U.S. may expand Nvidia and AMD’s 15% China chips deal to other companies

Introduction & Market Context

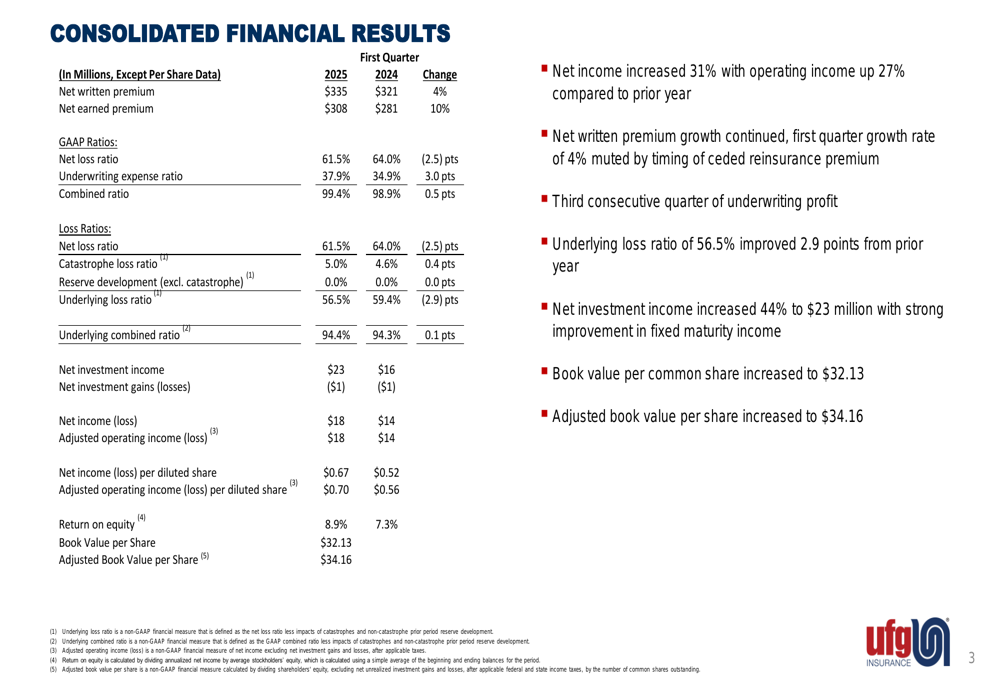

United Fire Group Inc (NASDAQ:UFCS) presented its first quarter 2025 financial results on May 7, 2025, showing continued premium growth and improved investment returns. The property and casualty insurer reported net income of $18 million, up 29% from the same period last year, as the company maintained its underwriting discipline while benefiting from higher interest rates.

UFCS shares closed at $28.60 on May 6, 2025, up 1.02% for the day, and have traded between $18.04 and $31.70 over the past 52 weeks. The company has been working to improve its underwriting performance while capitalizing on favorable rate conditions in commercial lines.

Quarterly Performance Highlights

United Fire Group reported net written premiums of $335 million for Q1 2025, representing a 4.4% increase from $321 million in Q1 2024. Net earned premiums grew at a faster pace, rising 9.6% to $308 million from $281 million in the prior-year period.

The company achieved a combined ratio of 99.4% in Q1 2025, slightly higher than the 98.9% reported in Q1 2024, but still representing an underwriting profit. This marks consecutive quarters of underwriting profitability, continuing the positive trend observed in the company’s Q3 2024 results.

