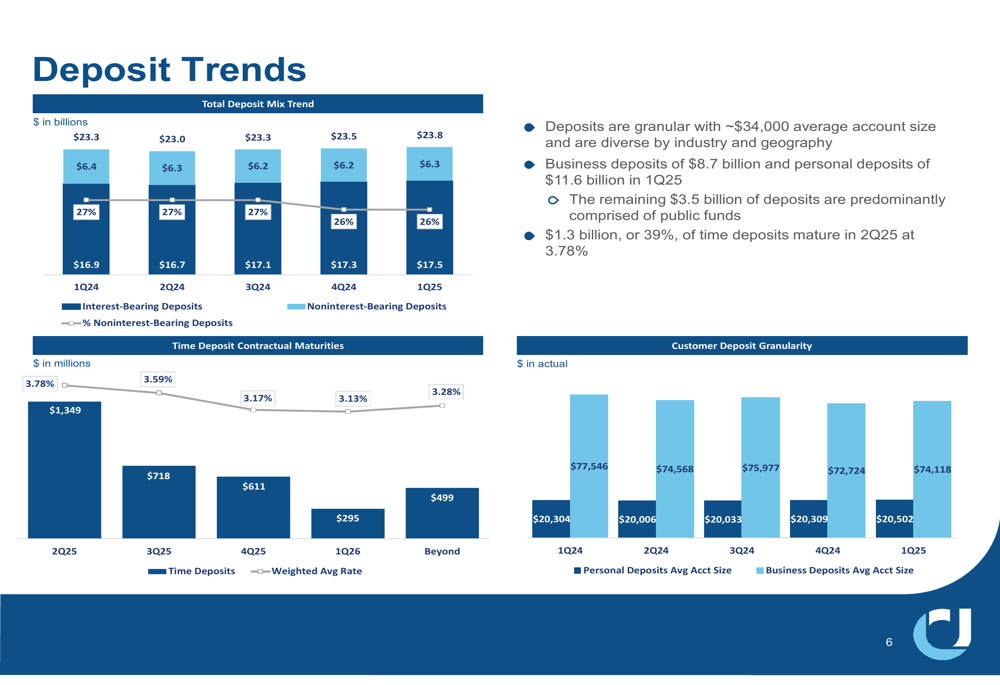

United Community Banks demonstrated strong deposit growth in Q1 2025. Excluding brokered deposits and public funds, customer deposits grew by $395 million, or 7.8% annualized, from the previous quarter. Importantly, the bank saw a reduction in deposit costs of 15 basis points quarter-over-quarter, with a cumulative deposit beta of 30% through Q1 2025.

The following chart illustrates the bank’s deposit growth and cost trends:

The bank’s deposit franchise remains granular and diverse, with an average account size of approximately $34,000. Business deposits totaled $8.7 billion, while personal deposits reached $11.6 billion in Q1 2025. The remaining $3.5 billion primarily comprised public funds.

The deposit mix remained relatively stable, with noninterest-bearing deposits representing 26% of total deposits:

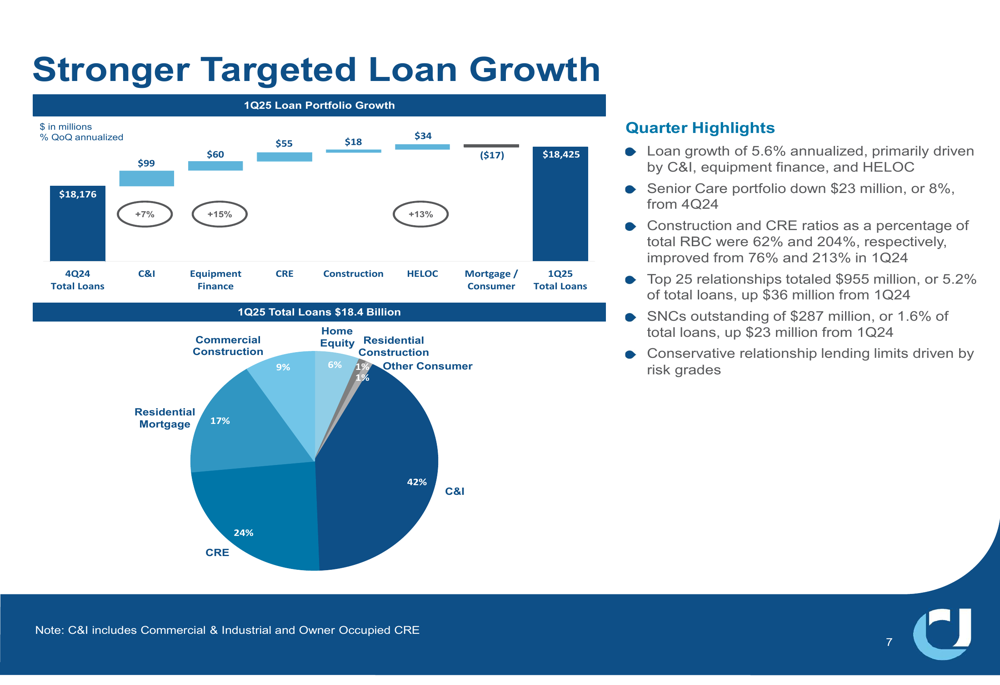

On the lending side, United Community Banks reported loan growth of 5.6% annualized, primarily driven by commercial and industrial (C&I) loans, equipment finance, and home equity lines of credit (HELOC). The bank’s loan portfolio is well-diversified, with C&I loans representing 42% of the total $18.4 billion portfolio.

The following chart details the composition and growth of the loan portfolio:

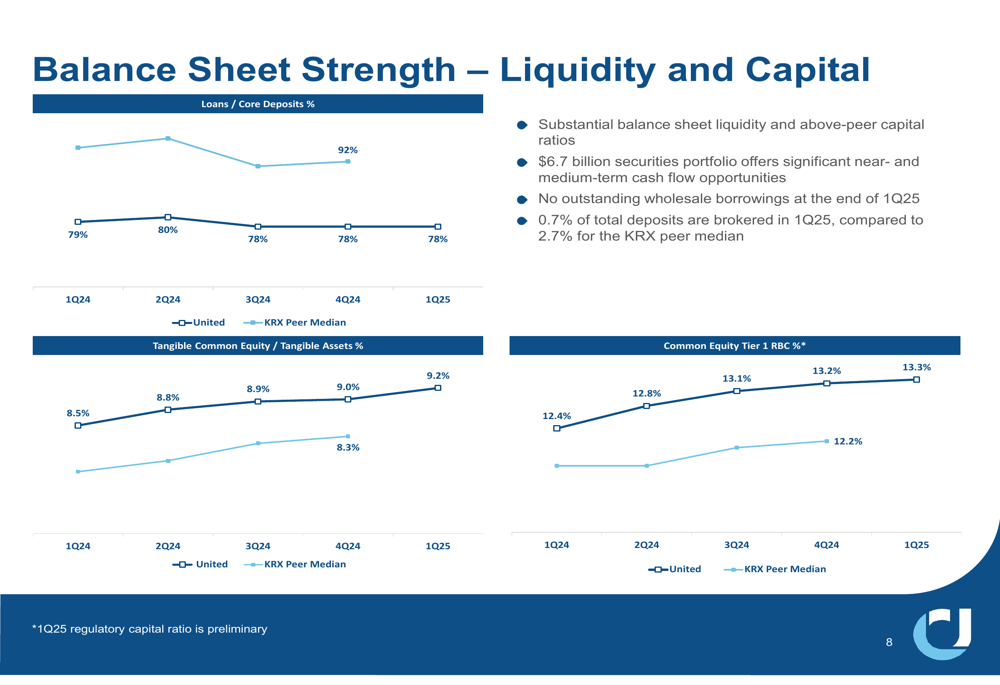

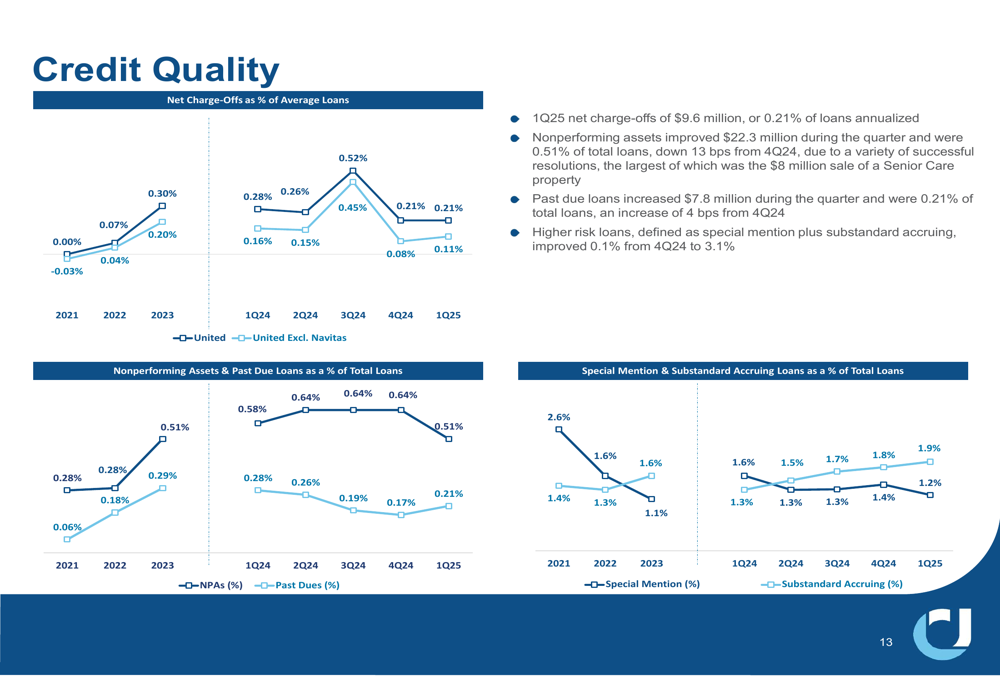

Capital Position and Credit Quality

United Community Banks maintained strong capital ratios in Q1 2025, with a Common Equity Tier 1 (CET1) ratio of 13.3%, significantly above the KRX peer median of 12.2%. The bank’s tangible common equity (TCE) ratio increased by 21 basis points from Q4 2024 to 9.18%.

The bank’s balance sheet liquidity remains substantial, with no outstanding wholesale borrowings at the end of Q1 2025. Only 0.7% of total deposits were brokered, compared to 2.7% for the KRX peer median. The loans-to-core deposits ratio stood at 78%, well below the peer median of 92%.

As illustrated in the following chart, the bank’s capital position compares favorably to industry peers:

Credit quality metrics showed improvement in Q1 2025. Net charge-offs were $9.6 million, or 0.21% of loans annualized, an improvement from the 26 basis points reported in Q2 2024. Nonperforming assets improved by $22.3 million during the quarter and represented 0.51% of total loans, down 13 basis points from the previous quarter.