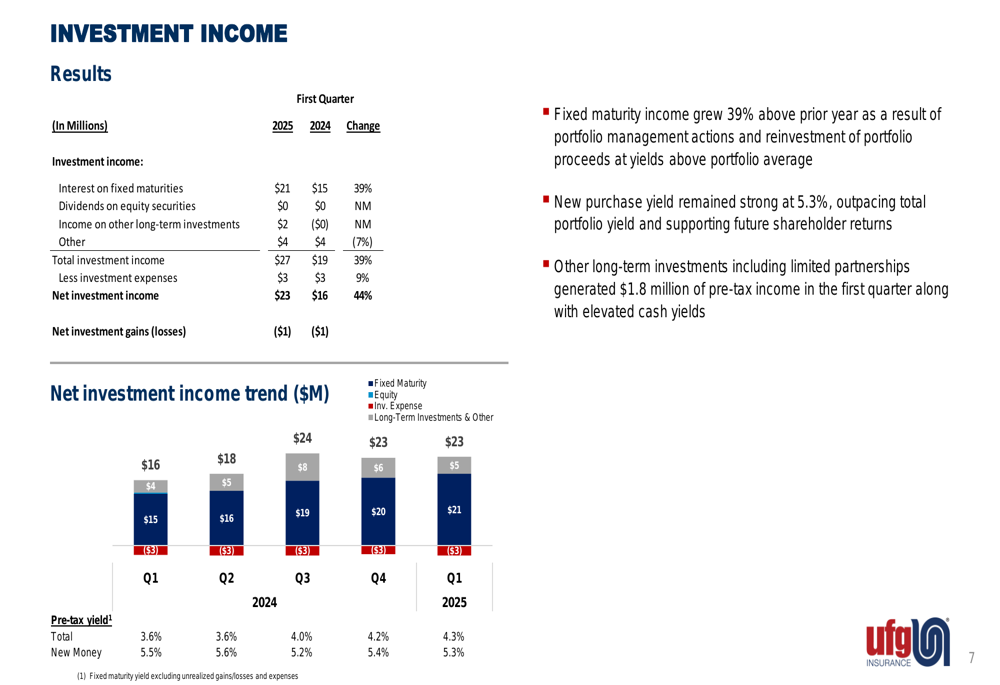

As shown in the following consolidated financial results:

Net income increased to $18 million ($0.67 per diluted share) in Q1 2025, compared to $14 million ($0.52 per diluted share) in Q1 2024. The company’s return on equity improved to 8.9%, up from 7.3% in the same period last year.