The following chart shows the trends in credit quality metrics:

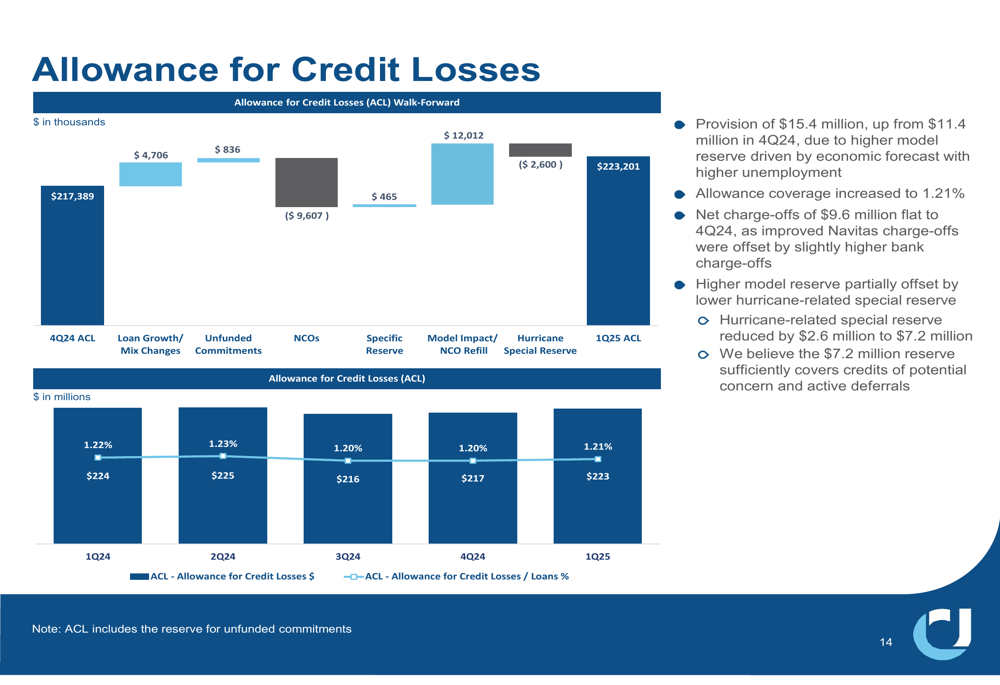

The allowance for credit losses increased slightly to 1.21% of loans. The provision for credit losses was $15.4 million, up from $11.4 million in Q4 2024, primarily due to a higher model reserve driven by an economic forecast with higher unemployment.

Strategic Positioning and Growth Outlook

United Community Banks continues to focus on high-growth metropolitan statistical areas (MSAs) across the Southeast. The bank’s deposit base is concentrated in markets with strong projected population and household income growth, with Atlanta representing the largest share at 22.3% of total deposits.

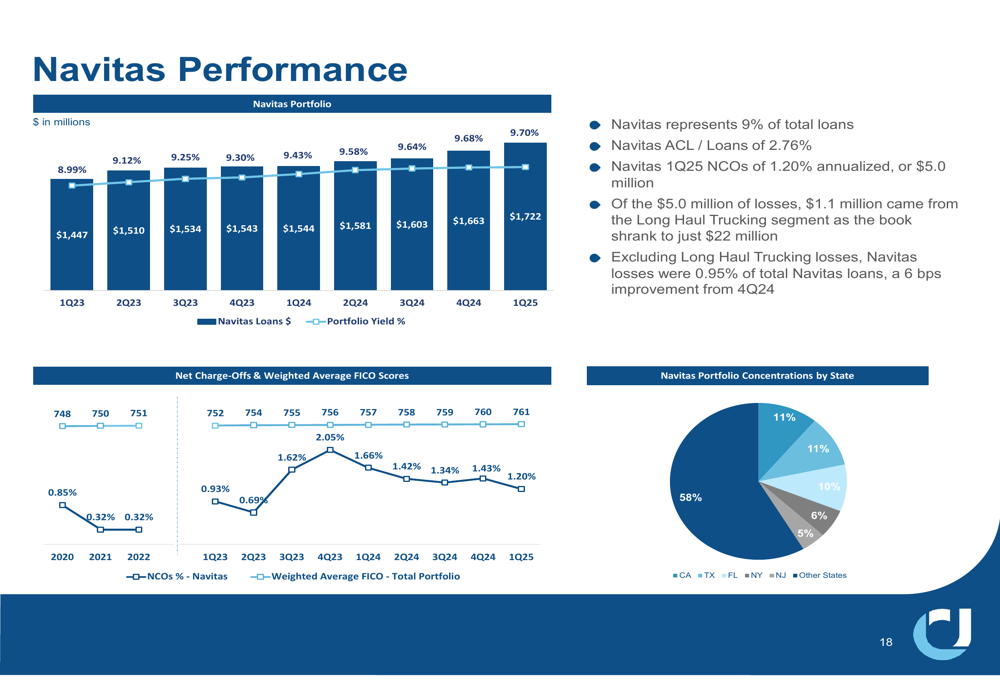

The bank’s subsidiary, Navitas, which specializes in equipment finance, represents 9% of total loans and maintains a robust allowance for credit losses at 2.76%. Navitas reported net charge-offs of 1.20% annualized, or $5.0 million, in Q1 2025.

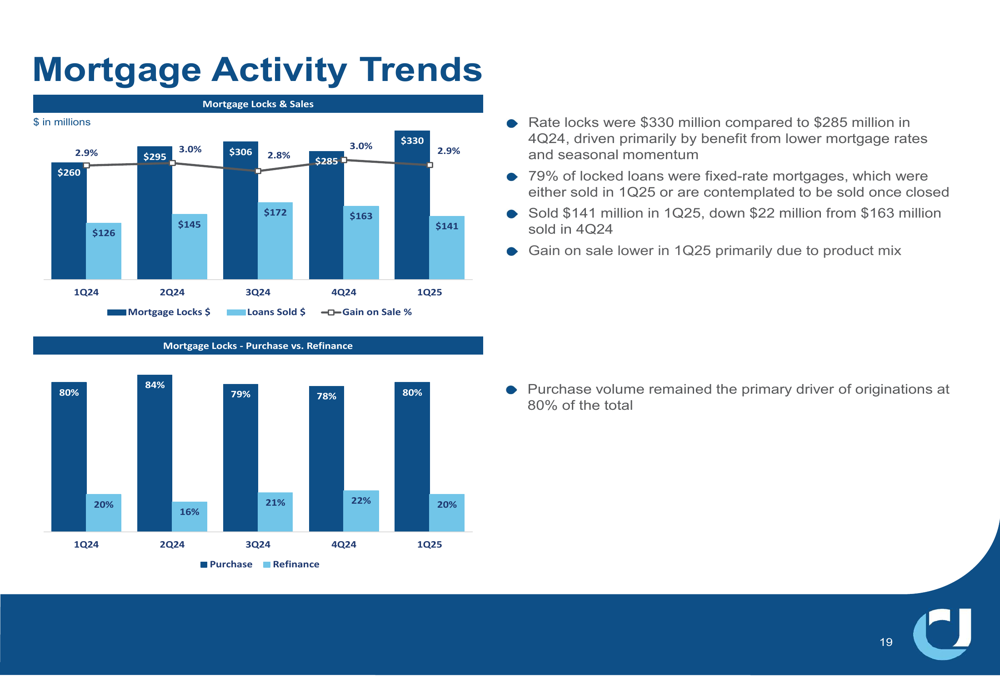

Mortgage activity showed positive momentum, with rate locks of $330 million compared to $285 million in Q4 2024, driven primarily by lower mortgage rates and seasonal factors. The bank sold $141 million in mortgages during Q1 2025.

Based on the previous quarter’s earnings call, United Community Banks appears to be executing on its strategy of focusing on expense management while maintaining growth in key areas. The slight improvement in operating earnings per share and the reduction in net charge-offs from 26 to 21 basis points align with management’s previous guidance.

The bank’s continued focus on the Southeast market, combined with its strong capital position and improving efficiency ratio, positions it well for sustainable growth as it celebrates its 75th anniversary of serving communities across the region.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.