Detailed Financial Analysis

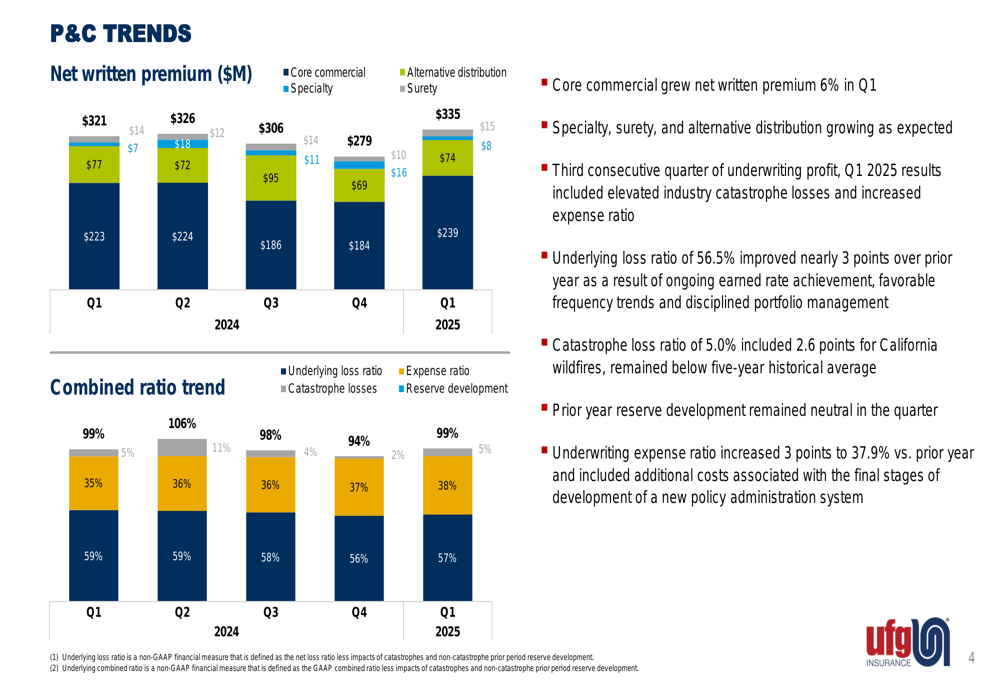

The company’s premium growth was driven primarily by its core commercial segment, which continues to benefit from favorable pricing conditions. The P&C trends chart illustrates the composition of net written premiums across business segments:

Core commercial lines generated $239 million in net written premiums, while alternative distribution contributed $74 million. Specialty and Surety lines added $16 million and $8 million, respectively. The company has maintained this growth momentum since Q3 2024, when it reported a 23% increase in net written premiums.

The underlying loss ratio improved to 56.5% in Q1 2025 from 59.4% in Q1 2024, reflecting enhanced underwriting discipline. However, this improvement was partially offset by an increase in the expense ratio to 37.9% from 34.9% in the prior-year period. The elevated expense ratio remains a challenge for the company, consistent with concerns noted in previous quarters.

Catastrophe losses accounted for 5% of the combined ratio in Q1 2025, while favorable reserve development contributed a 2% benefit.

Business Unit Performance

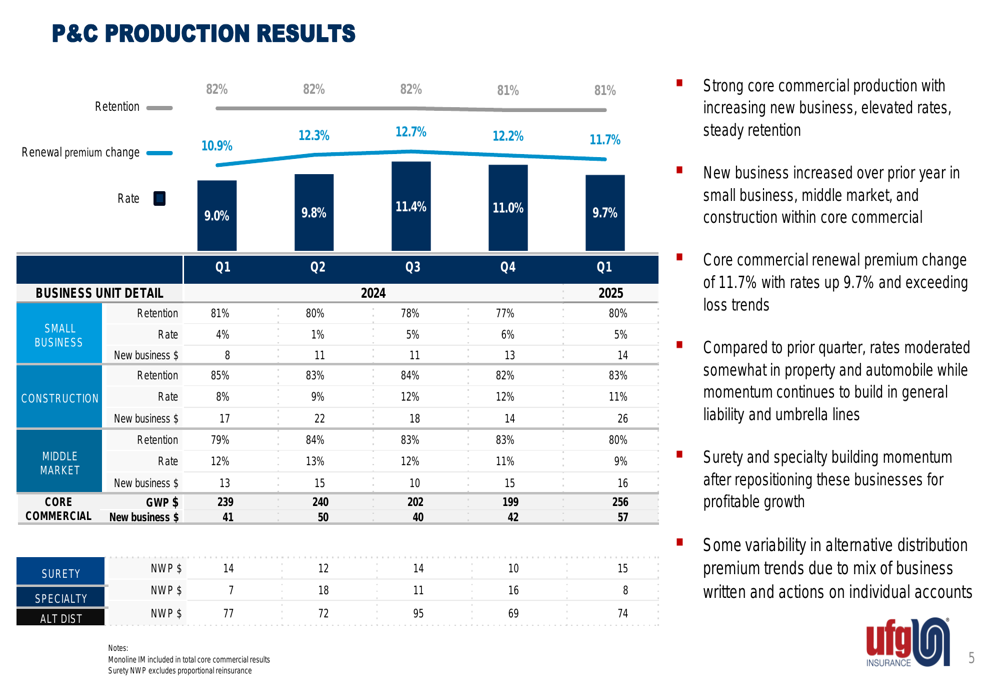

United Fire Group’s production results by business unit show strong renewal premium changes across segments, with particularly robust performance in its core commercial lines:

The company reported gross written premiums of $256 million for core commercial lines, with new business of $57 million in Q1 2025. Core commercial renewal premium change was 11.7%, with rates up 9.7%.

The company noted that while rates moderated somewhat in property and automobile lines compared to the prior quarter, momentum continues to build in general liability and umbrella lines. This selective approach to rate adequacy aligns with the company’s strategy of focusing on profitable growth.

Investment Portfolio Performance

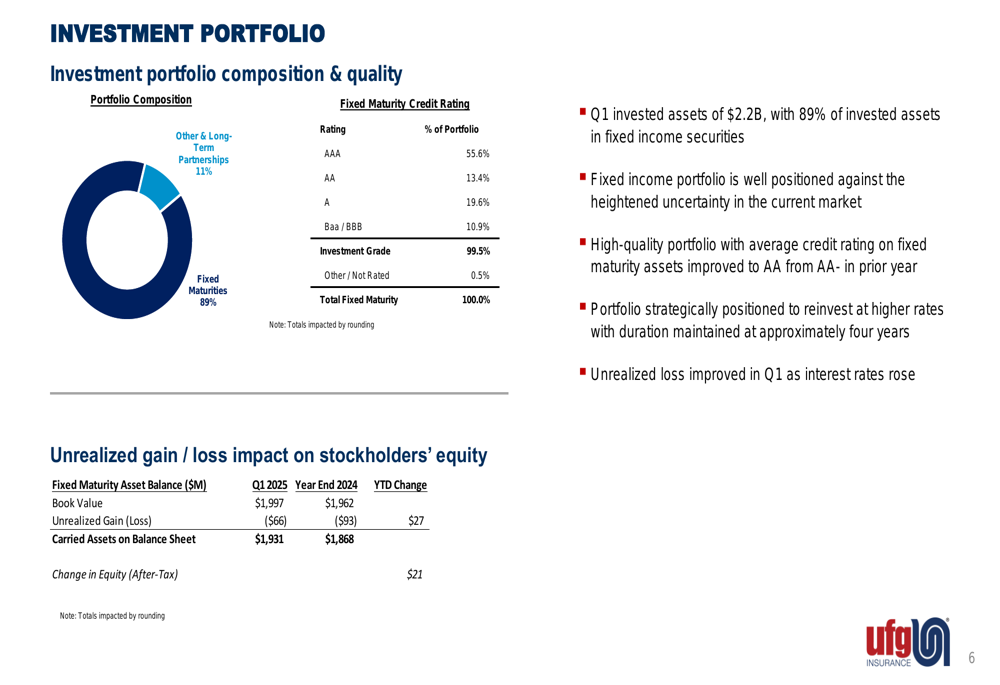

United Fire Group’s investment income was a significant contributor to its improved profitability in Q1 2025. The company’s investment portfolio composition remains conservative, with 89% allocated to fixed maturities:

The investment portfolio maintains high quality, with 99.5% of fixed maturities rated as investment grade. The average credit rating improved to AA, positioning the company well against market uncertainty.

Net investment income increased 44% to $23 million in Q1 2025 from $16 million in Q1 2024, primarily driven by higher interest rates:

Interest on fixed maturities grew 39% year-over-year to $21 million. The company reported a pre-tax yield of 3.9% and a new money yield of 5.5%, with new purchases yielding 5.3%. Other long-term investments generated $1.8 million of pre-tax income.

Forward-Looking Statements

United Fire Group appears well-positioned to continue its growth trajectory, with strong premium rates and improving investment returns. The company’s focus on underwriting discipline has resulted in an improved underlying loss ratio, though managing the expense ratio remains a priority.

The high-quality investment portfolio, with its strategic positioning to reinvest at higher rates, should continue to benefit from the current interest rate environment. The company’s book value per share stands at $32.13, providing a solid foundation for future growth.

As United Fire Group moves through 2025, investors will likely focus on the company’s ability to maintain underwriting profitability while addressing the elevated expense ratio that has persisted in recent quarters. The continued momentum in general liability and umbrella lines could provide additional opportunities for profitable growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.